Base Chemical Global Analysis

General Thoughts: Global industrial markets are no longer equilibrating through trade, as constrained logistics and feedstock access prevent arbitrage from normalizing regional price dislocations across

General Thoughts: Global industrial markets are no longer equilibrating through trade, as constrained logistics and feedstock access prevent arbitrage from normalizing regional price dislocations across

General Thoughts: Global industrial markets have fractured into parallel pricing regimes where cost, logistics, and access determine outcomes. Markets are no longer clearing globally; they

General Thoughts: Energy divergence, supply disruption, and logistics risk are forcing a structural shift toward integrated, feedstock-secure systems as merchant models lose reliability and margin

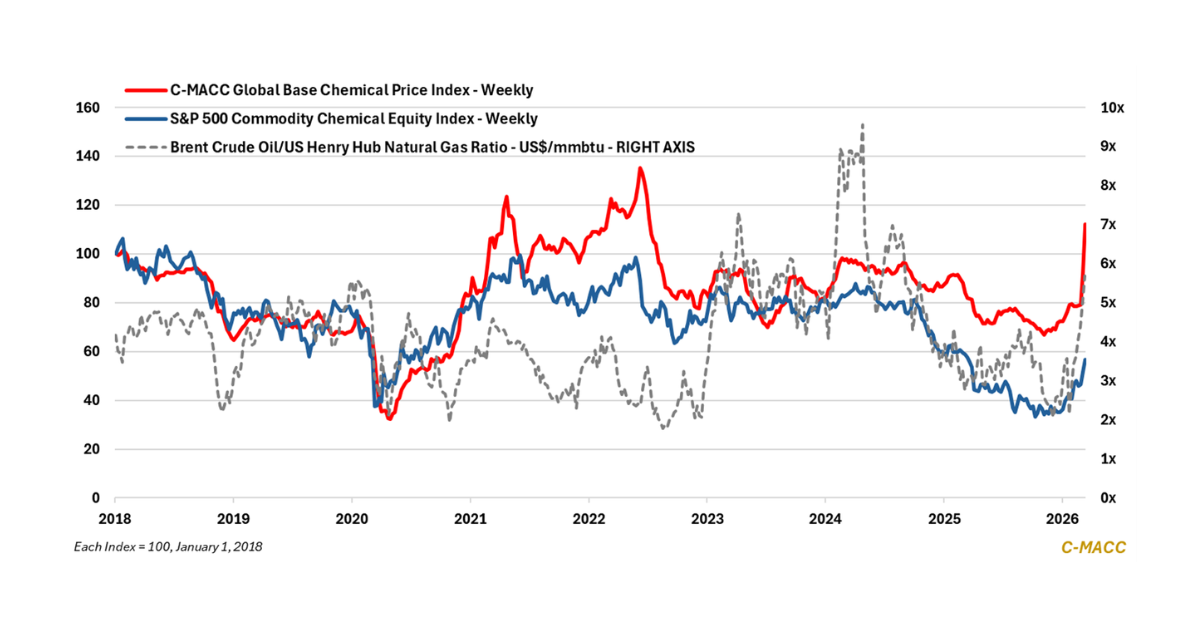

General Thoughts: Energy shocks are steepening global petrochemical cost curves, tightening supply balances, and boosting sentiment toward advantaged production systems after prolonged oversupply concerns.

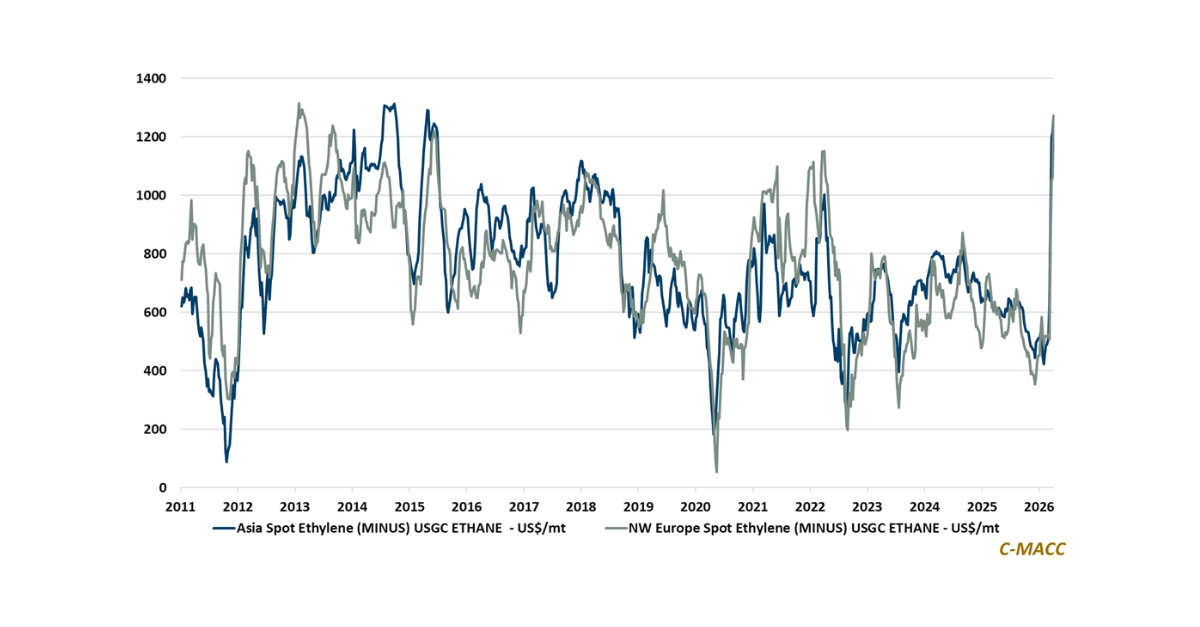

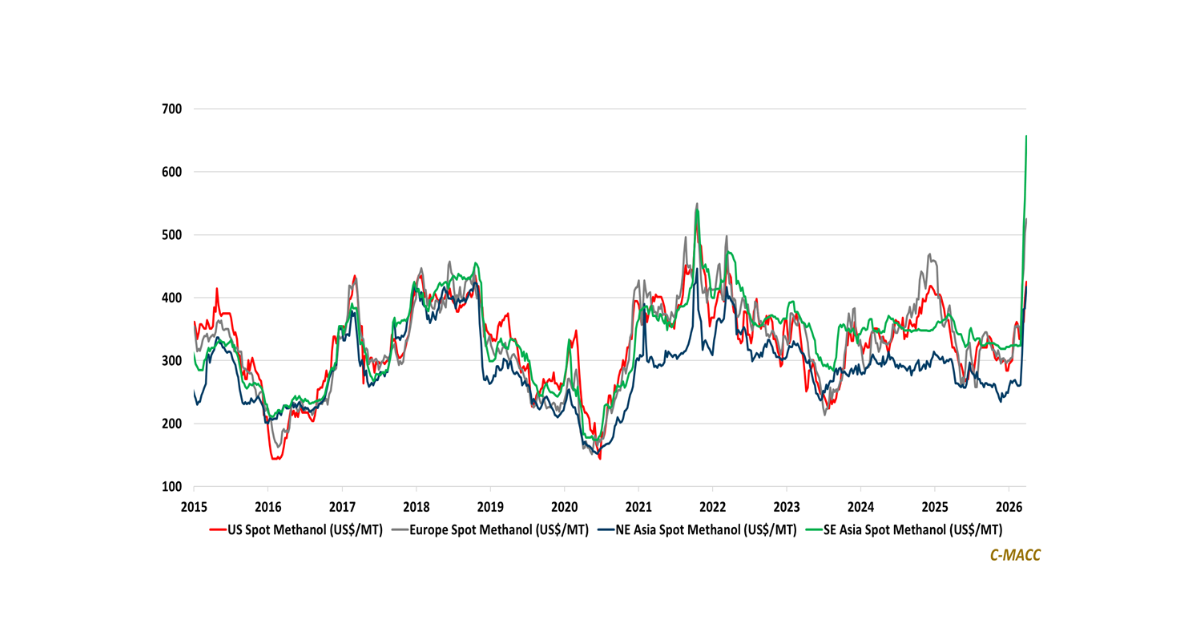

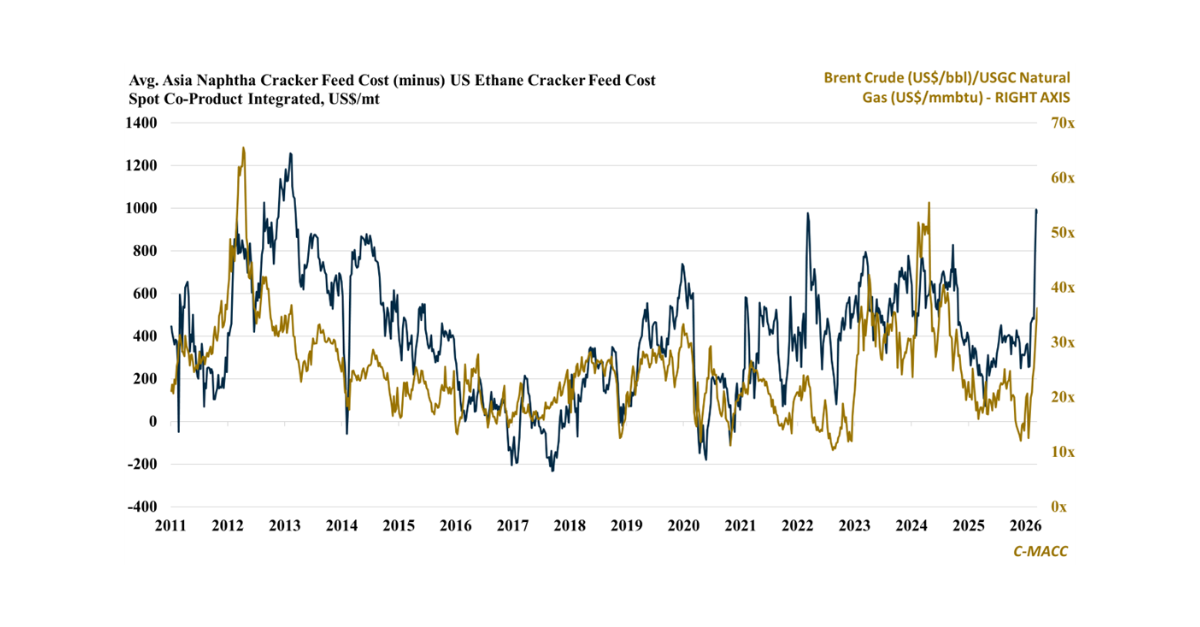

Feedstocks

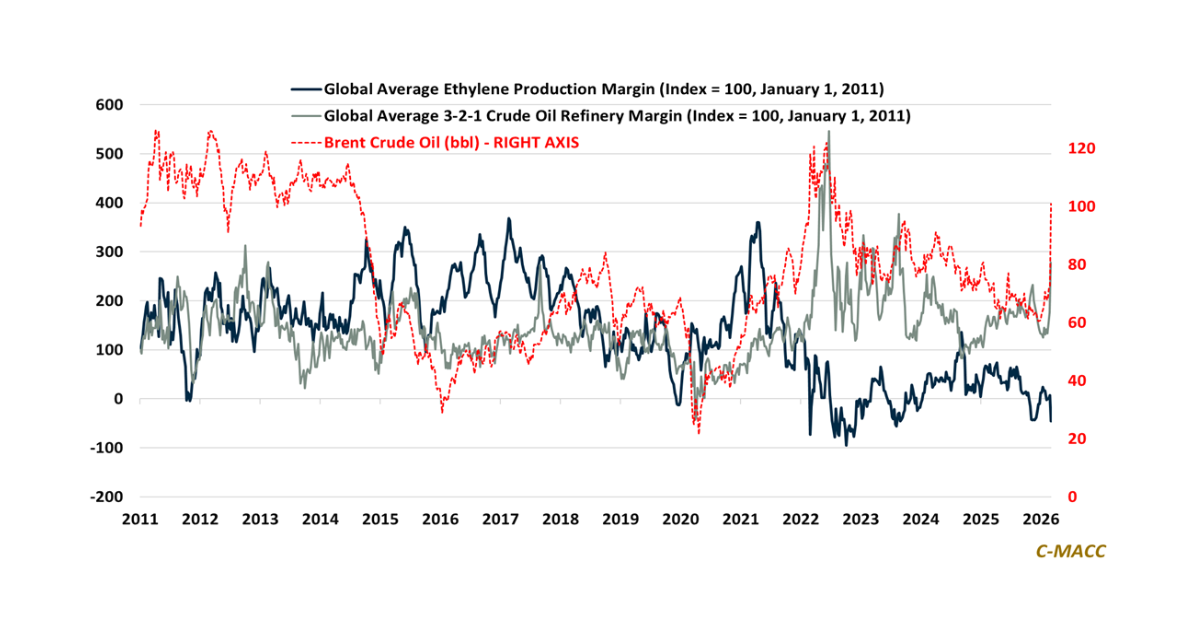

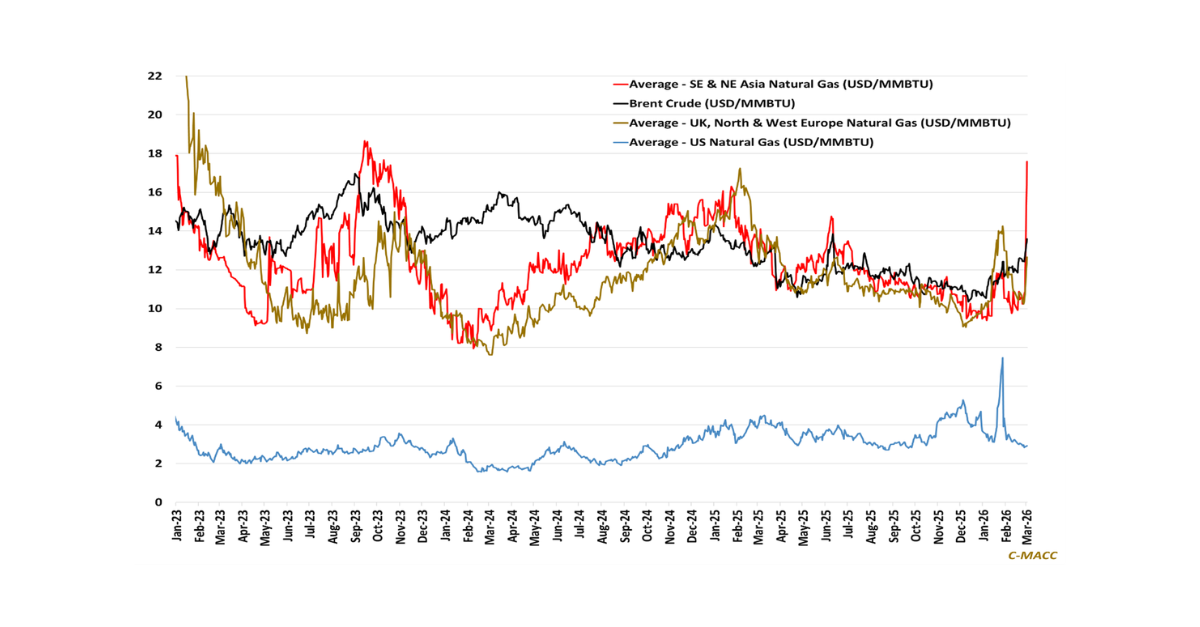

General Thoughts: Energy shocks are redistributing profitability across industrial value chains as surging ex-US energy costs compress petrochemical margins, tighten fertilizer markets, and strengthen North

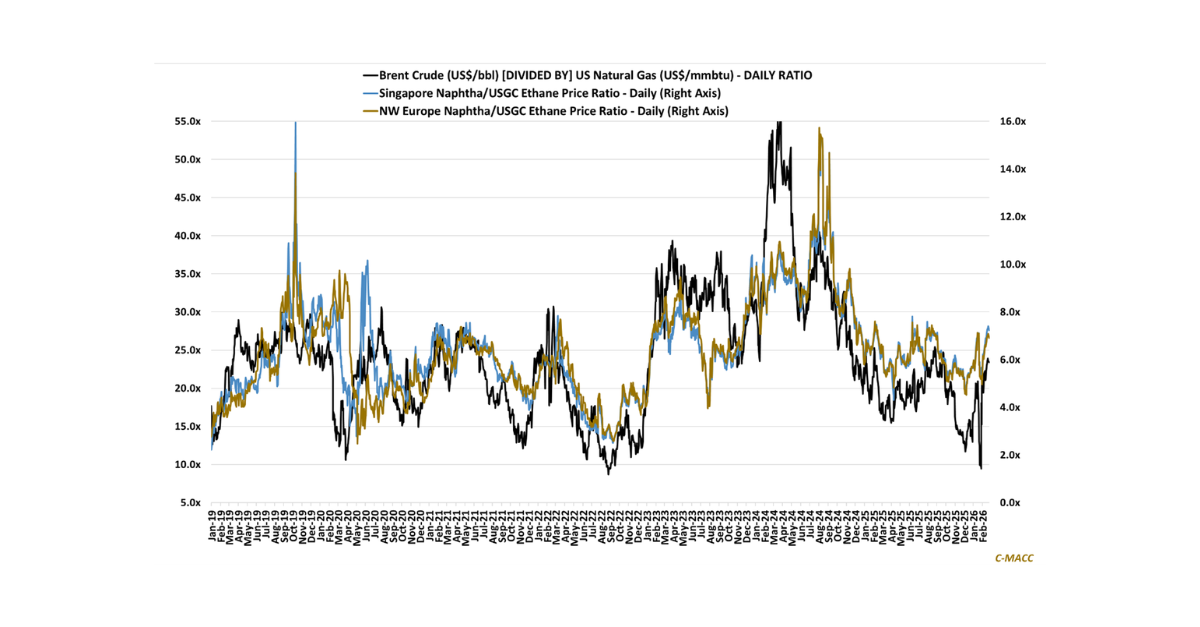

General Thoughts: Crude oil and Ex-US natural gas price strength relative to US levels has steepened the global cost curve for most chemicals, accelerating rationalization

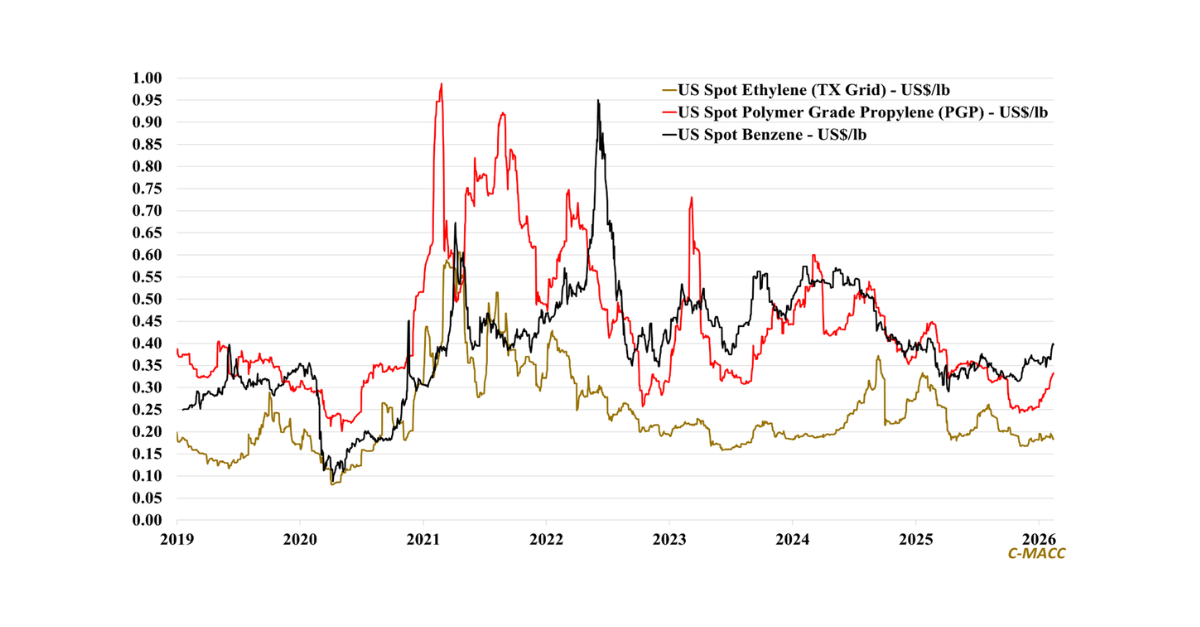

General Thoughts: Oil-to-gas dispersion, cracker co-product volatility, and logistics bottlenecks signal that 2026 returns will reward integration and execution over scale, while accelerating needed sector

General Thoughts: Structural global base chemical oversupply delays synchronization, leaving 2026 margins governed by feedstock dispersion, logistics control, and disciplined utilization rather than demand recovery.

General Thoughts: Global chemical markets are fragmenting across feedstocks, chemicals, and fuels, rewarding logistics, integration, and discipline, while exposing structurally misaligned assets to prolonged margin

General Thoughts: Energy retracement and post-storm natural gas normalization begin to restore relative cost balance, enabling advantaged producers to outperform, while persistent oversupply constrains pricing