Power Struggle: Europe Pays to Stand Still as America Keeps the Cost Edge

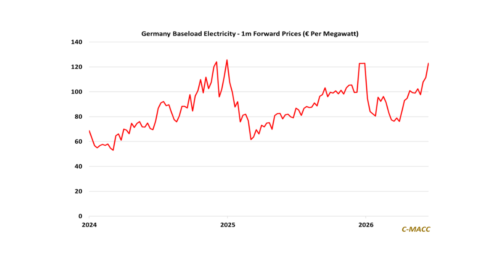

Global Market Analysis Power Struggle: Europe Pays to Stand Still as America Keeps the Cost Edge Key Findings Exhibit 1: Germany’s Rising Power Prices Add Another Headwind to Europe’s Industrial Competitiveness. Source: Bloomberg, C-MACC Analysis, July 2026 See the PDF below for all charts, tables, and diagrams