Easy Come, Uneasy Go: Cost Relief, Rewards Split

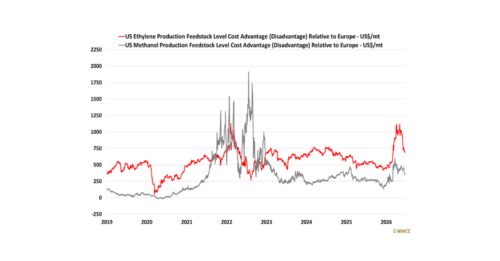

General Thoughts: The US feedstock advantage has eased from shock peaks, but Europe and Asia ex-China remain exposed, with naphtha and gas costs still limiting derivative recovery and trade flexibility.

Supply Chain/Commodities: Methanol tightness is sustaining premium value for North American supply in Western markets, as buyers need non-Middle East