Can’t Get No Supply-faction: Reliability Repriced, Pricing Power Fractures

General Thoughts: Feedstock inflation is shifting profit pools upstream, forcing buyers to absorb volatility as reliability overtakes price and accelerates alternative supply in procurement decisions.

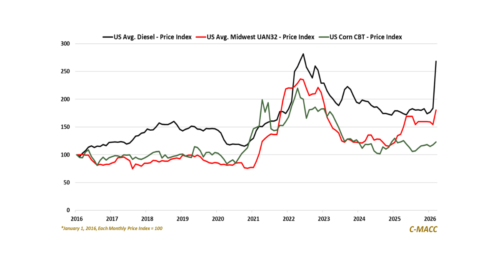

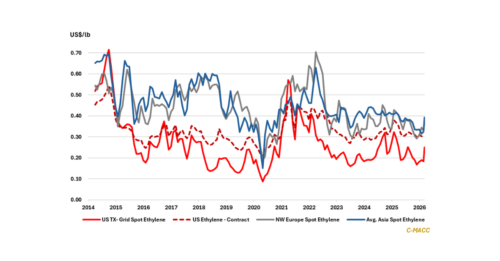

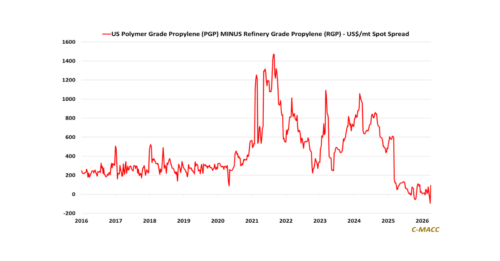

Supply Chain/Commodities: Global propylene tightness is supply-driven across crackers, PDH, and refineries, sustaining higher prices and compressing merchant margins as costs outpace derivative pass-through.

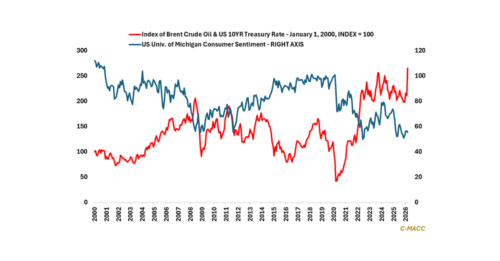

Energy/Upstream: