Sunday Executive Summary

Industrial companies are directing capital toward revenue that can finance continued investment without leaving the wider business exposed when customers, technologies, or regional economics change.

Industrial companies are directing capital toward revenue that can finance continued investment without leaving the wider business exposed when customers, technologies, or regional economics change.

1st Topic of the Week: The renewable fuel market is shifting from margin expansion to margin defense as feedstocks catch up, making flexible assets and

General Thoughts: Supportive prices and cost takeouts increase upside for low-cost producers as high-cost operators restructure for survival, widening earnings gaps and increasing pressure for

General Thoughts: North American producers are gaining an edge as overseas margins weaken, with dependable integrated plants best placed to convert lower feedstock costs into

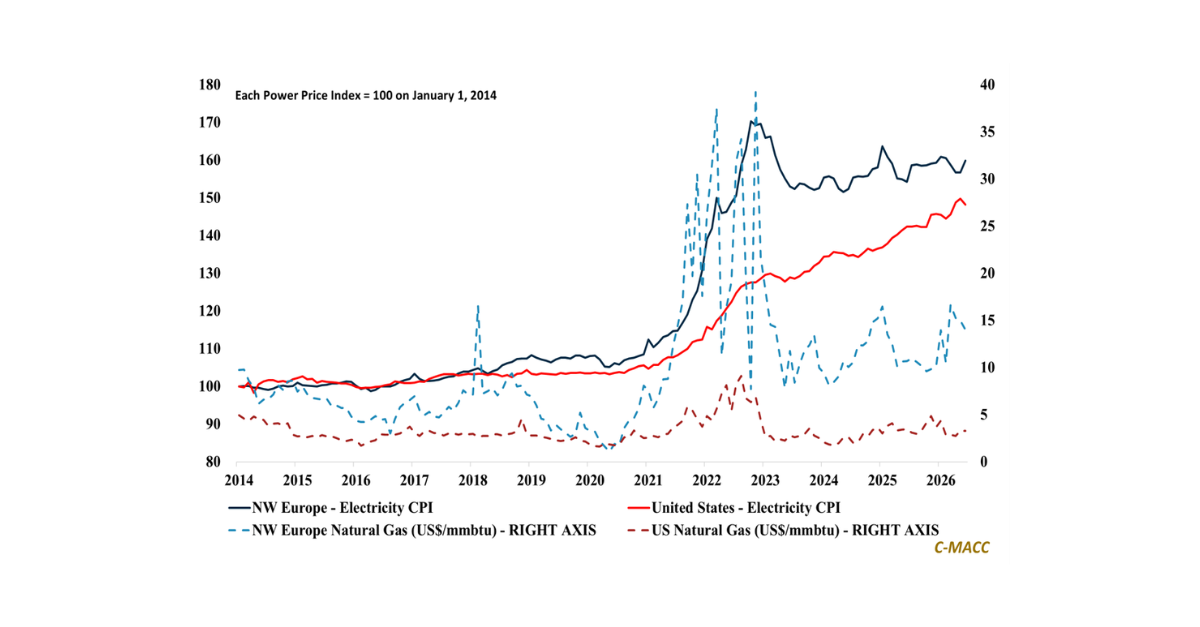

Global Market Analysis Power Struggle: Europe Pays to Stand Still as America Keeps the Cost Edge Key Findings Exhibit 1: Germany’s Rising Power Prices Add

General Thoughts: Rising input costs are separating price gains from earnings, rewarding refiners and feedstock-advantaged producers as cautious customers delay commitments and higher-cost operators reduce

Being low cost widens producer margins, but customer resistance can reduce utilization, realized volume, and total earnings even when the underlying cost advantage remains intact

1st Topic of the Week: Fuel advantage is only the opening position, raising the harder question: which regions can convert it into electricity without sacrificing

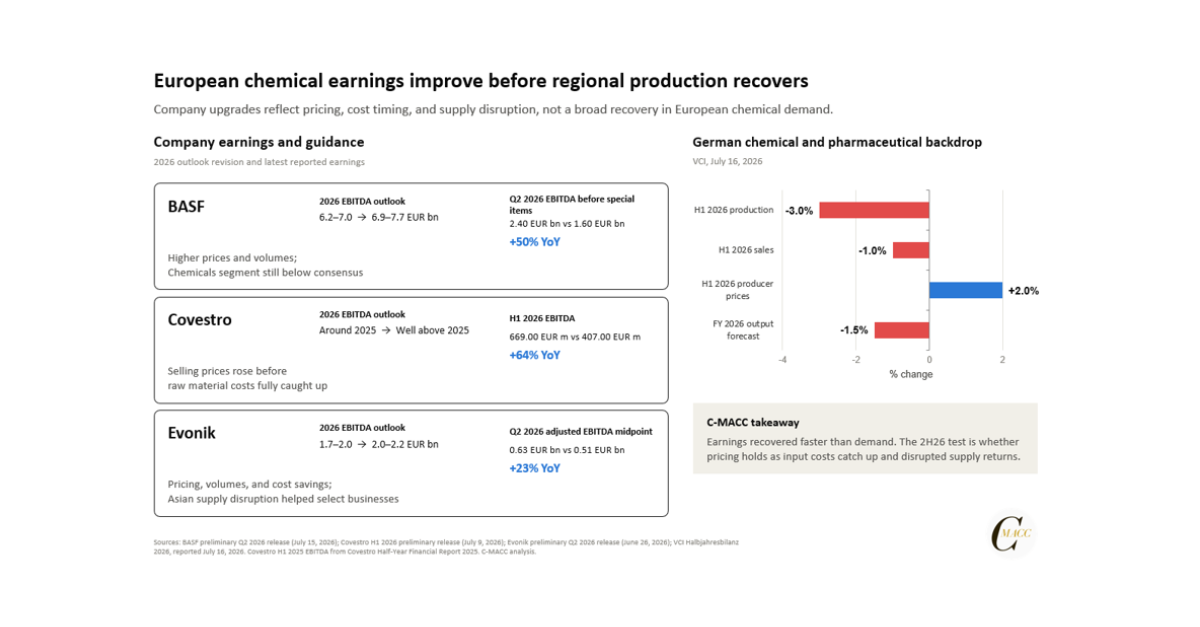

General Thoughts: Company-specific pricing, cost timing, and supply advantages lifted 2Q26 results before end demand improved, leaving 2H26 performance exposed to higher inputs and normalized

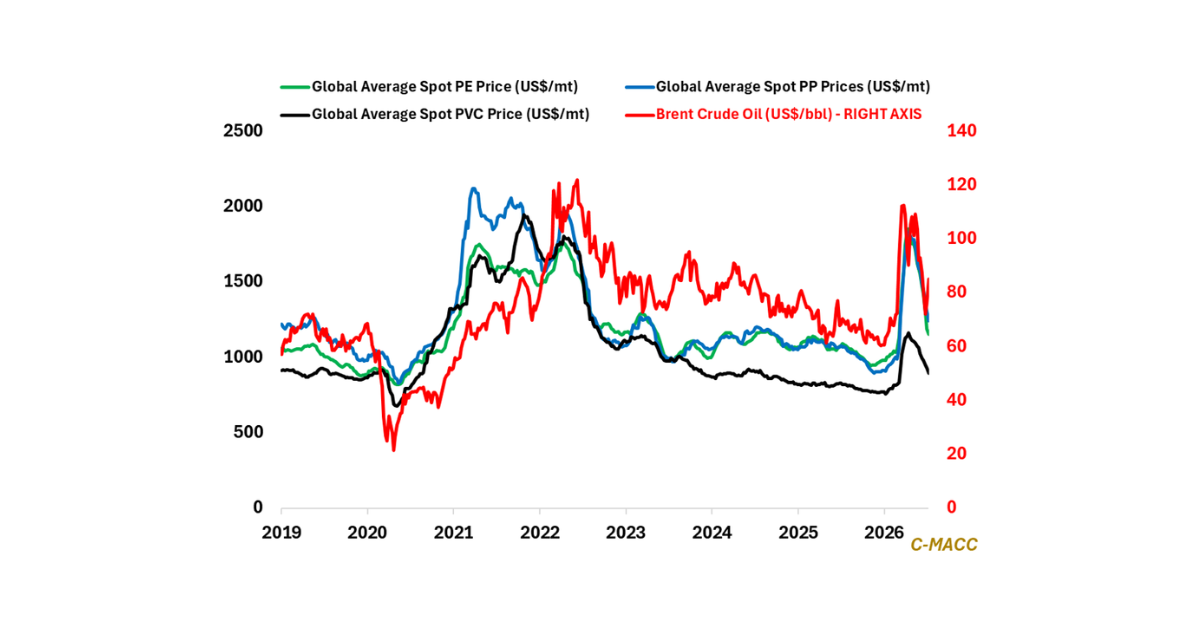

General Thoughts: During 2Q26 earnings calls, polymer producers will address July prices below June-quarter averages, but higher costs and supply risks challenge forecasts for sustained