Global Market Analysis

General Thoughts: Industrial value is shifting toward integrated systems that manage energy, logistics, and continuity to protect margins, as disruption fragments markets and limits standalone

General Thoughts: Industrial value is shifting toward integrated systems that manage energy, logistics, and continuity to protect margins, as disruption fragments markets and limits standalone

General Thoughts: Feedstock inflation is shifting profit pools upstream, forcing buyers to absorb volatility as reliability overtakes price and accelerates alternative supply in procurement decisions.

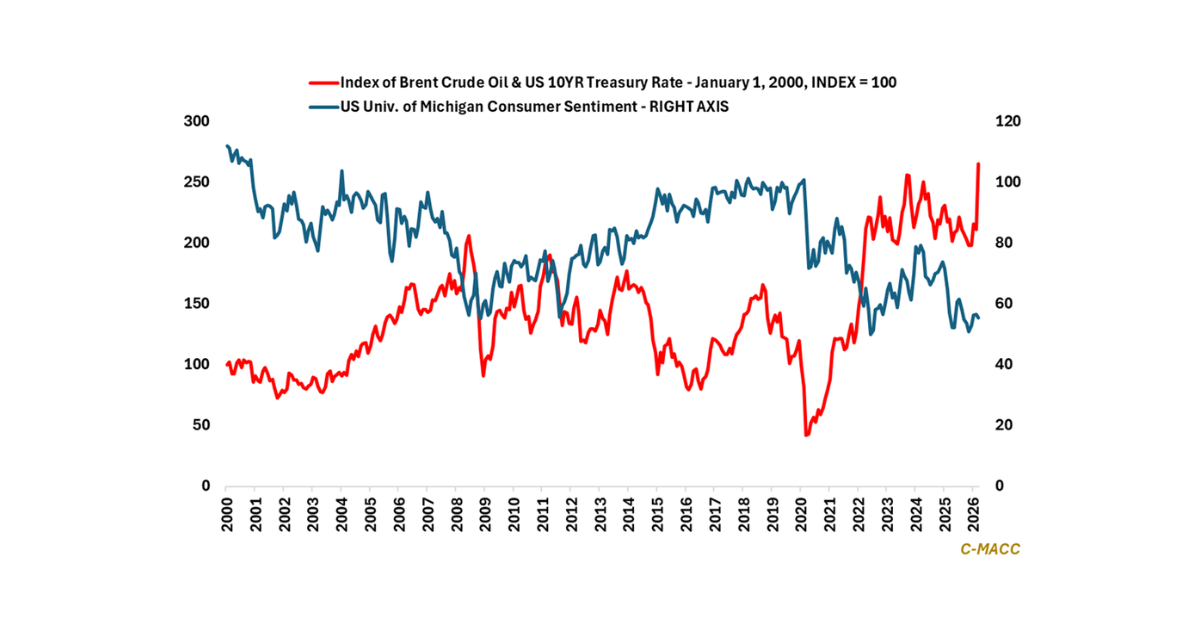

General Thoughts: Rising input costs are exposing margin fragility across industries, shifting advantage to pricing power, as policy-driven demand hopes build to offset war-driven inflation

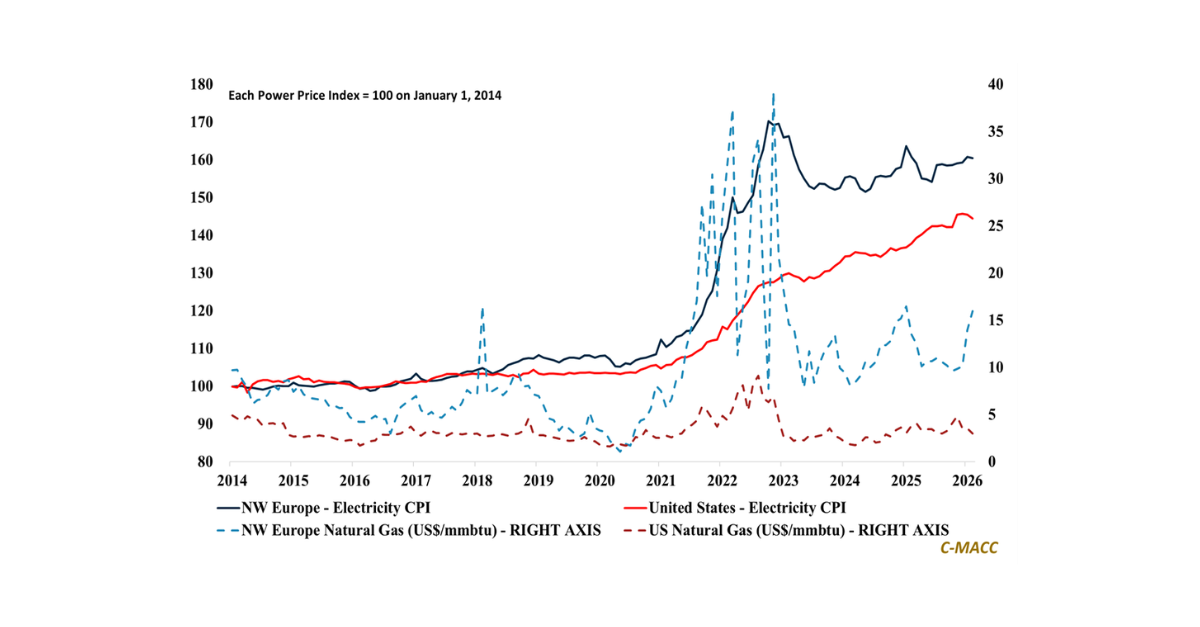

General Thoughts: Power markets increasingly show delivery timing and capacity access, not fuel direction, set prices, as constraints and rising capital requirements shape regional and

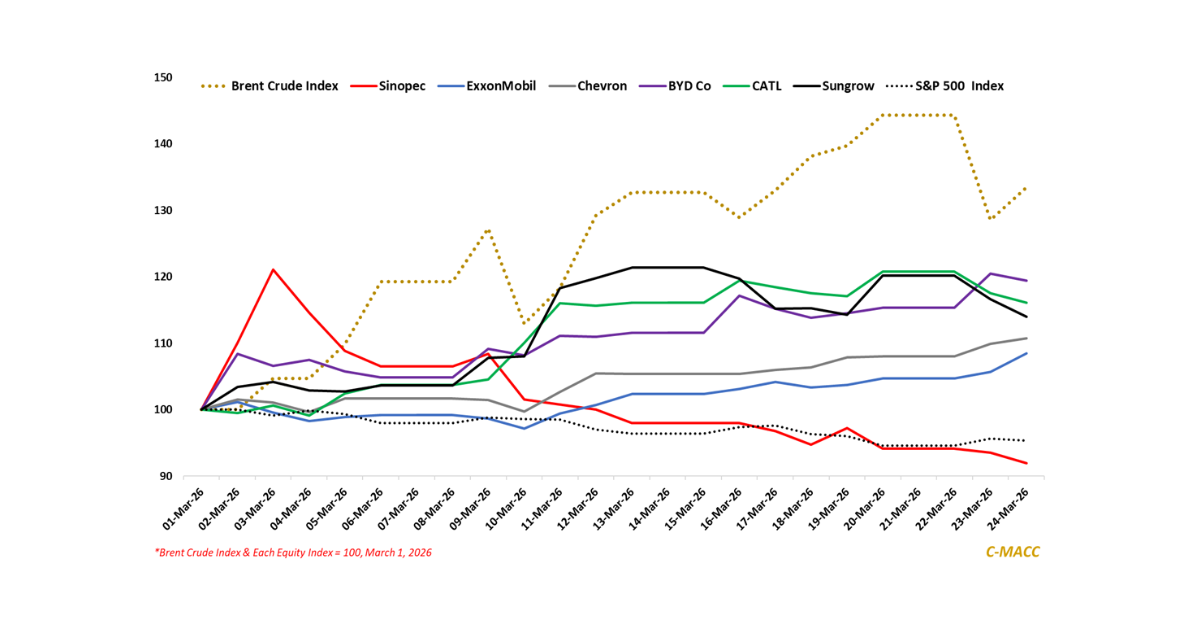

General Thoughts: Supply shocks are shifting power from cost to control, concentrating value in integrated systems as export-driven convergence reshapes demand, margins, and capital allocation

General Thoughts: Energy security is reshaping value chains, driving a bifurcation in which capital concentrates in low-cost hydrocarbons and in electrification, compressing high-cost industrial systems.

General Thoughts: Escalating Middle East disruption scale is reducing system flexibility faster than it can be restored, shifting pricing power, capital allocation, and competitive positioning

General Thoughts: Rising energy costs and elevated interest rates are compressing consumer sentiment, shifting risk from inputs toward demand, and constraining earnings visibility across global

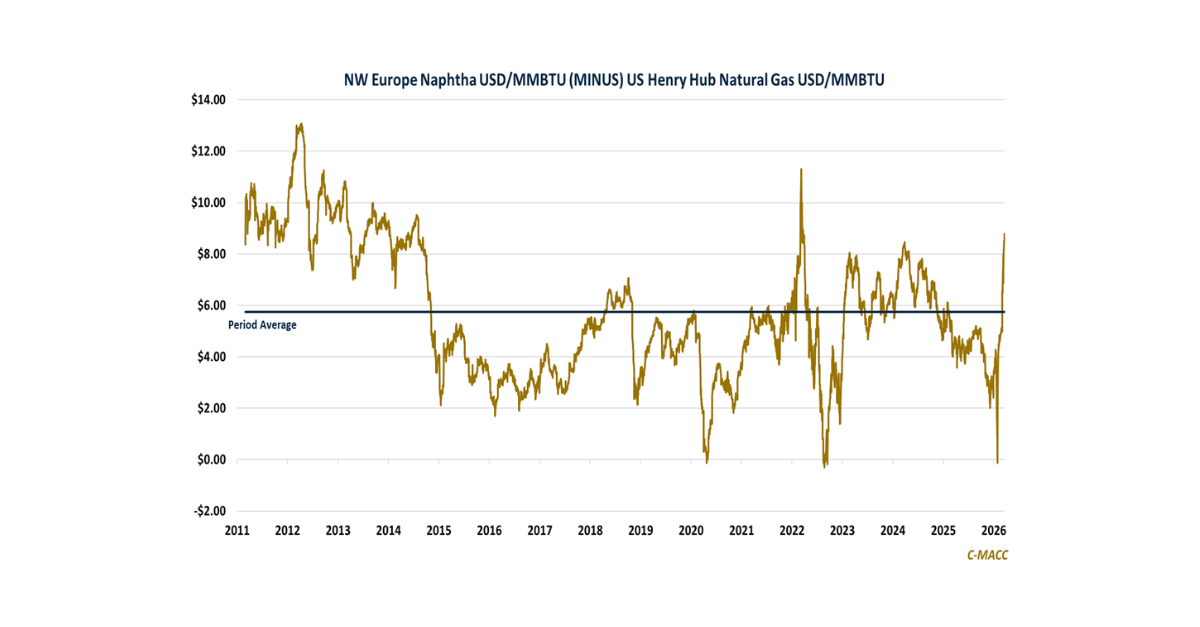

General Thoughts: Supply disruptions expose structural weaknesses in global petrochemical trade, favoring logistics flexibility and advantaged feedstocks while limiting new investment responses.

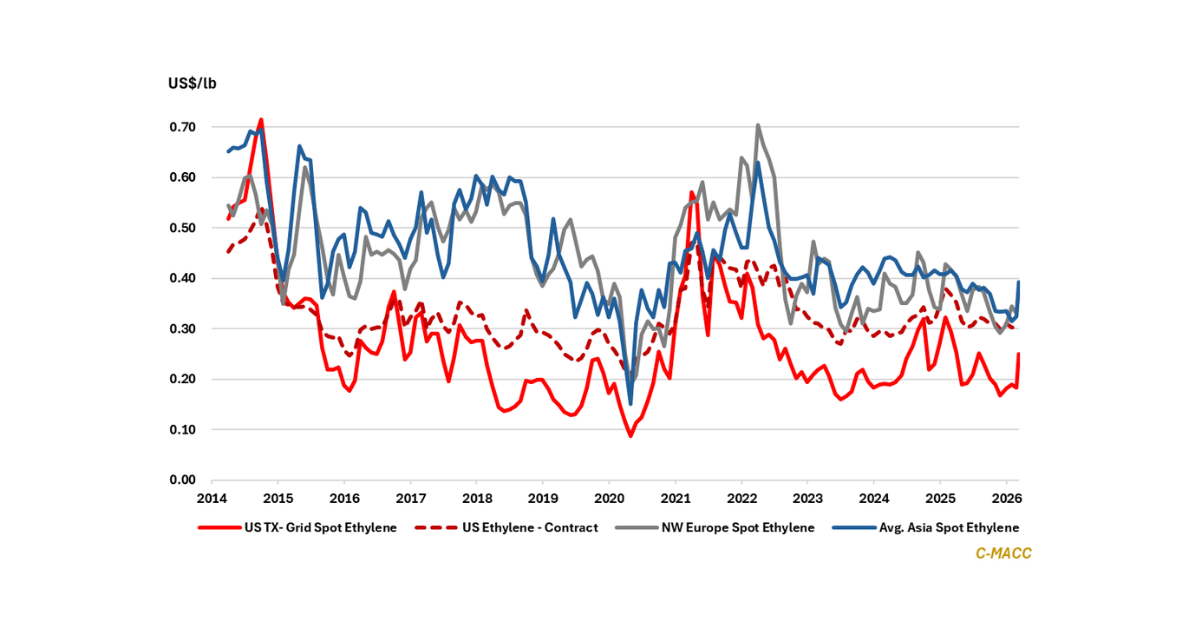

Supply Chain/Commodities: Ethylene

General Thoughts: Integration, logistics flexibility, and feedstock advantage are increasingly replacing scale as the chemical sector’s defining competitive edge, steering capital toward integrated production platforms.