Global Market Analysis

General Thoughts: US relative cost advantages persist, but rising global prices are compressing downstream margins as exports rise and cost transmission accelerates across global industrial

General Thoughts: US relative cost advantages persist, but rising global prices are compressing downstream margins as exports rise and cost transmission accelerates across global industrial

1st Topic of the Week: As EPR increasingly shifts packaging economics, which value-chain players will redesign fastest to protect margins, and who risks absorbing compounding

1st Topic of the Week: Water scarcity poses a growing constraint to lithium production, with over half of global reserves in water-stressed regions—escalating risks of

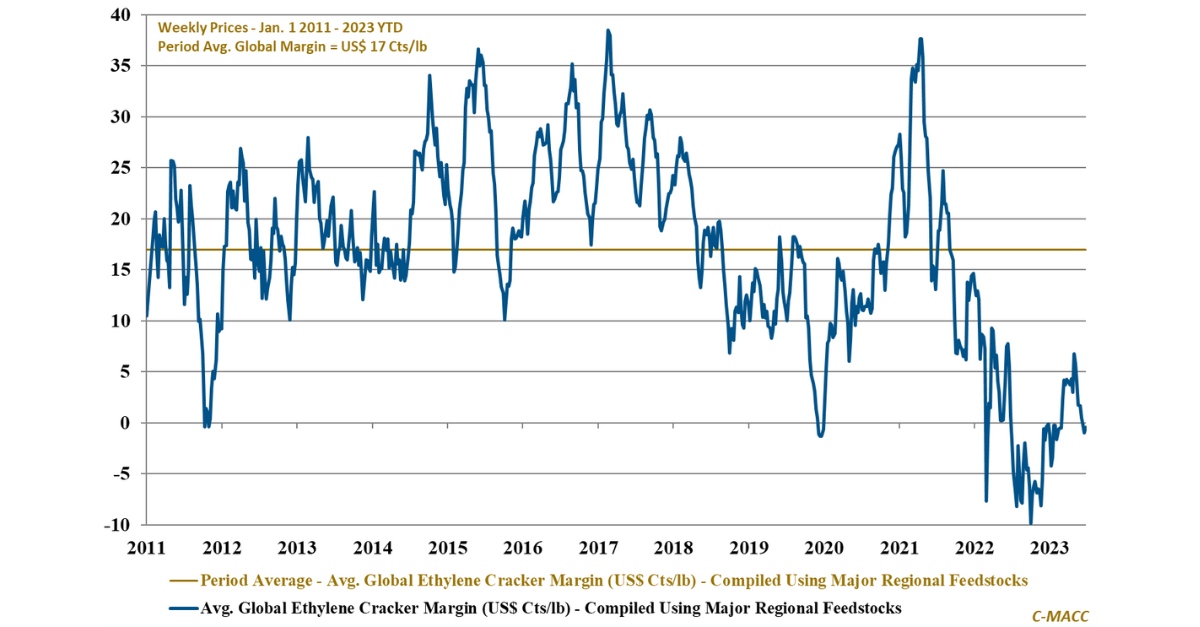

At several points over the last 40 years, ethylene co-products have been so valuable relative to feedstocks that ethylene has been free – US propane

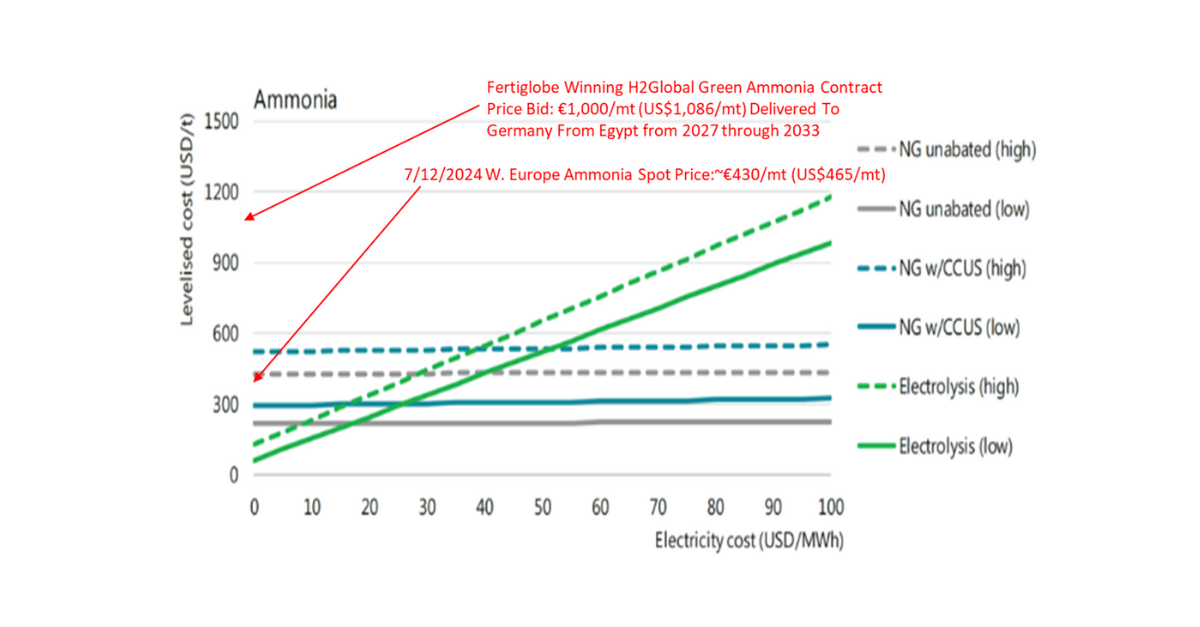

General Thoughts: We discuss efforts to subsidize green ammonia supplies from relatively low-cost areas to high-cost regions, highlighting the Fertiglobe winning the H2Global pilot auction

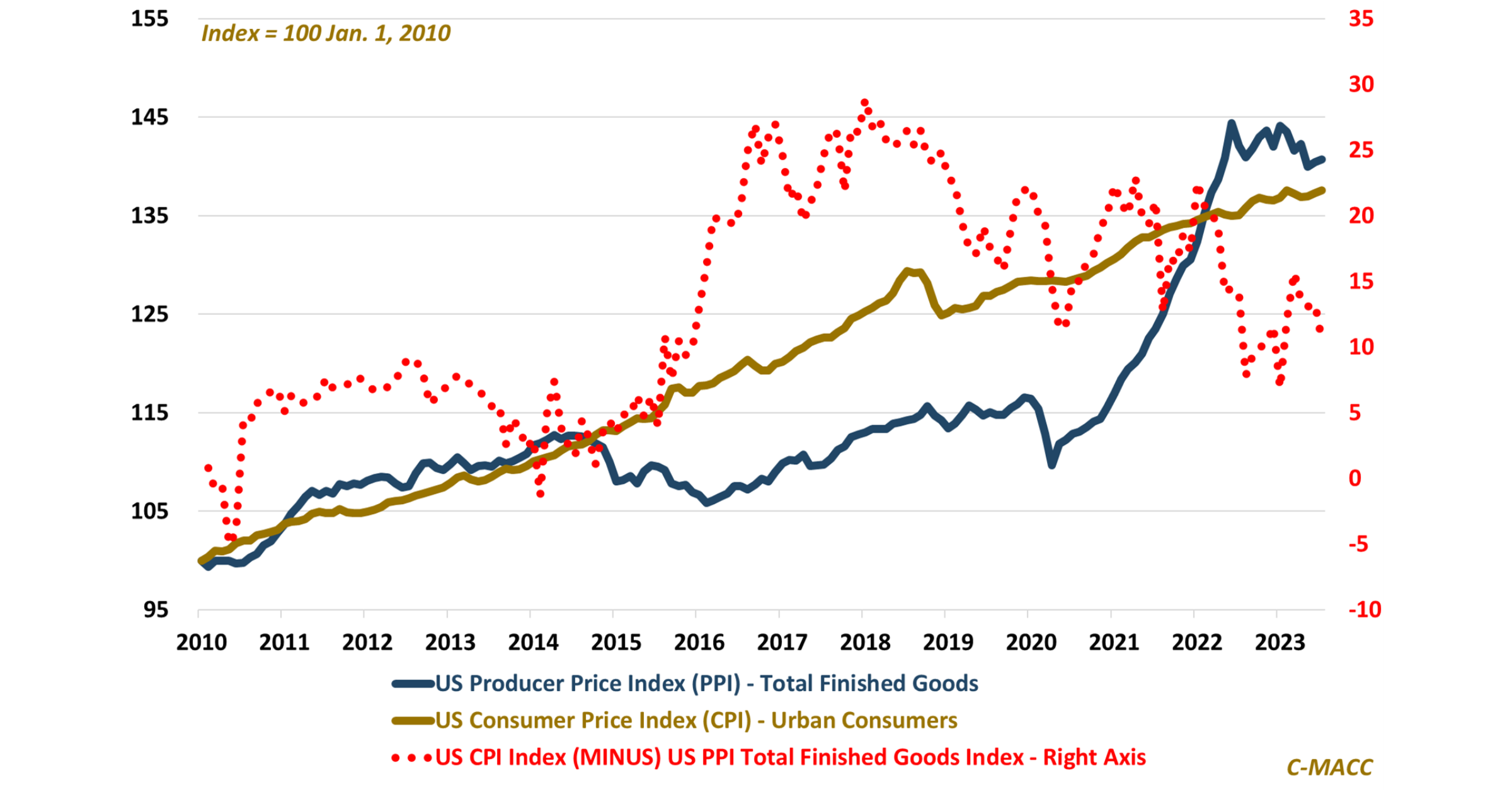

US prices increased at the consumer and wholesale level in July. While most indicators reflect price support in August, further strength, notably in petrochemicals, requires

Most chemical producers anticipate a weak 2H23 before improvement in 2024 – we view some markets, such as fertilizer and selectively in specialties, as better

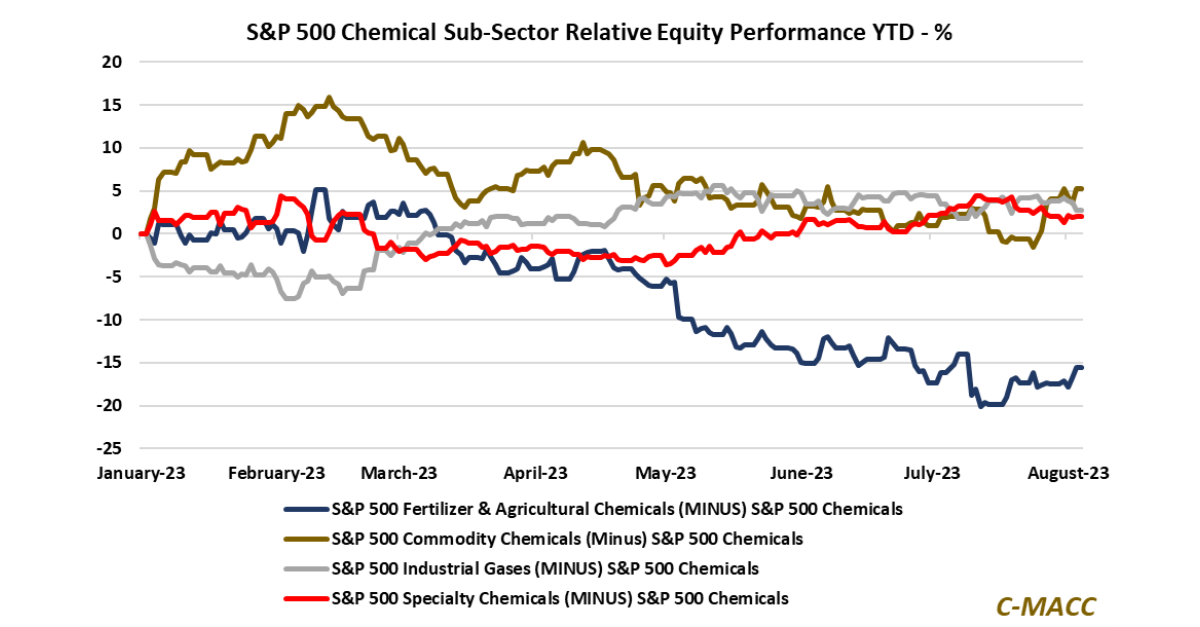

Global petrochemical markets began 3Q23 reflecting lower levels of profitability compared to 1H23, and conditions appear more likely to worsen in 2H23 than improve from

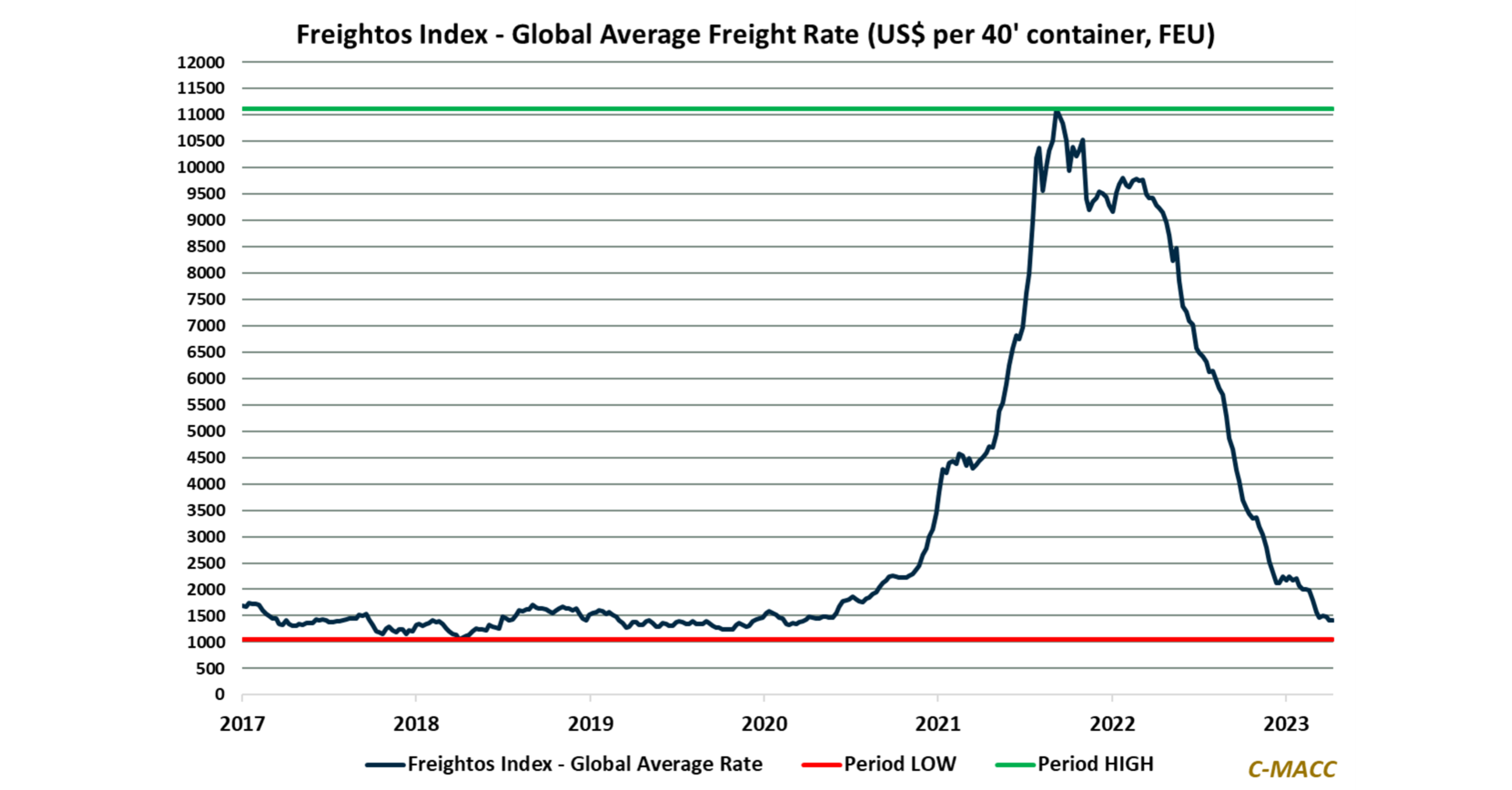

Global freight rates reflect downward pressure in 1H23, supporting the case for supply chain improvements and suggesting reduced commodity price differentials between regions in 2023.

Our theme around the possible need for backward integration for all basic chemical producers as energy transition evolves was validated by INEOS this week.

INEOS