Sunday Executive Summary

Route control sets the margin gate as low-cost supply realizes less value when access owners or customers govern timing, price, outlet choice, and demand commitment

Route control sets the margin gate as low-cost supply realizes less value when access owners or customers govern timing, price, outlet choice, and demand commitment

General Thoughts: Weak returns are forcing strategic repair as producers separate, combine, or reposition assets to improve risk-adjusted returns rather than wait for cleaner demand,

Affordability constraints increasingly determine pricing durability as manufacturers defend margins through promotions, inventory timing, and customer prioritization rather than demand growth.

Reliable supply commands rising

The Middle East conflict is forcing risk-priced decisions, where volatility and uncertainty directly alter capital allocation, contract durations, and required return thresholds across markets.

Buyers

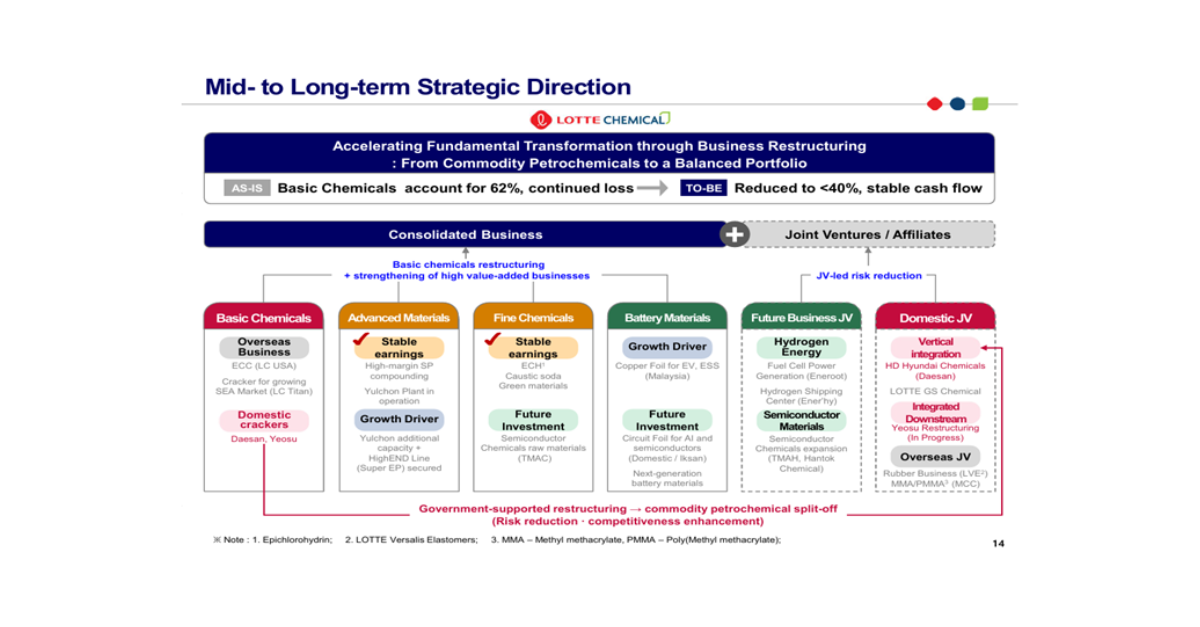

General Thoughts: Lotte’s Daesan spin-off signals forced restructuring across high-cost regions, where policy-backed capital enables consolidation and shifts value toward integrated, advantaged platforms.

Supply Chain/Commodities:

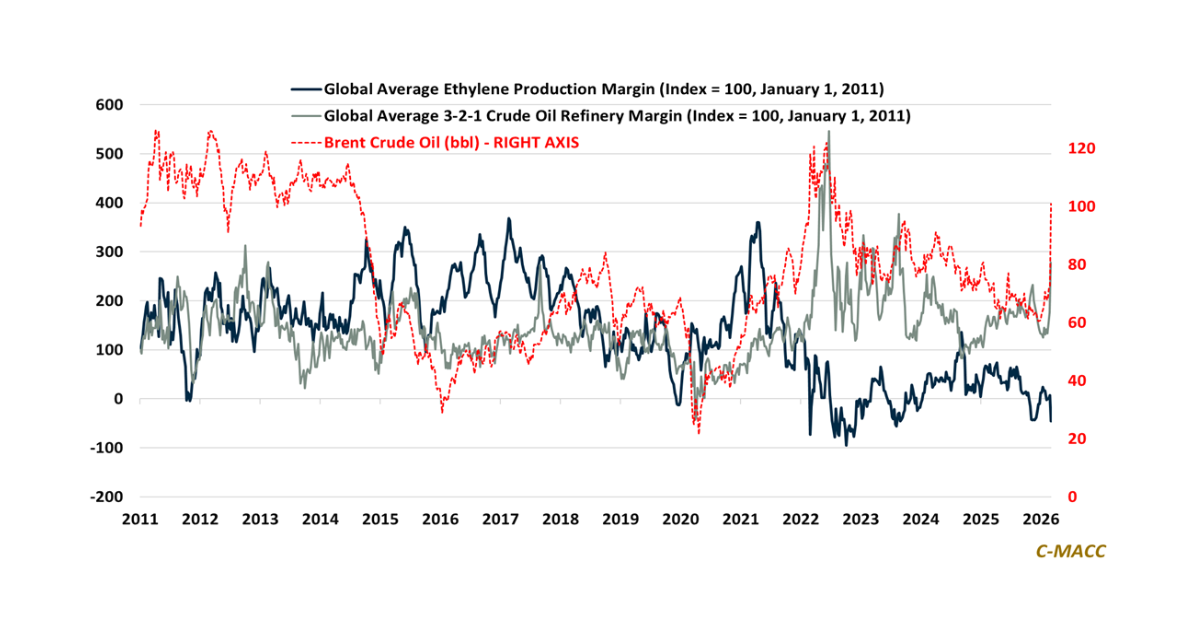

General Thoughts: Energy shocks are redistributing profitability across industrial value chains as surging ex-US energy costs compress petrochemical margins, tighten fertilizer markets, and strengthen North

General Thoughts: Global chemical markets are fragmenting across feedstocks, chemicals, and fuels, rewarding logistics, integration, and discipline, while exposing structurally misaligned assets to prolonged margin

General Thoughts: Energy retracement and post-storm natural gas normalization begin to restore relative cost balance, enabling advantaged producers to outperform, while persistent oversupply constrains pricing

General Thoughts: Across markets, tighter conditions are mainly driven by higher costs and lingering curtailments, not by demand, as US propylene firms WoW, while early-year

General Thoughts: Early-year chemical spot prices and relative feedstock cost movements suggest that the pace of restructuring and regional return-enhancement efforts will be more decisive