Sunday Executive Summary

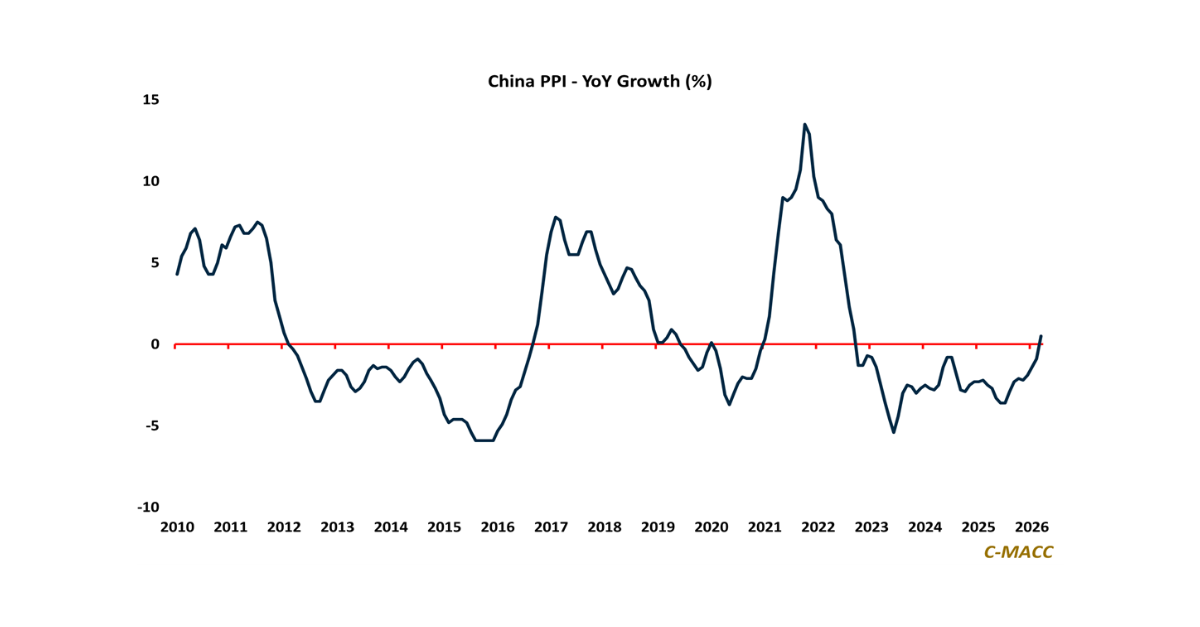

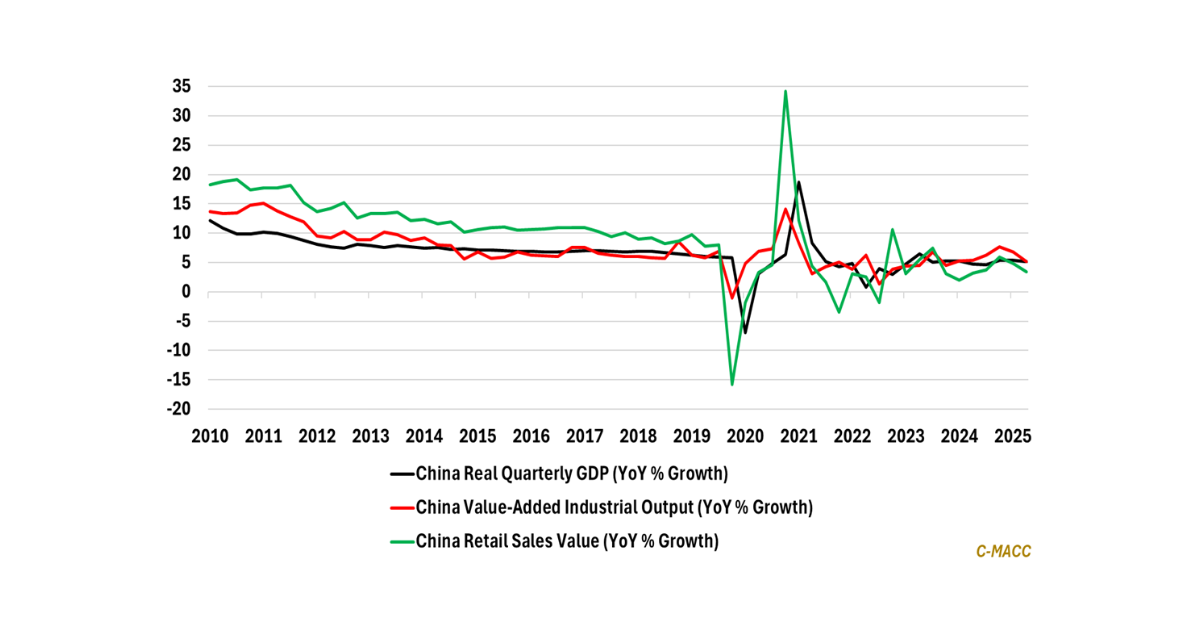

China’s 0.5% YoY factory-gate inflation in March removed a trusted global relief valve, forcing markets to underwrite firmer resin and intermediate floors, slower cost deflation,

China’s 0.5% YoY factory-gate inflation in March removed a trusted global relief valve, forcing markets to underwrite firmer resin and intermediate floors, slower cost deflation,

Dependable operations now define competitive advantage, with non-integrated assets losing ground as fragility disrupts throughput, raises risk, and weakens returns under stress.

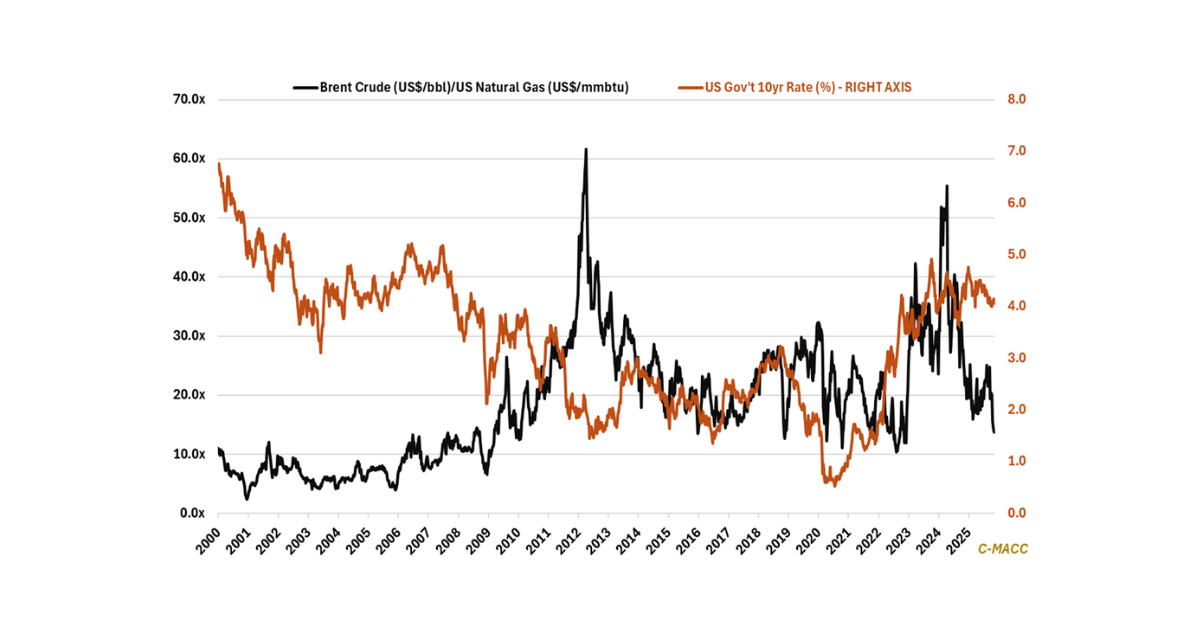

Oil-linked feedstock systems

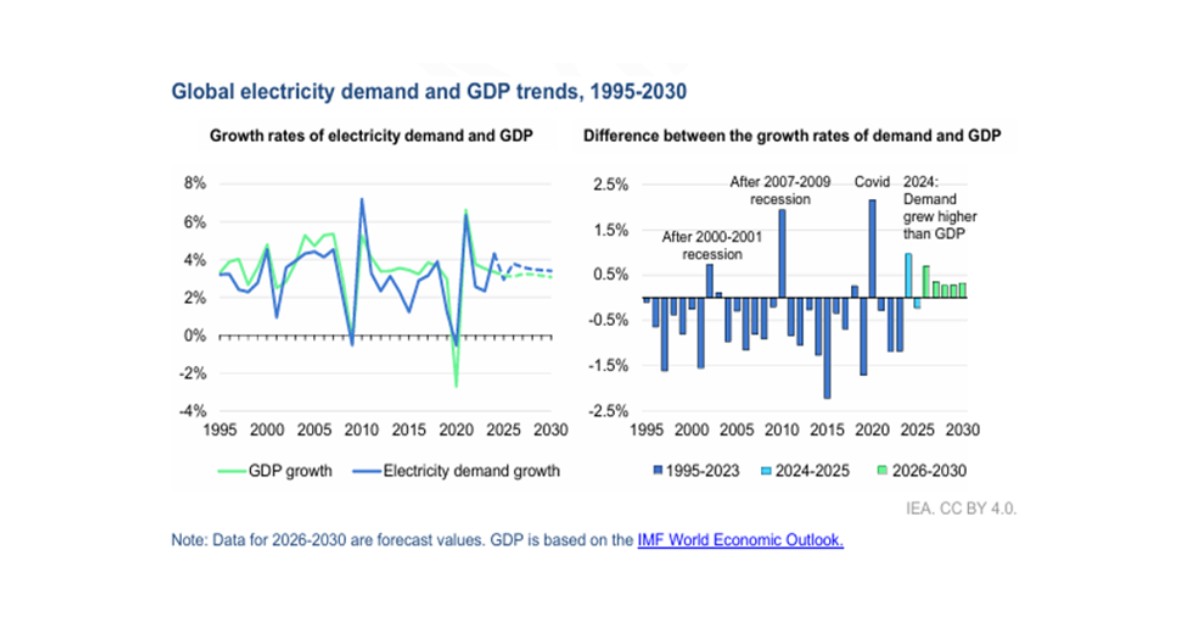

1st Topic of the Week: Electricity demand is positioned to outpace economic growth, shifting competitive advantage toward regions with secure, scalable power access, reliable infrastructure,

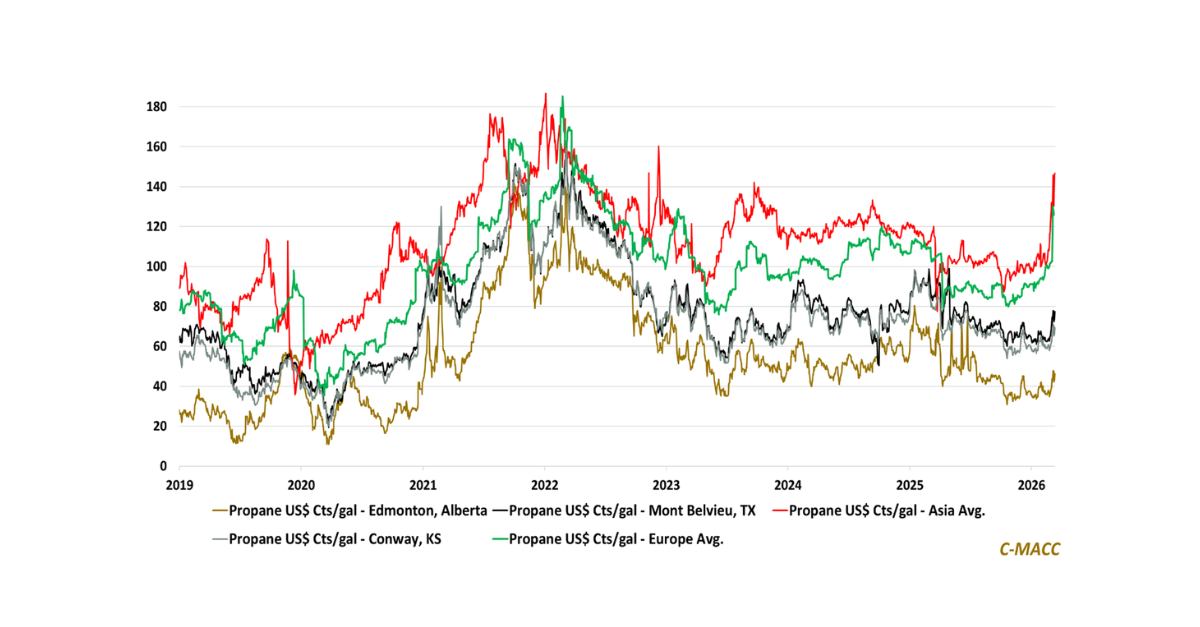

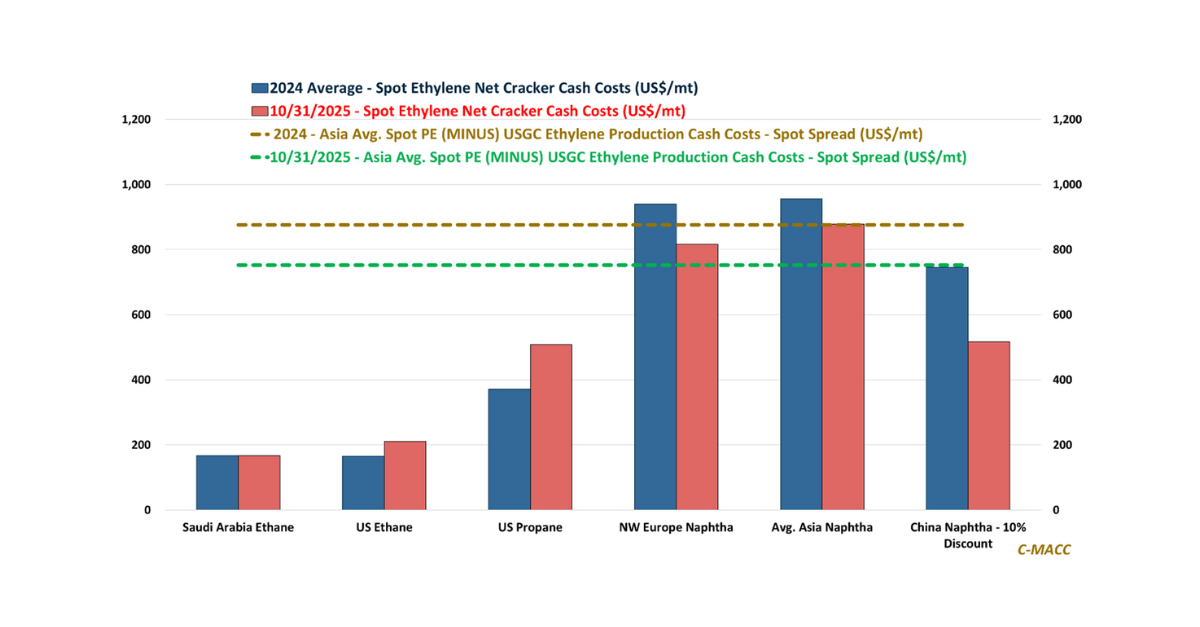

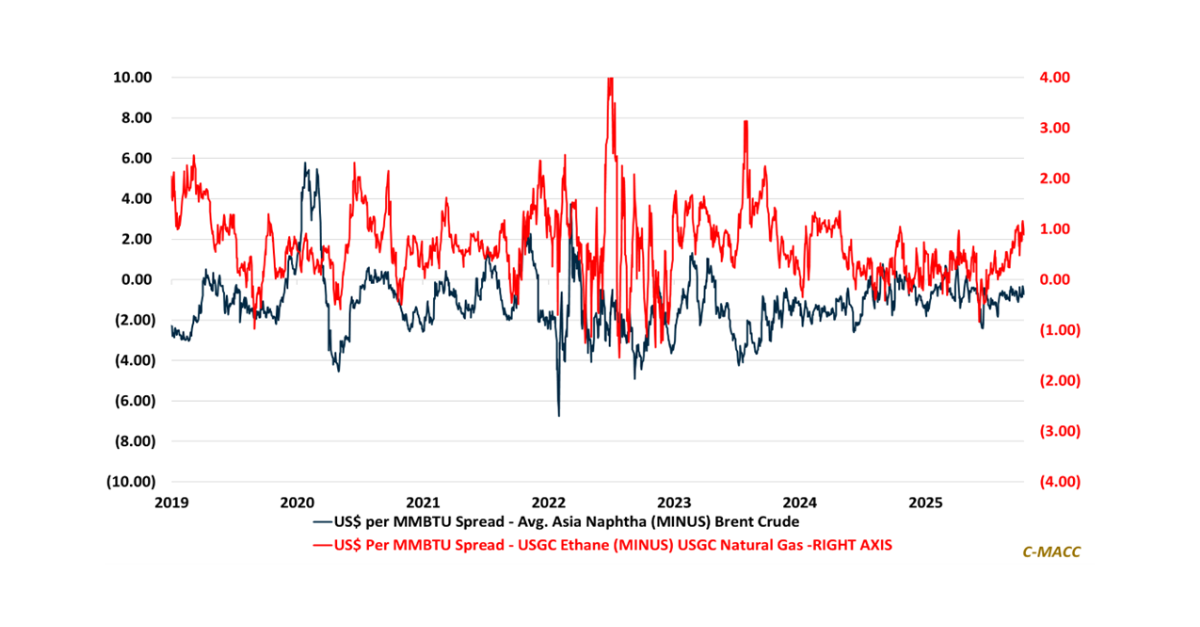

Asia and Europe now pay a structural propane premium as Middle East disruption risk lifts import costs, compressing PDH production margins abroad and reinforcing North

Procurement-led synergy engines, not scale alone, are increasingly becoming the primary determinant of industrial competitiveness in a high-cost-capital, low-growth world increasingly defined by structural volatility.

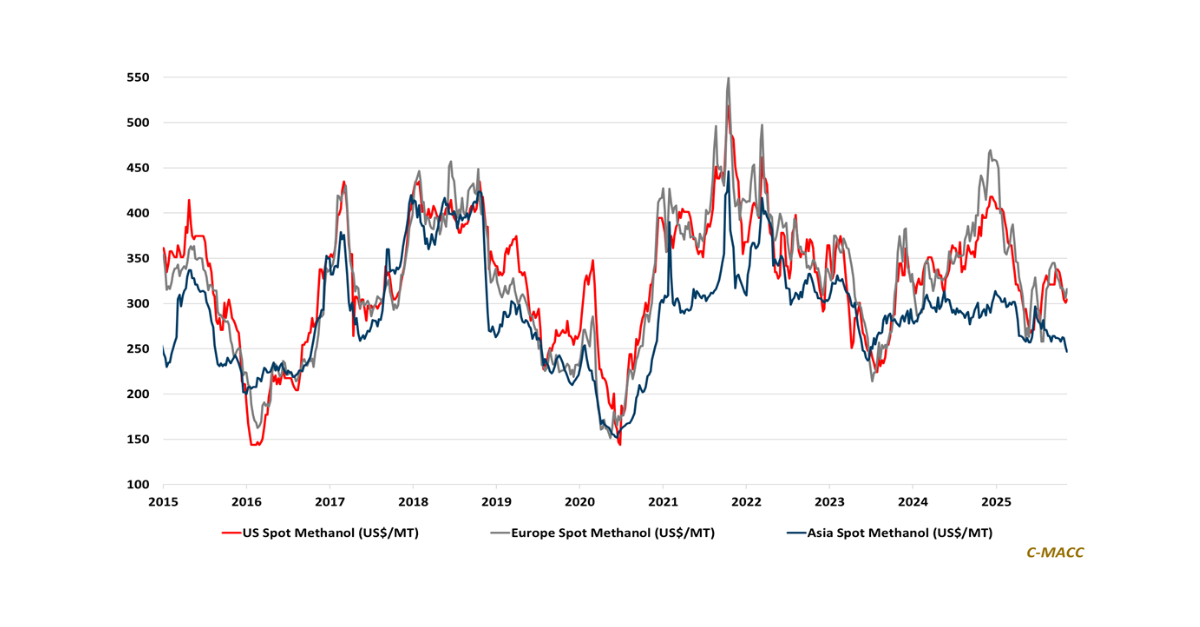

General Thoughts: Red Sea freight normalization could compress Western chemical market premiums, including for methanol, exposing cost curves, trade defenses, and discipline as differentiators in

Liquidity precision replaces scale as the ultimate competitive edge in commodity chemicals, transforming balance sheets from static safeguards into dynamic, return-focused engines of enduring strategic

General Thoughts: Global chemical sector margin compression is reprogramming markets as returns migrate from volume to precision, with integration, agility, and cost discipline eclipsing geographic

Volatility has transcended cycle theory to become global industrial gravity, where policy cadence, not demand elasticity, dictates profitability, capital sequencing, and the new tempo of

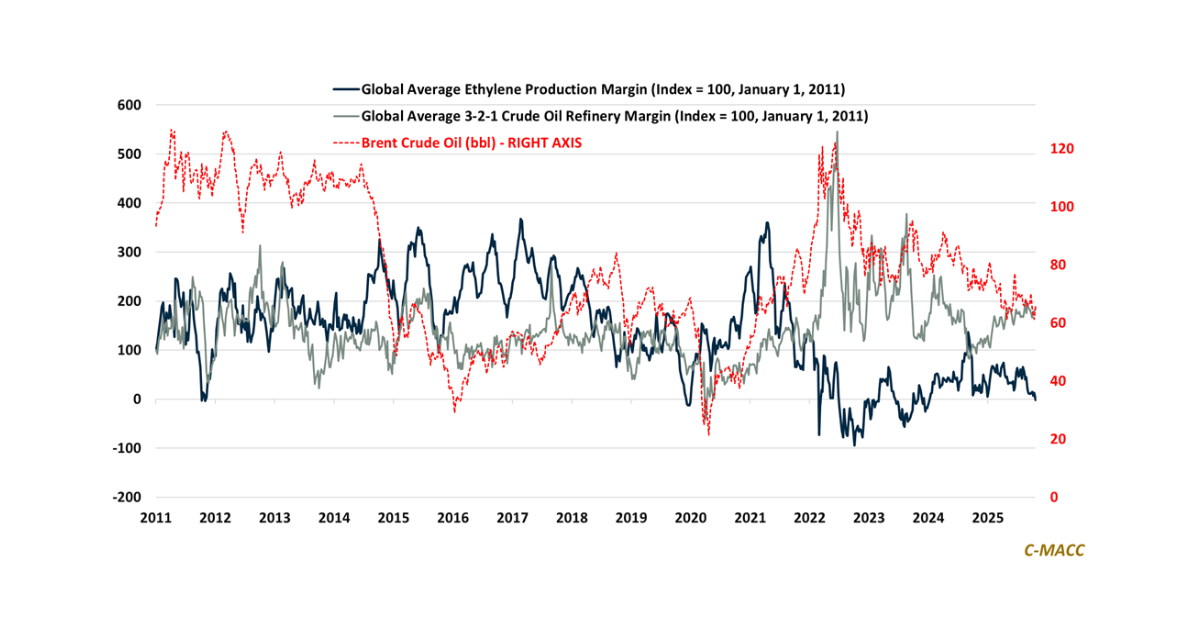

General Thoughts: Chemical feedstock dynamics increasingly signal a global inflection; margin compression forcing strategic resets, capital discipline, and system-wide realignment across industrial value chains.

Supply