Global Weekly Catalyst No. 337

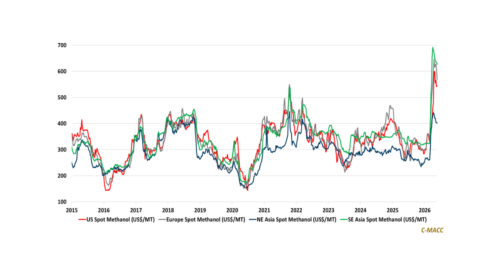

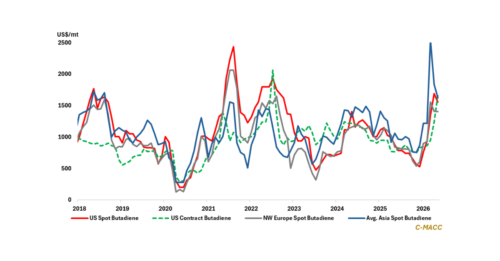

General Thoughts: Market indicators near early-year levels do not mean risks have reset; lower ex-US production costs and working capital positions test routes, timing, and customer urgency as supply returns against weak demand.

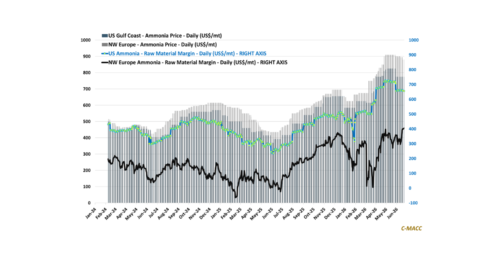

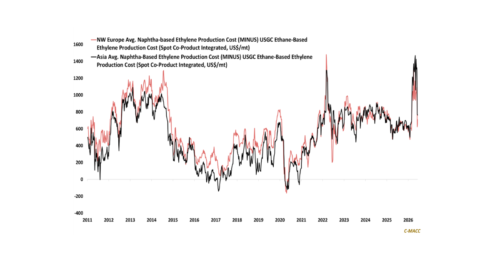

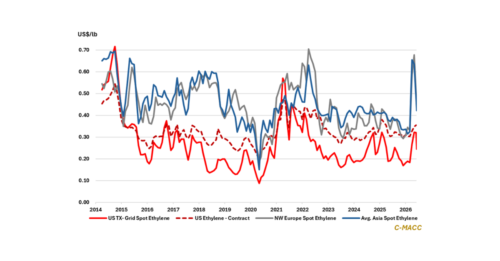

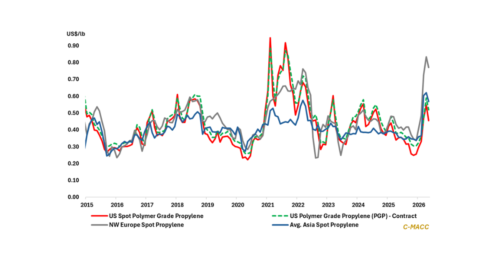

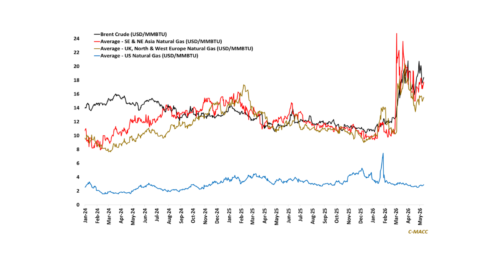

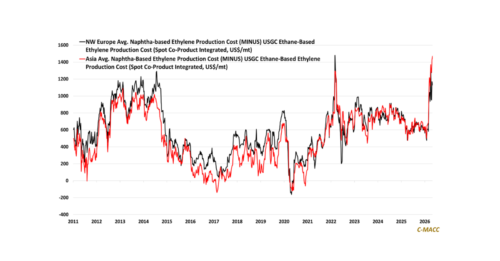

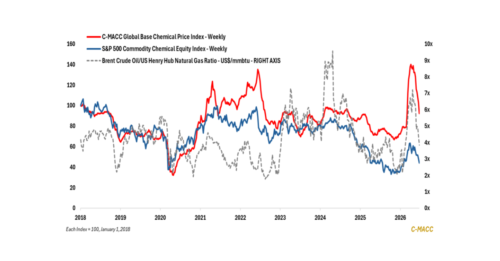

Feedstocks & Energy: Oil-linked feedstock relief and ex-US natural gas declines have flattened global chemical cost curves,