Sunday Executive Summary

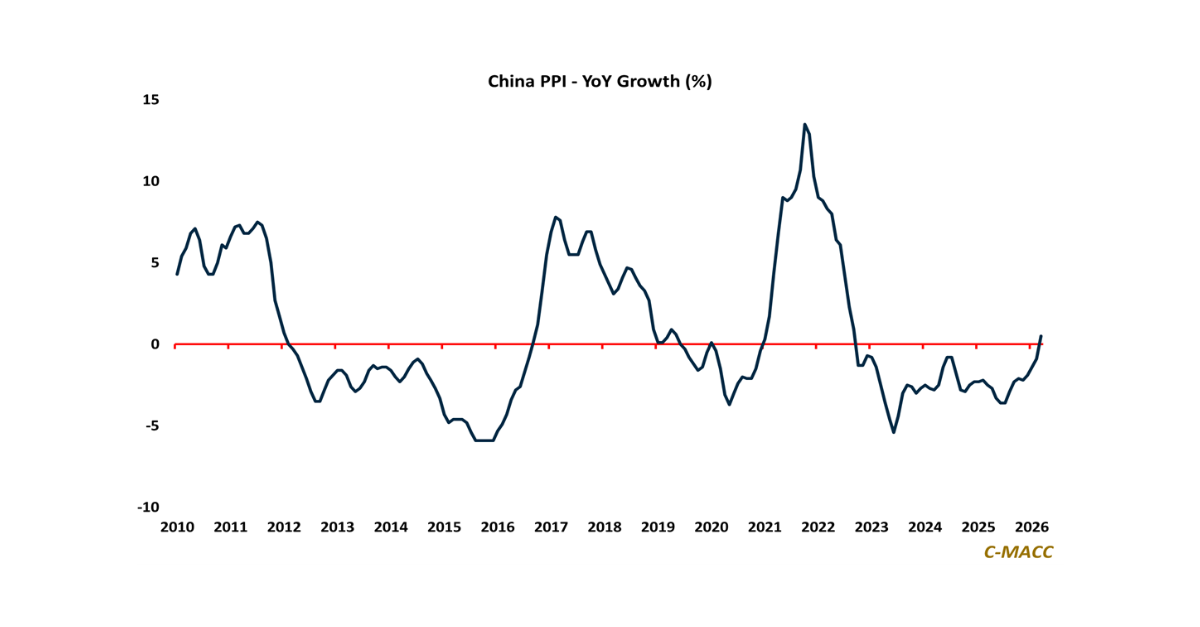

China’s 0.5% YoY factory-gate inflation in March removed a trusted global relief valve, forcing markets to underwrite firmer resin and intermediate floors, slower cost deflation,

China’s 0.5% YoY factory-gate inflation in March removed a trusted global relief valve, forcing markets to underwrite firmer resin and intermediate floors, slower cost deflation,

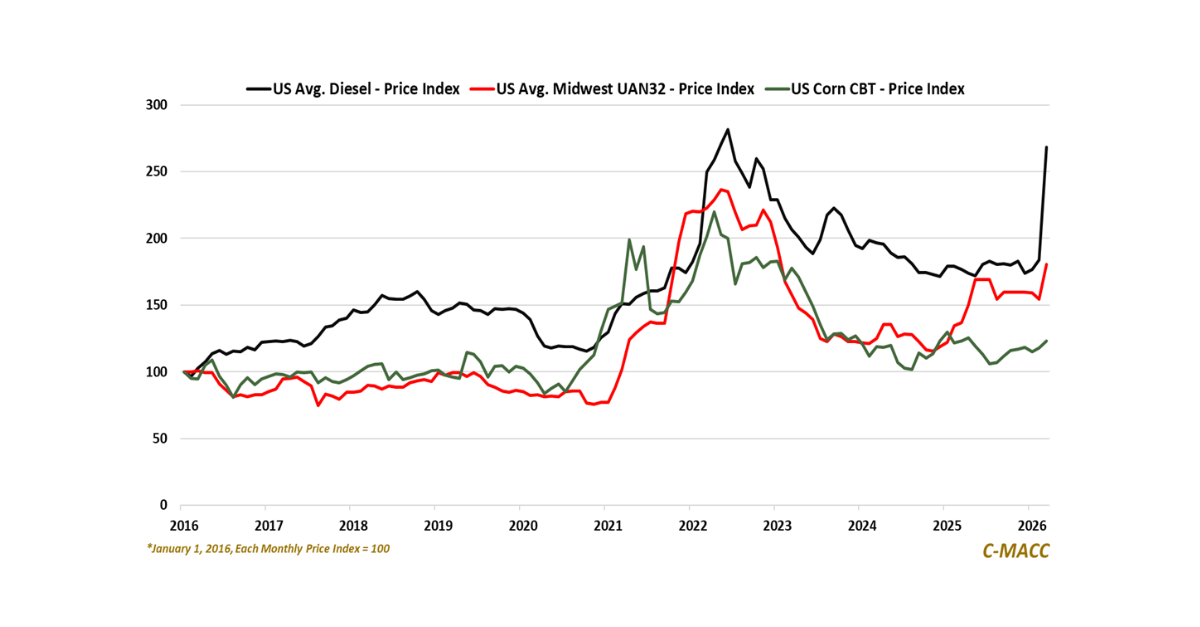

General Thoughts: Rising input costs are exposing margin fragility across industries, shifting advantage to pricing power, as policy-driven demand hopes build to offset war-driven inflation

1st Topic of the Week: Capital is consolidating decisively around systems that either monetize energy scarcity or eliminate exposure to it, directing deployment decisions and

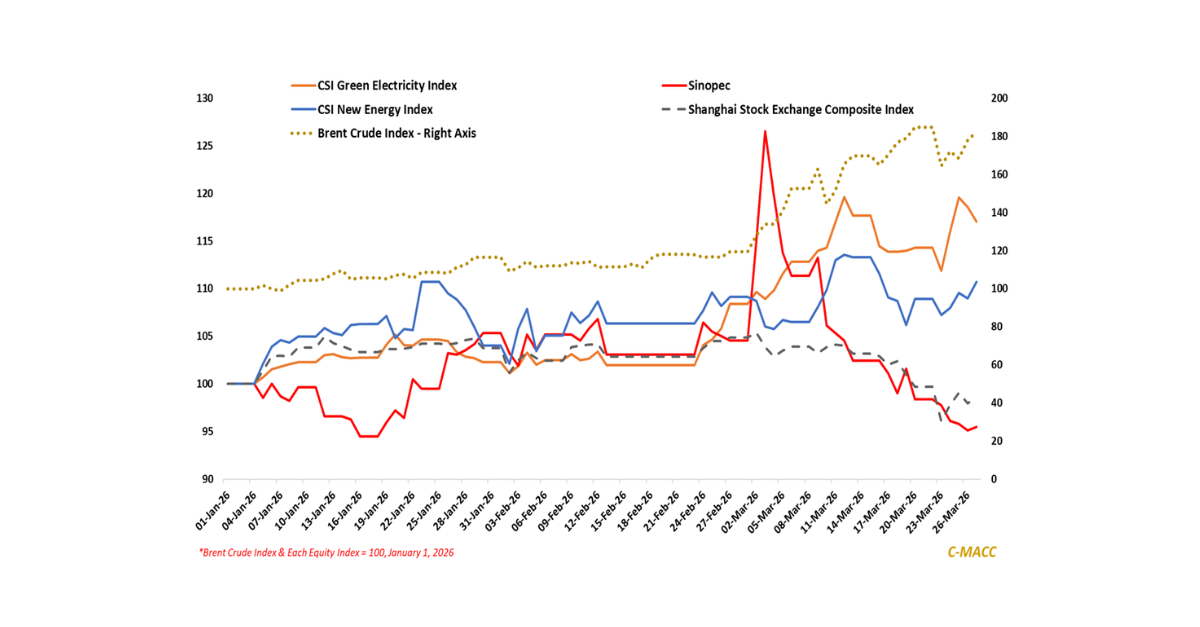

General Thoughts: Supply shocks are shifting power from cost to control, concentrating value in integrated systems as export-driven convergence reshapes demand, margins, and capital allocation

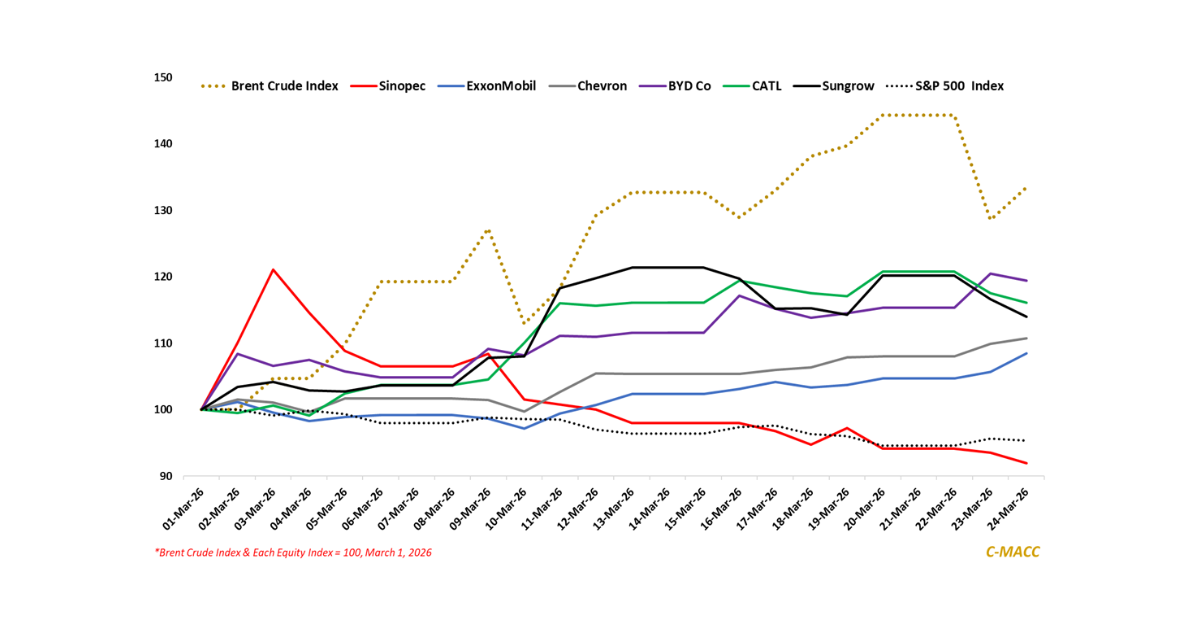

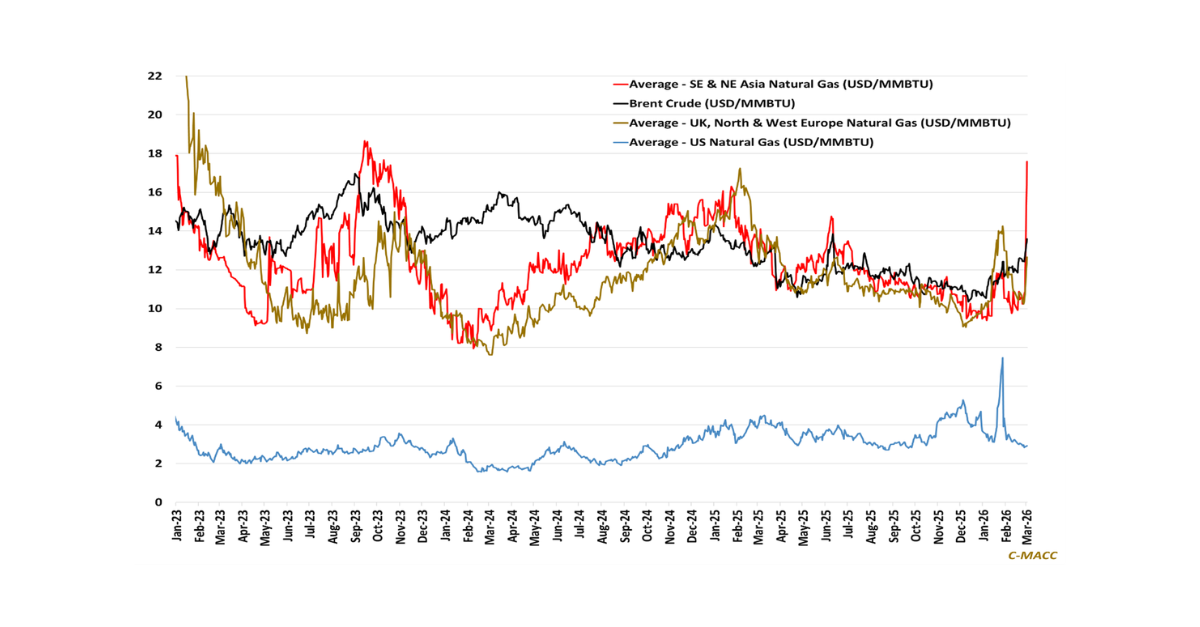

General Thoughts: Energy security is reshaping value chains, driving a bifurcation in which capital concentrates in low-cost hydrocarbons and in electrification, compressing high-cost industrial systems.

General Thoughts: Integration, logistics flexibility, and feedstock advantage are increasingly replacing scale as the chemical sector’s defining competitive edge, steering capital toward integrated production platforms.

General Thoughts: Energy shocks are redistributing profitability across industrial value chains as surging ex-US energy costs compress petrochemical margins, tighten fertilizer markets, and strengthen North

General Thoughts: Feedstock volatility, still weak demand, and supply chain stress accelerate global chemical restructuring as companies actively reshape portfolios to improve long-term risk-adjusted returns.

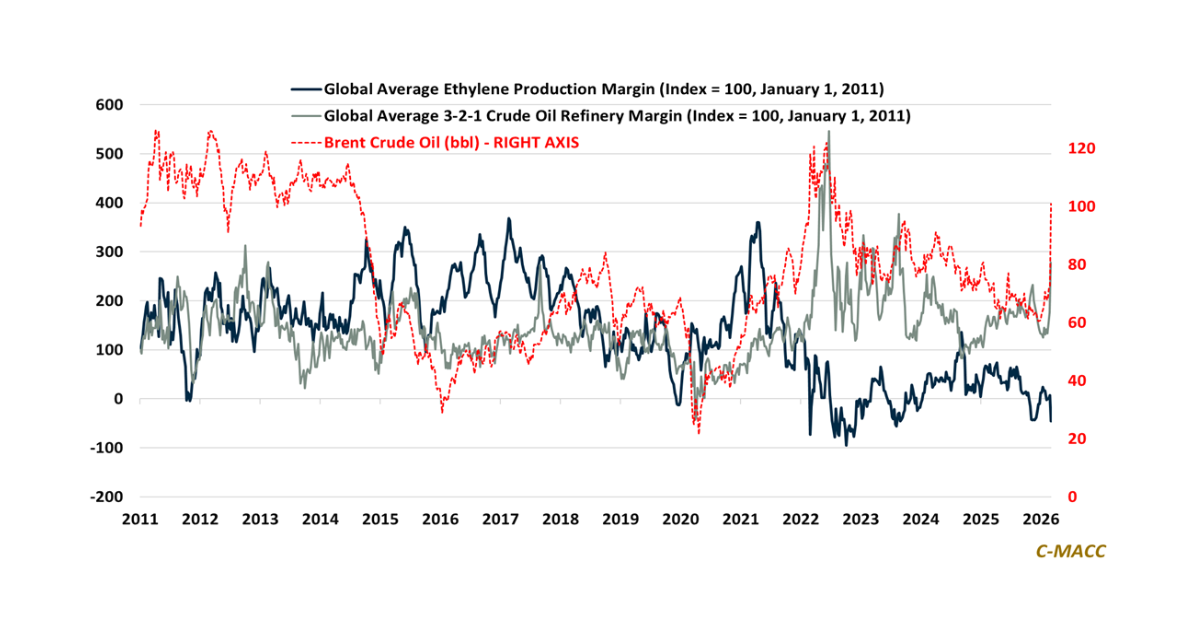

General Thoughts: Global energy shocks, narrowing sanctioned crude oil discounts, and persistent olefin oversupply converge to lift marginal costs, accelerate restructuring, and benefit gas-advantaged producers.

General Thoughts: Crude oil and Ex-US natural gas price strength relative to US levels has steepened the global cost curve for most chemicals, accelerating rationalization