Global Market Analysis

General Thoughts: US relative cost advantages persist, but rising global prices are compressing downstream margins as exports rise and cost transmission accelerates across global industrial

General Thoughts: US relative cost advantages persist, but rising global prices are compressing downstream margins as exports rise and cost transmission accelerates across global industrial

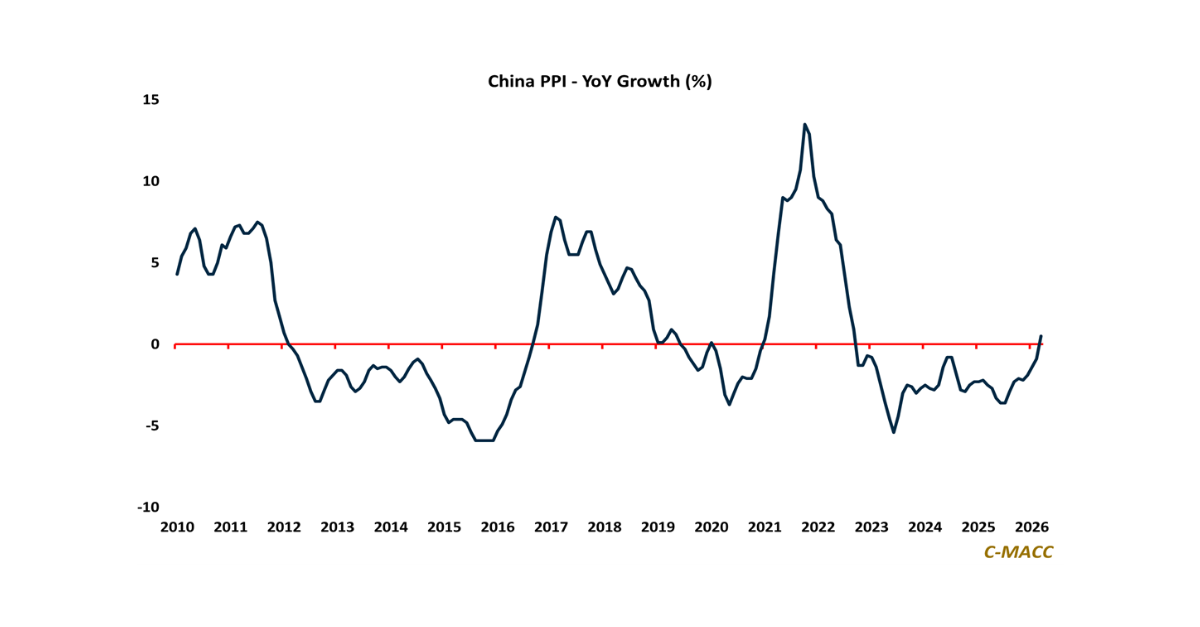

China’s 0.5% YoY factory-gate inflation in March removed a trusted global relief valve, forcing markets to underwrite firmer resin and intermediate floors, slower cost deflation,

General Thoughts: Industrial value is shifting toward integrated systems that manage energy, logistics, and continuity to protect margins, as disruption fragments markets and limits standalone

System constraints are compressing global corporate decision cycles, forcing capital into platforms that secure inputs, logistics, and execution simultaneously rather than optimizing sequentially across markets.

General Thoughts: Supply shocks are shifting power from cost to control, concentrating value in integrated systems as export-driven convergence reshapes demand, margins, and capital allocation

Dependable operations now define competitive advantage, with non-integrated assets losing ground as fragility disrupts throughput, raises risk, and weakens returns under stress.

Oil-linked feedstock systems

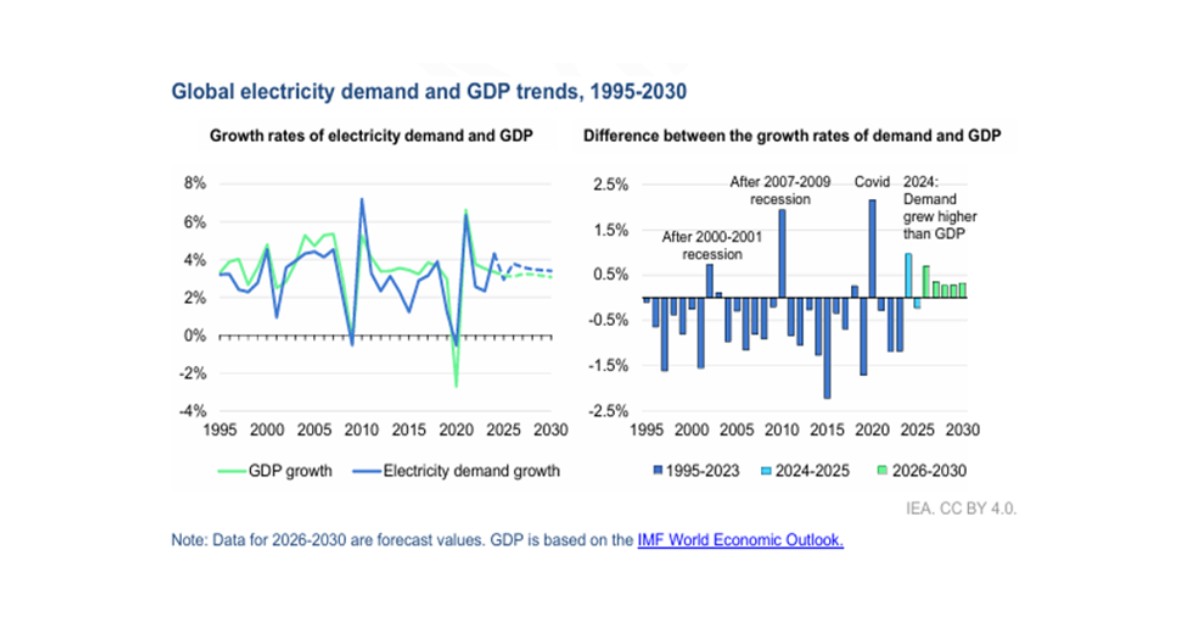

1st Topic of the Week: Electricity demand is positioned to outpace economic growth, shifting competitive advantage toward regions with secure, scalable power access, reliable infrastructure,

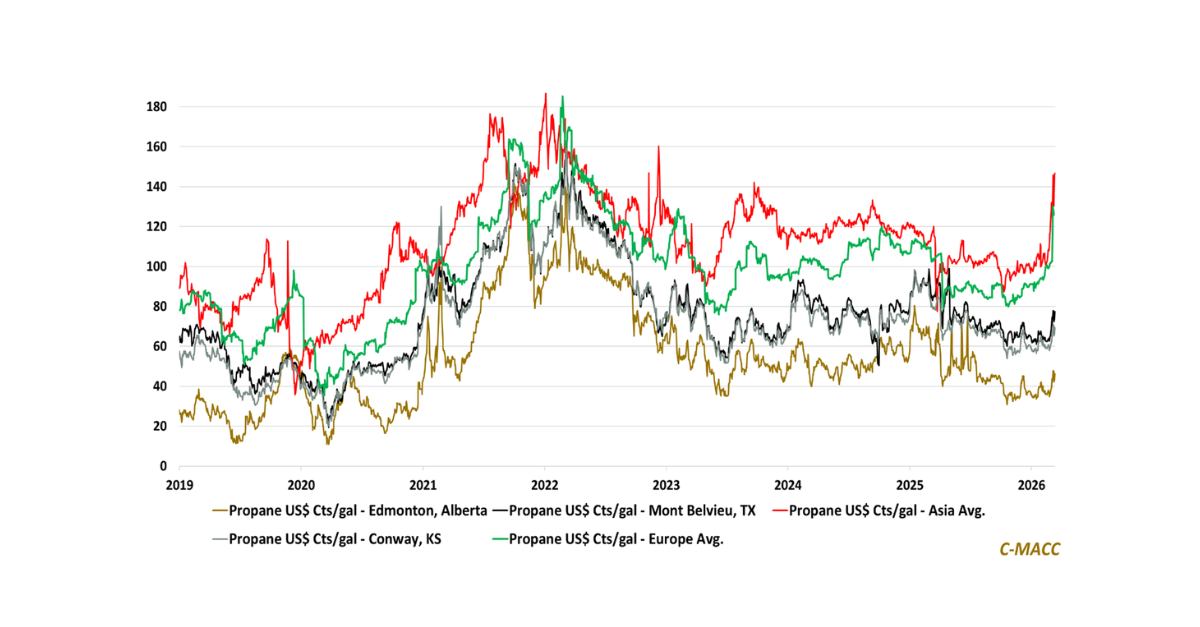

Asia and Europe now pay a structural propane premium as Middle East disruption risk lifts import costs, compressing PDH production margins abroad and reinforcing North

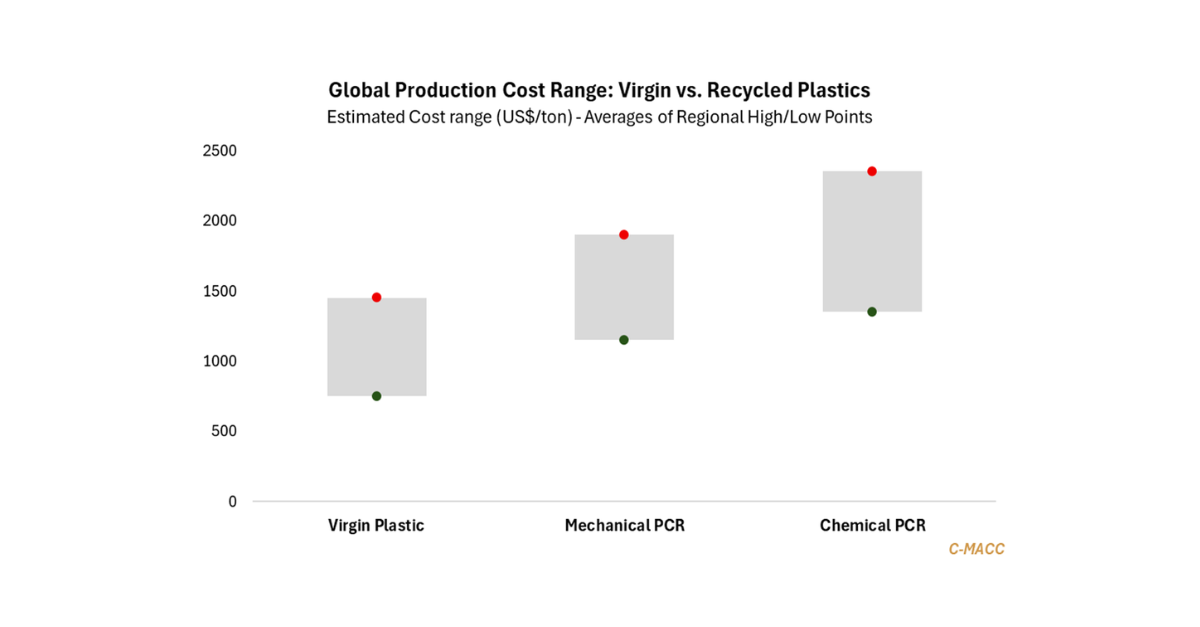

1st Topic of the Week: Energy-driven resin repricing narrows virgin-PCR gaps, benefiting circular adoption and shifting advantage toward suppliers that control feedstock, specification, and customer

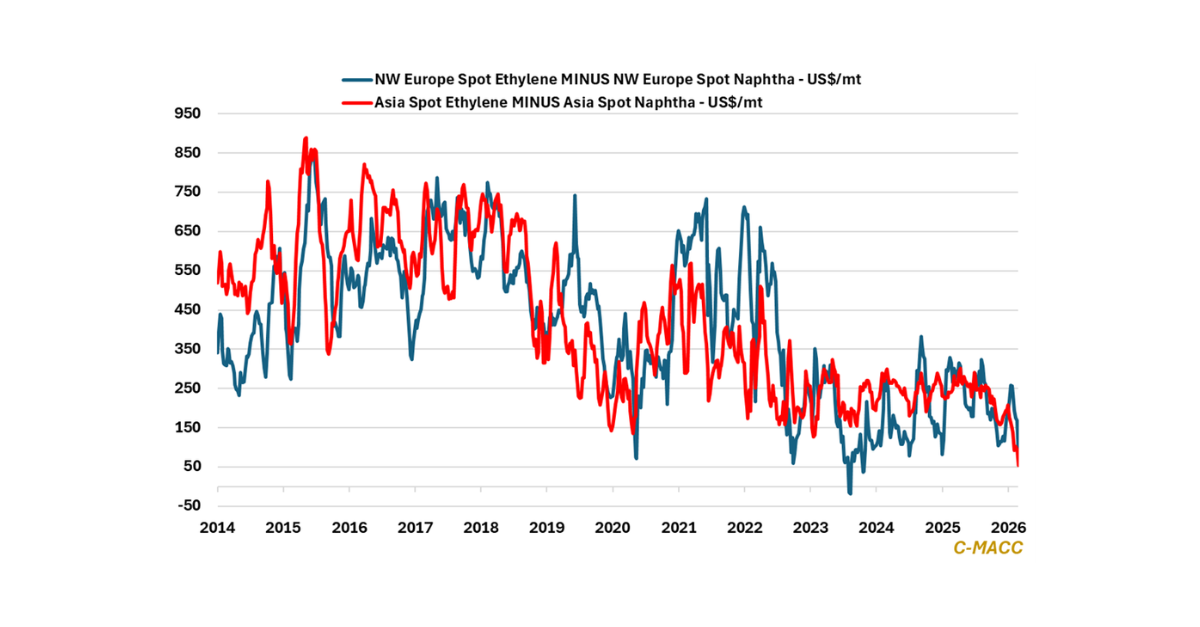

General Thoughts: Global energy shocks, narrowing sanctioned crude oil discounts, and persistent olefin oversupply converge to lift marginal costs, accelerate restructuring, and benefit gas-advantaged producers.