Sunday Executive Summary

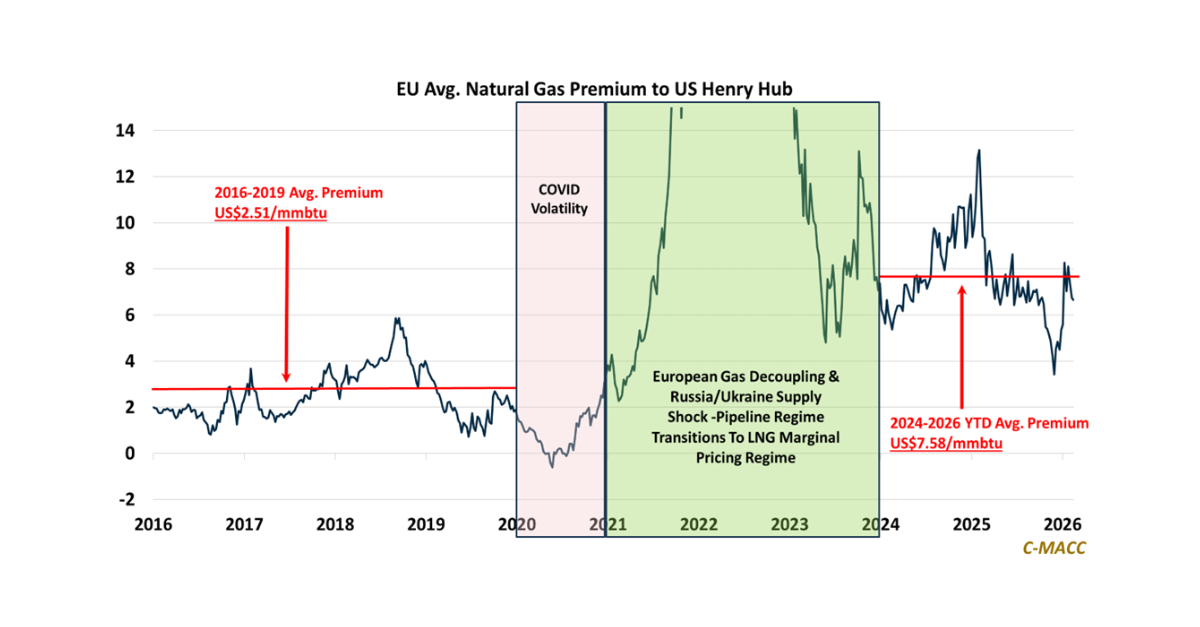

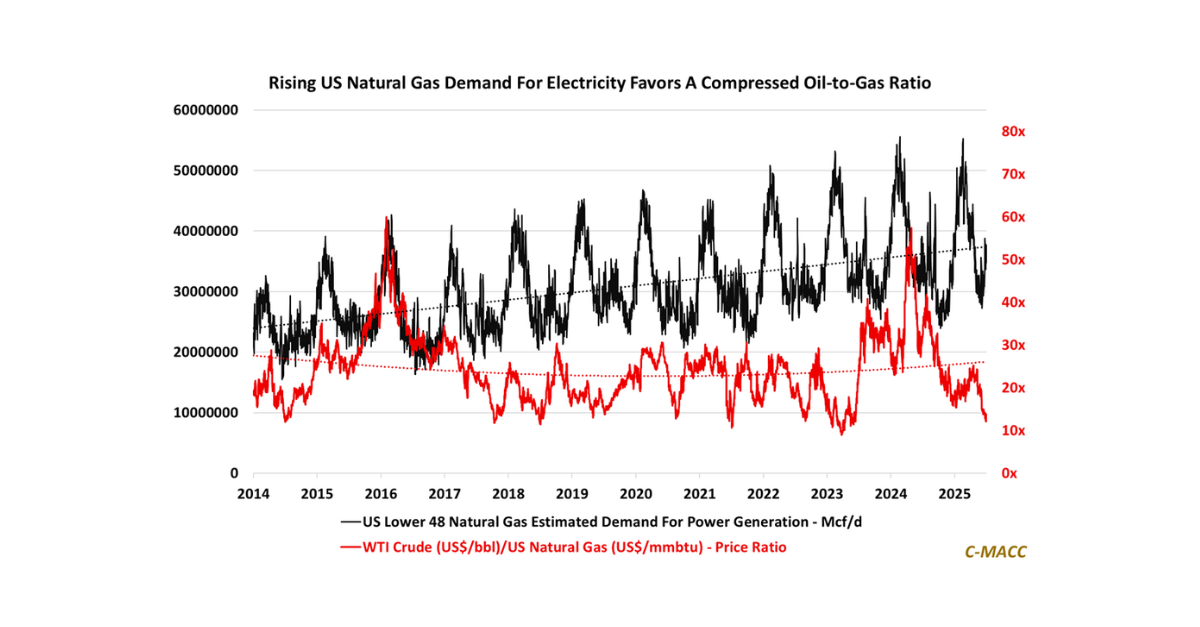

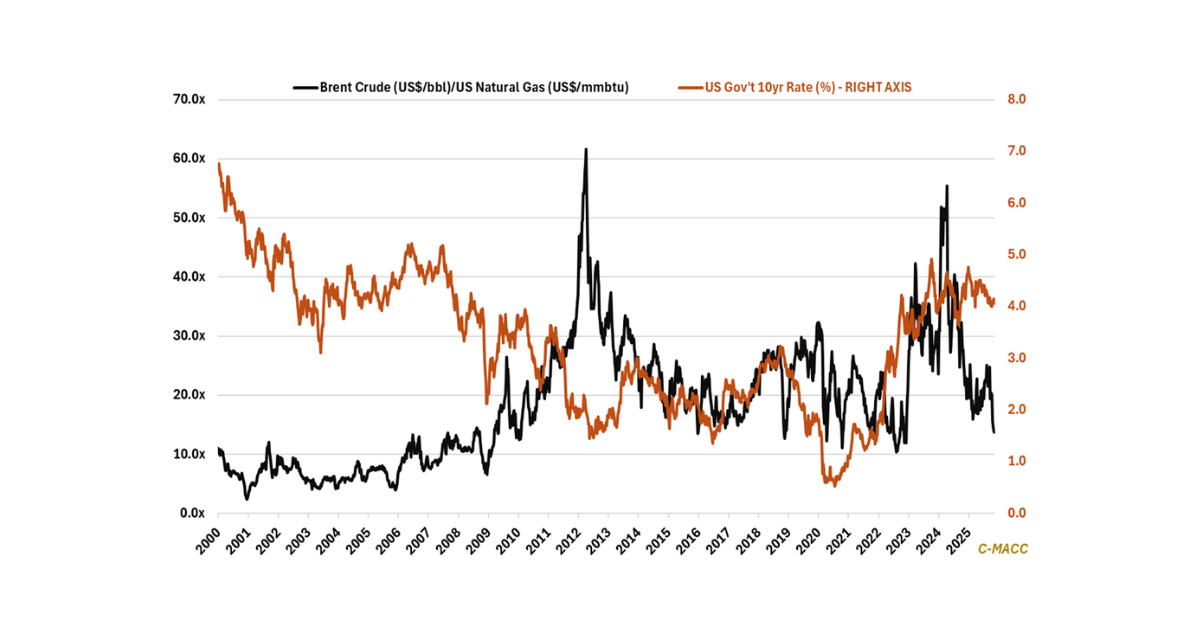

Persistent European premiums over Henry Hub confirm LNG marginal clearing as the dominant marginal price-setting mechanism, anchoring US export-linked gas economics and long-cycle infrastructure returns.

Persistent European premiums over Henry Hub confirm LNG marginal clearing as the dominant marginal price-setting mechanism, anchoring US export-linked gas economics and long-cycle infrastructure returns.

General Thoughts: Energy-linked corn economics and widening oil–gas dispersion are shifting global marginal cost leadership toward natural gas advantaged, capital-disciplined integrated production platforms globally.

Supply

China’s slowing consumption and persistently low relative price inflation push excess supply outward, reviving export-led clearing and intensifying global price competition as logistics increasingly normalize

General Thoughts: Early-2026 cost-curve shifts amid persistent chemical market oversupply are forcing restructuring, with clear evidence likely emerging in 4Q25 results and more decisive 2026

Chemical sector outcomes in 2026 will hinge more on managing volatility across power, gas, and policy, not on forecasting averages, as infrastructure constraints and capital

Global Market Analysis There Will Be Blood, Closures: Global Return Hurdles Further Harden Into 2026 Key Findings Exhibit 1: Real rates strengthen globally in late

Capital allocation is increasingly shifting from speculative growth and volume chasing toward return gating, as firms demand contracted cash flows, controllable execution risk, and downside

1st Topic of the Week: Wind input demand is shrinking as power dollars pivot to other generation sources and grid equipment; will policy ultimately redirect

General Thoughts: Growing structural natural gas demand, persistent global chemical overcapacity, and tighter grid constraints will jointly determine competitiveness and boost cross-sector consolidation well into

Procurement-led synergy engines, not scale alone, are increasingly becoming the primary determinant of industrial competitiveness in a high-cost-capital, low-growth world increasingly defined by structural volatility.