Global Market Analysis

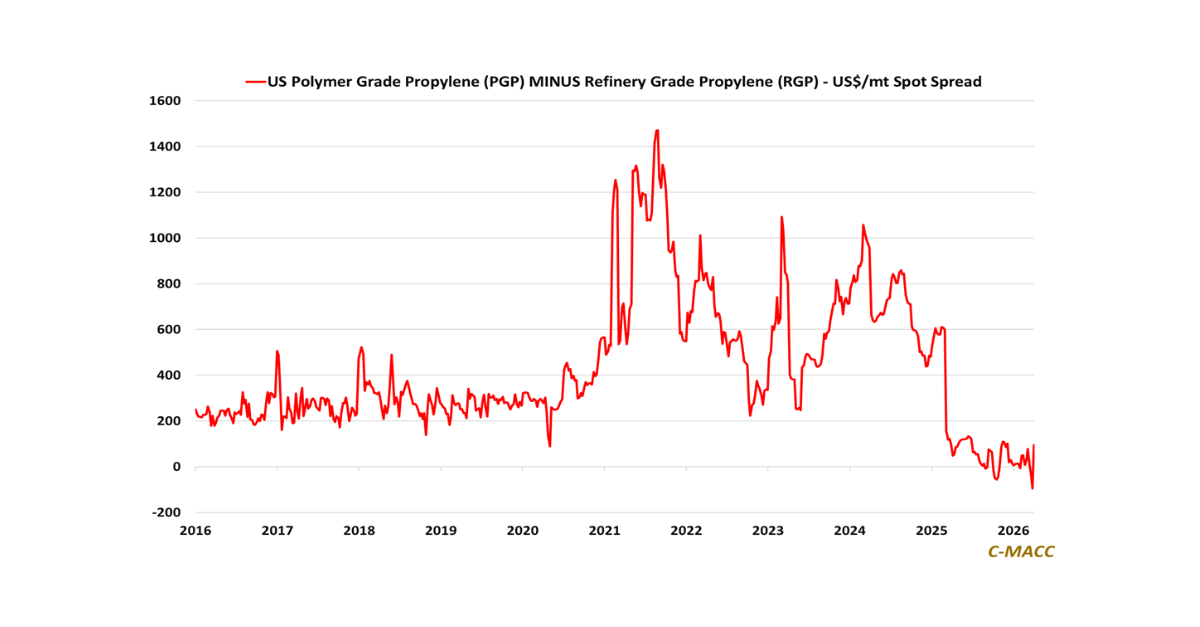

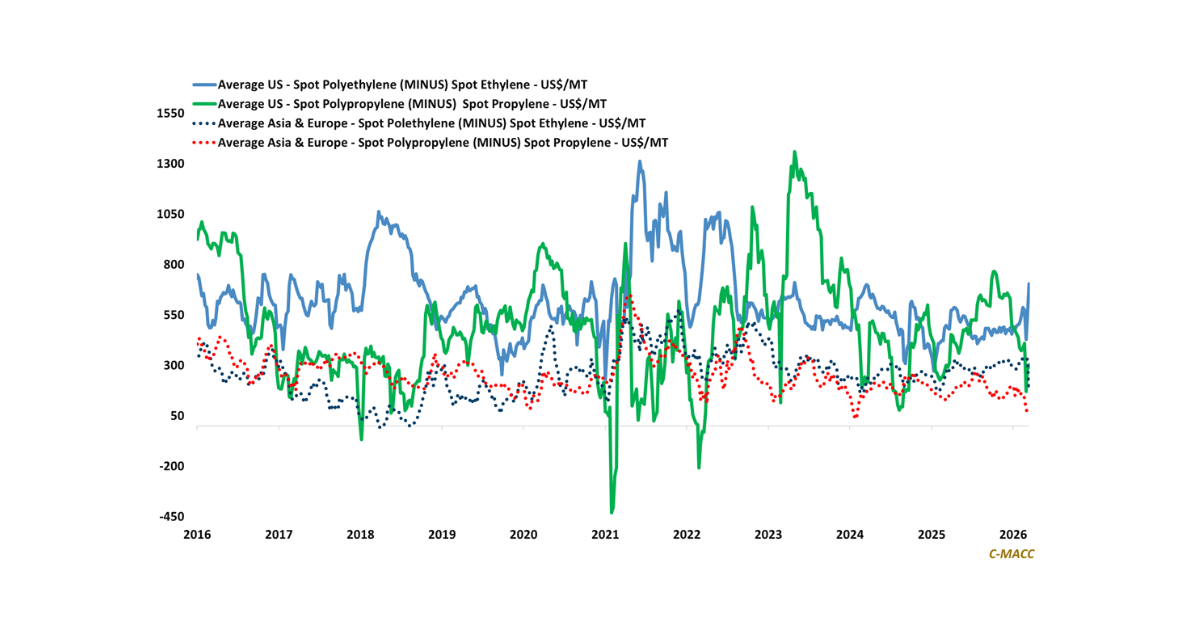

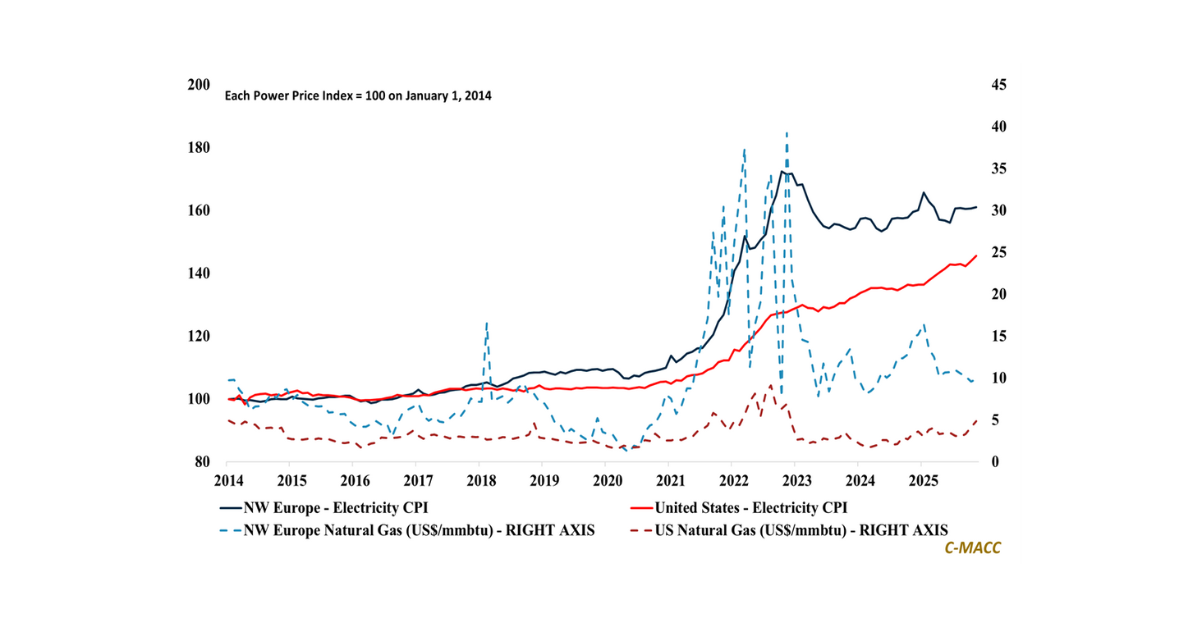

General Thoughts: US relative cost advantages persist, but rising global prices are compressing downstream margins as exports rise and cost transmission accelerates across global industrial

General Thoughts: US relative cost advantages persist, but rising global prices are compressing downstream margins as exports rise and cost transmission accelerates across global industrial

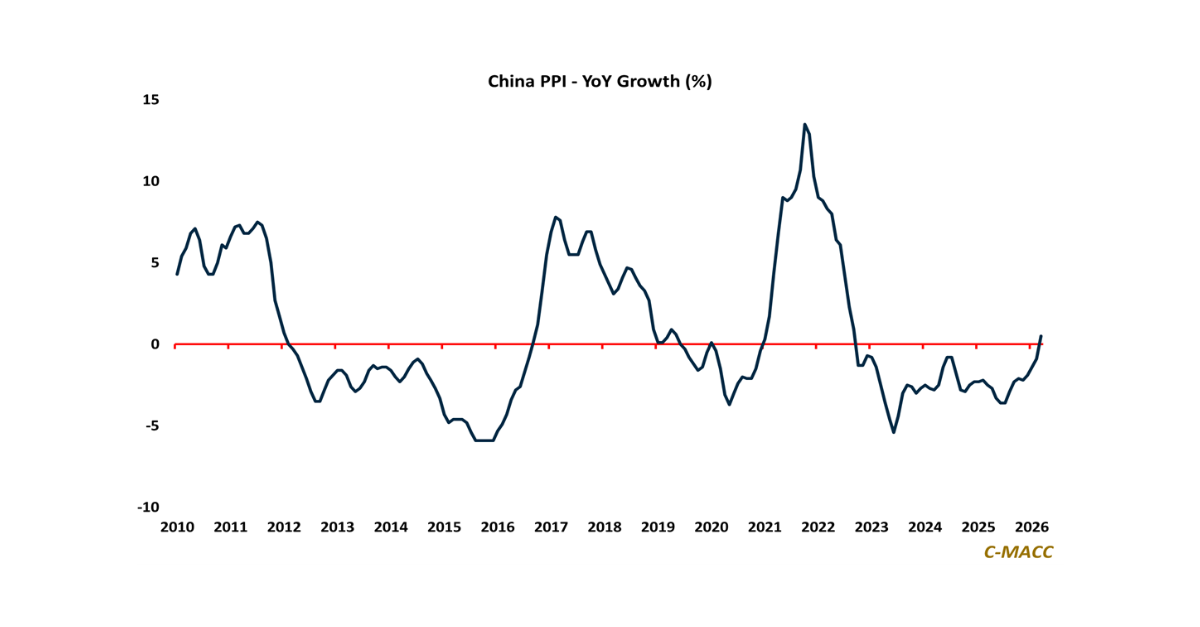

China’s 0.5% YoY factory-gate inflation in March removed a trusted global relief valve, forcing markets to underwrite firmer resin and intermediate floors, slower cost deflation,

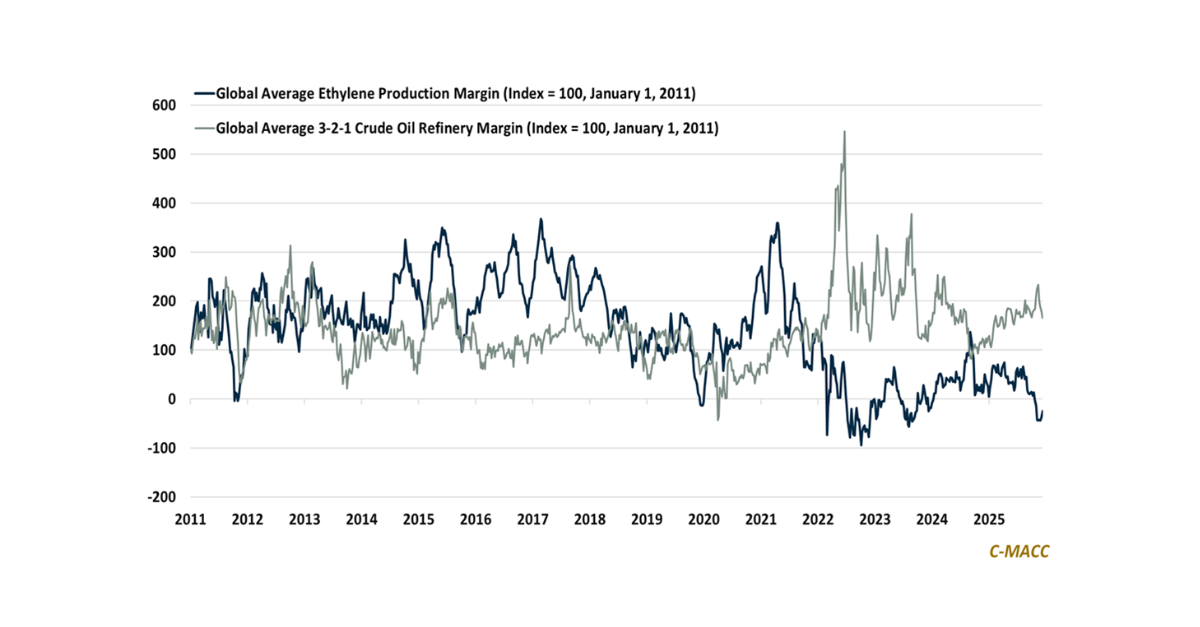

General Thoughts: Feedstock inflation is shifting profit pools upstream, forcing buyers to absorb volatility as reliability overtakes price and accelerates alternative supply in procurement decisions.

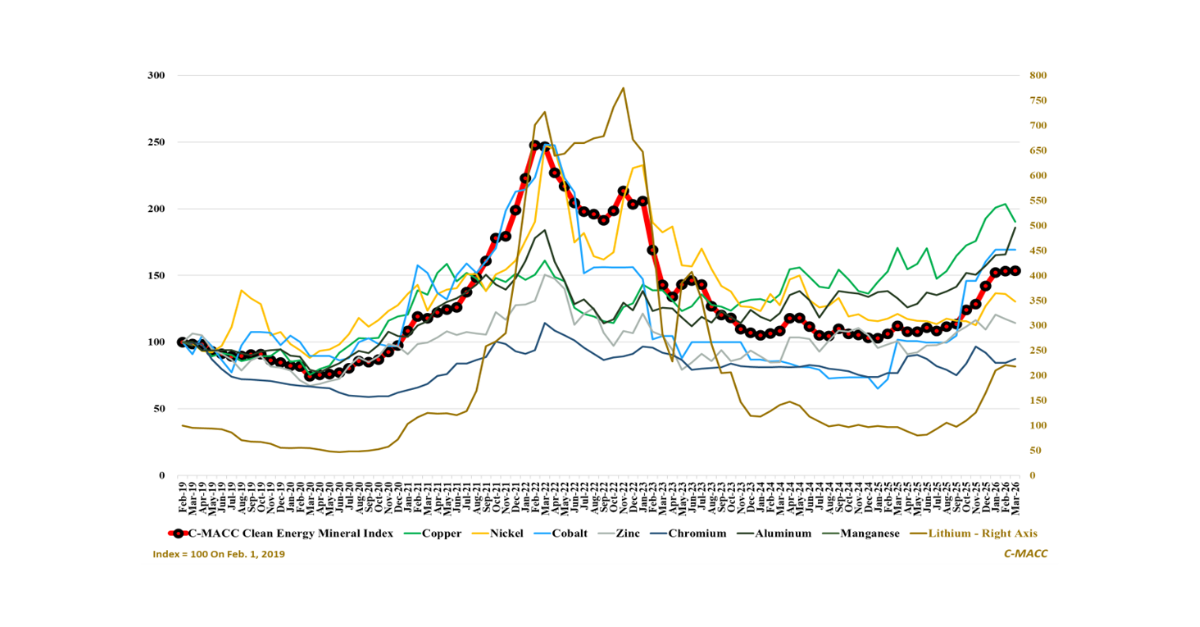

Critical minerals diverge as electrification costs fall structurally, confirming inputs are no longer the binding constraint and decisively shifting advantage toward systems that deliver reliable

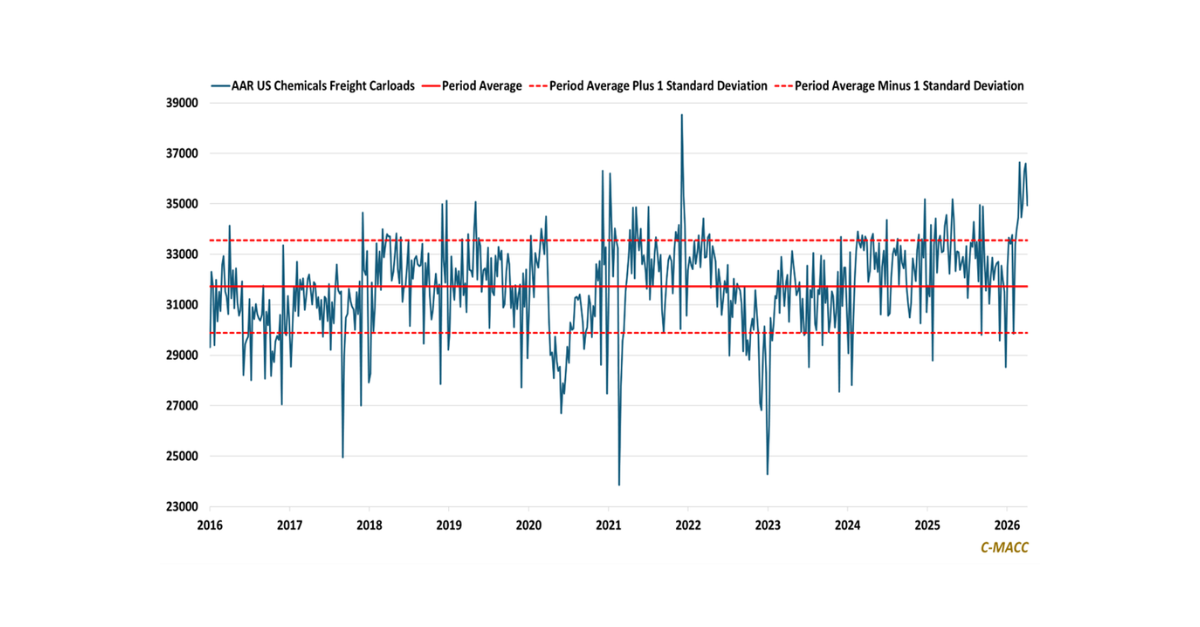

Dependable operations now define competitive advantage, with non-integrated assets losing ground as fragility disrupts throughput, raises risk, and weakens returns under stress.

Oil-linked feedstock systems

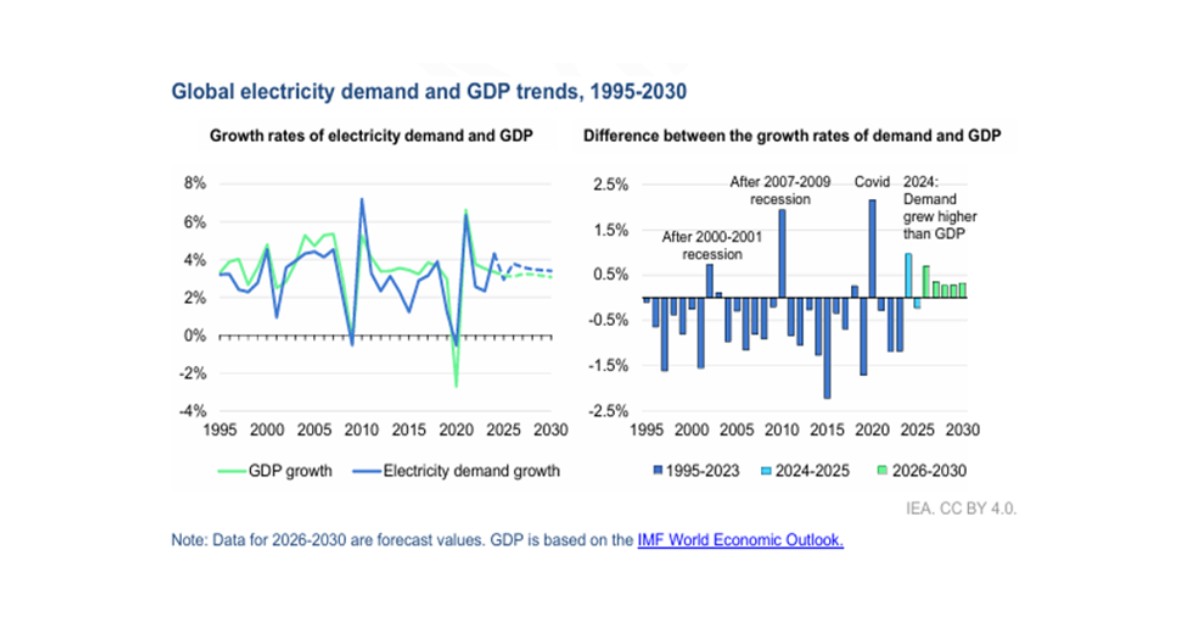

1st Topic of the Week: Electricity demand is positioned to outpace economic growth, shifting competitive advantage toward regions with secure, scalable power access, reliable infrastructure,

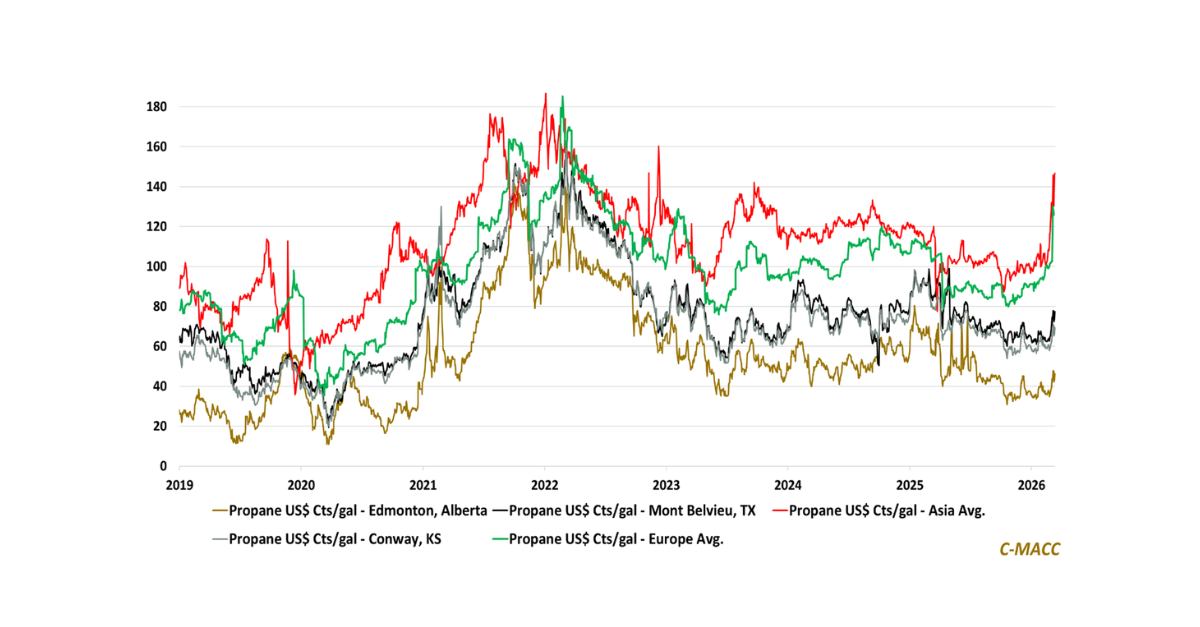

Asia and Europe now pay a structural propane premium as Middle East disruption risk lifts import costs, compressing PDH production margins abroad and reinforcing North

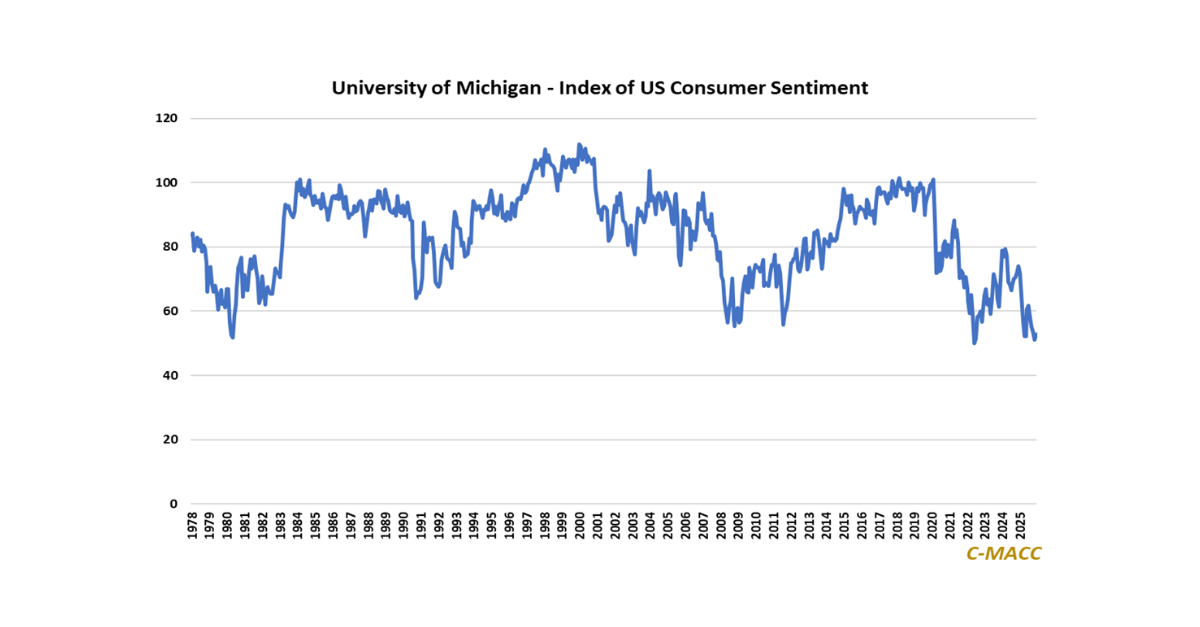

Depressed consumer sentiment and weak business expectations imply demand will not offset oversupply, with 2026 outcomes more likely to be determined by restructuring discipline rather

Chemical sector outcomes in 2026 will hinge more on managing volatility across power, gas, and policy, not on forecasting averages, as infrastructure constraints and capital

General Thoughts: Global average ethylene production margins collapsed in early 4Q25 then stabilized modestly, but only restructuring like high-cost cracker closures can loosely replicate refining’s