Sunday Executive Summary

Procurement-led synergy engines, not scale alone, are increasingly becoming the primary determinant of industrial competitiveness in a high-cost-capital, low-growth world increasingly defined by structural volatility.

Procurement-led synergy engines, not scale alone, are increasingly becoming the primary determinant of industrial competitiveness in a high-cost-capital, low-growth world increasingly defined by structural volatility.

General Thoughts: Critical minerals pivot from simple price-recovery bets to resilience math, where capital discipline, restructuring, community license, and carbon intensity increasingly shape competitiveness and

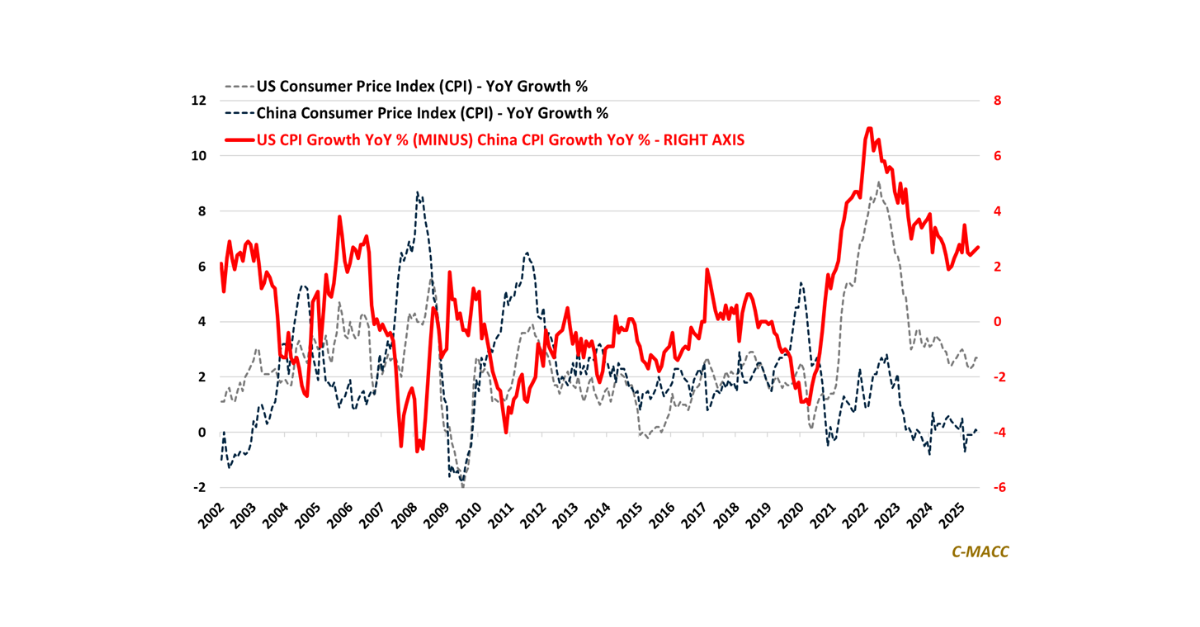

US-China inflation divergence realigns capital flows, currency dynamics, and trade competitiveness across services, manufacturing, and energy-linked exports spanning petrochemicals, agriculture, and industrial inputs.

US chemical

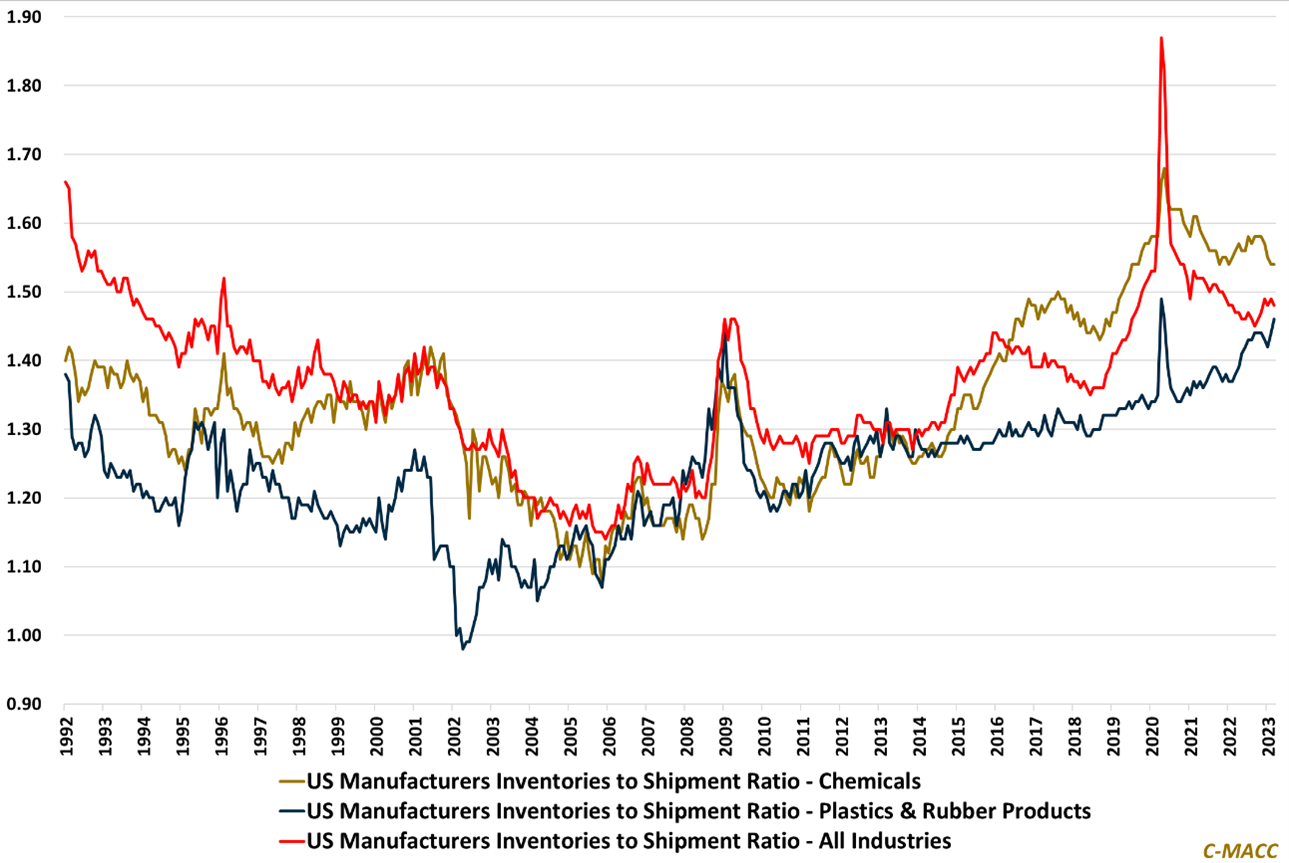

General Thoughts: Relative cost position has become a major discussion topic in terms of YTD margin support and profit outlooks for 2024, as many global

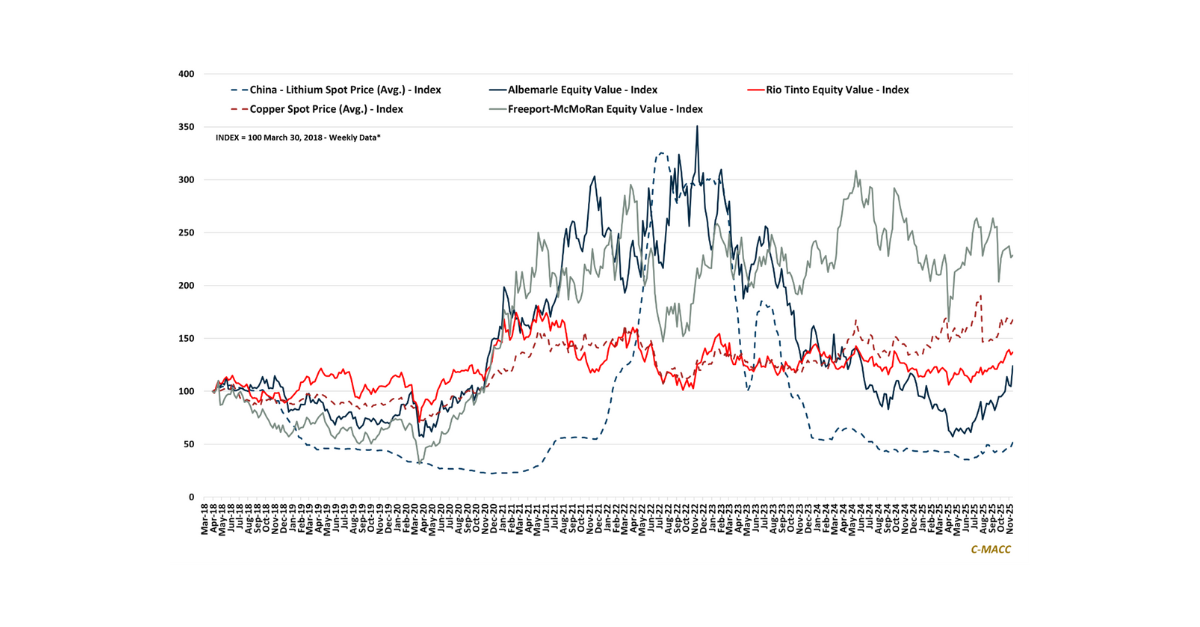

The lithium spot price collapse relative to early 2023 estimates has caused producer Albemarle to cut its full-year profit outlook – an example of a

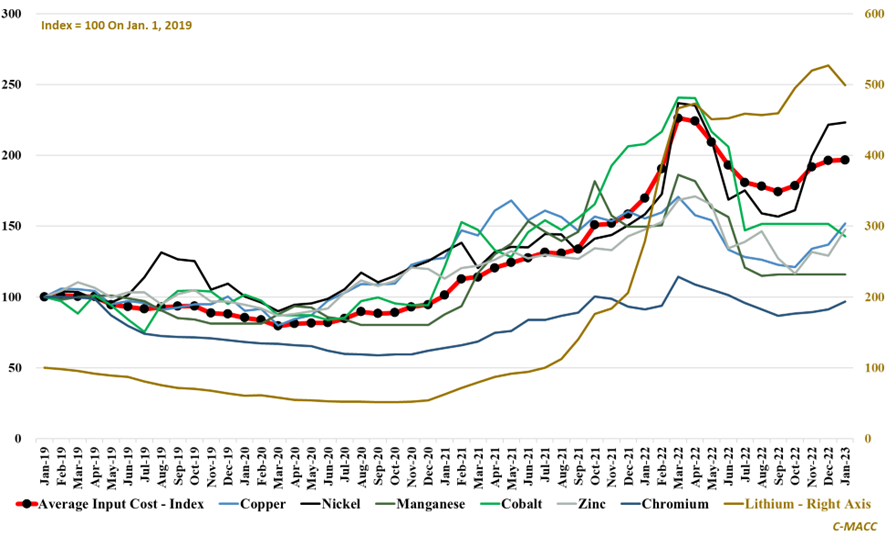

The C-MACC Clean Energy Minerals Monthly Price Index was unchanged MoM in January, and we anticipate continued support in 1H23, though some materials will stay

As worsening business conditions into yearend lower 2023 outlooks, we think money will be made by those making consolidation moves versus those who hide.

Almost

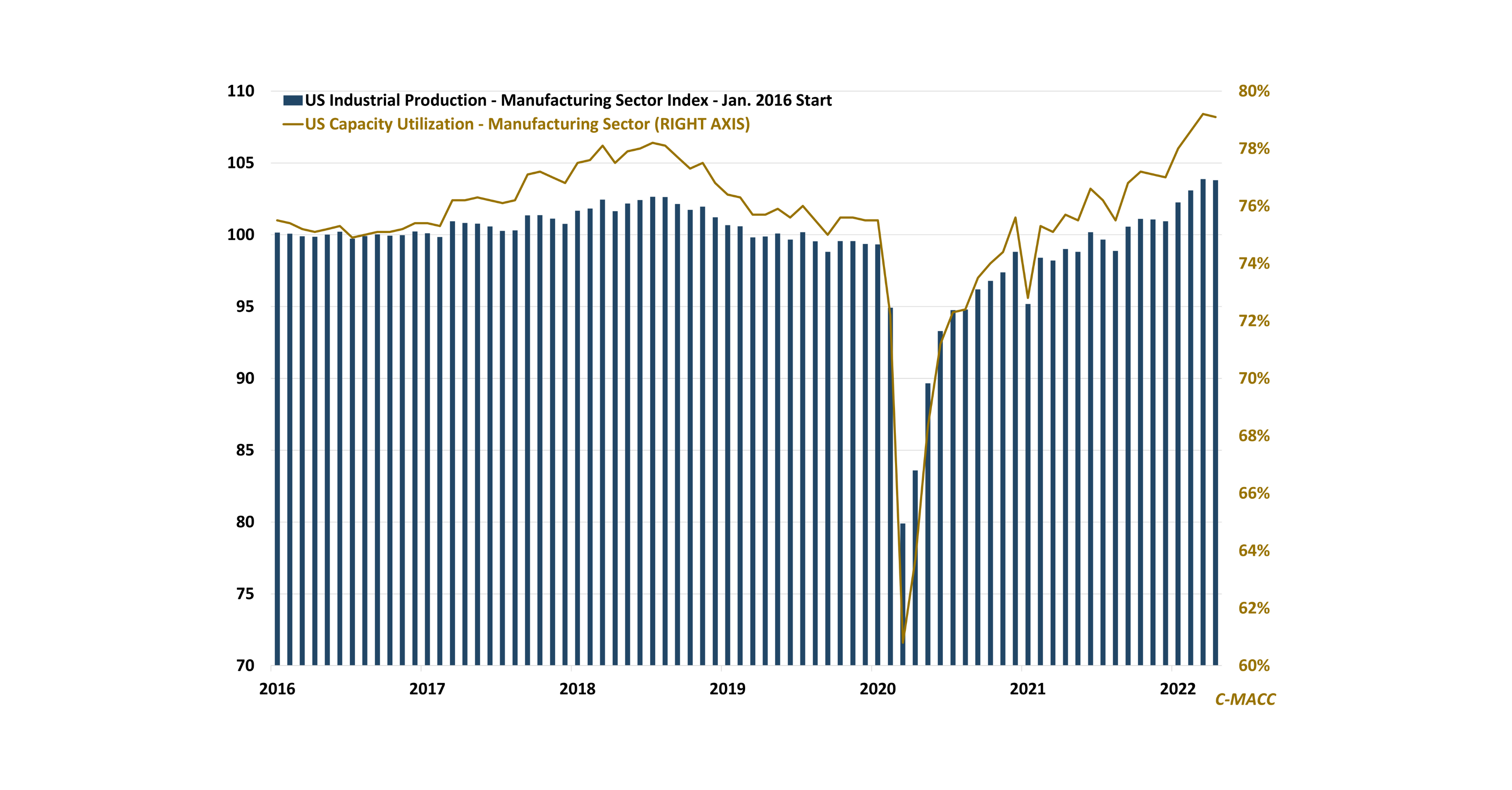

U.S. industrial production growth slowed in May due to a decline in manufacturer output, supporting our near-term chemical sector concerns amid mounting evidence that domestic

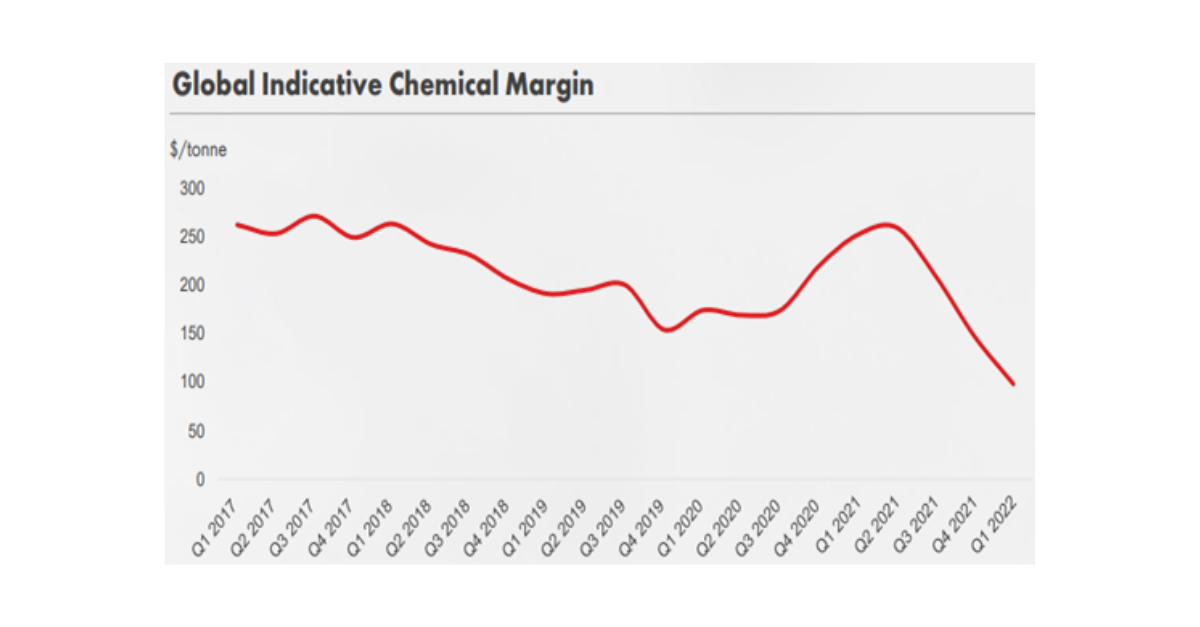

Global chemical sector margins take a hit from higher energy costs YTD. We foresee mounting product price headwinds in 2H22 as supply availability improves, consumer

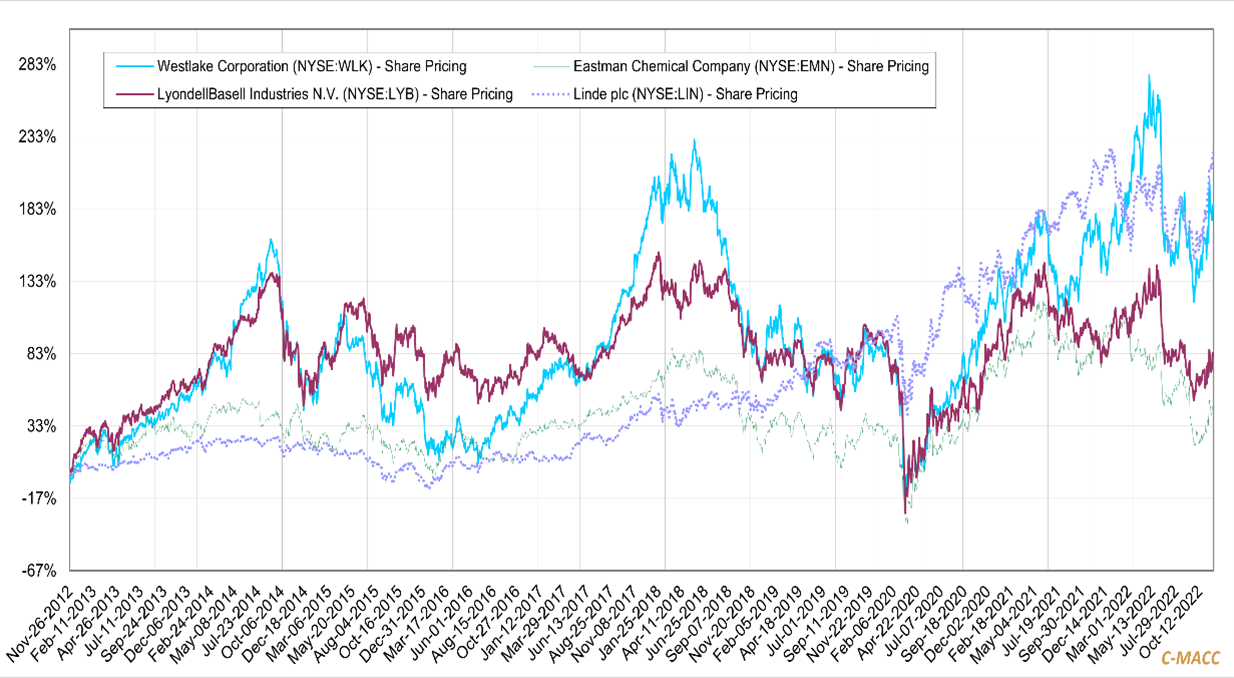

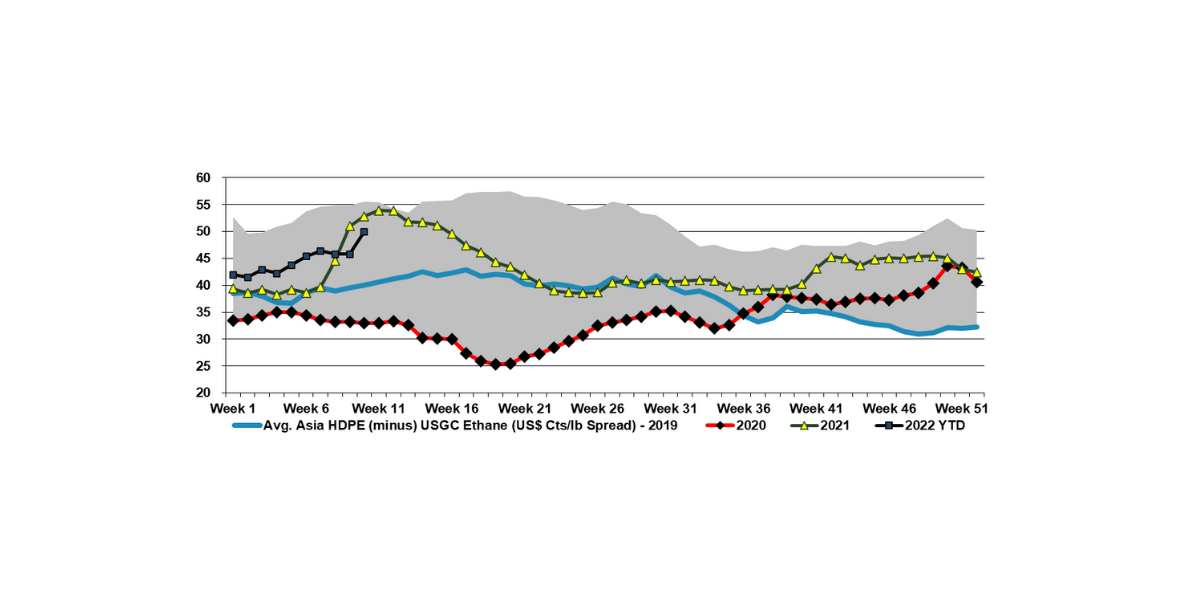

Global market indicators favor North American chemical producers relative to overseas peers. Our research flags US retail sales trends, European naphtha premiums, and US commodity