Global Market Analysis

The considerable downward pressure on global lithium prices YTD will likely push the C-MACC critical mineral index for April lower MoM, though its other components

The considerable downward pressure on global lithium prices YTD will likely push the C-MACC critical mineral index for April lower MoM, though its other components

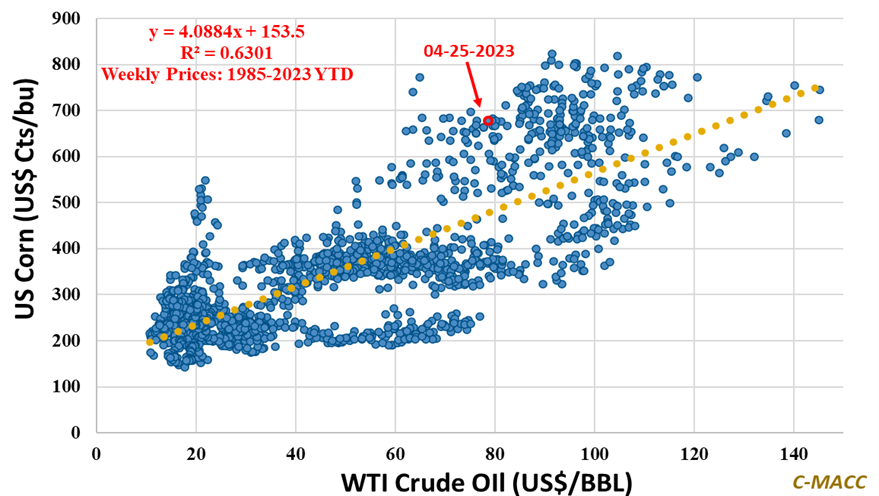

Using bio-based inputs, such as corn, in fuels and materials can cost more than conventional methods, lack scalability, and not be inherently green considering the

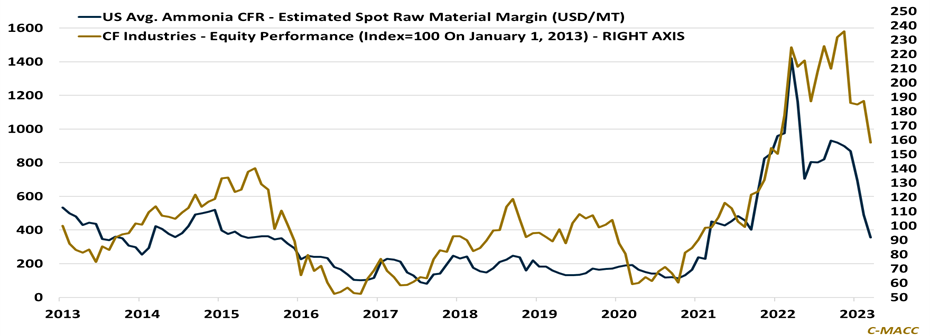

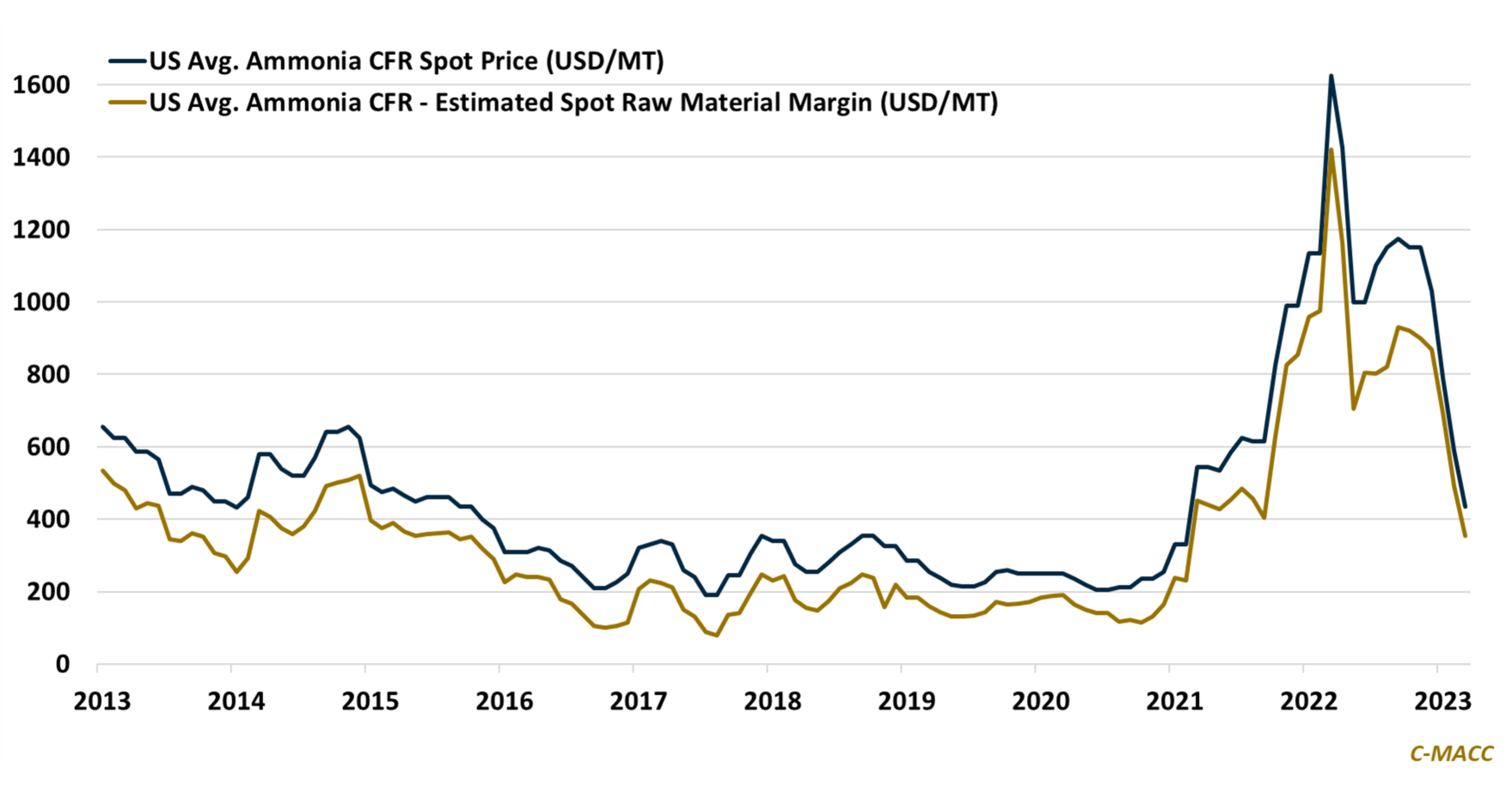

North American ammonia and methanol margins have contracted YTD, putting downward pressure on producer equities, though we see the medium-term potential for much tighter markets

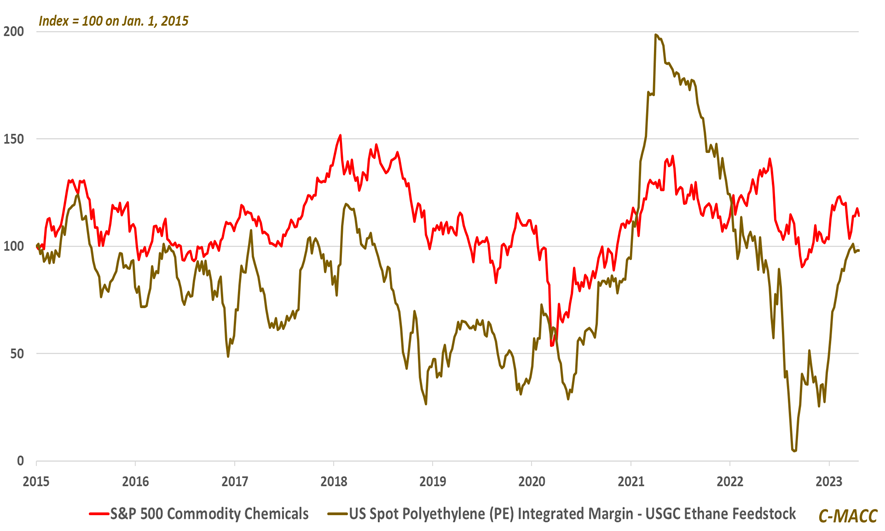

Falling production costs and higher prices favored the US commodity chemical sector in 1Q, beating most estimates – we see more potential to disappoint than

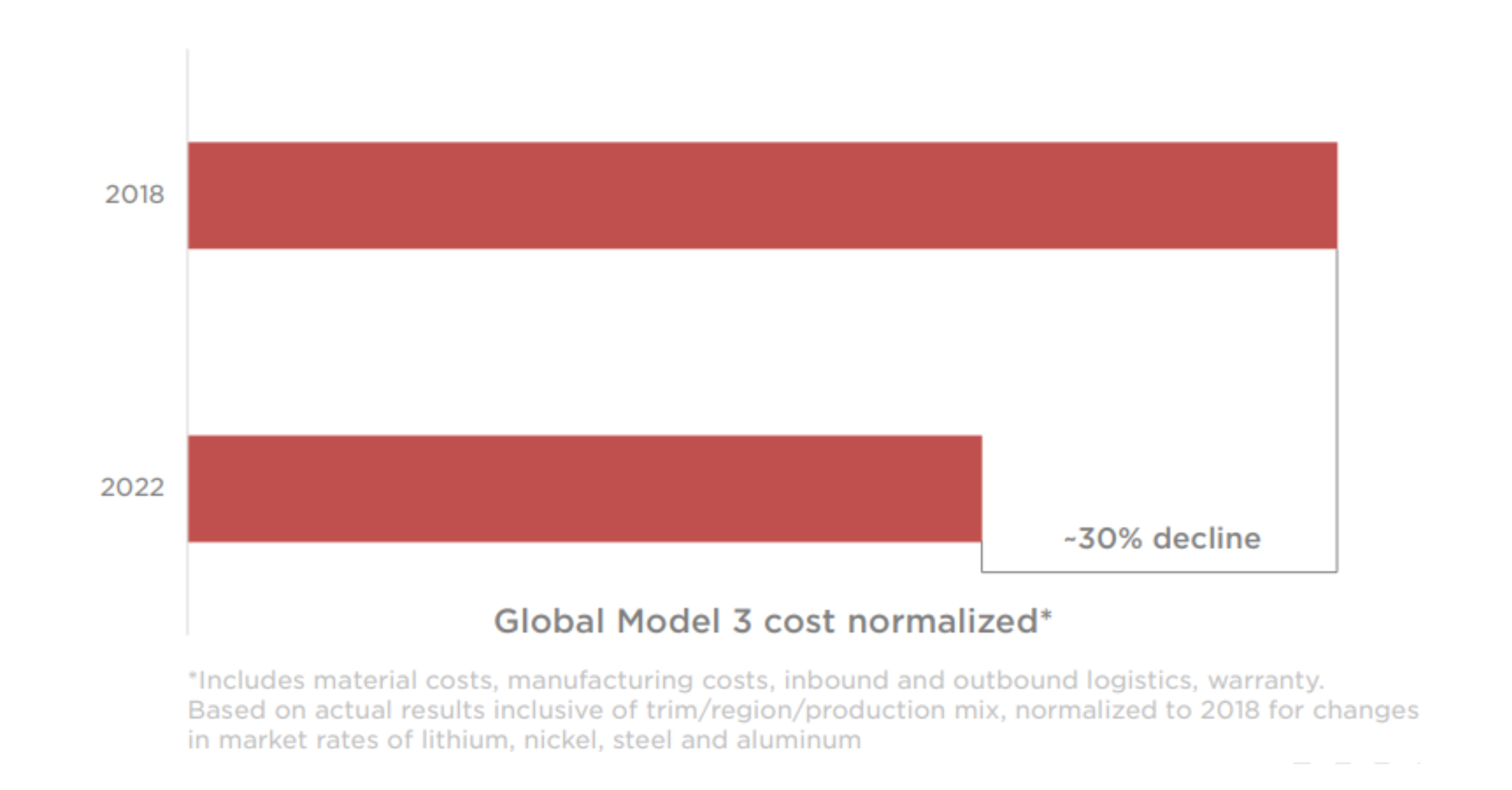

Tesla cuts prices to spur demand, signaling a willingness to cut margins for market share. We foresee a rising EV industry focus on costs becoming

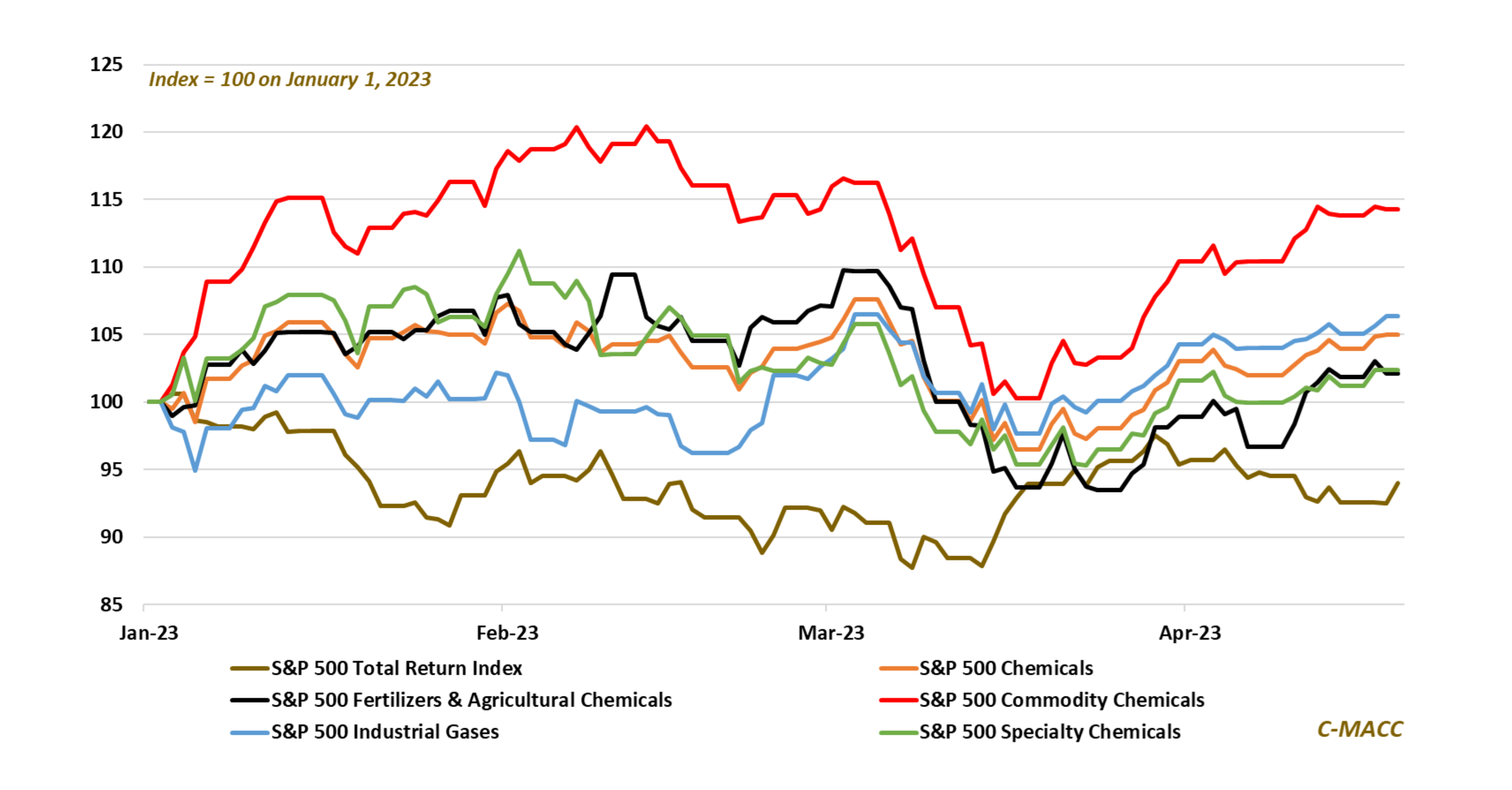

US chemical sector equities markedly outperformed the market YTD. Specialties have notably underperformed the commodity sector, and we discuss why this trend could reverse in

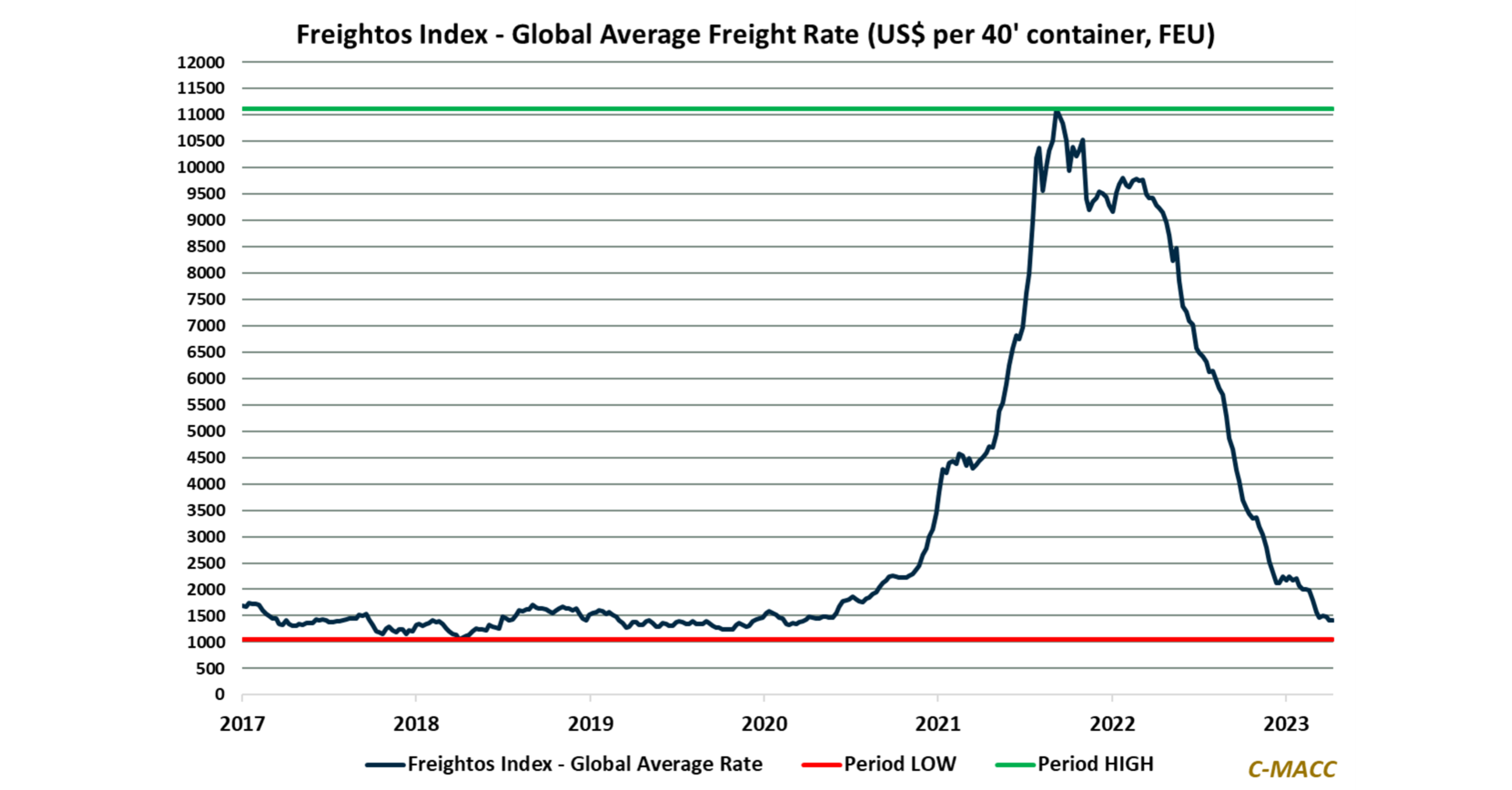

Global freight rates reflect downward pressure in 1H23, supporting the case for supply chain improvements and suggesting reduced commodity price differentials between regions in 2023.

North American ammonia and methanol spot prices have decreased YTD. We think recent margin pressure will work to delay capacity expansions, setting up a period

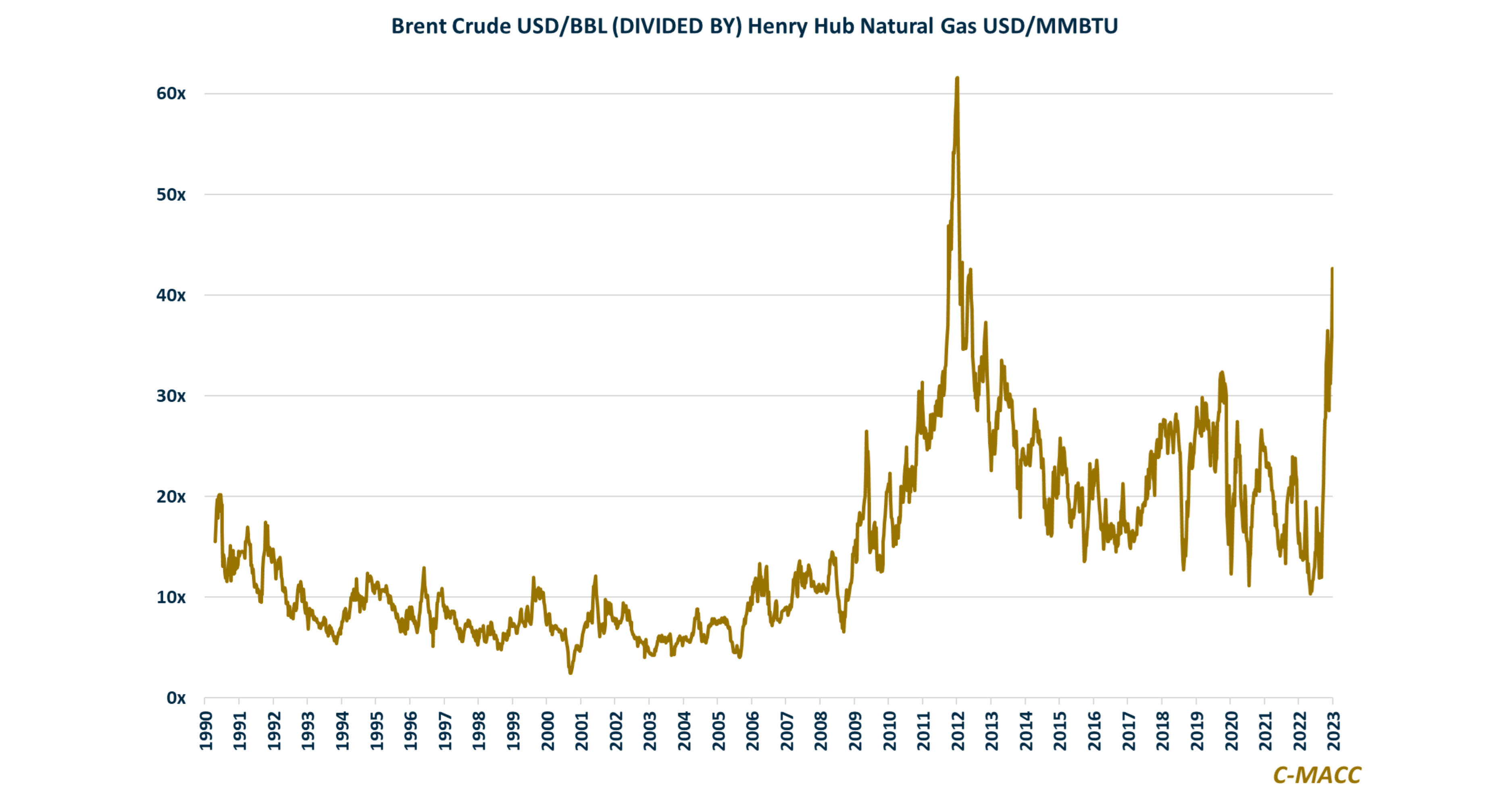

Global feedstock costs shift further WoW in favor North American chemical producers relative to Asia and Europe, curbing but not erasing profit downside risk into

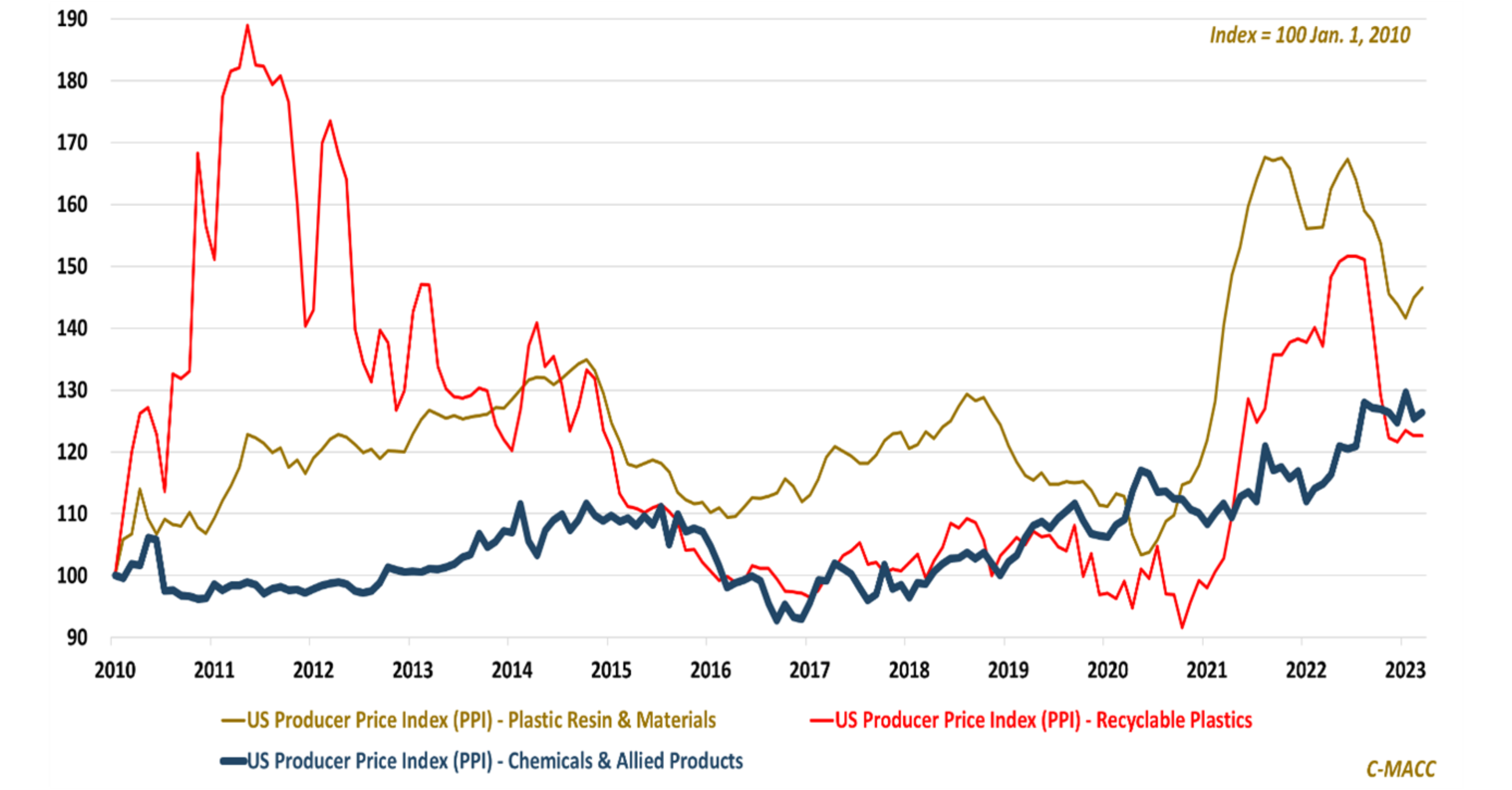

The PPI for plastic resin & materials rose MoM in March on an absolute basis and relative to the recyclable resin index – more of