Global Market Analysis

Chemical producers face stiff profit headwinds due to high costs and oversupply in 2H22 – an opportunistic setting for energy players evaluating chemical investments.

Chemical producers face stiff profit headwinds due to high costs and oversupply in 2H22 – an opportunistic setting for energy players evaluating chemical investments.

Daily Chemical Reaction Playing The Long Game – Energy Sector Capex Drives To Chemicals, Europe Tries To Get Out Of The Bunker Key Points: We

The Weekly Catalyst Global Chemical Update – Falling Down Key Points: Global polymer prices have fallen more than integrated production costs in 3Q driving sizable

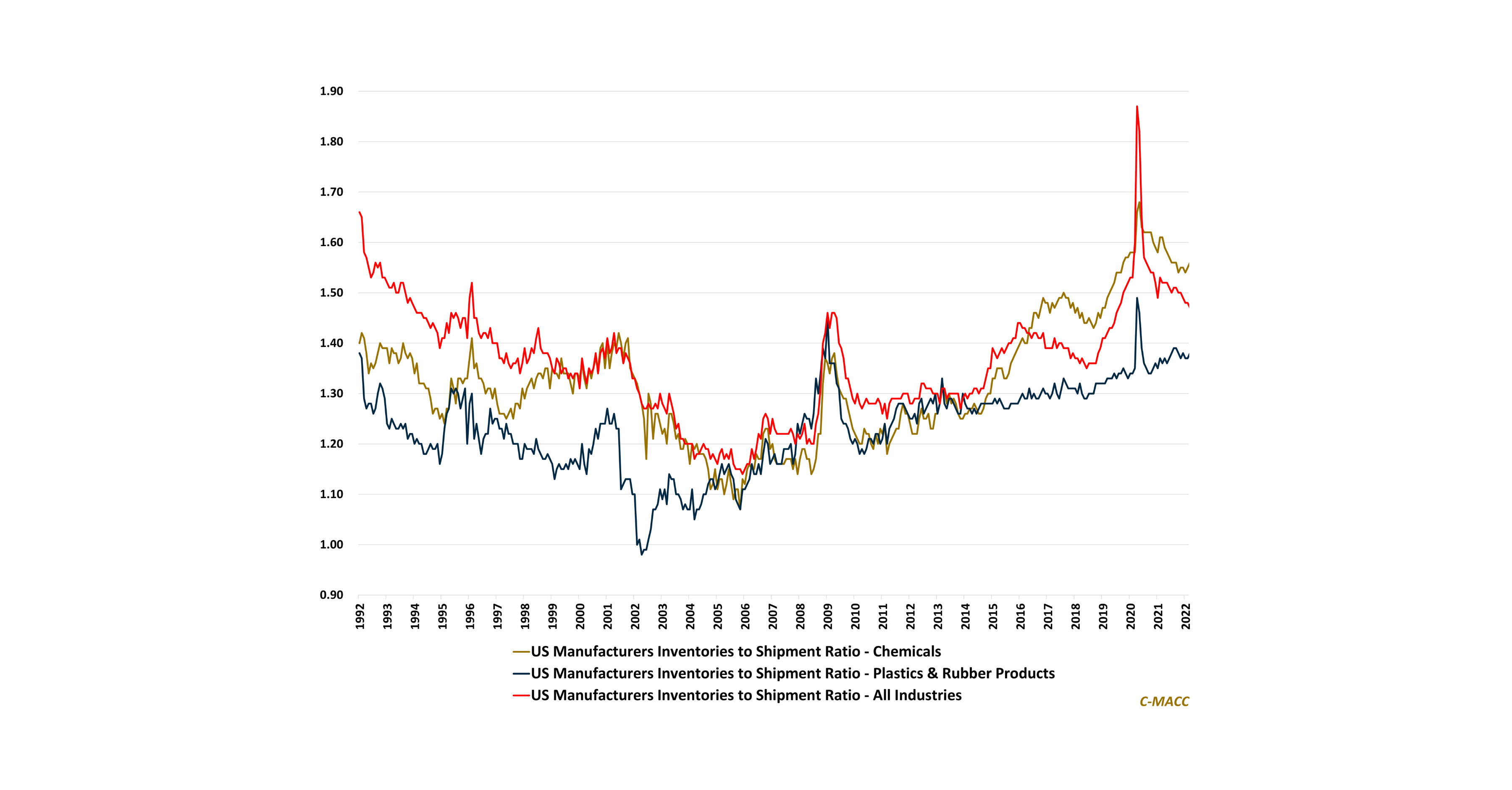

Global demand concerns, lingering logistic issues, and elevated inventory levels are spurring US chemical production cuts despite its shrinking but still notable low-cost global position.

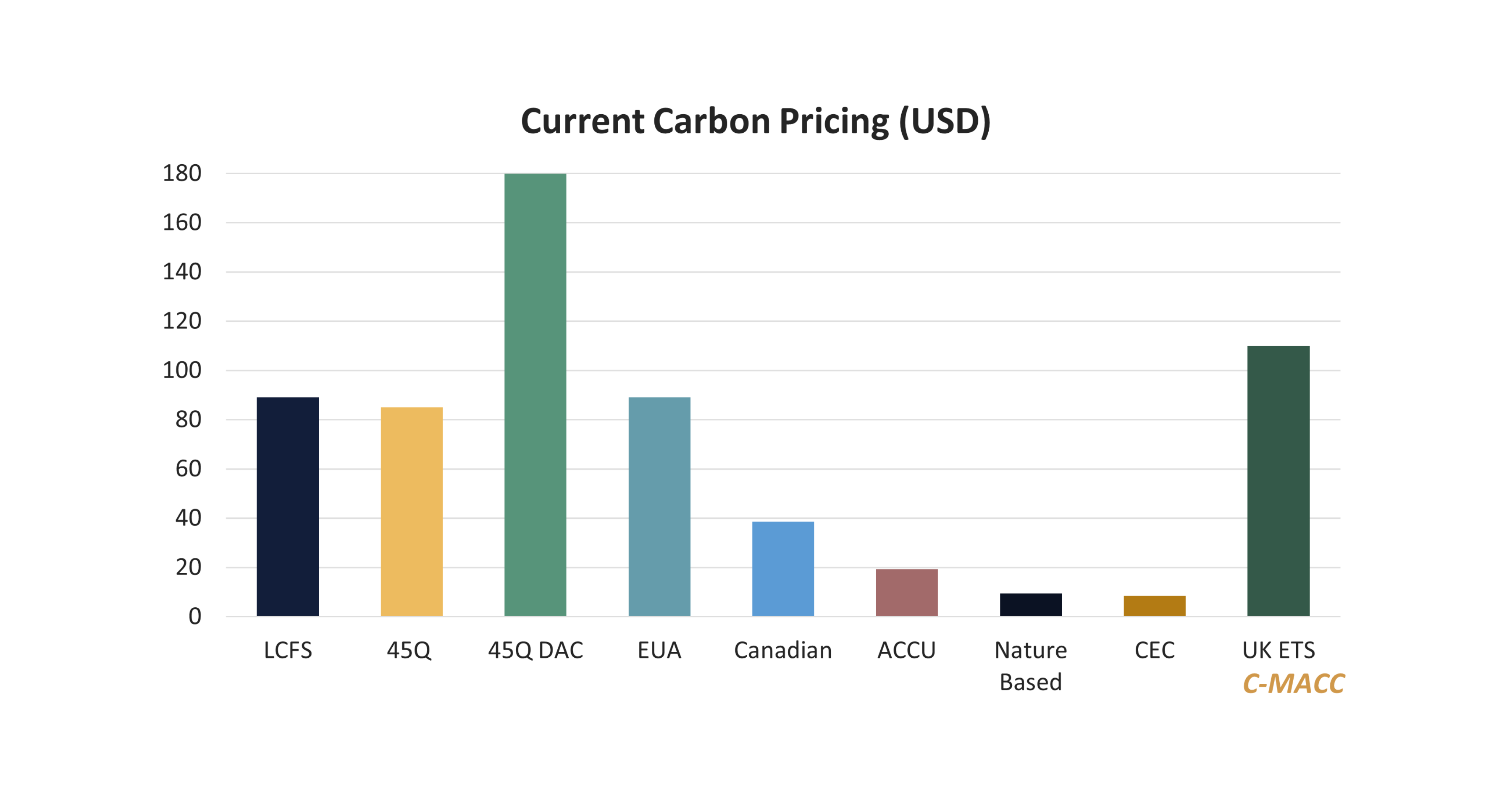

As carbon prices/costs rise globally, we anticipate a significant increase in investment to reduce emissions or capture them, especially in the US.

The 45Q

Higher production costs, ranging from petrochemicals to crops, favor higher prices and lower margins in many product chains. The C-MACC team shares its market views

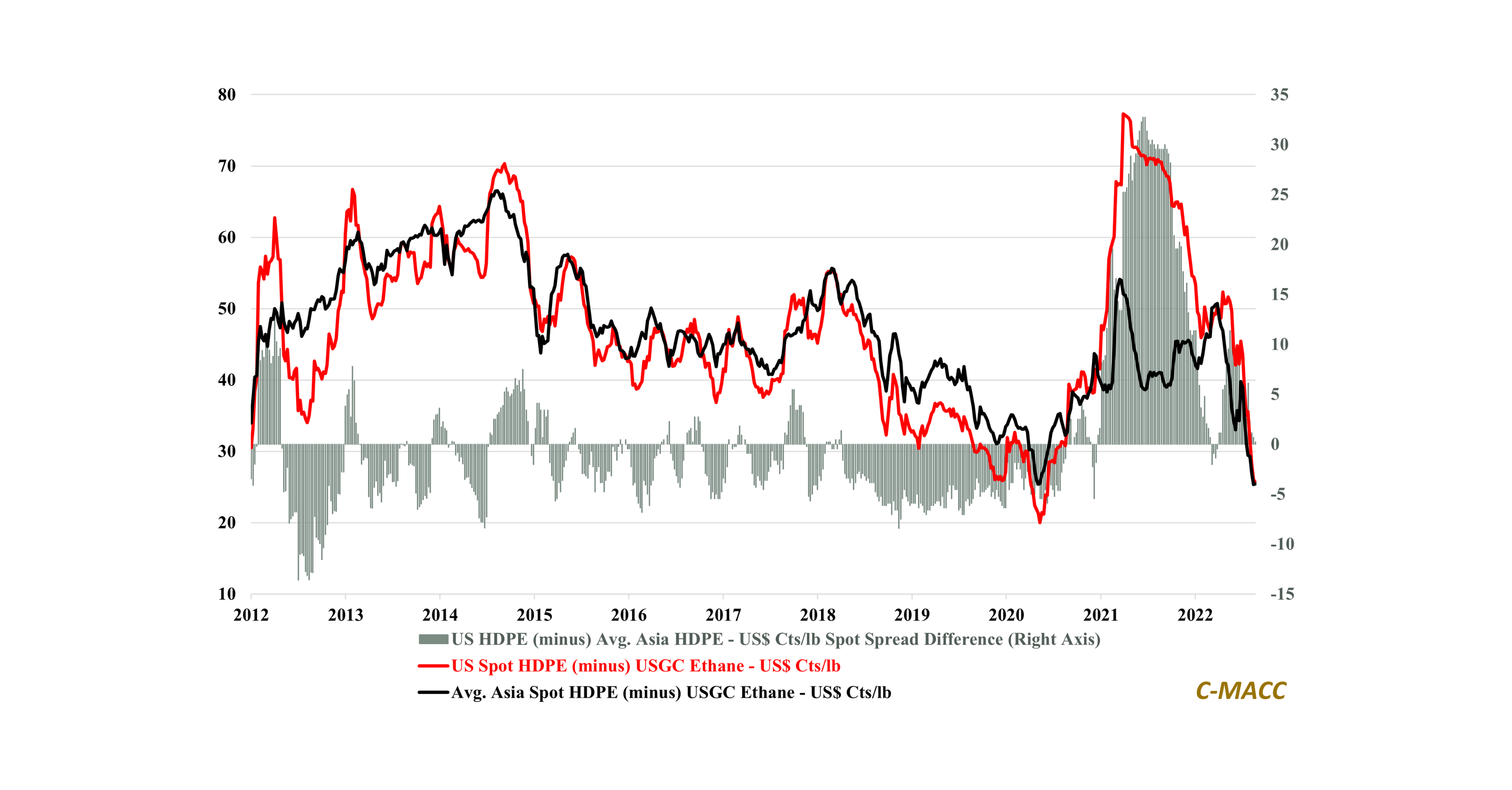

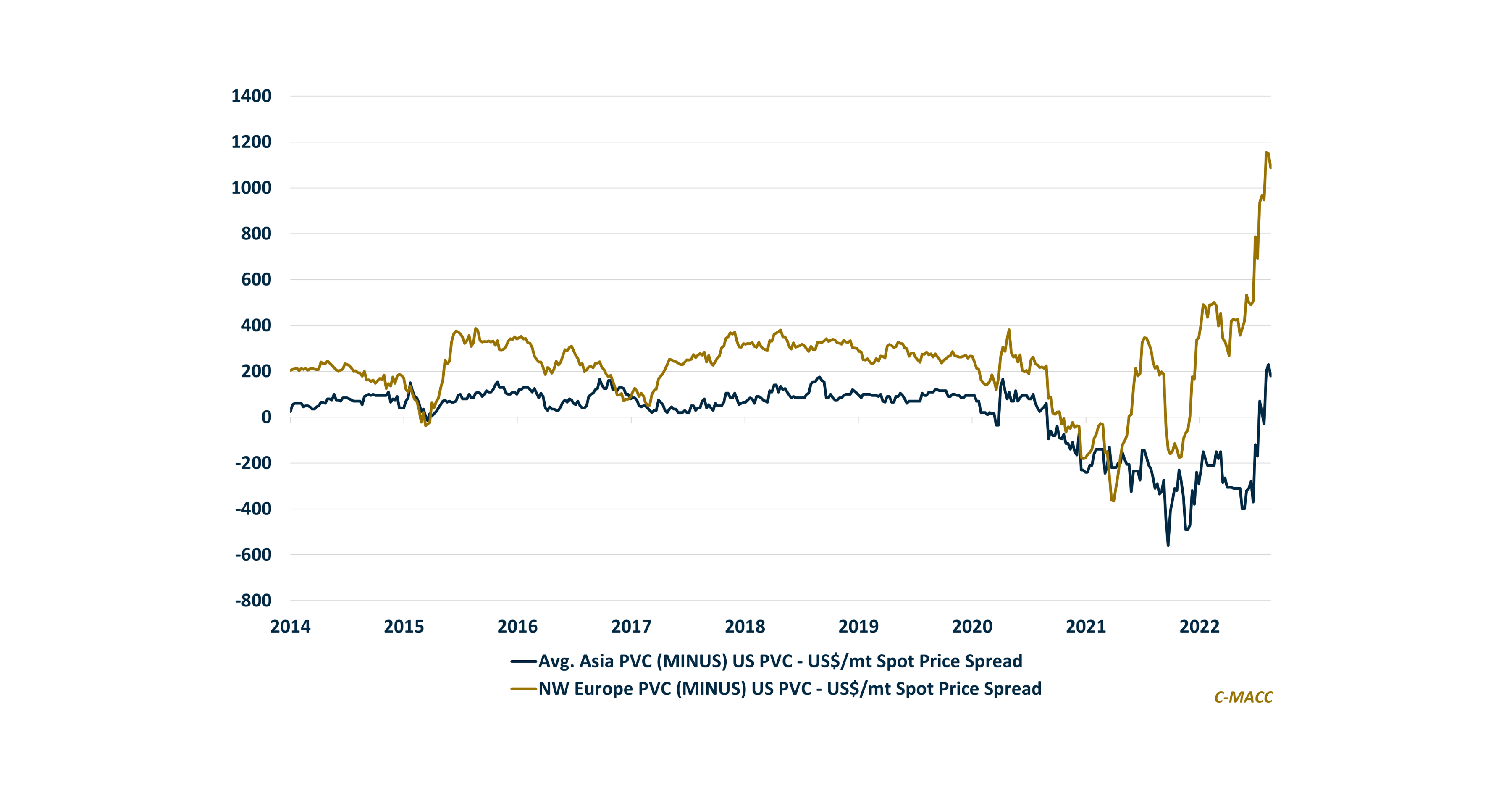

US integrated polymer producers face falling prices and higher costs in 2H22. We discuss the collapse in US PVC prices (and margins) and why our

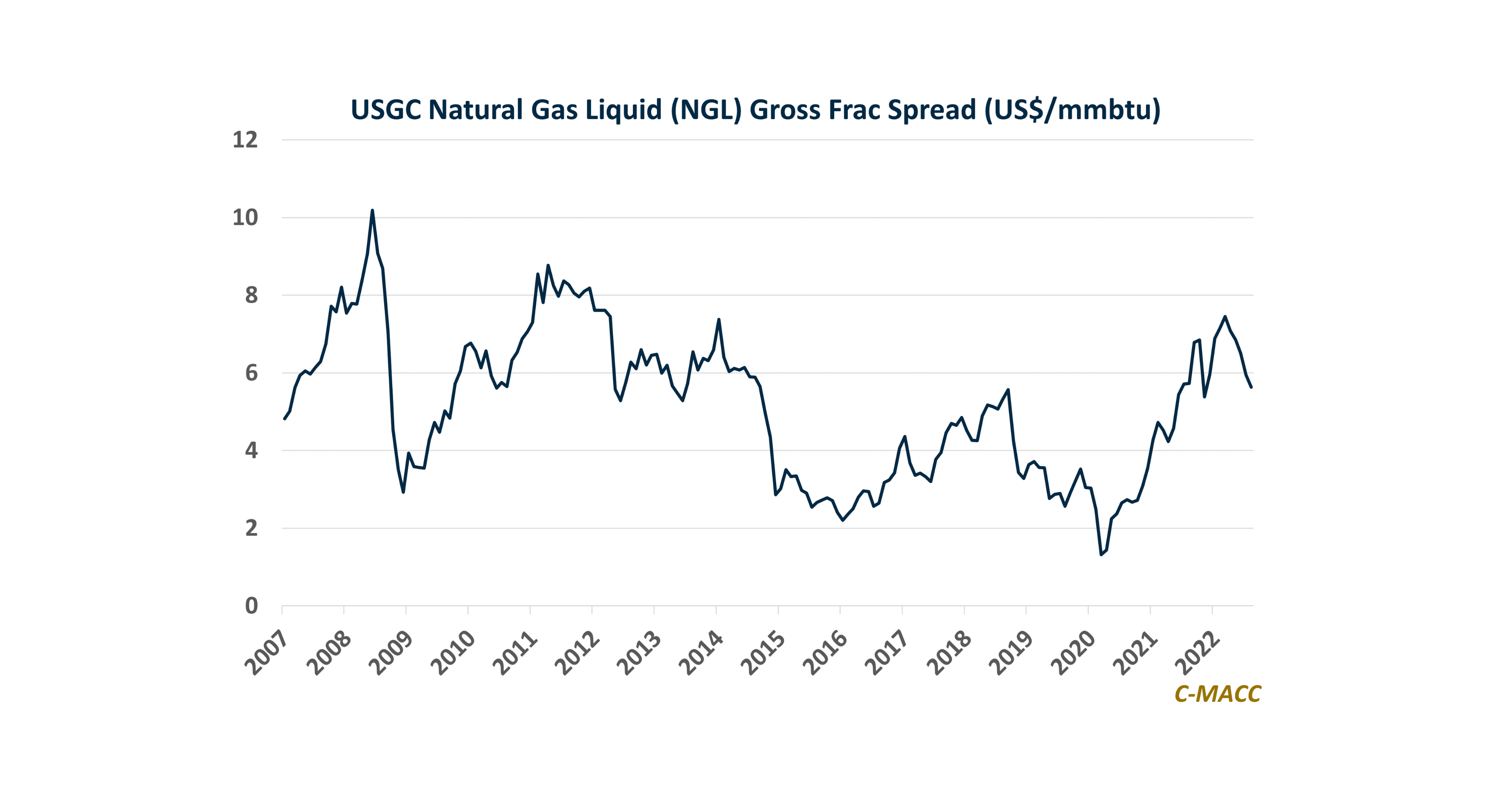

US chemical inventories remain elevated, but logistic and cost issues abroad favor exports, such as in PVC, which will help support US prices as inventories

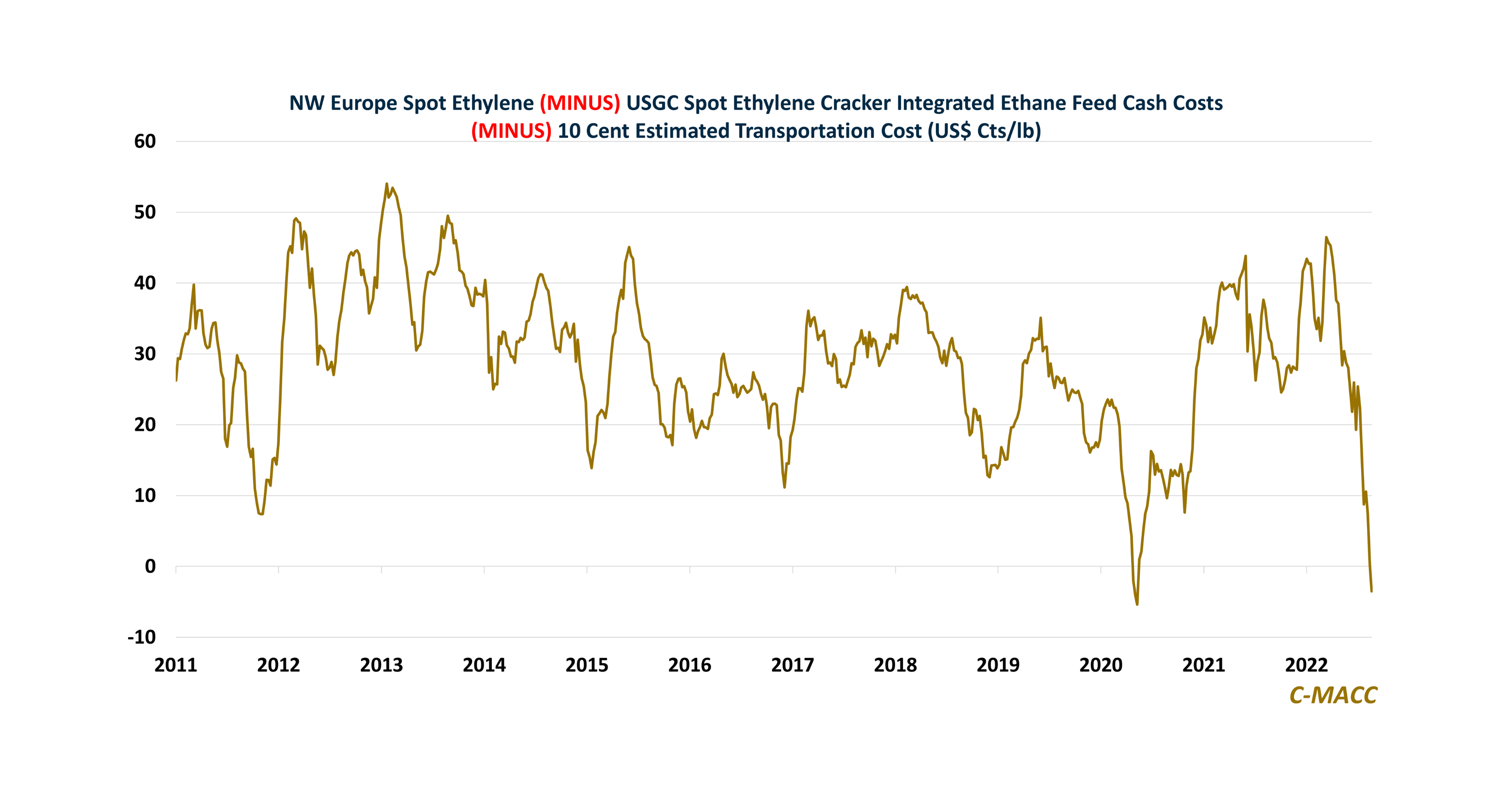

European chemical producers are not responding to high downstream prices due to logistic challenges and high net production costs – this development favors imports. <br

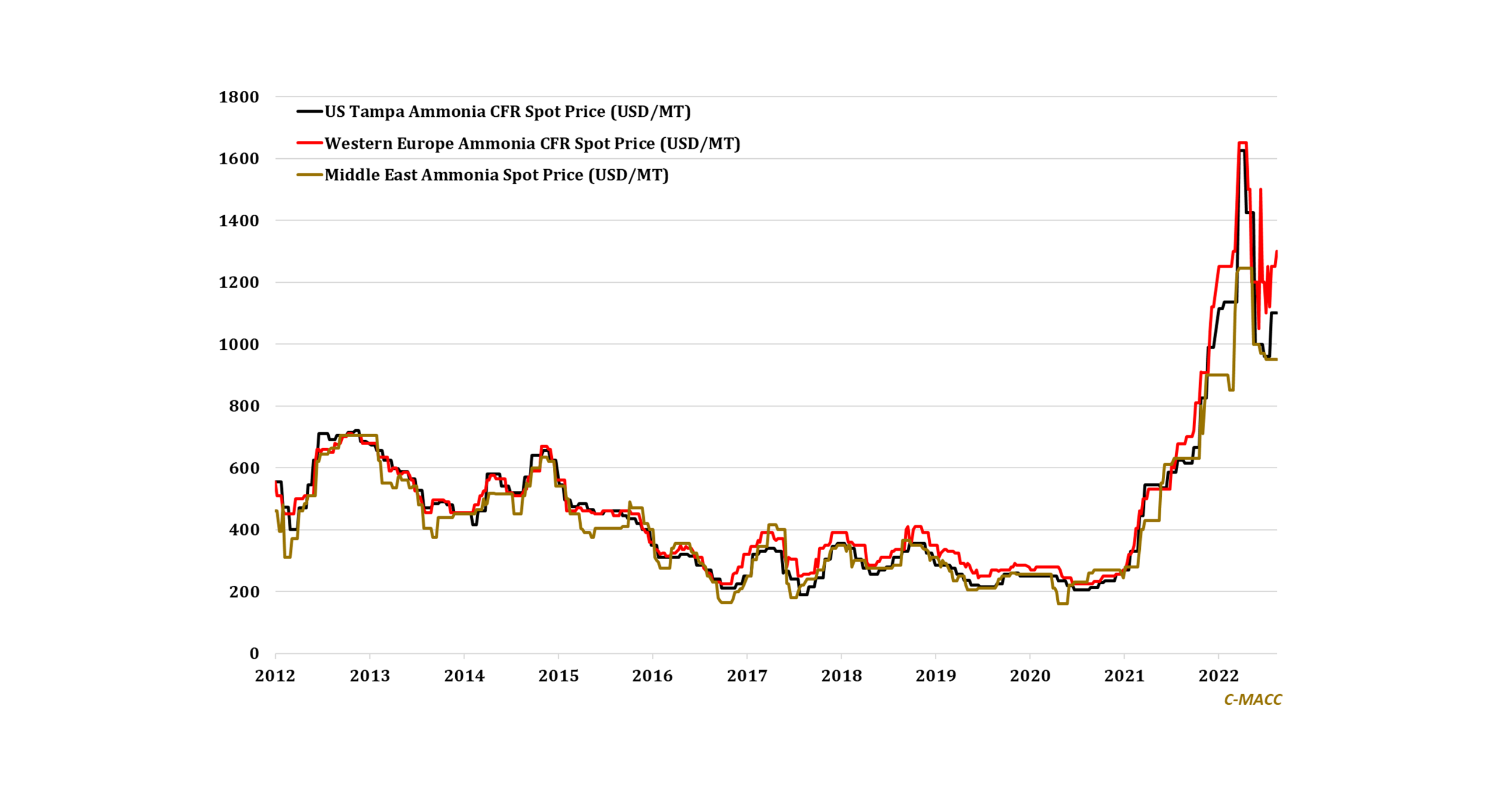

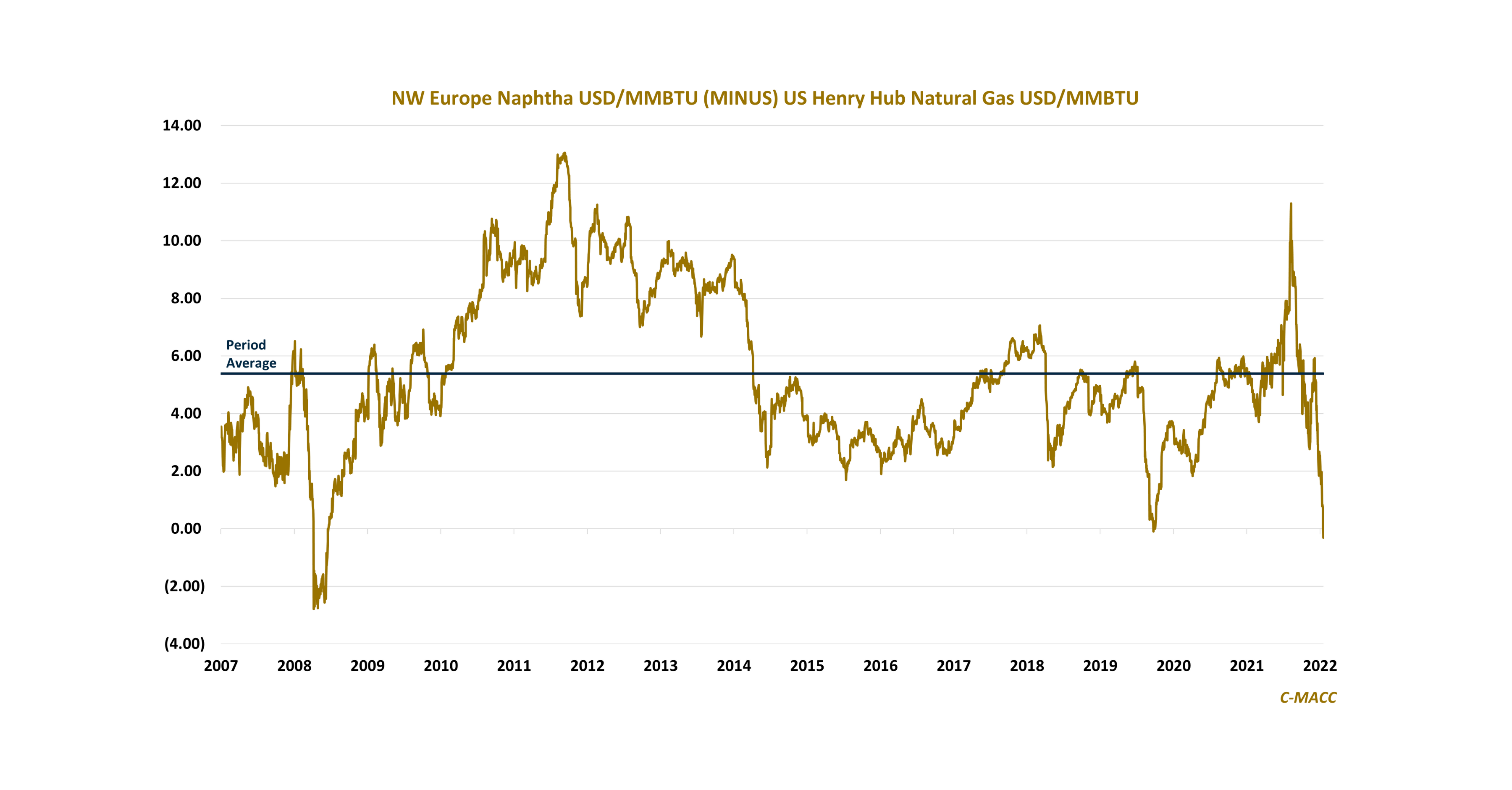

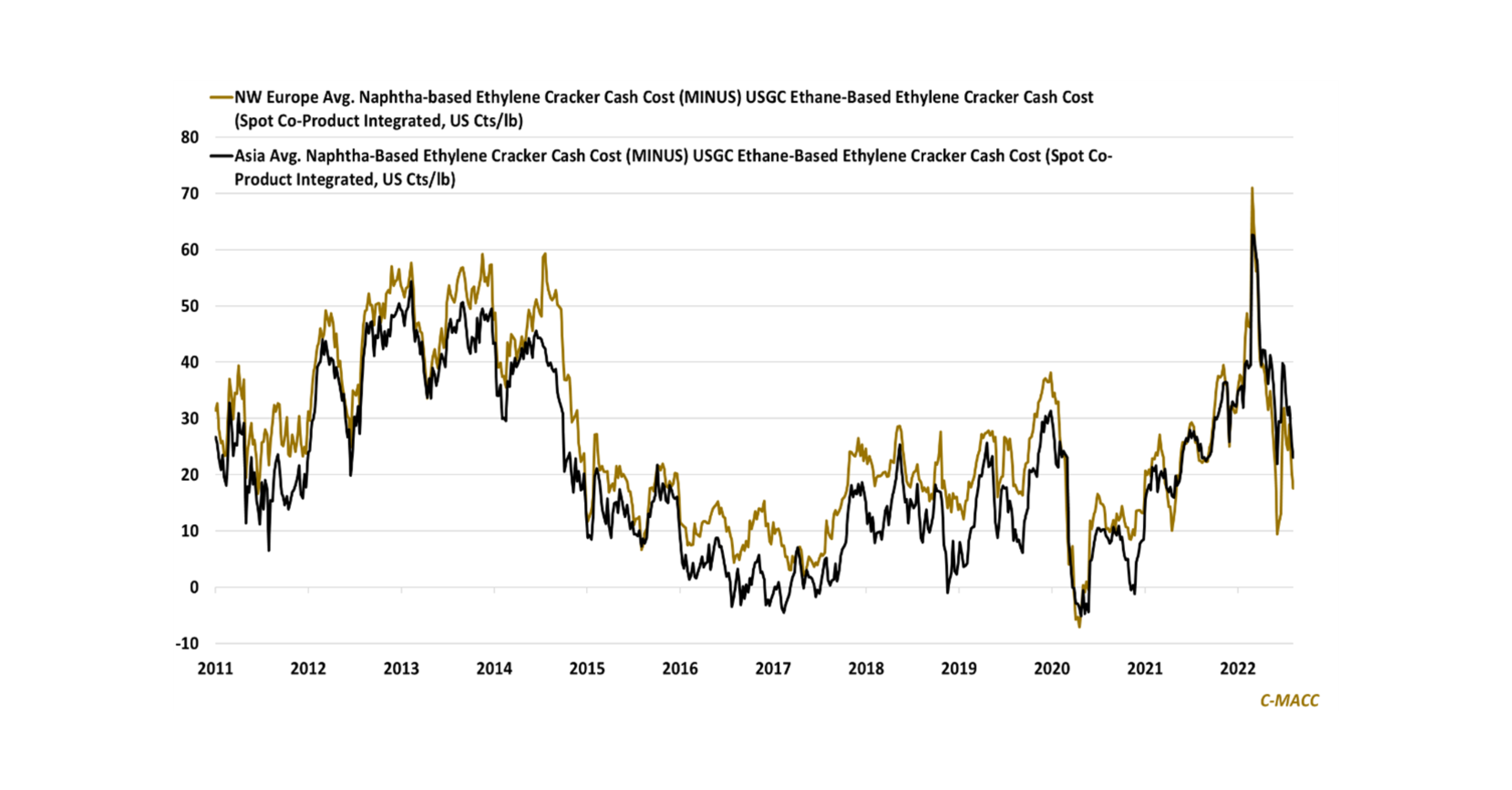

The global petrochemical production cost curve favors US producers, but lower prices and higher costs to still drive margin compression for most in 2H22.