Global Market Analysis

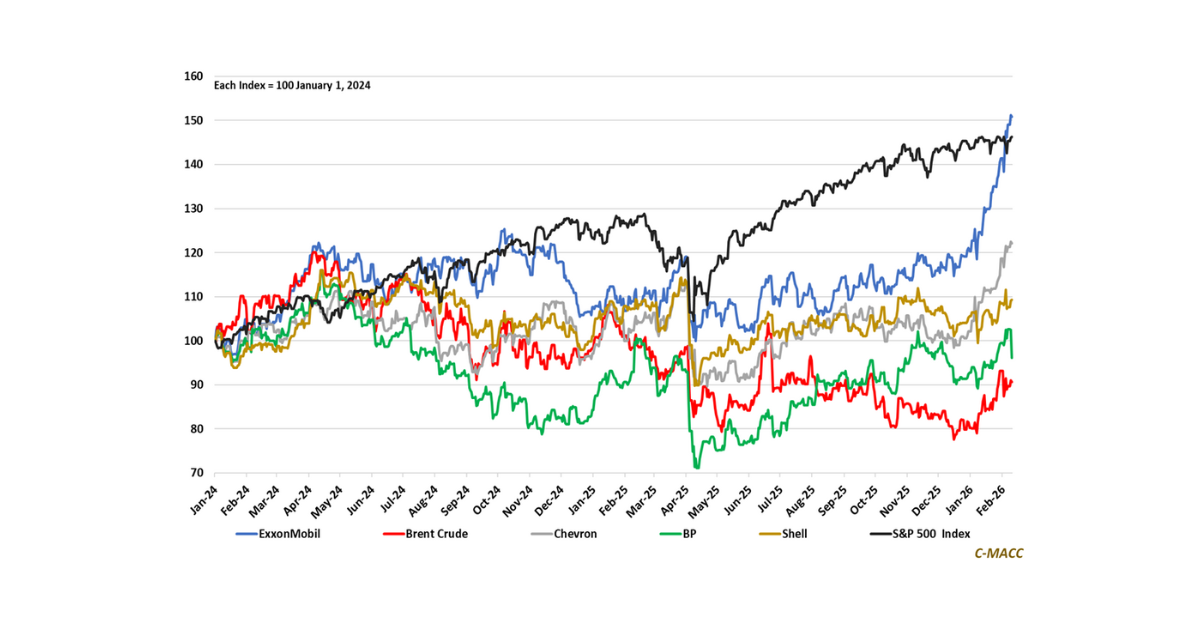

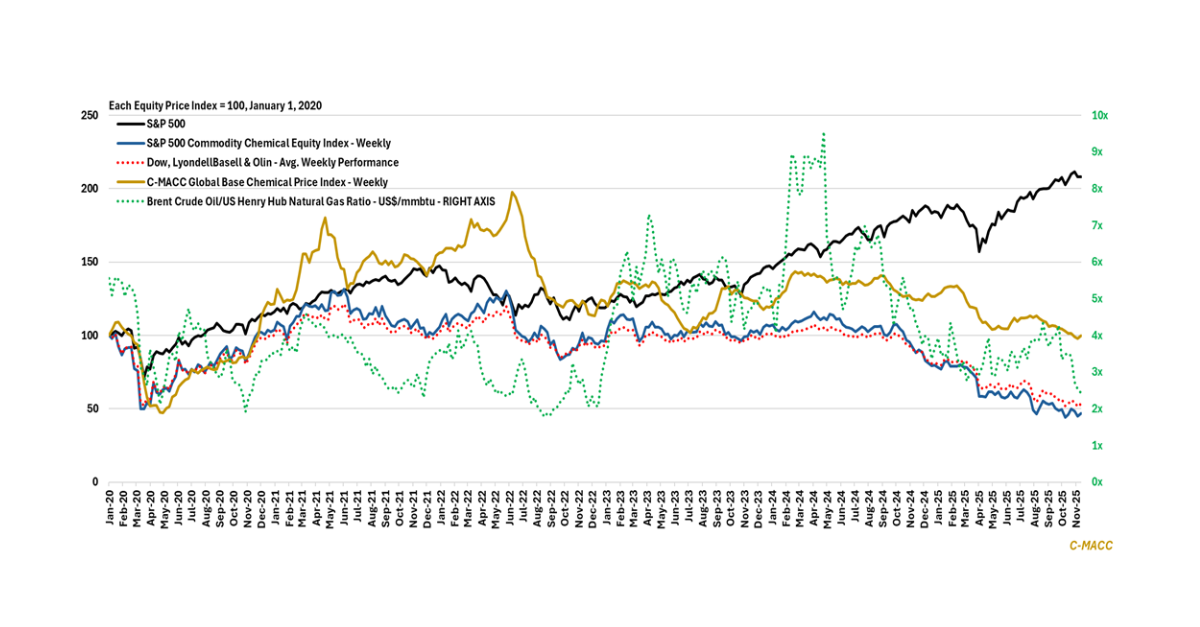

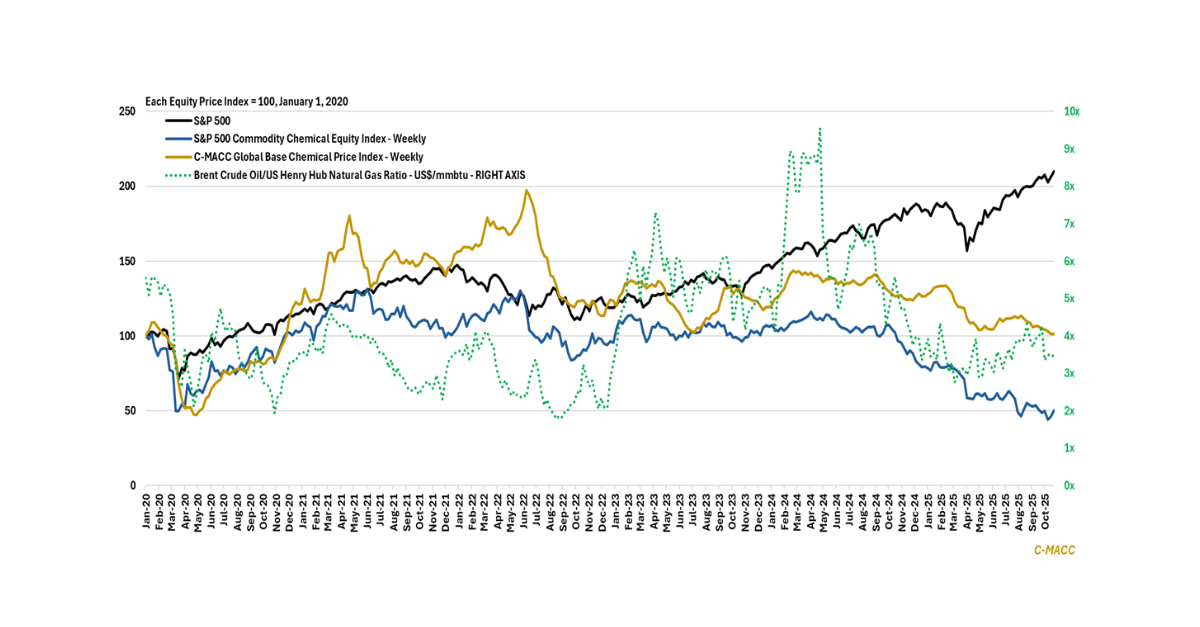

General Thoughts: ExxonMobil’s outperformance shows markets reward relatively clearer return profiles and capital discipline, a lesson chemicals and industrial players must heed as volatility tests

General Thoughts: ExxonMobil’s outperformance shows markets reward relatively clearer return profiles and capital discipline, a lesson chemicals and industrial players must heed as volatility tests

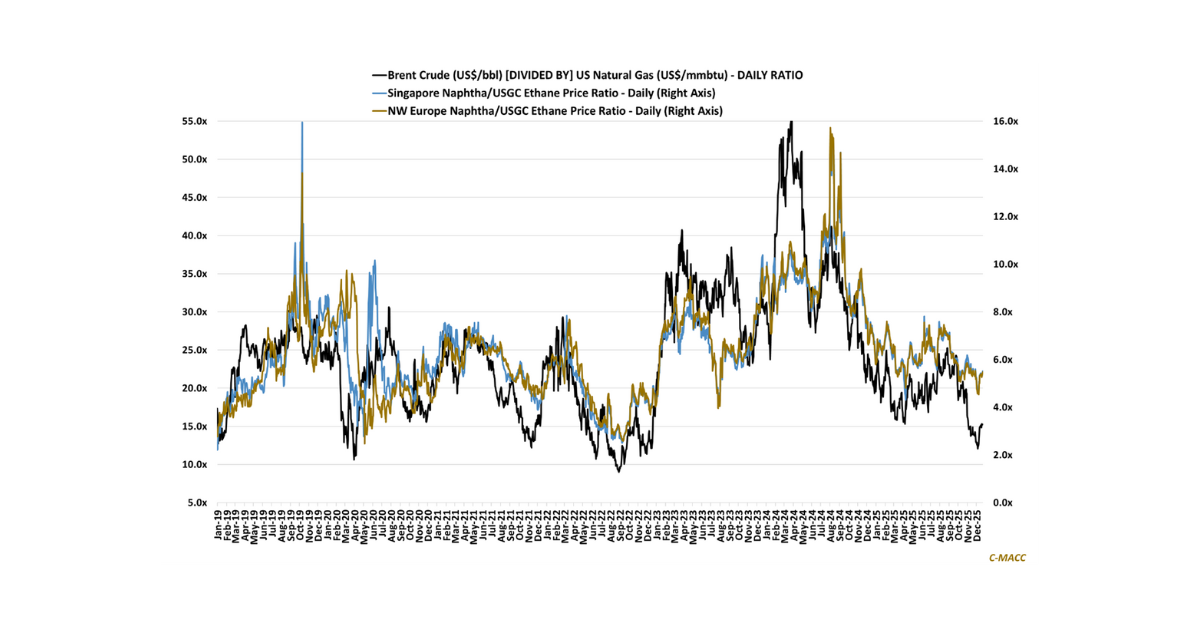

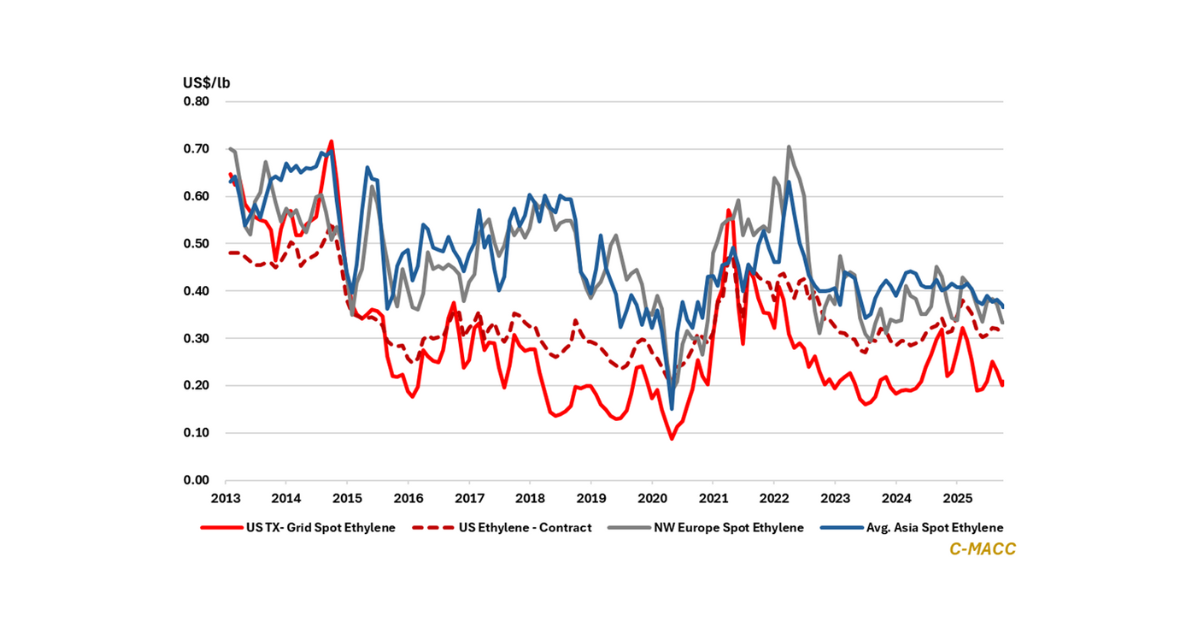

General Thoughts: Early-year chemical spot prices and relative feedstock cost movements suggest that the pace of restructuring and regional return-enhancement efforts will be more decisive

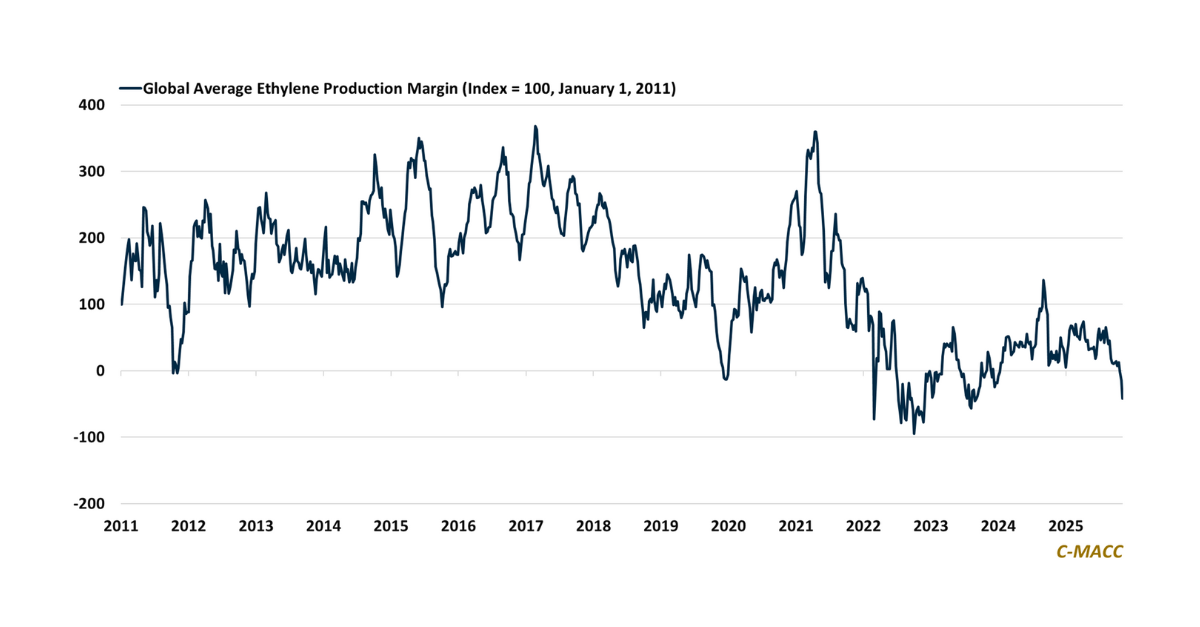

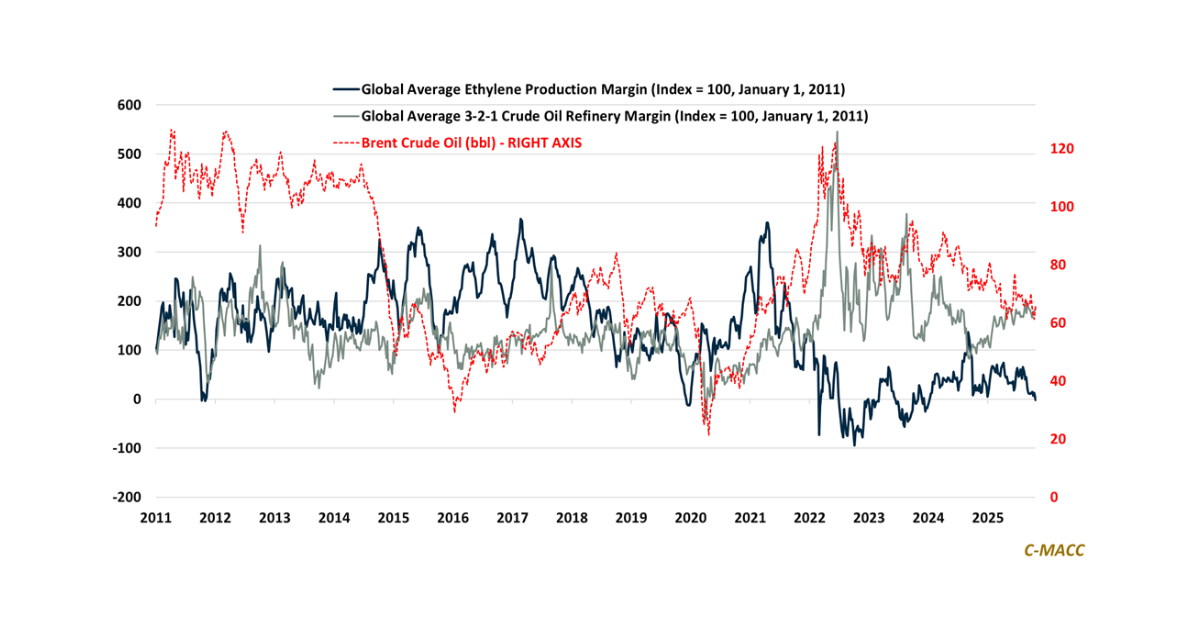

General Thoughts: Depressed global chemical sector growth expectations, co-product erosion, and flattened cost curves make restructuring pace and margin resilience more decisive than demand recovery

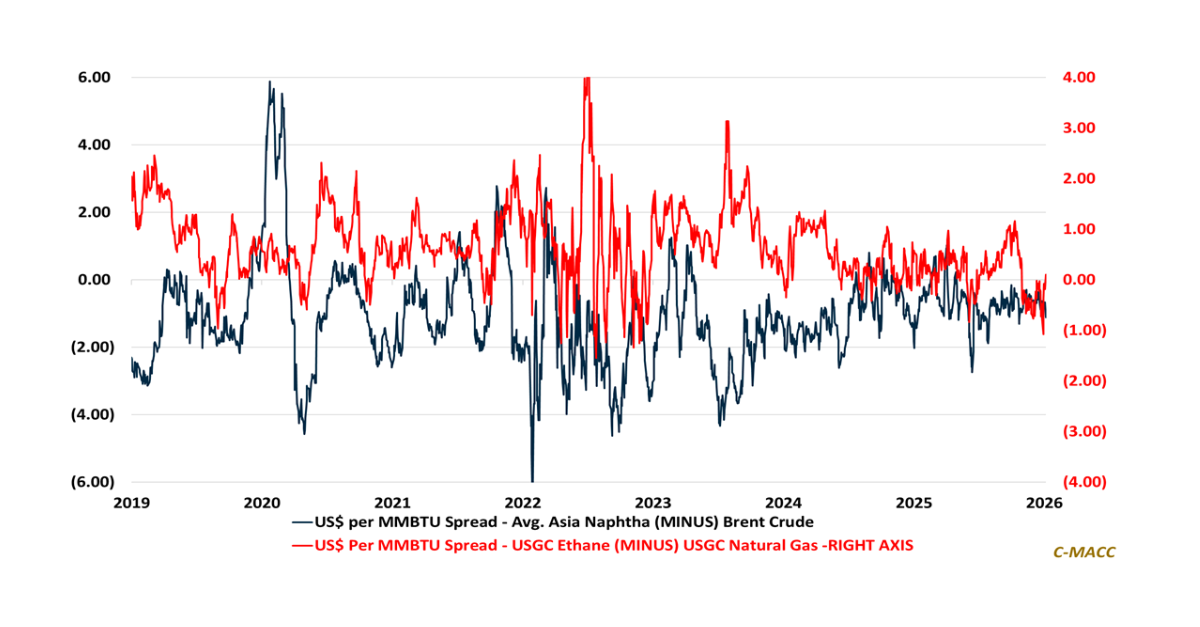

General Thoughts: Chemical feedstock movements drive greater sector margin compression WoW than price shifts, as late 2025 supply adjustments and flatter global cost curves shape

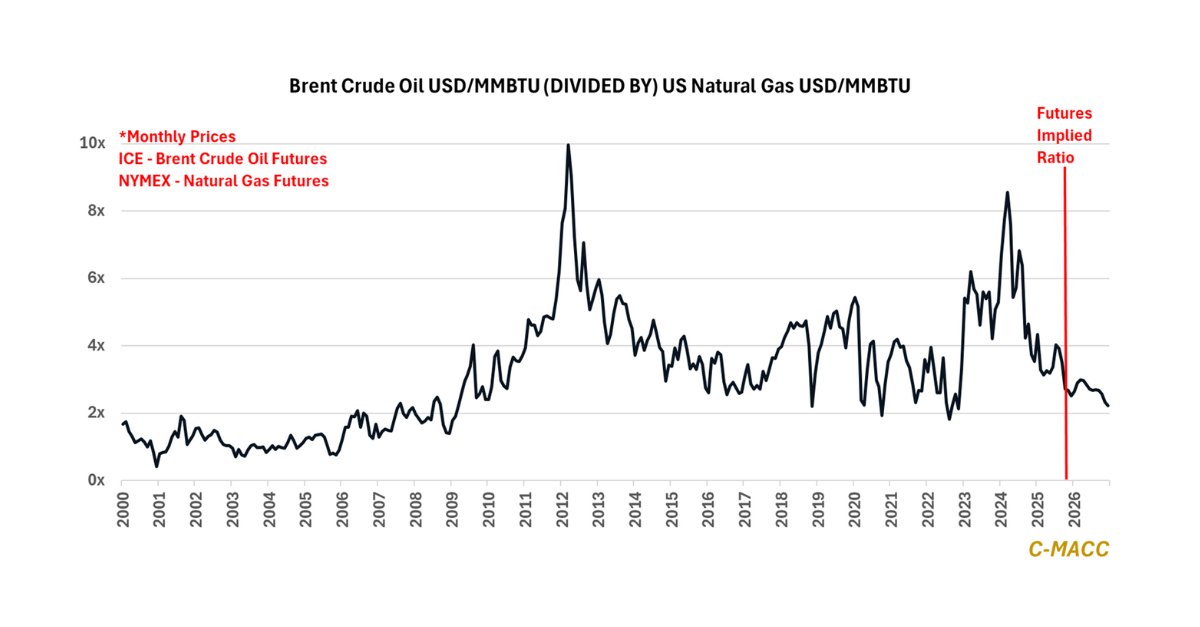

General Thoughts: Sector momentum in late 2025 reflects commodity divergence, with easing crude and Ex-US natural gas prices, firm US gas, and mixed demand exposing

General Thoughts: Global chemical profit improvement in the near term depends less on cyclical recovery and more on rationalized capacity, cost integration, and policy agility

General Thoughts: Chemical feedstock volatility is uneven and mostly net-margin negative, as derivative demand stays soft into early November and rationalization, not restarts, is broadly

General Thoughts: Global chemical sector margin compression is reprogramming markets as returns migrate from volume to precision, with integration, agility, and cost discipline eclipsing geographic

General Thoughts: Feedstock volatility is uneven and mostly net margin negative, as weak derivative demand keeps chemical profits under pressure in late October, with supply

General Thoughts: Shifting energy costs, tighter margins, and policy uncertainty redraw the global chemicals map, favoring integrated, flexible producers but pressuring most in a demand-