Sunday Executive Summary

The Middle East conflict is forcing risk-priced decisions, where volatility and uncertainty directly alter capital allocation, contract durations, and required return thresholds across markets.

Buyers

The Middle East conflict is forcing risk-priced decisions, where volatility and uncertainty directly alter capital allocation, contract durations, and required return thresholds across markets.

Buyers

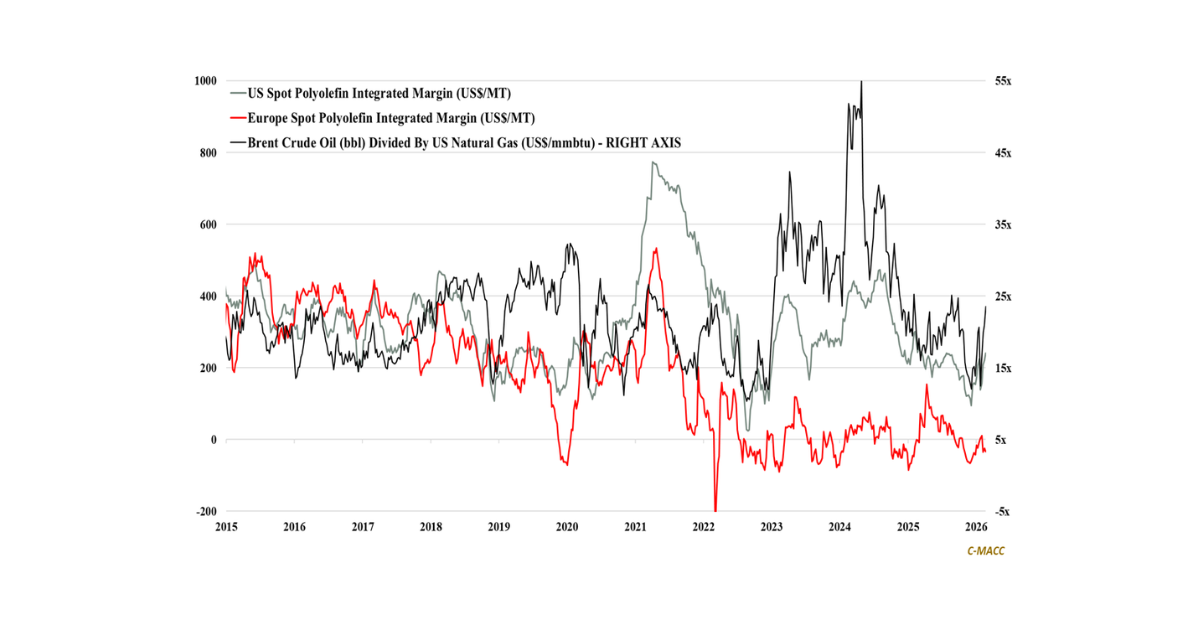

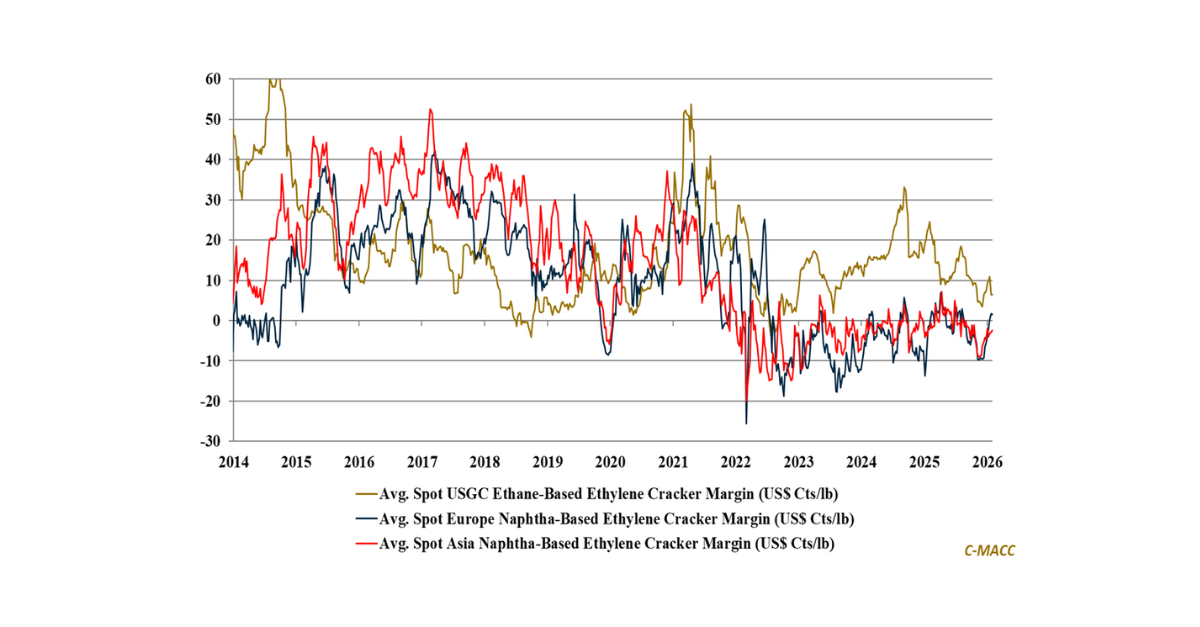

Europe’s chemical sector return outlook now hinges far less on cyclical recovery and far more on feedstock structure, carbon exposure, and policy-backed demand durability amid

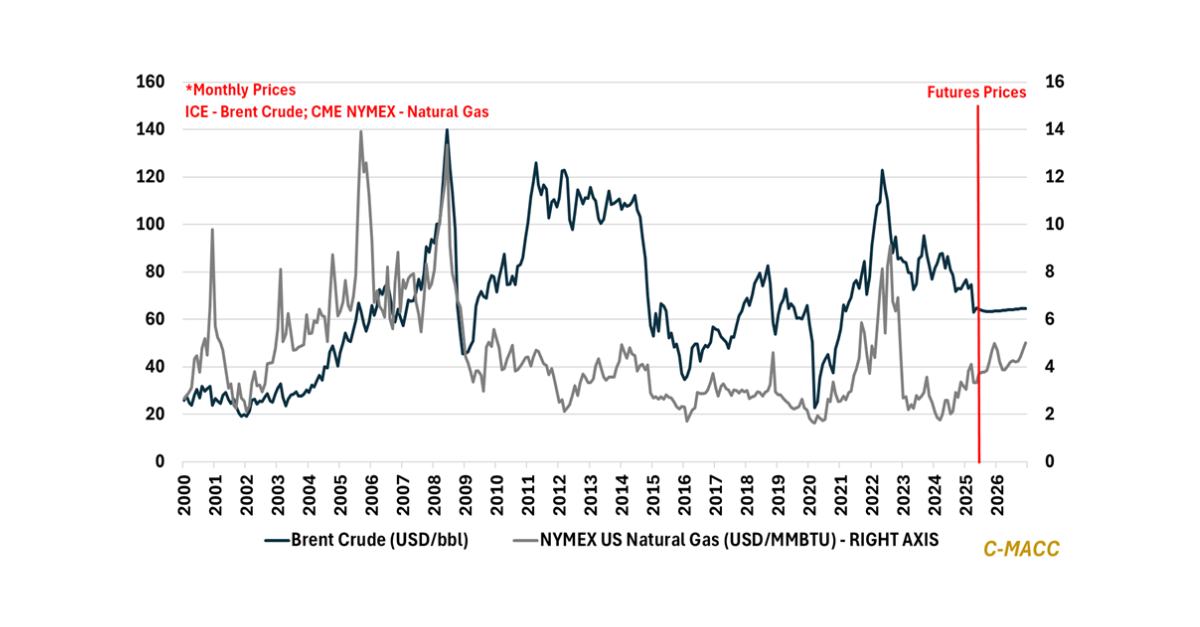

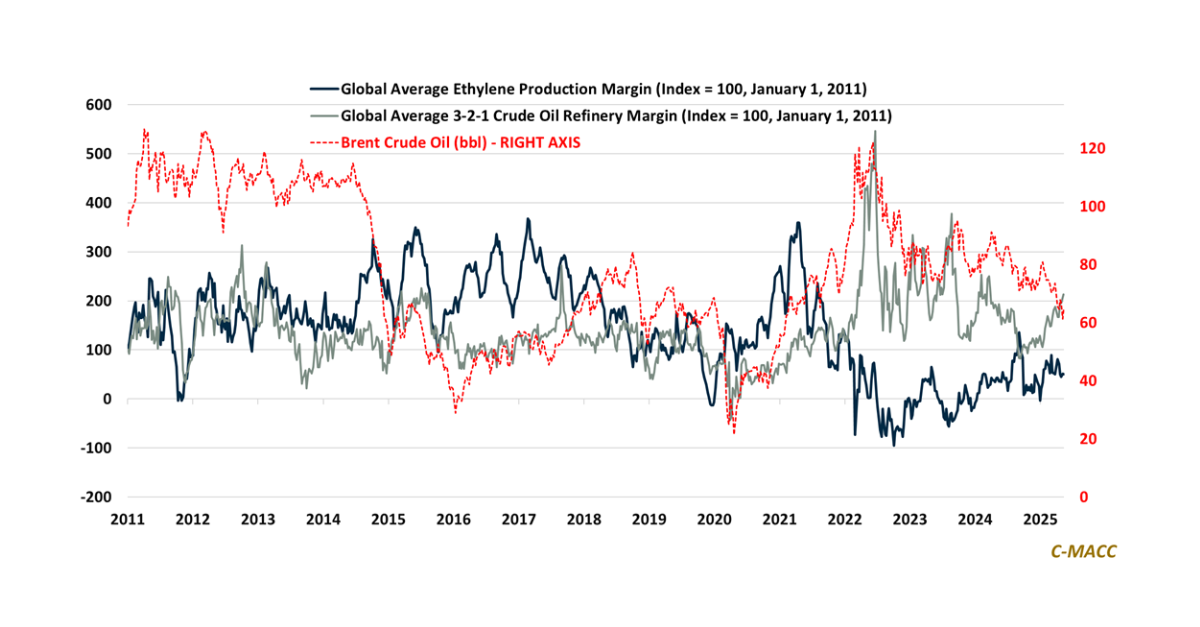

General Thoughts: Energy retracement and post-storm natural gas normalization begin to restore relative cost balance, enabling advantaged producers to outperform, while persistent oversupply constrains pricing

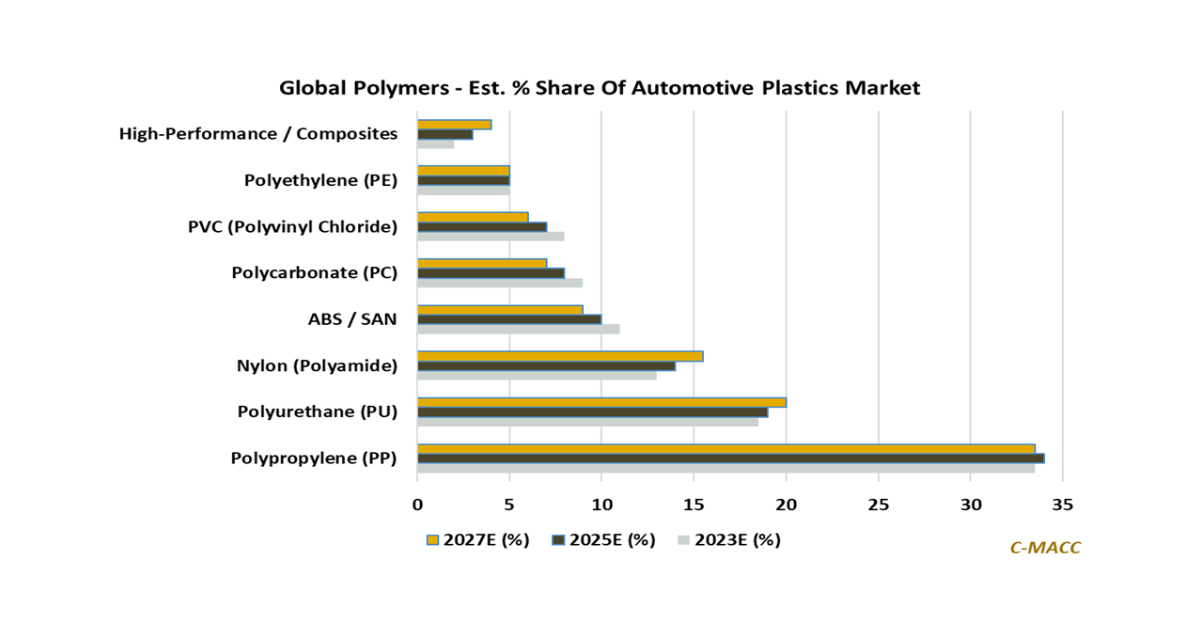

Automotive polymer demand decouples from unit growth, shifting toward lifecycle intensity and system-driven specifications where performance assurance, recyclability, and circular compliance define material value.

Integration

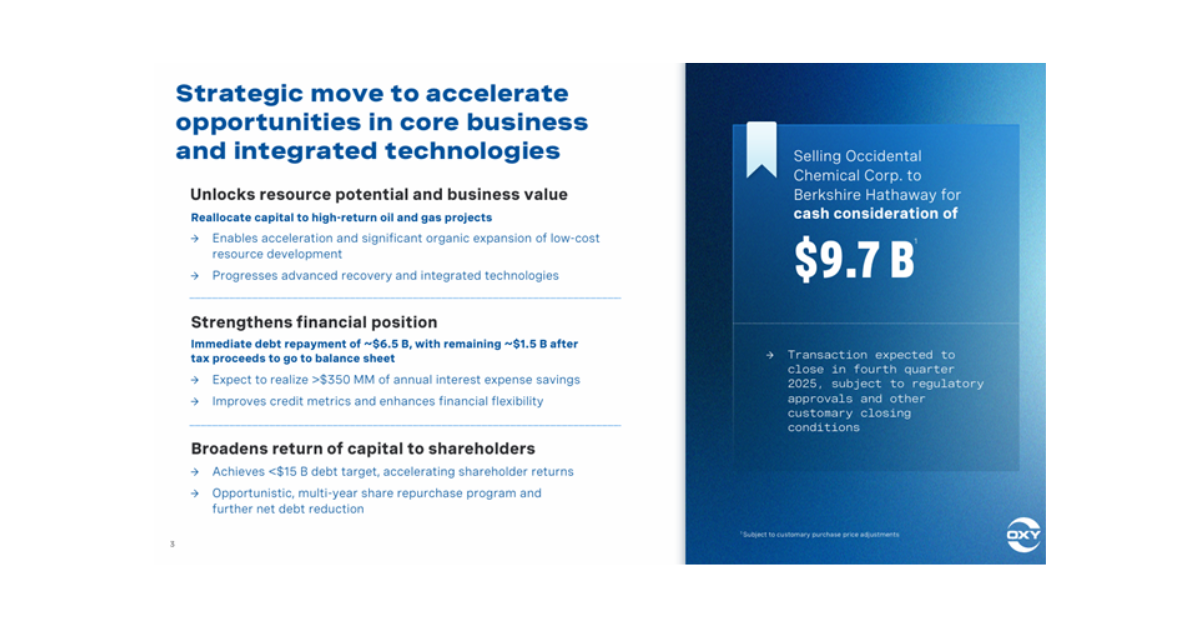

Global Market Analysis Optionality Engineered: Strategic Shifts Forge Disciplined Path to Returns Key Findings Exhibit 1: Berkshire’s acquisition of Oxychem bolsters Oxy’s financials in exchange

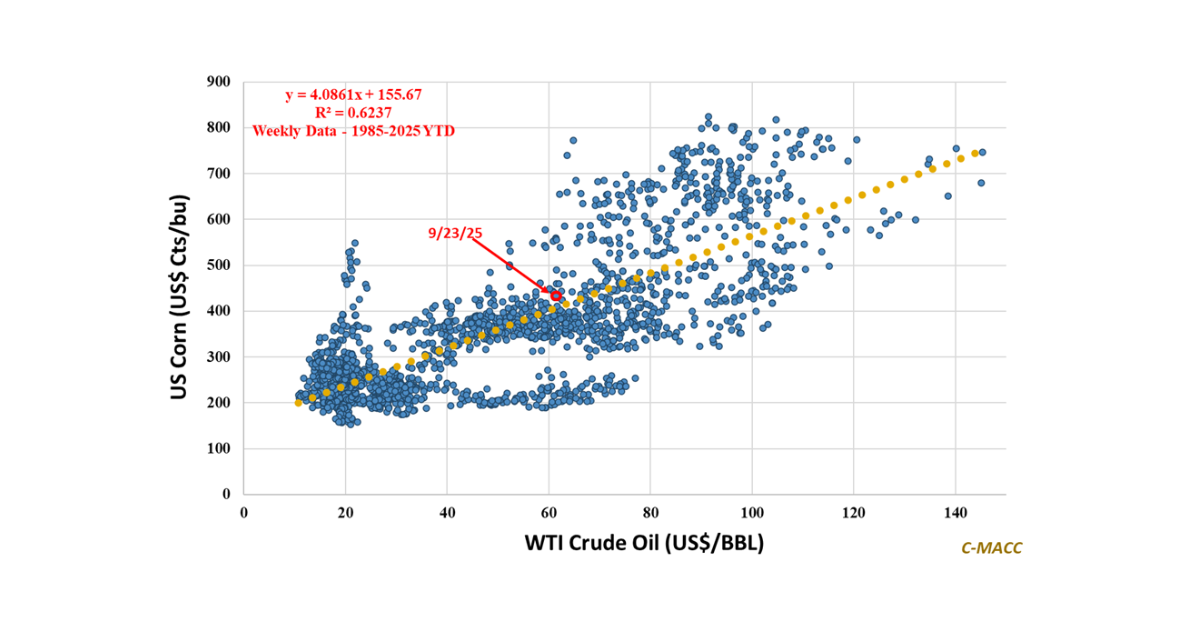

General Thoughts: Energy–agriculture linkages redefine global competitiveness and cost trajectories, reshaping inflation pathways, trade flows, investment decisions, and strategic resilience in late 2025 and 2026.

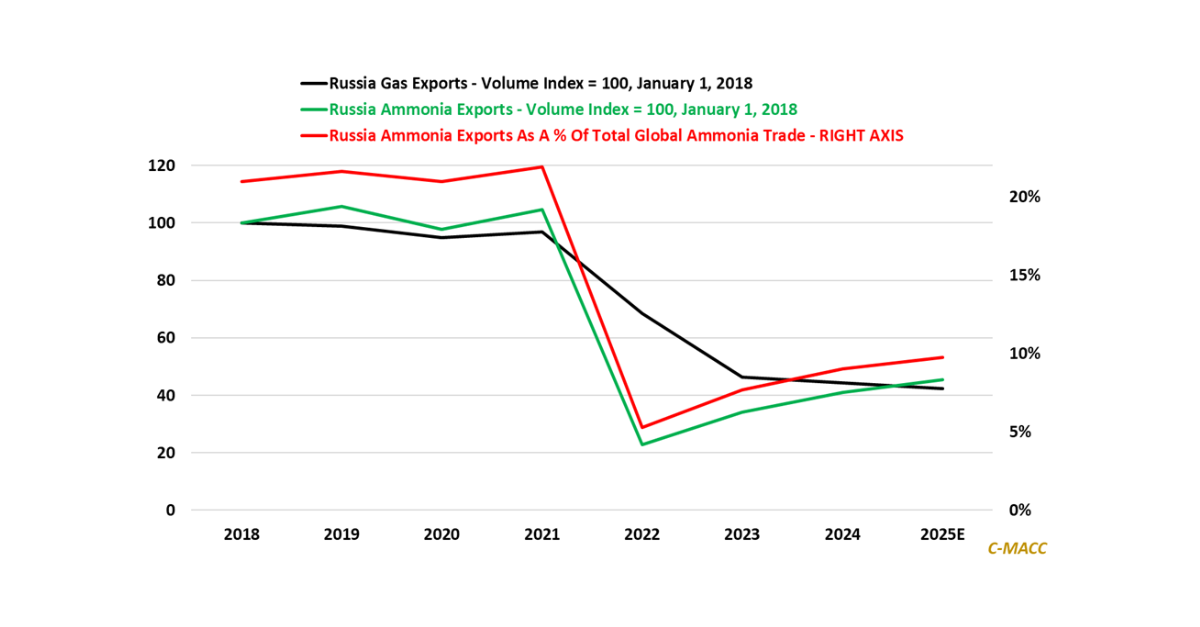

Fertilizer resilience highlights how geopolitical carve-outs create durable moats, making sanction circumvention, rerouting agility, and compliance sophistication as valuable as traditional feedstock advantage.

Ammonia’s contrasting

Integration isn’t a choice—it’s the new competitive design. Fragmented US models absorb volatility; state-aligned systems deflect it, reallocating shocks and defending margins through unified industrial

General Thoughts: Deep feedstock-to-chemical integration is not just a strategy—it is accelerating structural disruption and holds the potential to redraw the map of global industrial

Radical shifts are needed in the European Chemical industry, and the moves announced by BASF this week suggest that the company is positioning itself better