Sunday Executive Summary

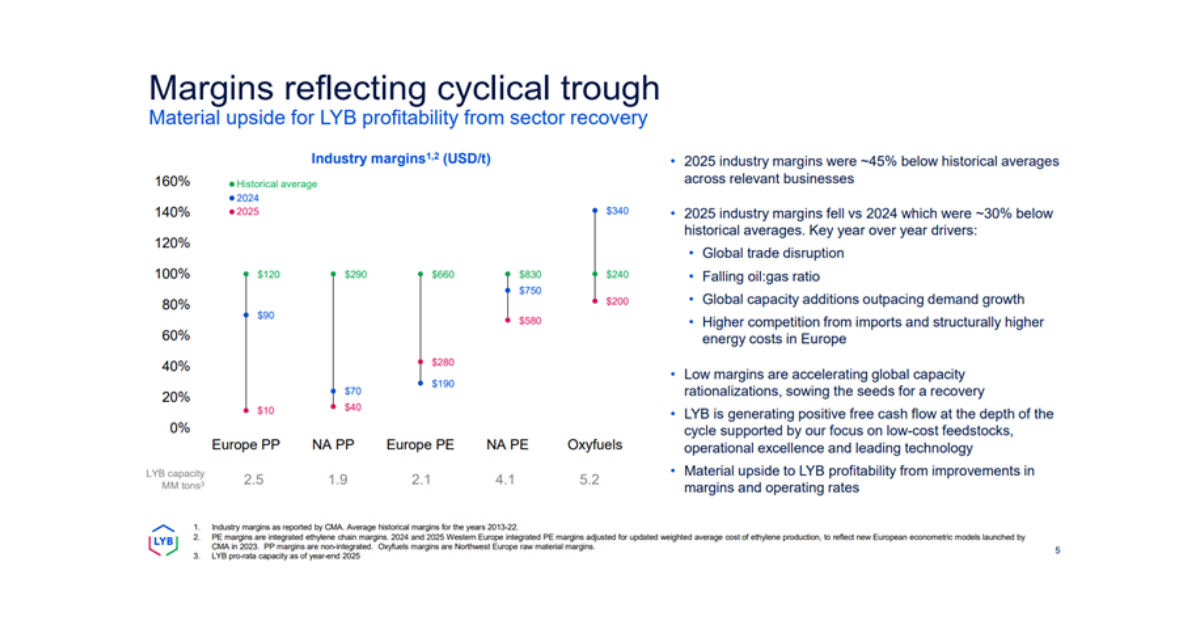

Prolonged petrochemical weakness reflects oversupply not demand collapse, extending the cycle and shifting strategy from growth to margin defense, cost-curve control, and execution-led recovery outcomes.

Prolonged petrochemical weakness reflects oversupply not demand collapse, extending the cycle and shifting strategy from growth to margin defense, cost-curve control, and execution-led recovery outcomes.

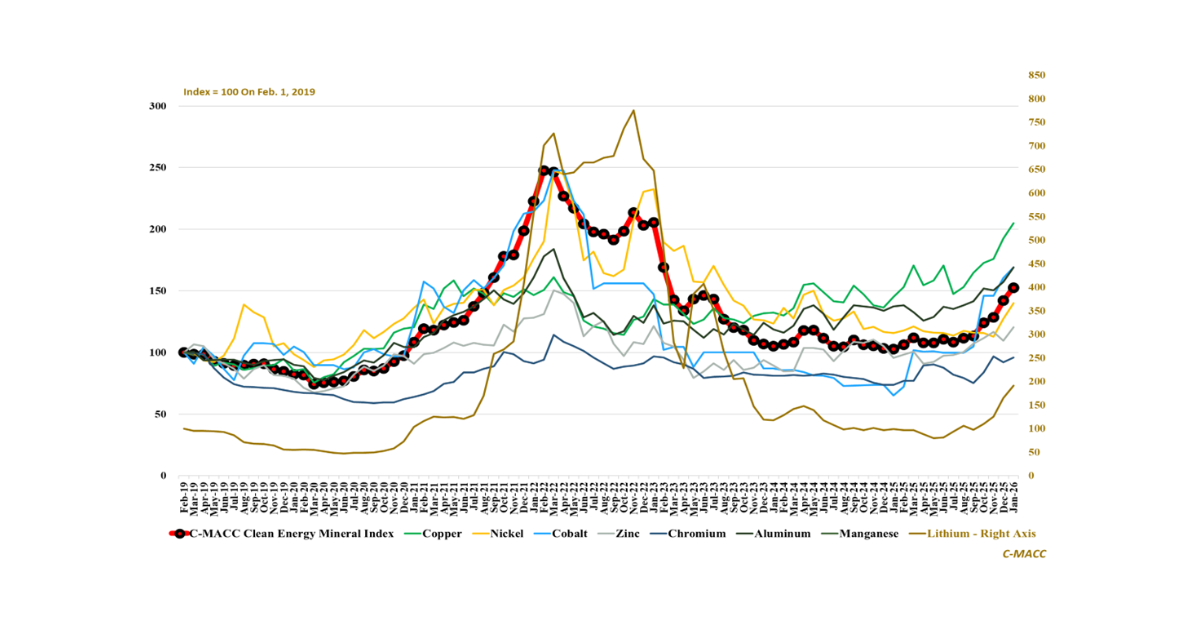

1st Topic of the Week: Critical mineral markets increasingly reward faster processing execution with cost and value-chain advantages, but will compressed timelines undermine return profiles

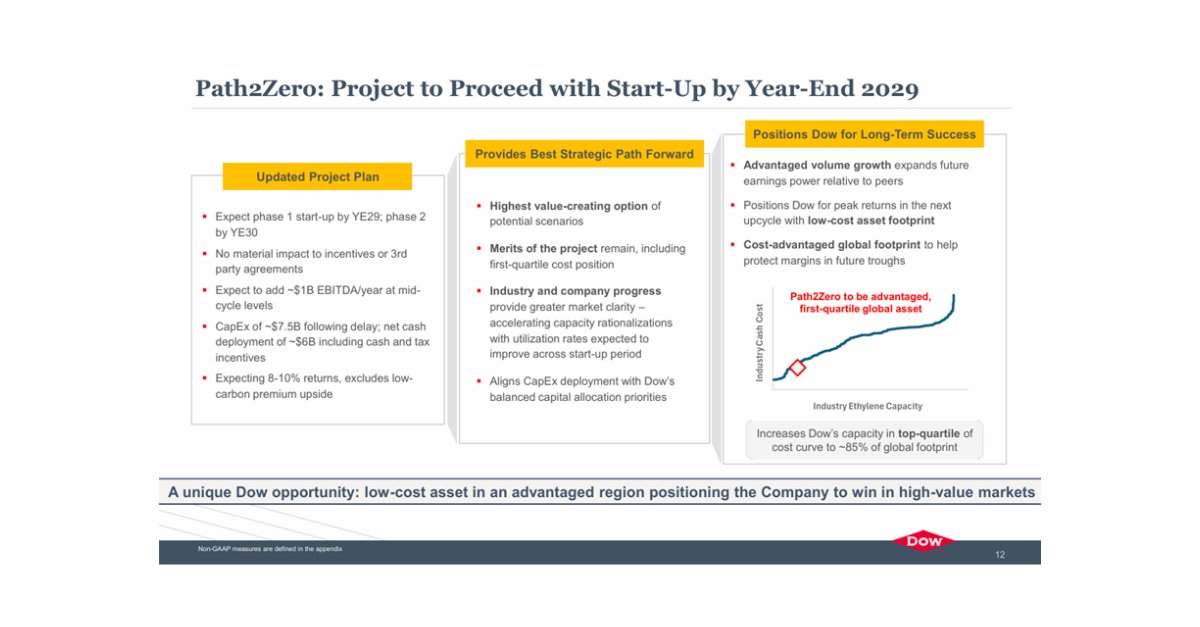

General Thoughts: Global chemical restructuring optimizes footprints, shrinks effective supply, and embeds optionality, positioning low-cost, low-carbon assets like Dow’s Path2Zero to lift returns in the

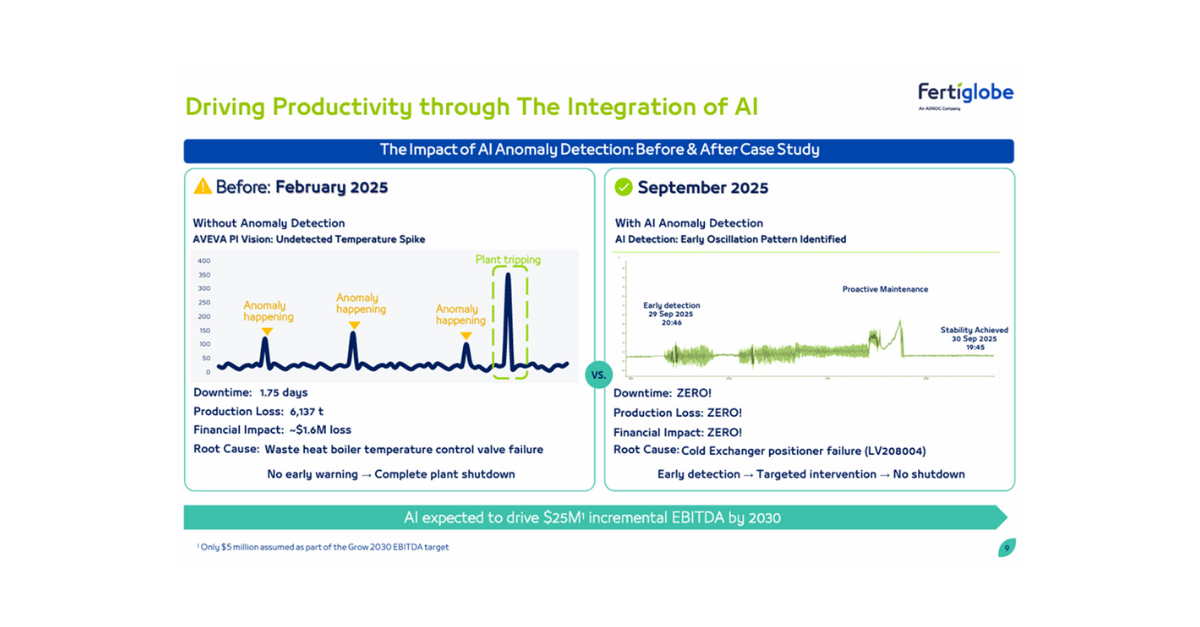

General Thoughts: AI-driven optimization converts operational noise into margin clarity, embedding predictive reliability, capital sequencing, and digital decision velocity across complex global industrial systems.

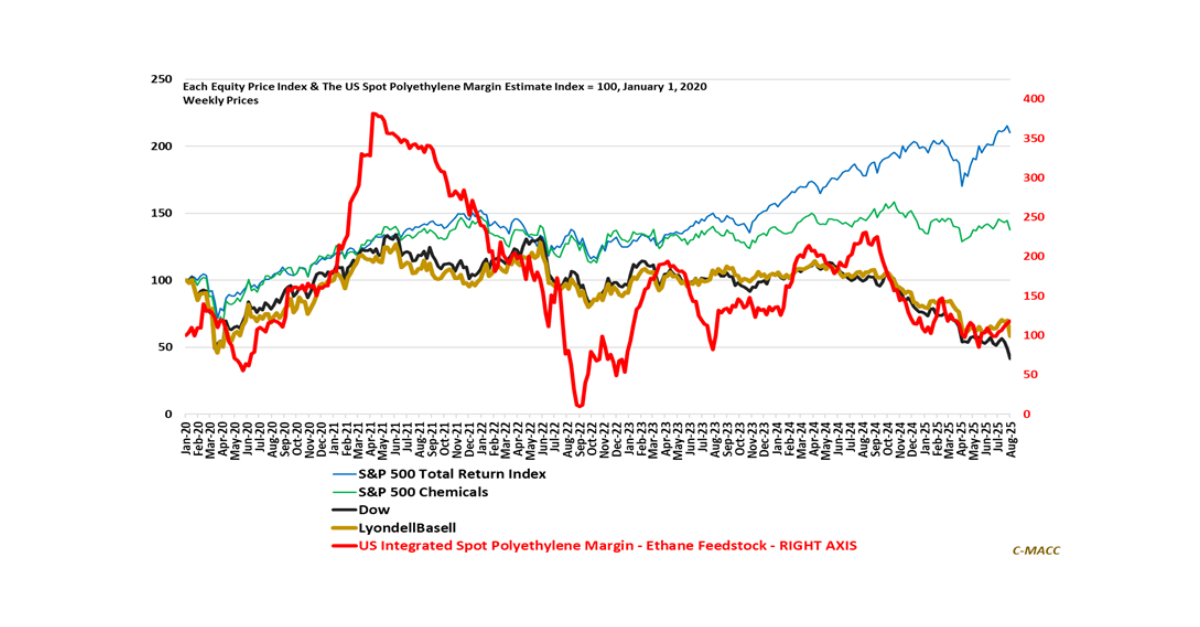

Supply

Capital deployment in the current market setting favors the orchestration of precision over the pursuit of scale, sequenced only when sufficient risk-adjusted returns, timing leverage,

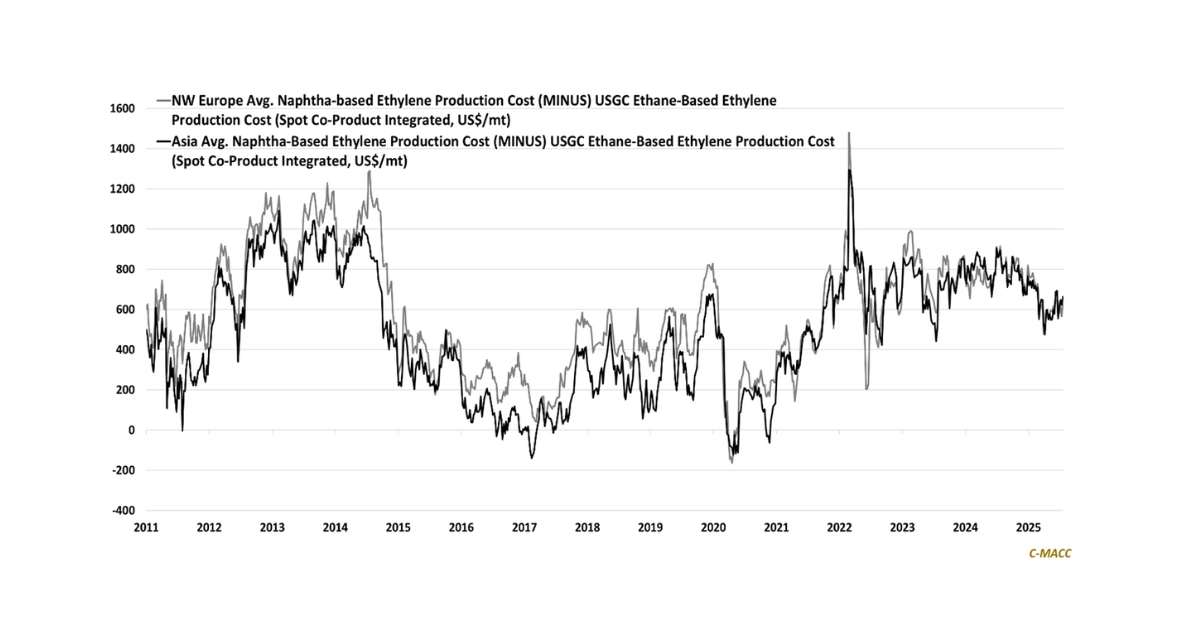

General Thoughts: The US-EU trade deal could quietly fracture EU cracker economics by taxing co-products, lifting integrated costs, and triggering accelerated rationalization across Europe’s naphtha-based

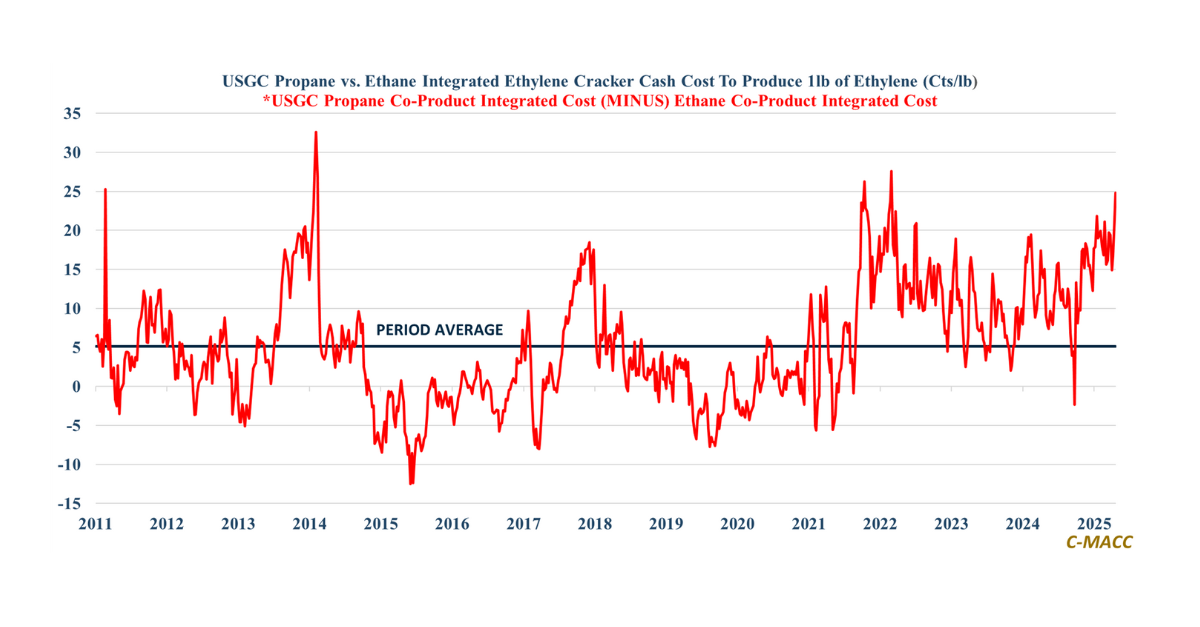

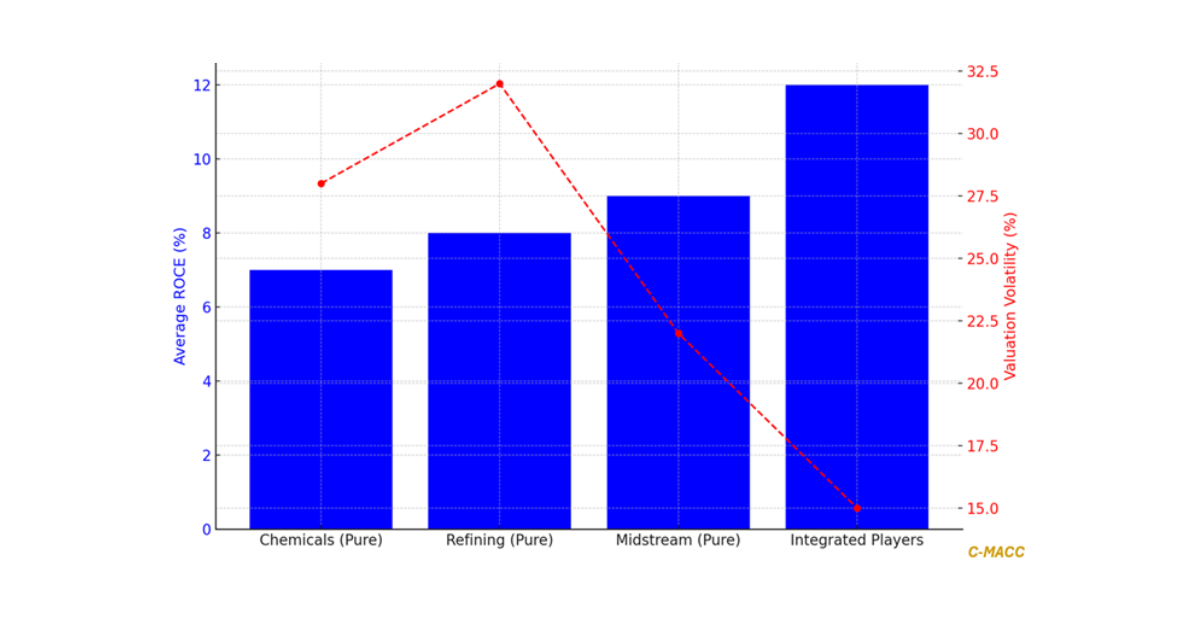

Vertical integration — via low-cost feedstocks or downstream differentiation — builds structural resilience, helping absorb shocks, protect margins, and outlast undifferentiated commodity strategies across cycles.

General Thoughts: US-integrated chemical producers and midstream players gain as global feedstock pulls intensify and rising Chinese integration reshapes markets, tightening margins for US ethylene

Structural flexibility — not theoretical options — often defines who survives, consolidates, and leads when global energy and chemical markets fracture into volatility, opportunity, and

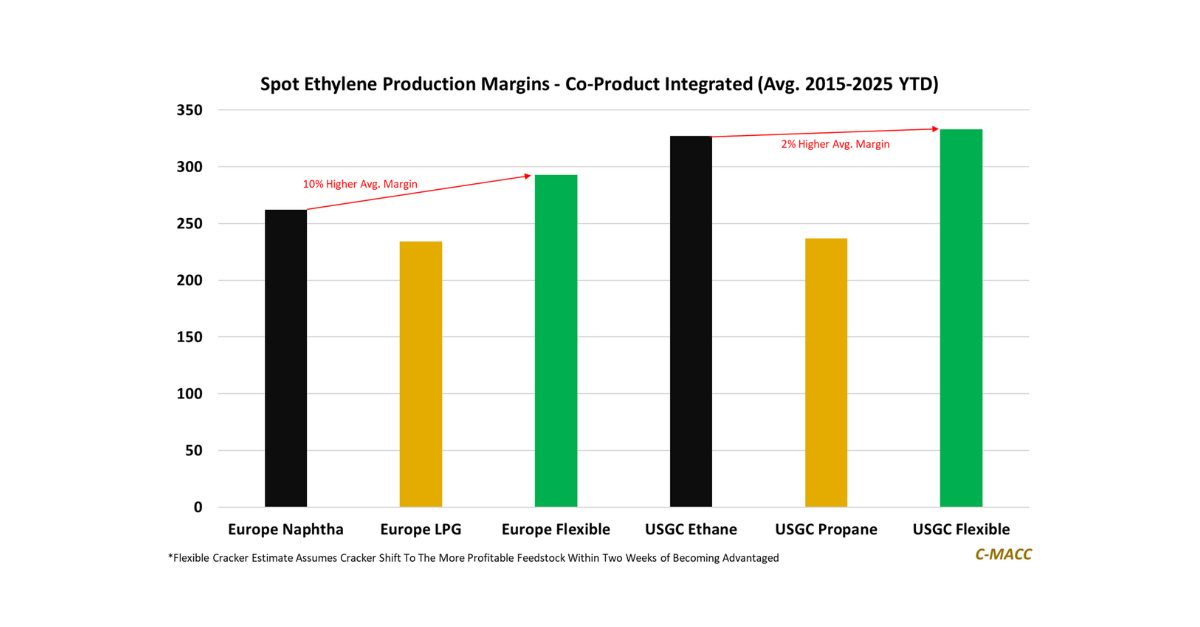

General Thoughts: In volatile, oversupplied markets, feedstock flexibility—while costly to build—enables higher, more stable risk-adjusted returns, separating producers like Dow from less adaptive peers facing