Global Weekly Catalyst No. 343

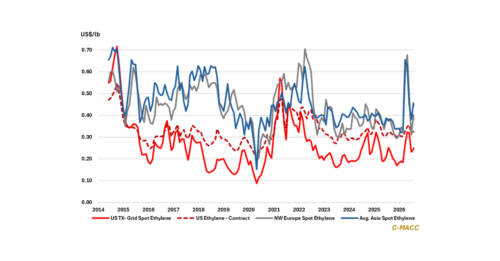

General Thoughts: Headline price relief is arriving faster than market balances are resetting, allowing competitive advantages to persist and making regional operating conditions more influential

General Thoughts: Headline price relief is arriving faster than market balances are resetting, allowing competitive advantages to persist and making regional operating conditions more influential

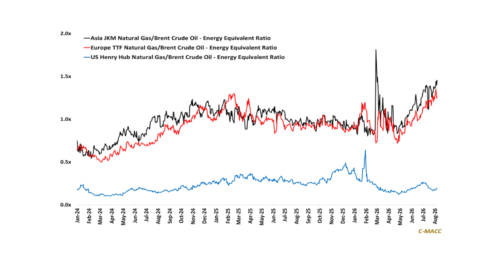

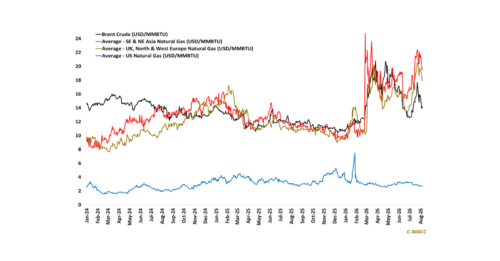

Crude oil can regain physical flexibility faster than LNG, allowing international gas premiums and selected North American feedstock advantages to persist even as headline energy

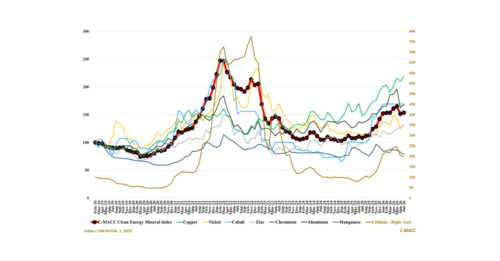

1st Topic of the Week: C-MACC Clean Energy Mineral Index recovered in July, but diverging supply responses leave copper better supported and lithium more exposed

General Thoughts: Recent crude relief is narrowing oil-linked costs faster than gas-linked economics, preserving North America’s ammonia and methanol advantage as energy markets normalize unevenly.