Polymer Global Analysis

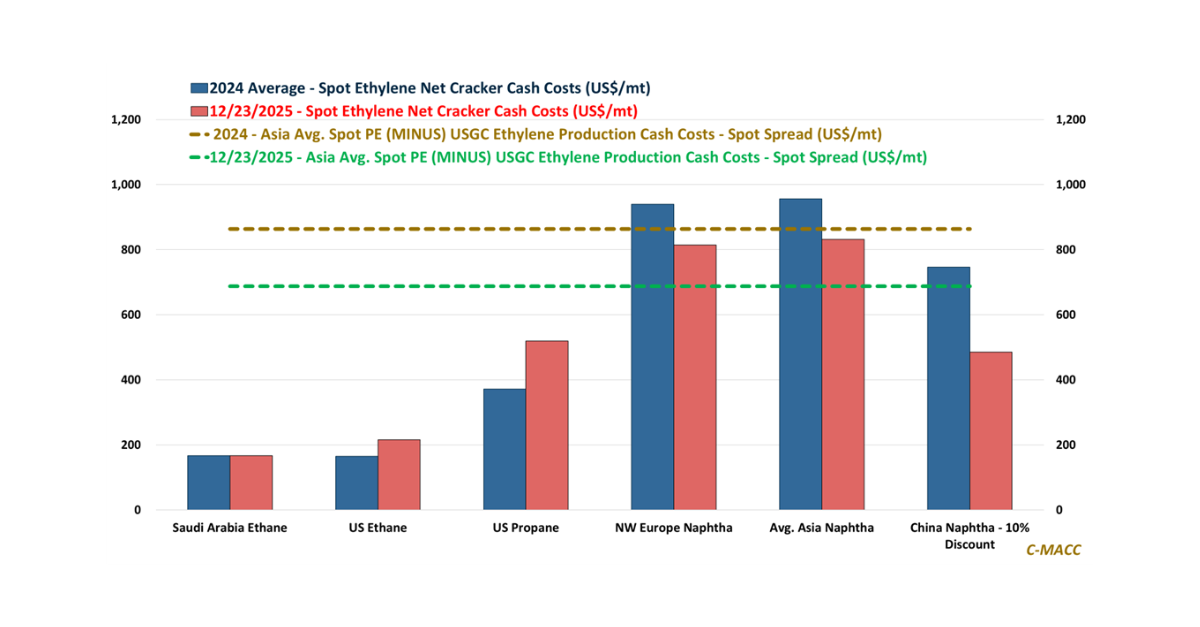

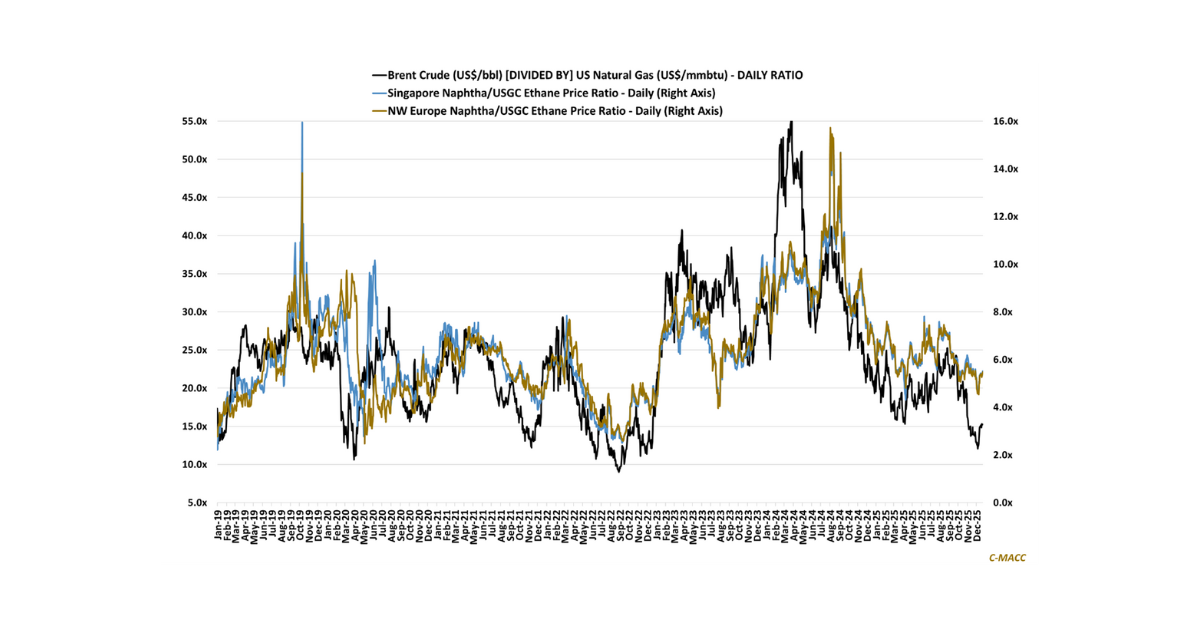

General Thoughts: Global polymer markets continue to clear tactically, not cyclically, in late 2025 as oversupply, logistics normalization, and discipline overwhelm demand signals, leaving price

General Thoughts: Global polymer markets continue to clear tactically, not cyclically, in late 2025 as oversupply, logistics normalization, and discipline overwhelm demand signals, leaving price

General Thoughts: Depressed global chemical sector growth expectations, co-product erosion, and flattened cost curves make restructuring pace and margin resilience more decisive than demand recovery

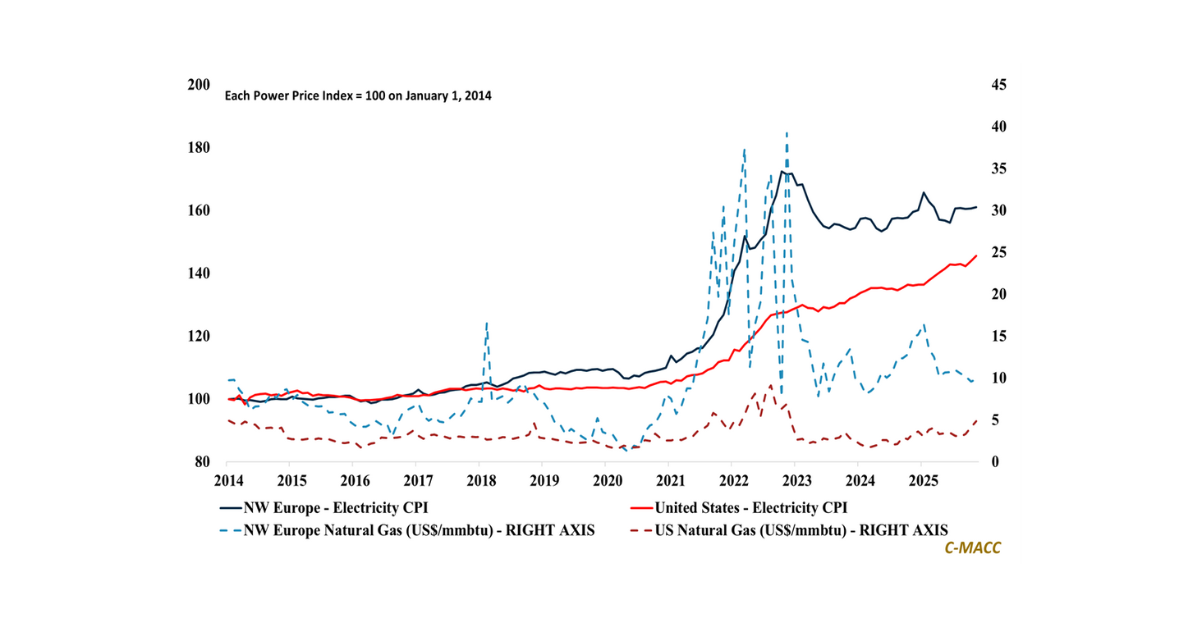

Chemical sector outcomes in 2026 will hinge more on managing volatility across power, gas, and policy, not on forecasting averages, as infrastructure constraints and capital

Polypropylene – December Monthly Price Expectation Report

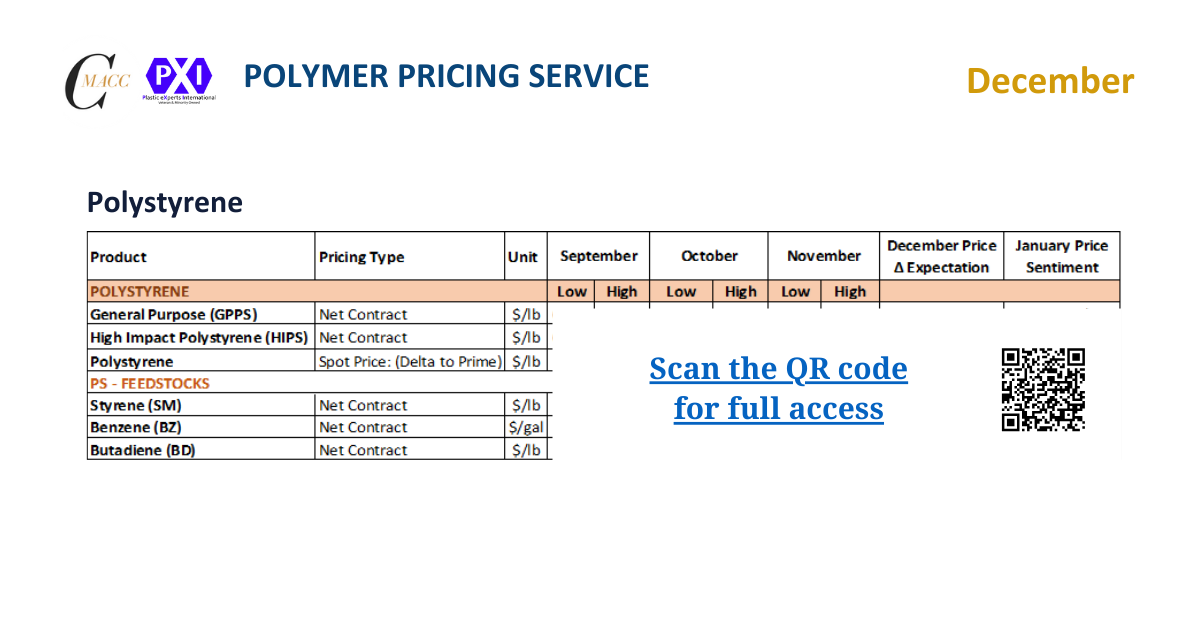

Polystyrene – December Monthly Price Expectation Report

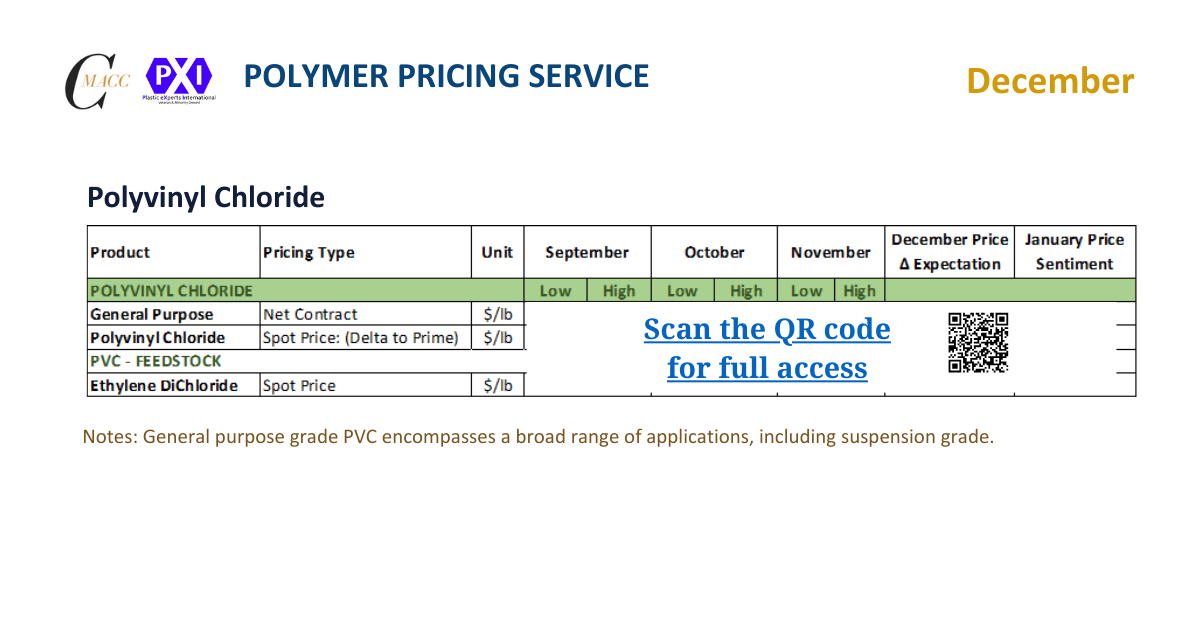

Polyvinyl Chloride – December Monthly Price Expectation Report

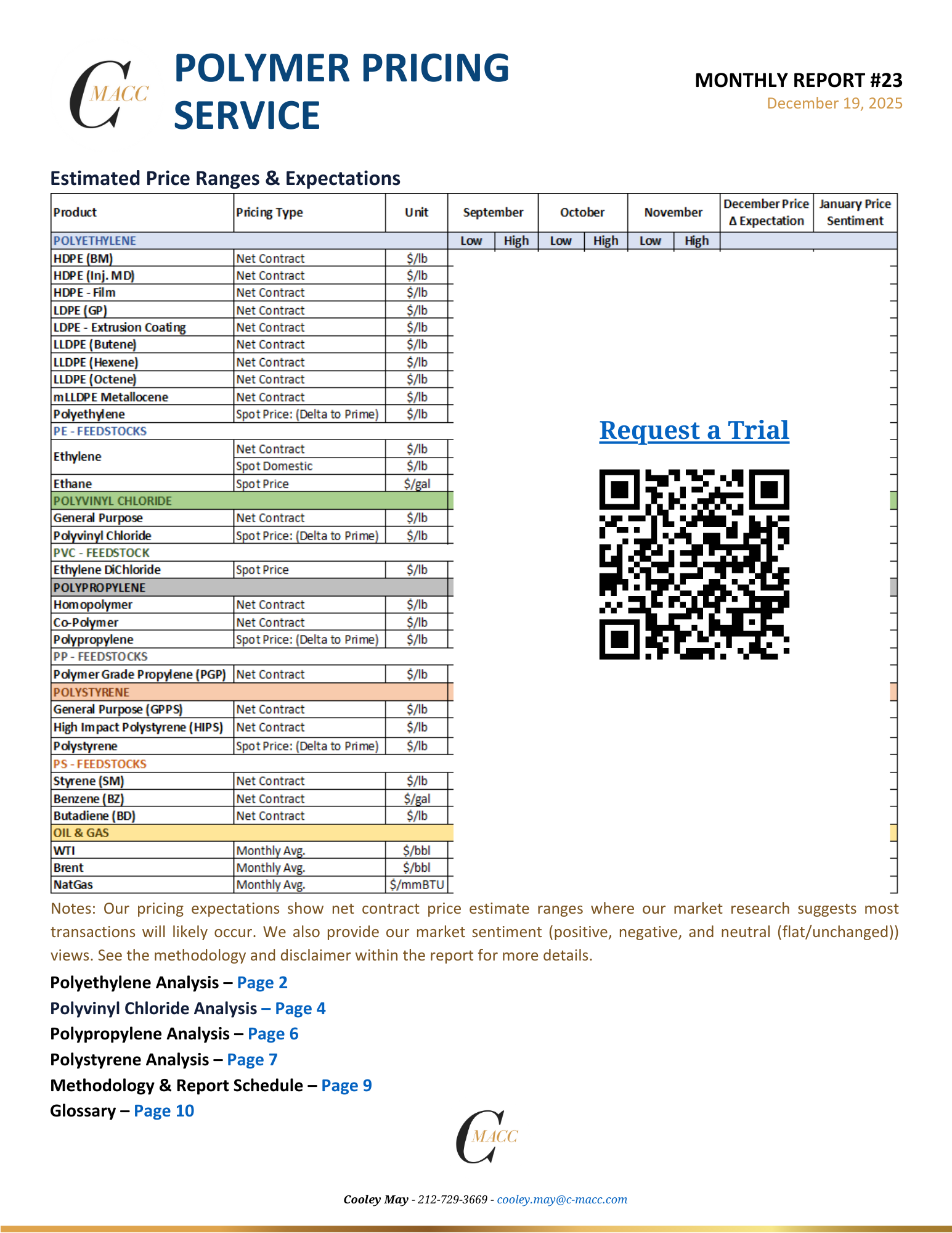

Polymer Price Expectations – Monthly Report # 23

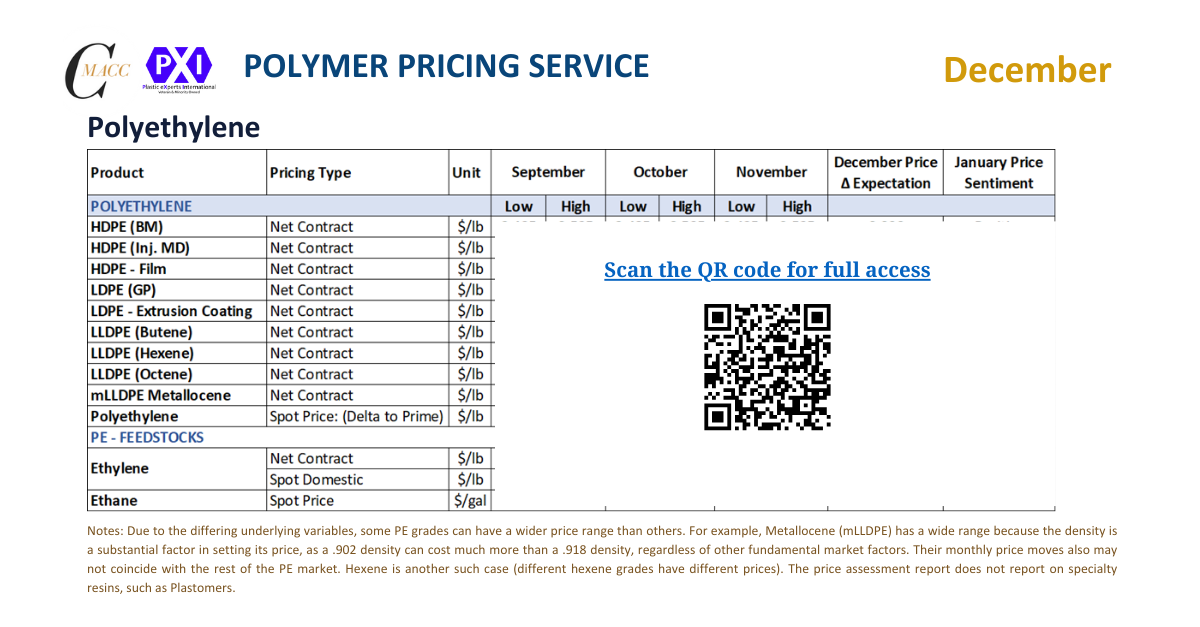

Polyethylene – December Monthly Price Expectation Report

1st Topic of the Week: If verified product-level sustainability increasingly decides access and win rates, which chemical and polymer producers gain pricing power, and which

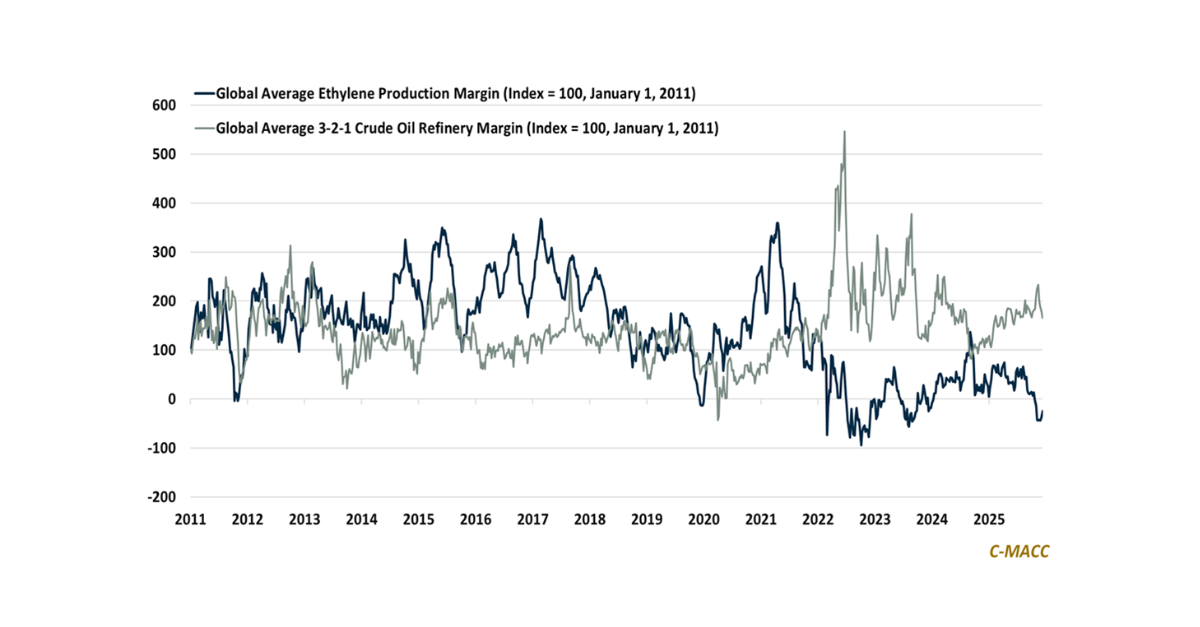

General Thoughts: Global average ethylene production margins collapsed in early 4Q25 then stabilized modestly, but only restructuring like high-cost cracker closures can loosely replicate refining’s