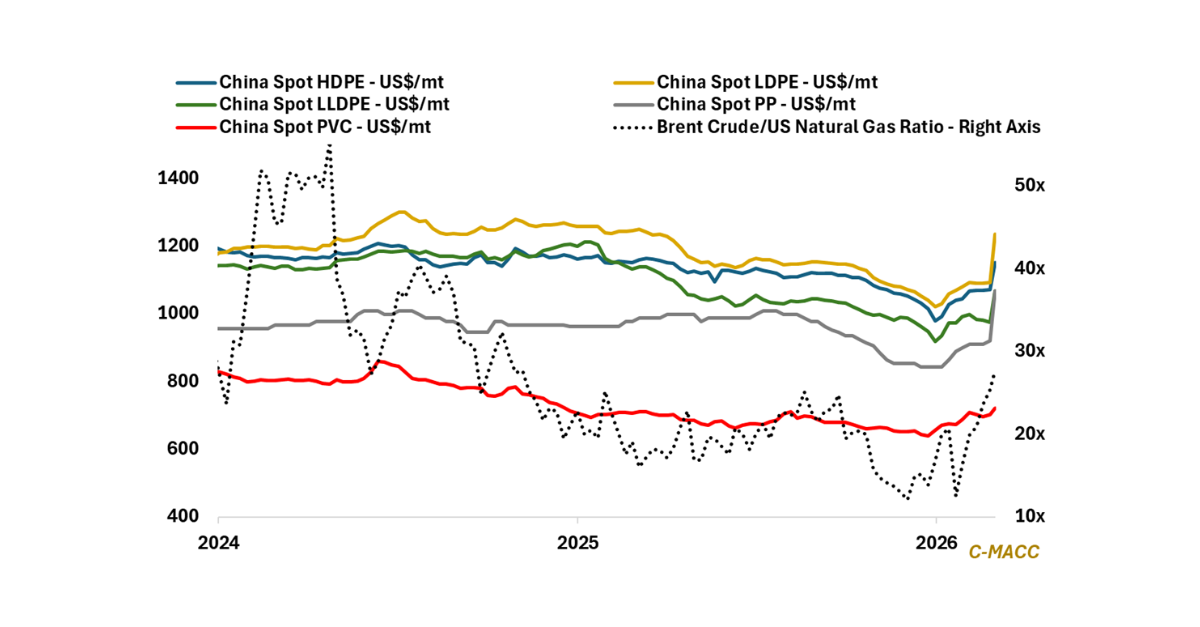

Polymer Global Analysis

General Thoughts: Volatility is rewarding integrated reach as feedstock dislocation, shipping delays, and buyer hesitation favor sustained pricing power while delaying physical market normalization despite

General Thoughts: Volatility is rewarding integrated reach as feedstock dislocation, shipping delays, and buyer hesitation favor sustained pricing power while delaying physical market normalization despite

General Thoughts: Cyclicality persists, but value increasingly concentrates in integrated systems that align cost, reliability, and flexibility as volatility reshapes risk-adjusted returns across markets in

General Thoughts: Integrated polymer producers retain a durable margin advantage through cost position, system capture, and reliability, as converters and non-integrated producers face tighter spreads

General Thoughts: Global polymer markets face constrained investment amid geopolitical disruption, raising delay risk across Asia and the Middle East, and tightening supply as cost

General Thoughts: Polymer markets are shifting toward supply security economics amid logistics disruptions, feedstock shocks, and precautionary buying, which are shifting global trade flows and

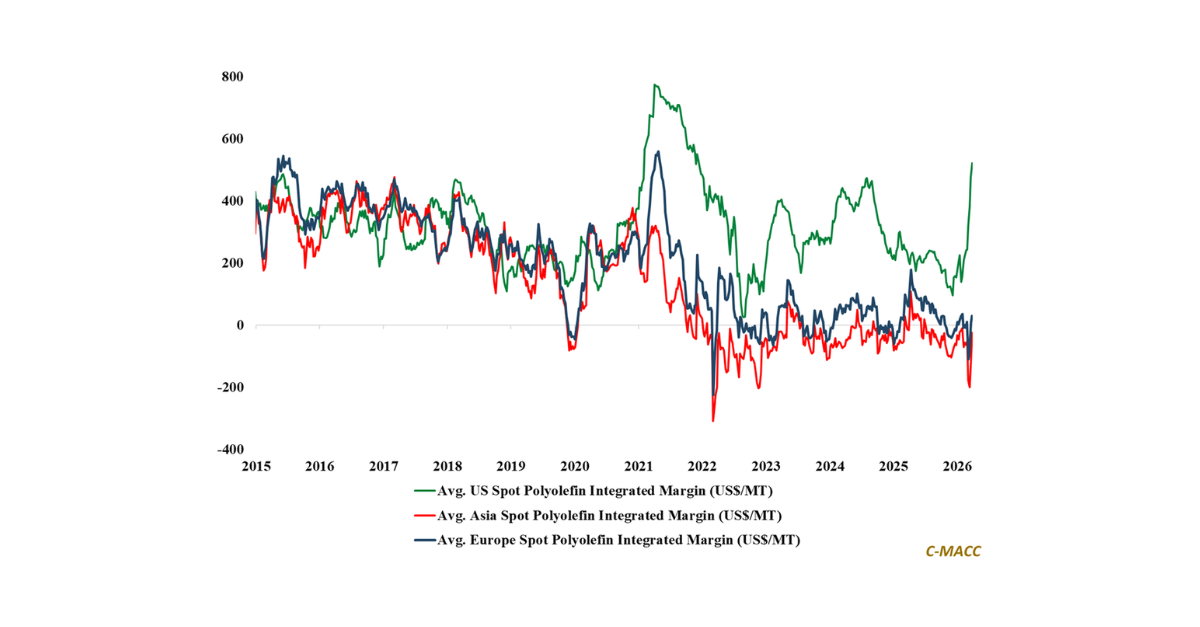

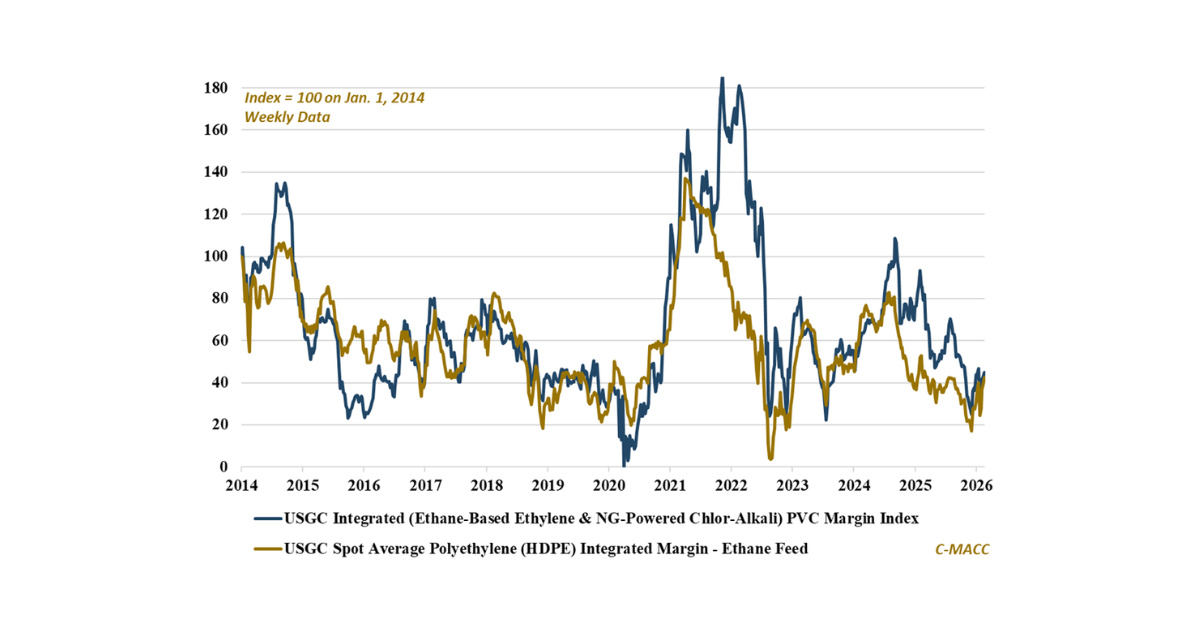

General Thoughts: Surging feedstock costs are compressing global polymer margins, forcing restructuring across Europe and Asia while restoring pricing power for integrated North American and

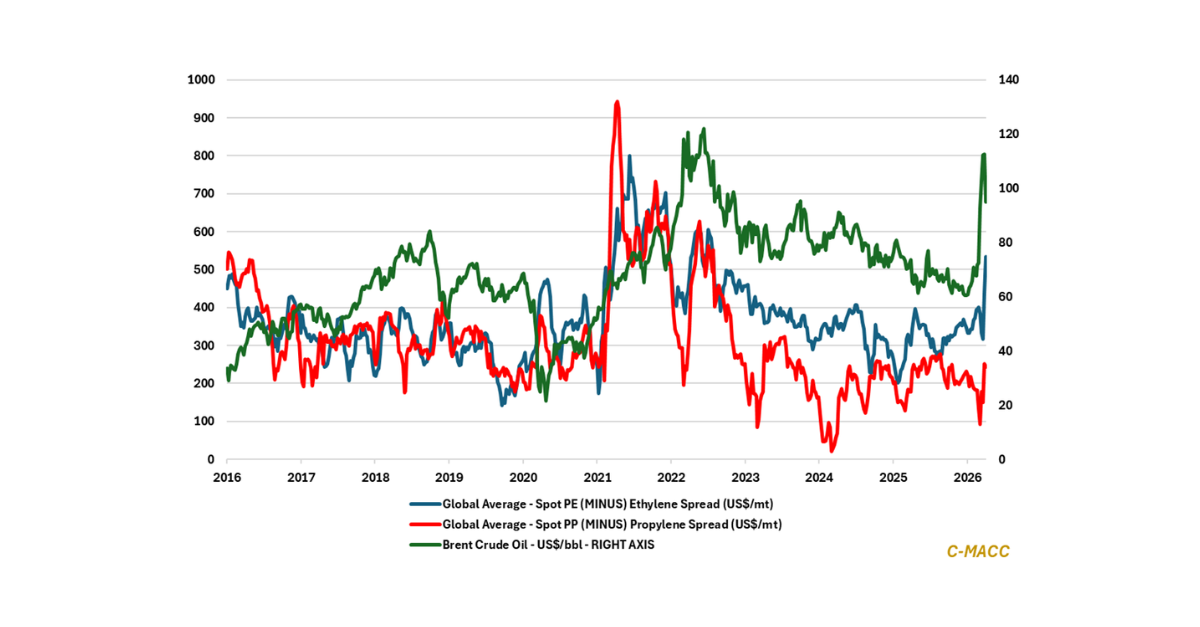

Polymer Global Analysis Resin To Riches: Weekly Plastic Market Insights Exhibit 1 – Chart of the Day: US integrated PVC and PE margins rebound in

General Thoughts: Regulation is poised to reallocate packaging profit pools toward design-led ecosystems, rewarding early specification control and lifting risk for volume-driven players that delay

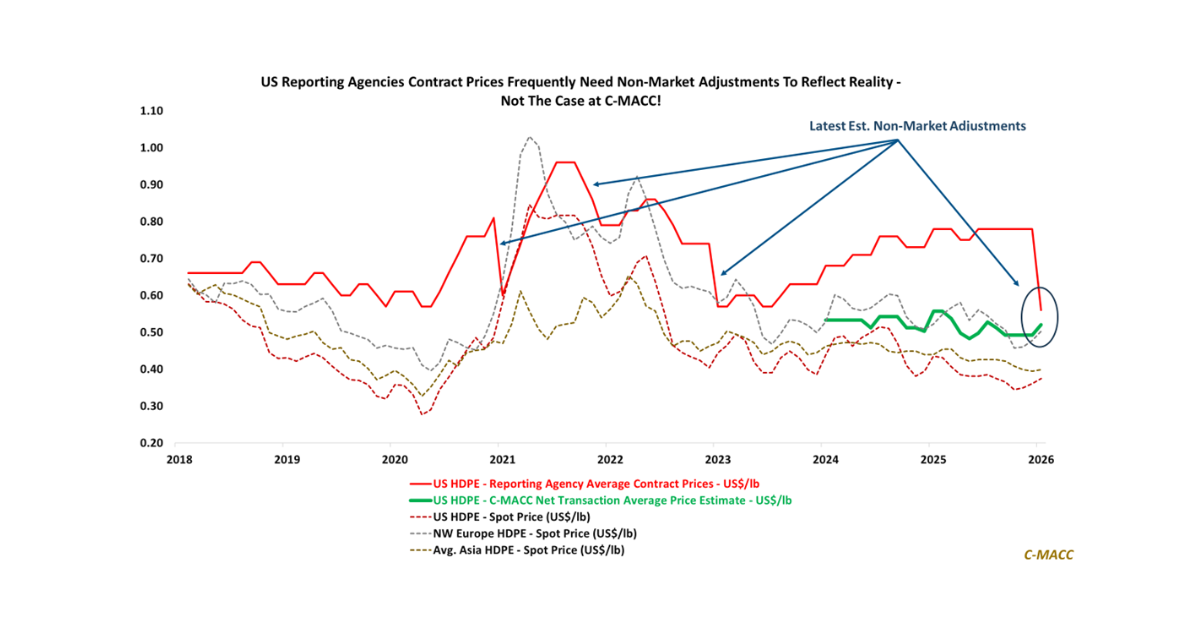

General Thoughts: Repeated NMAs highlight how published benchmarks can diverge from transactional reality, reinforcing the value of C-MACC’s polymer market services in aligning pricing strategy,

General Thoughts: Value premia earned through differentiation at cycle troughs can signal future share gains, enabling advantaged producers to run hard, more consistently price on