What Shows Up Gets Paid: If You Can’t Deliver, You Don’t Compete

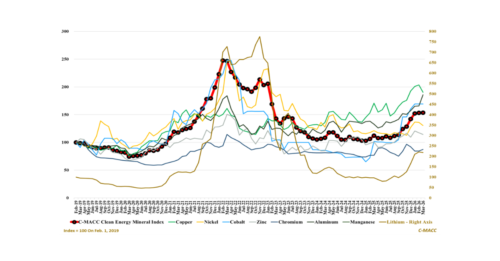

Critical minerals diverge as electrification costs fall structurally, confirming inputs are no longer the binding constraint and decisively shifting advantage toward systems that deliver reliable power.

Power markets no longer clear on fuel economics, exposing how capacity, transmission, and timing determine pricing and leaving traditional cost-based strategies increasingly misaligned with