Sunday Executive Summary

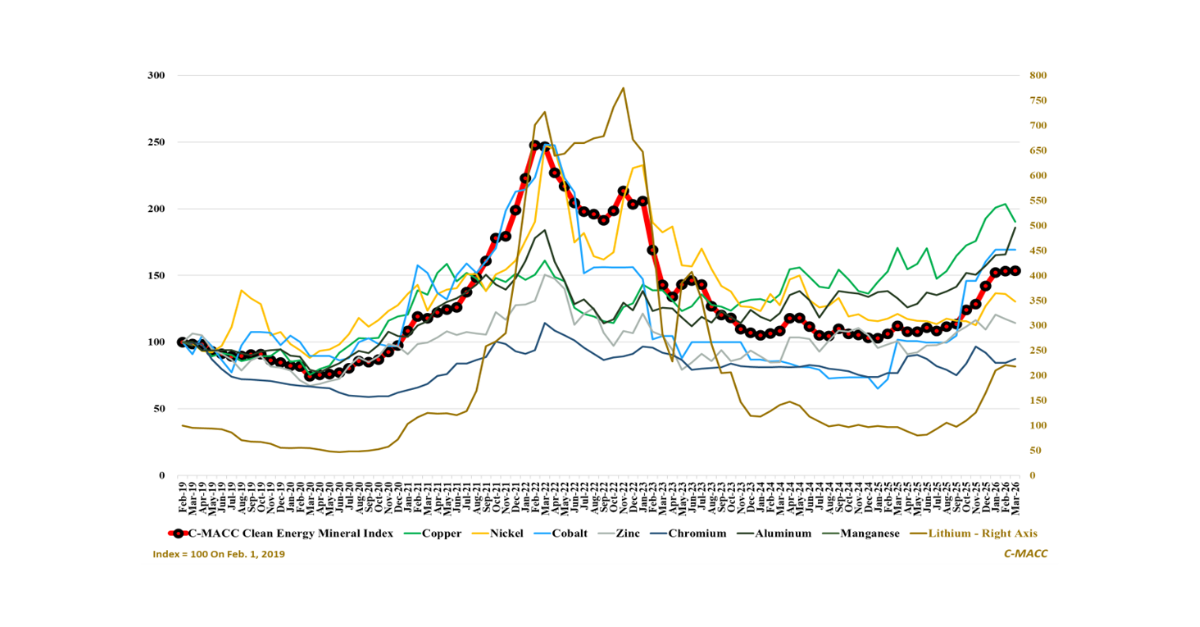

Critical minerals diverge as electrification costs fall structurally, confirming inputs are no longer the binding constraint and decisively shifting advantage toward systems that deliver reliable

Critical minerals diverge as electrification costs fall structurally, confirming inputs are no longer the binding constraint and decisively shifting advantage toward systems that deliver reliable

System constraints are compressing global corporate decision cycles, forcing capital into platforms that secure inputs, logistics, and execution simultaneously rather than optimizing sequentially across markets.

Dependable operations now define competitive advantage, with non-integrated assets losing ground as fragility disrupts throughput, raises risk, and weakens returns under stress.

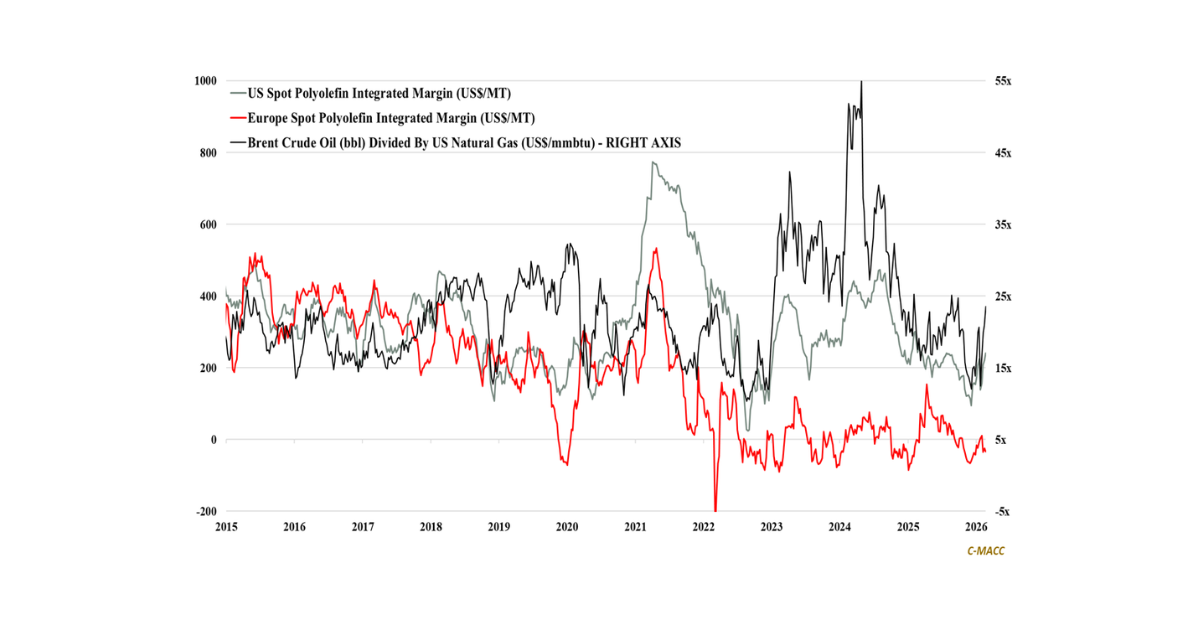

Oil-linked feedstock systems

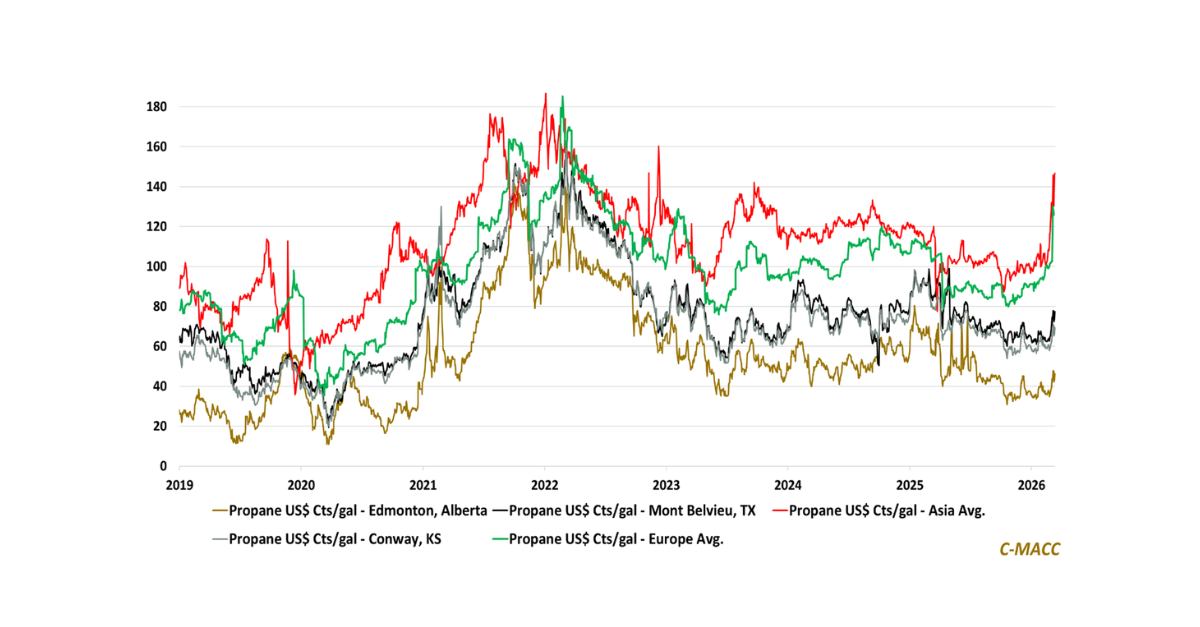

Asia and Europe now pay a structural propane premium as Middle East disruption risk lifts import costs, compressing PDH production margins abroad and reinforcing North

Surging crude prices and widening feedstock spreads are steepening the global petrochemical cost curve. Cheap regional gas and NGLs may support selective integration, but not

Europe’s chemical sector return outlook now hinges far less on cyclical recovery and far more on feedstock structure, carbon exposure, and policy-backed demand durability amid

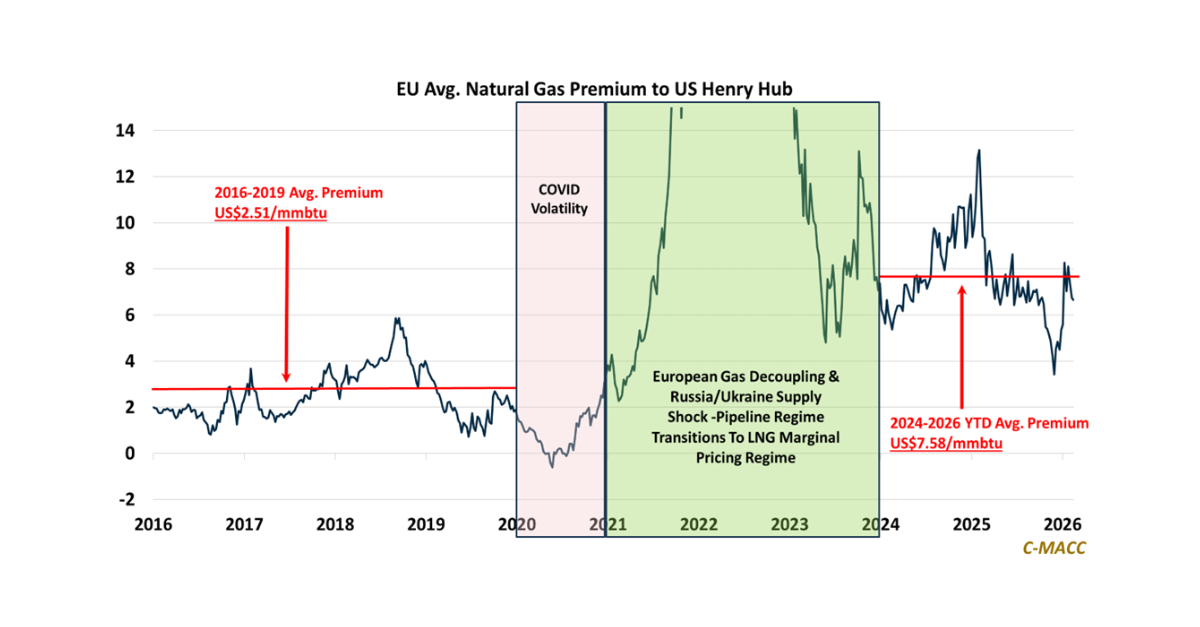

Persistent European premiums over Henry Hub confirm LNG marginal clearing as the dominant marginal price-setting mechanism, anchoring US export-linked gas economics and long-cycle infrastructure returns.

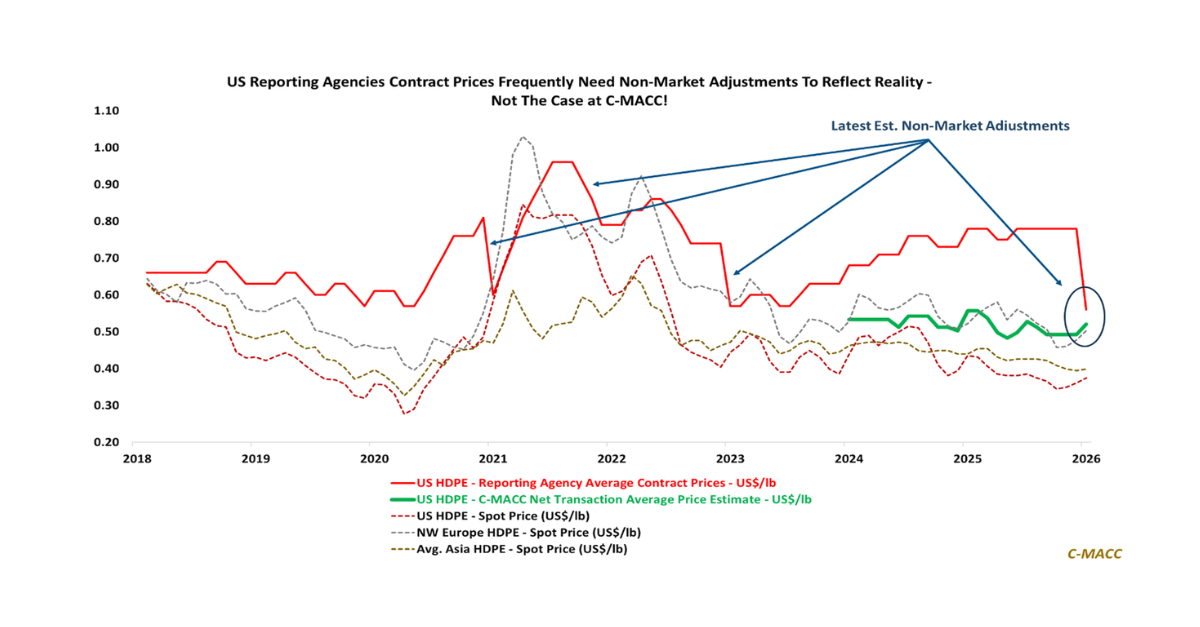

Are you underwriting capital and pricing decisions using benchmarks that periodically reset to reflect reality, or real-time intelligence that recalibrates risk before global and regional

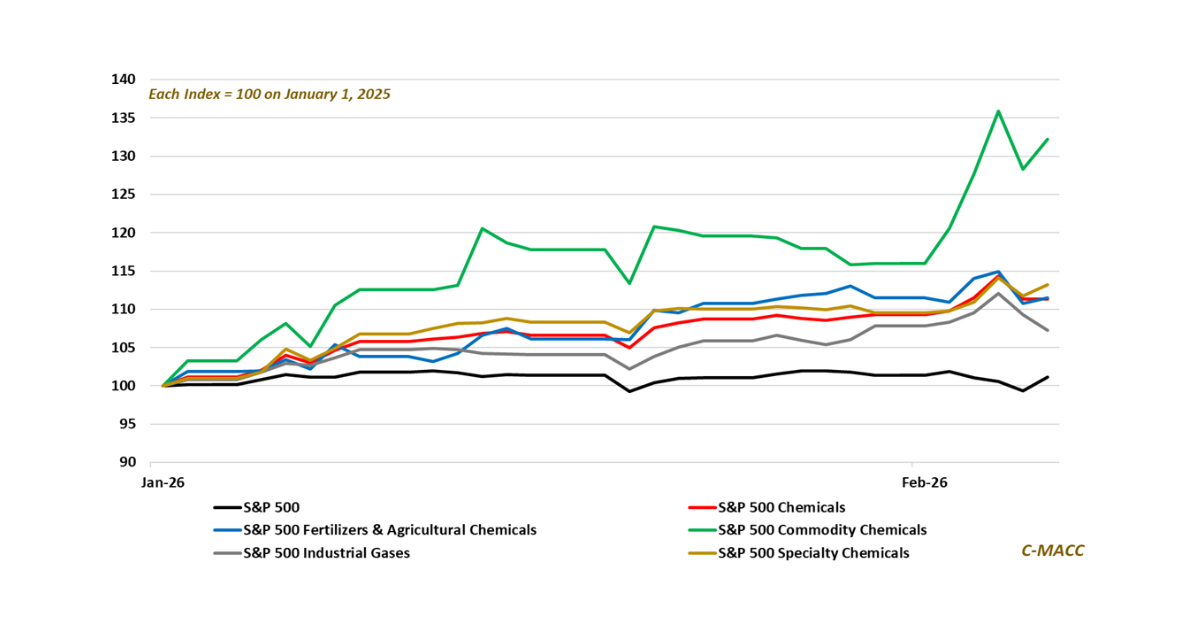

Cycles matter, but winners change as structure evolves; disciplined capital allocation separates chemical sector participants positioning for durable advantage from those who let pessimism delay

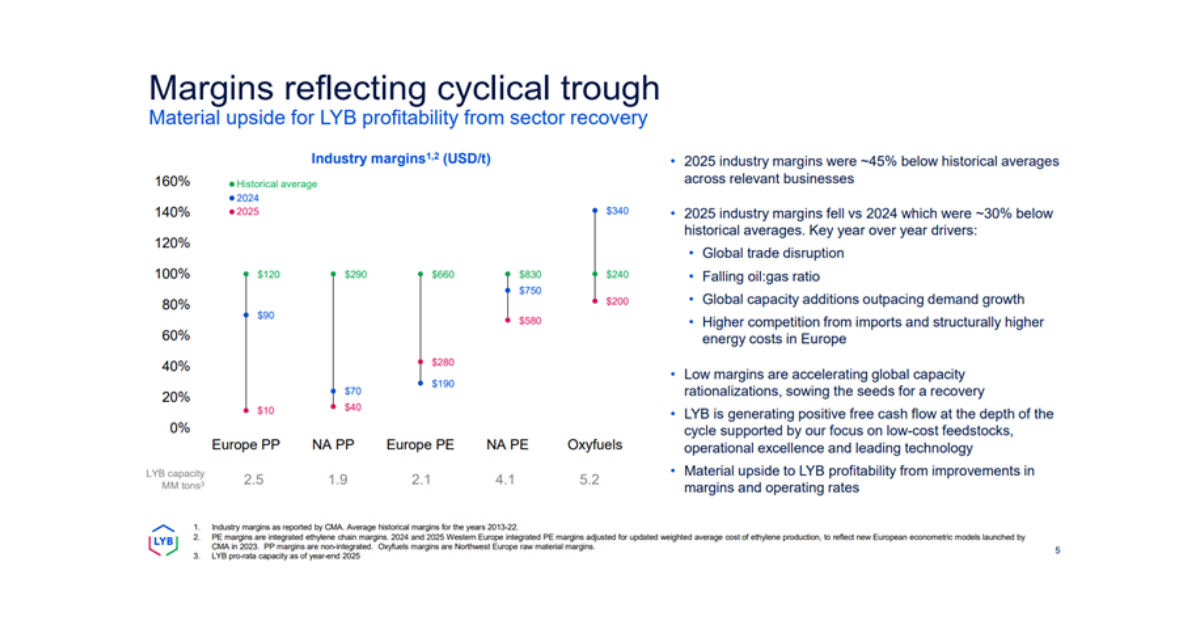

Prolonged petrochemical weakness reflects oversupply not demand collapse, extending the cycle and shifting strategy from growth to margin defense, cost-curve control, and execution-led recovery outcomes.