Sunday Executive Summary

System constraints are compressing global corporate decision cycles, forcing capital into platforms that secure inputs, logistics, and execution simultaneously rather than optimizing sequentially across markets.

System constraints are compressing global corporate decision cycles, forcing capital into platforms that secure inputs, logistics, and execution simultaneously rather than optimizing sequentially across markets.

General Thoughts: Supply shocks are shifting power from cost to control, concentrating value in integrated systems as export-driven convergence reshapes demand, margins, and capital allocation

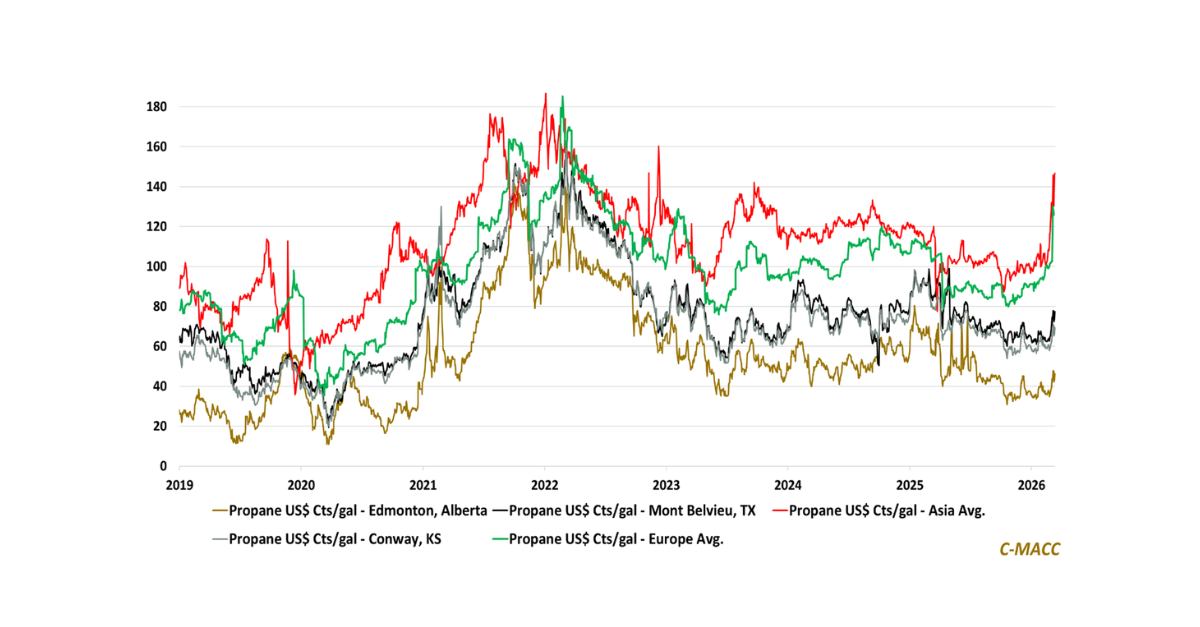

Asia and Europe now pay a structural propane premium as Middle East disruption risk lifts import costs, compressing PDH production margins abroad and reinforcing North

General Thoughts: Supply disruptions expose structural weaknesses in global petrochemical trade, favoring logistics flexibility and advantaged feedstocks while limiting new investment responses.

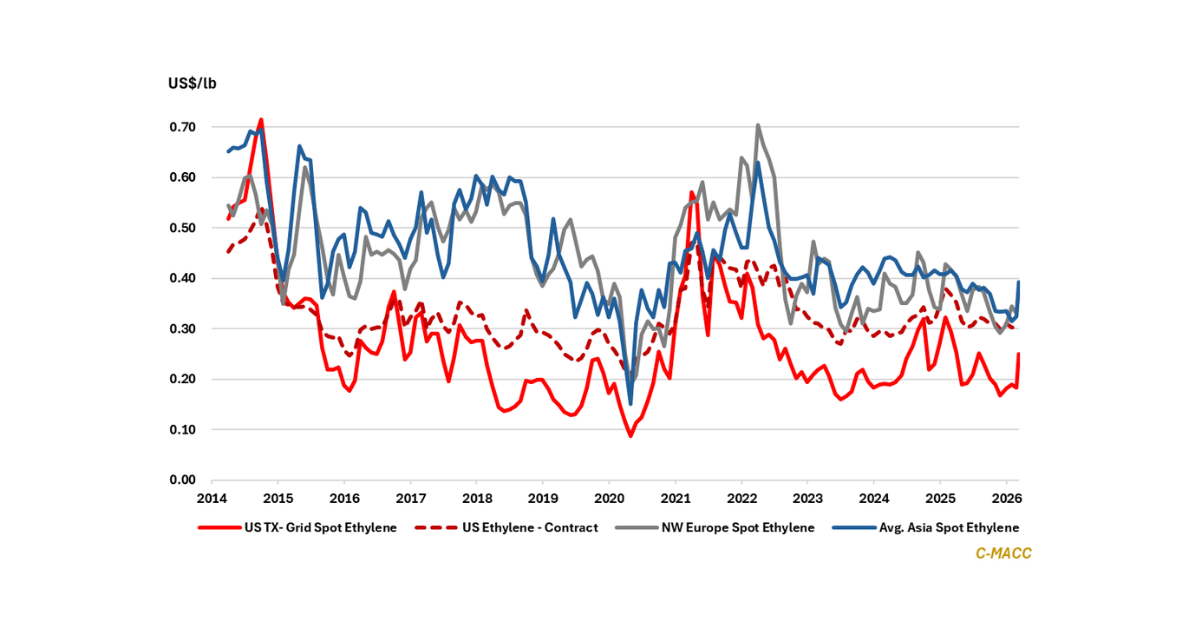

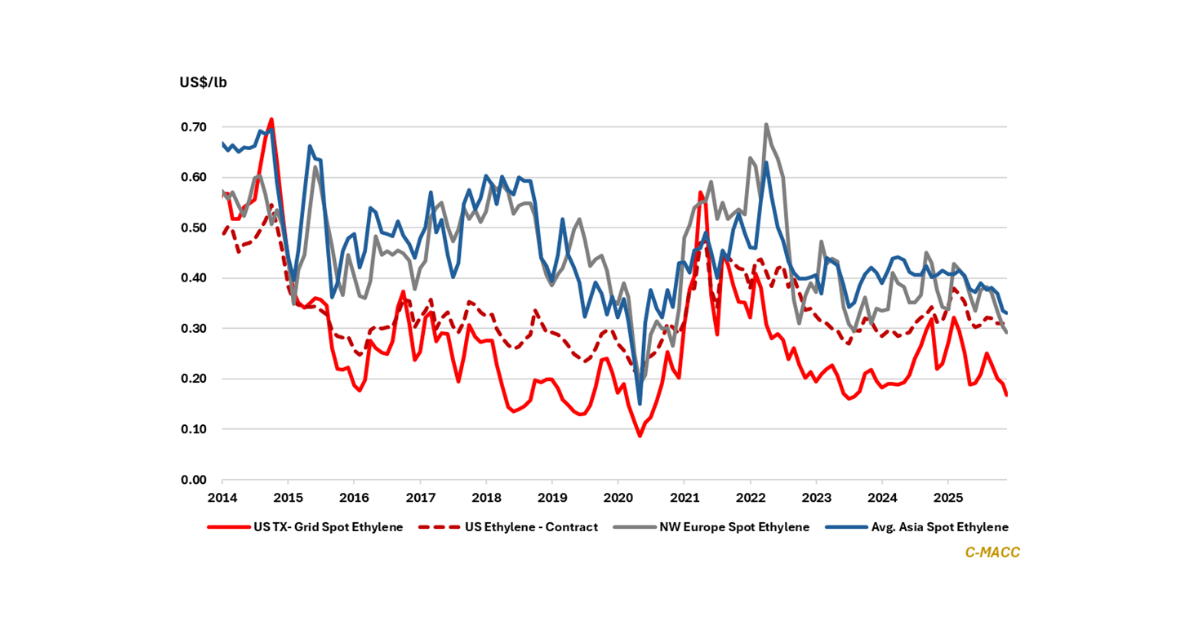

Supply Chain/Commodities: Ethylene

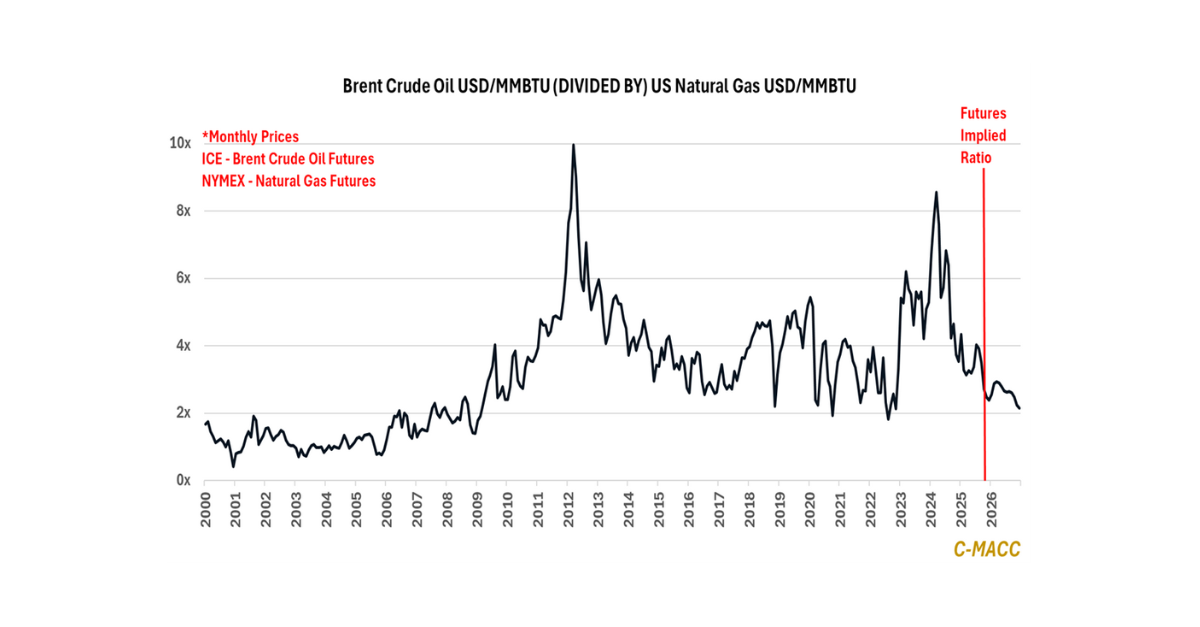

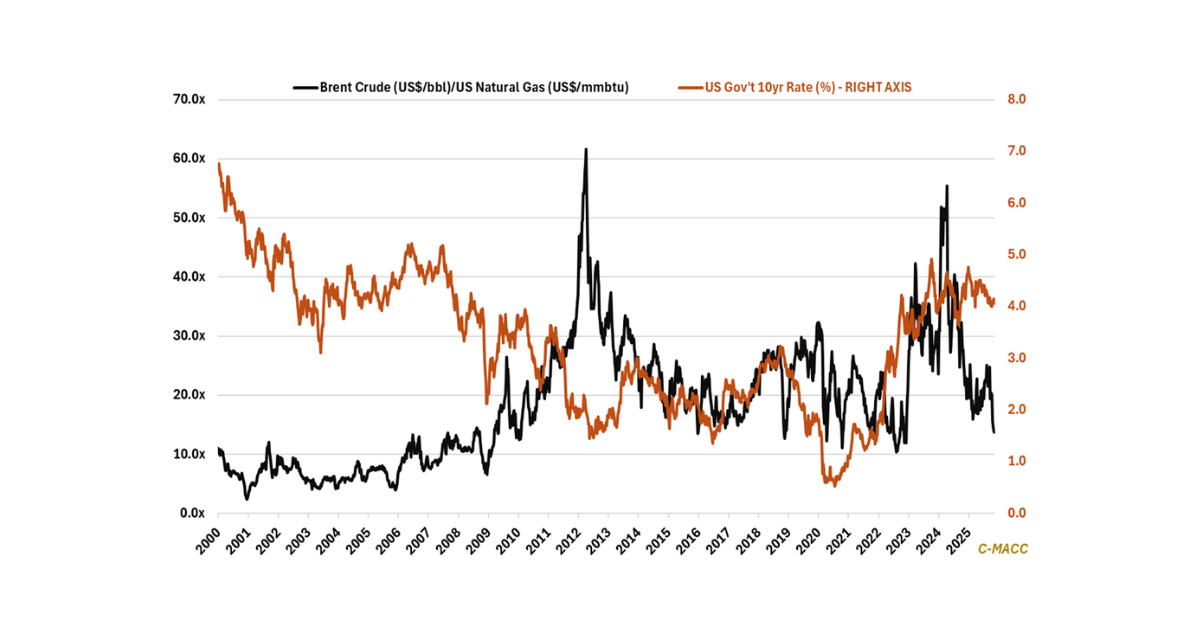

Depressed oil-to-gas ratios and elevated soy-to-corn prices shift chemical-sector risk profiles: commodity chemical underperformers in 2025 face low expectations in 2026, whereas agriculture faces the

General Thoughts: Exporting the advantaged US ethane cost position and surplus ethylene amid low oil prices and downstream market oversupply will likely be a bumpy

Procurement-led synergy engines, not scale alone, are increasingly becoming the primary determinant of industrial competitiveness in a high-cost-capital, low-growth world increasingly defined by structural volatility.

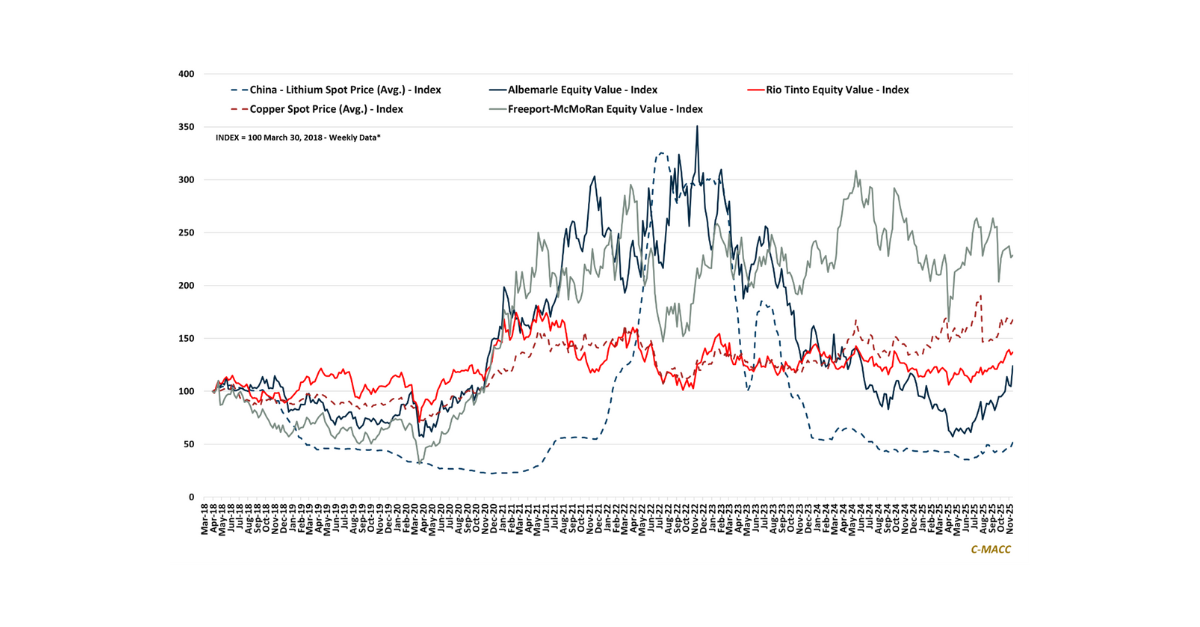

General Thoughts: Critical minerals pivot from simple price-recovery bets to resilience math, where capital discipline, restructuring, community license, and carbon intensity increasingly shape competitiveness and

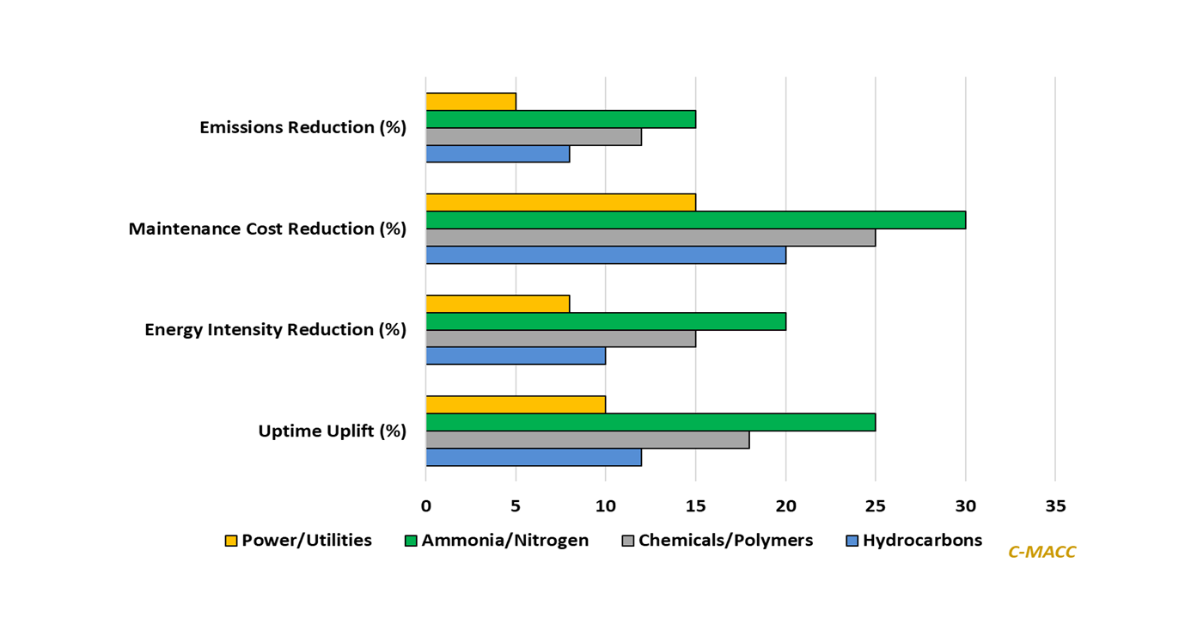

AI-driven stability converts volatile energy and chemical systems into more predictable cash engines, revealing structural advantage patterns that most operators still underestimate in a rapidly

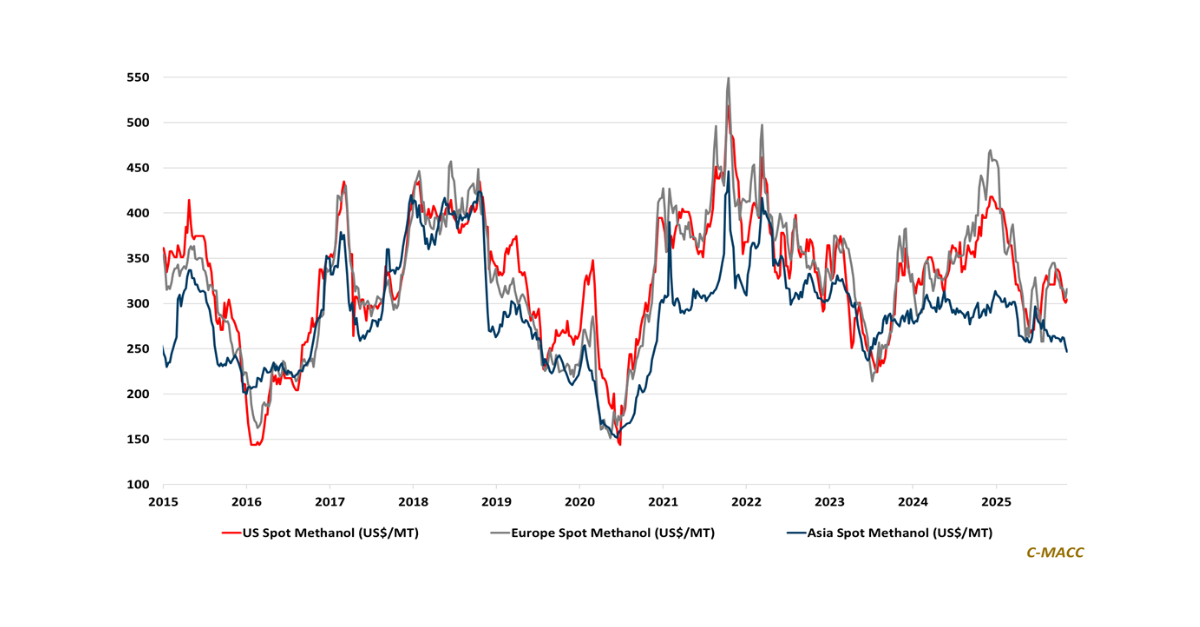

General Thoughts: Red Sea freight normalization could compress Western chemical market premiums, including for methanol, exposing cost curves, trade defenses, and discipline as differentiators in