Global Market Analysis

We are more concerned about chemical demand than supply in 2023. A steepening of global production cost curves may help offset tepid demand in support

We are more concerned about chemical demand than supply in 2023. A steepening of global production cost curves may help offset tepid demand in support

Commodity chemical producers lacking feedstock integration face difficult choices as the energy sector expands downstream, pressuring non-integrated chemical returns.

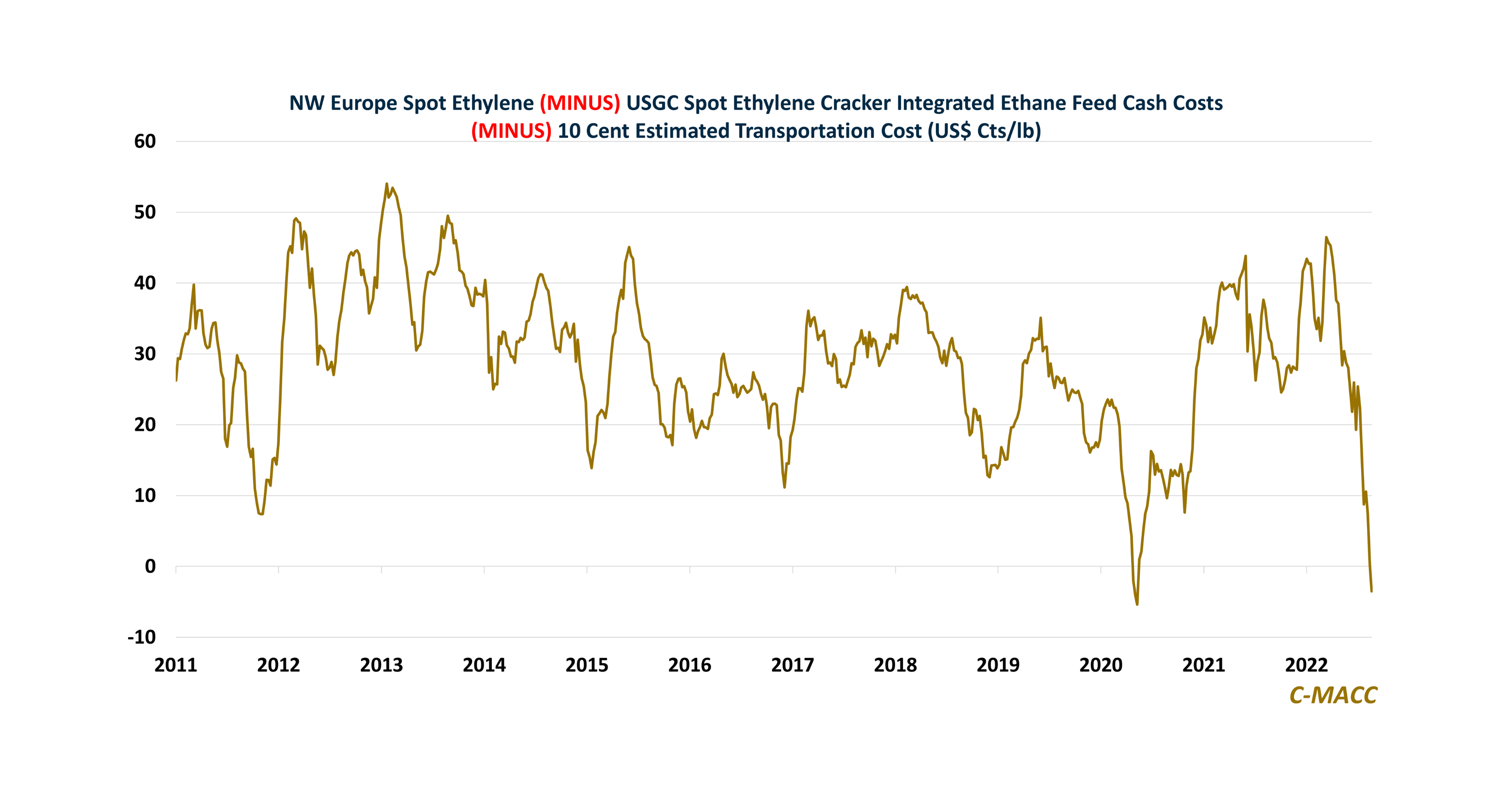

The North American petrochemical producer cost

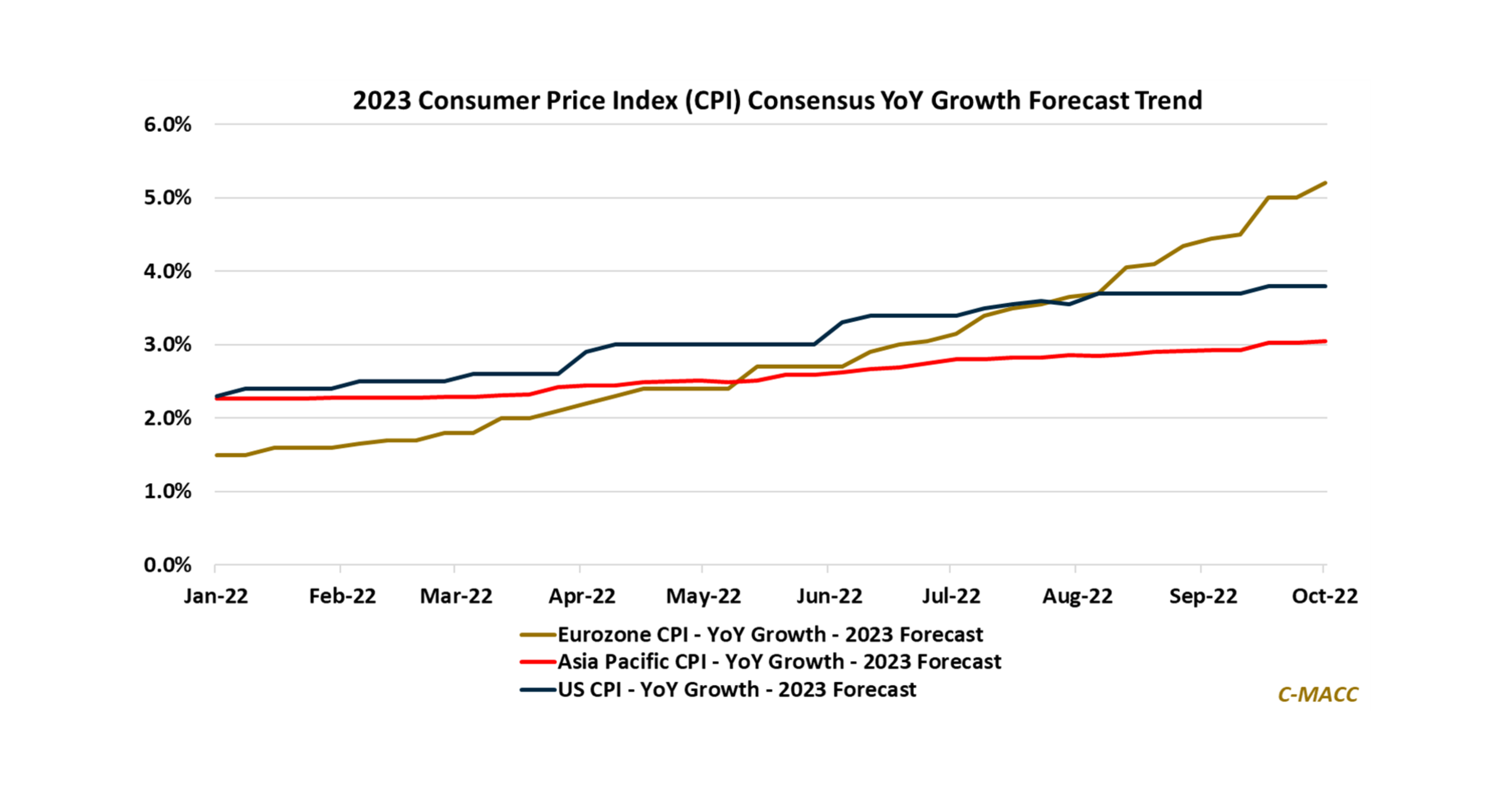

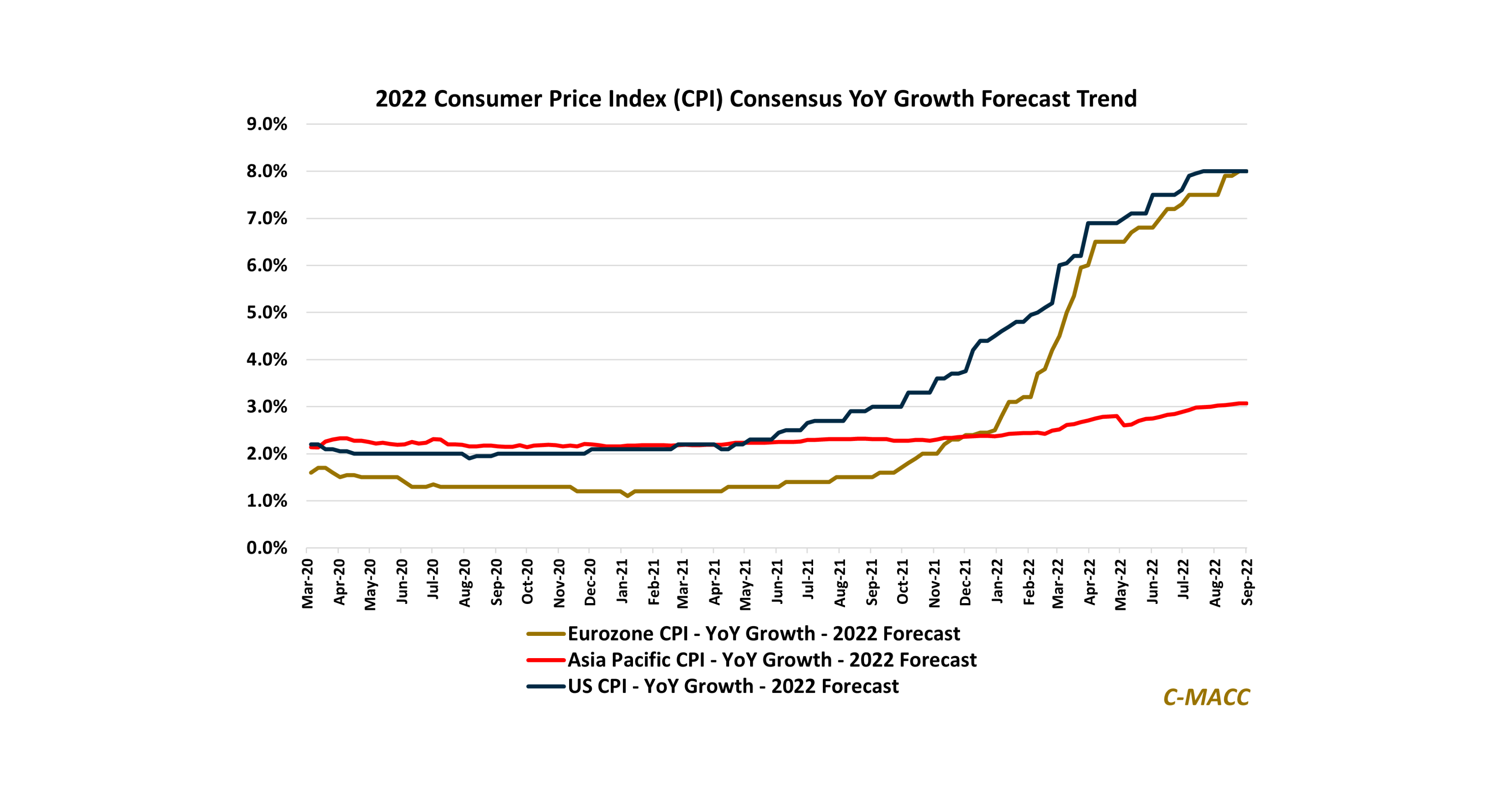

Western market consumers face greater price inflation than those in Asia in 2022, and most expect it to occur again in 2023. A plus for

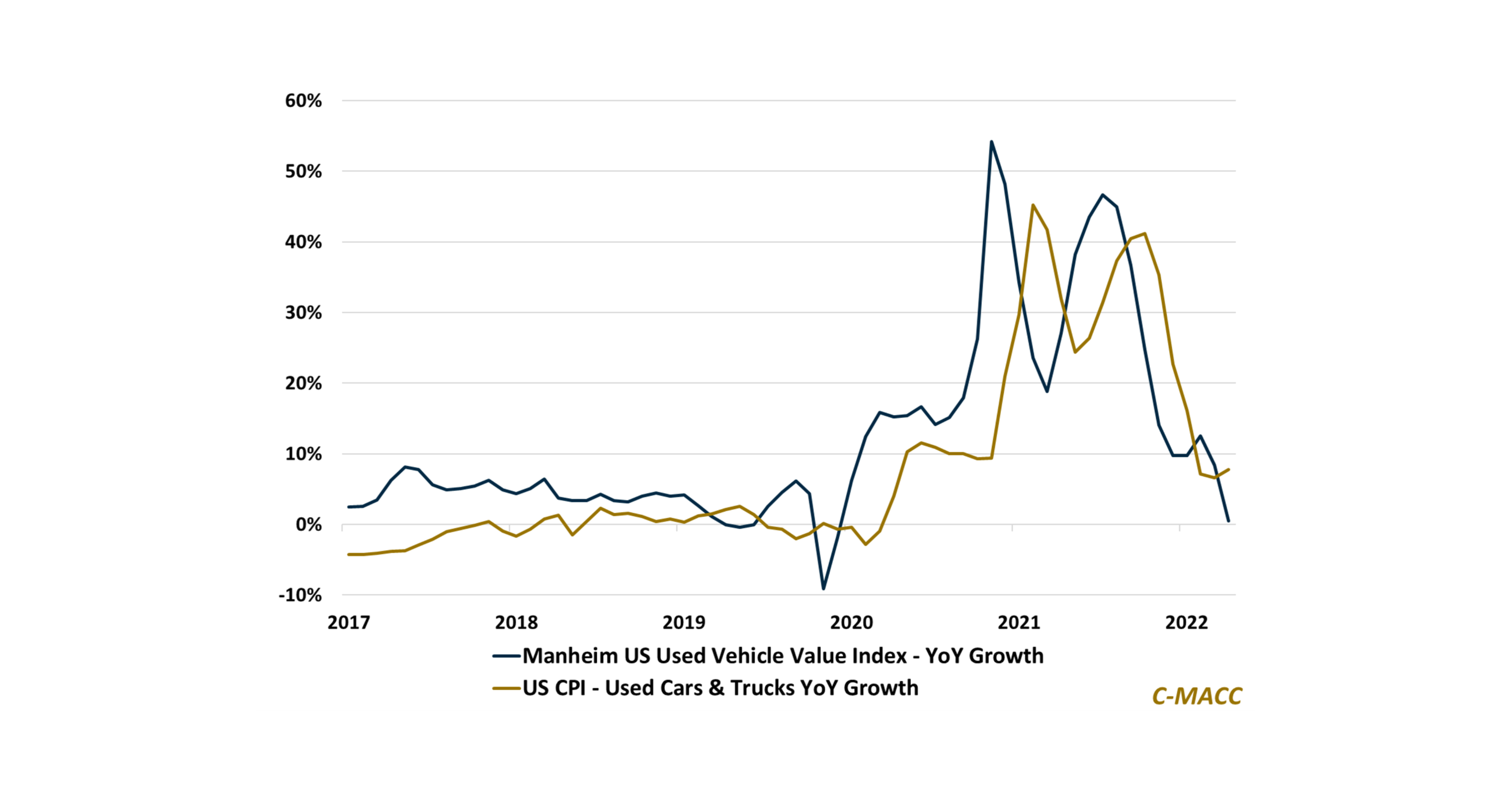

Consumer affordability indicators are braking amid rising borrowing costs and low confidence, positioning auto markets to hit a brick wall with chemical suppliers in tow.<br

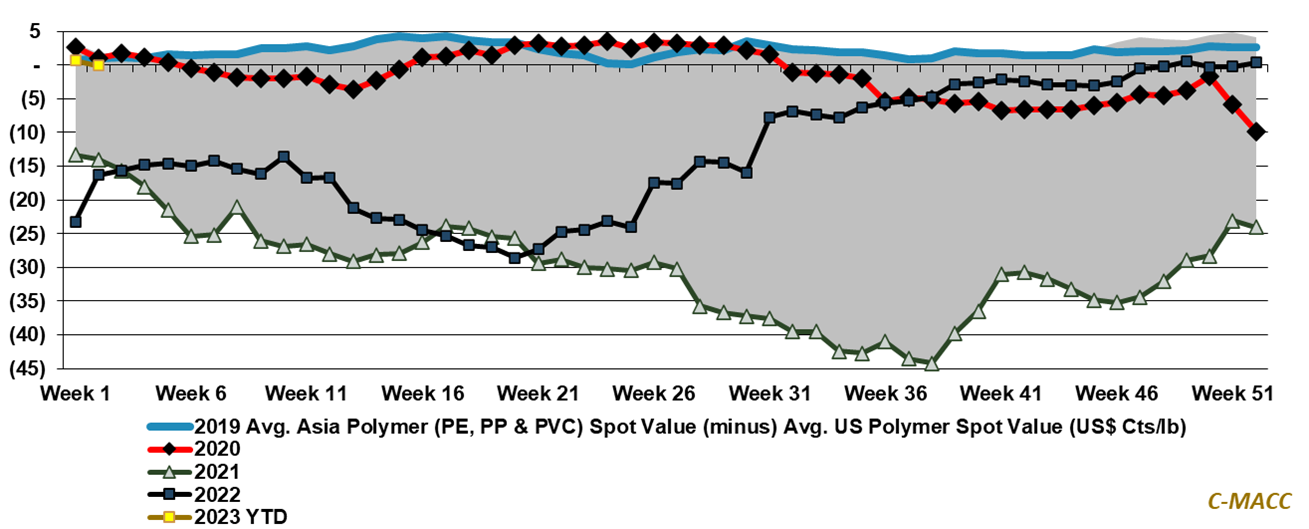

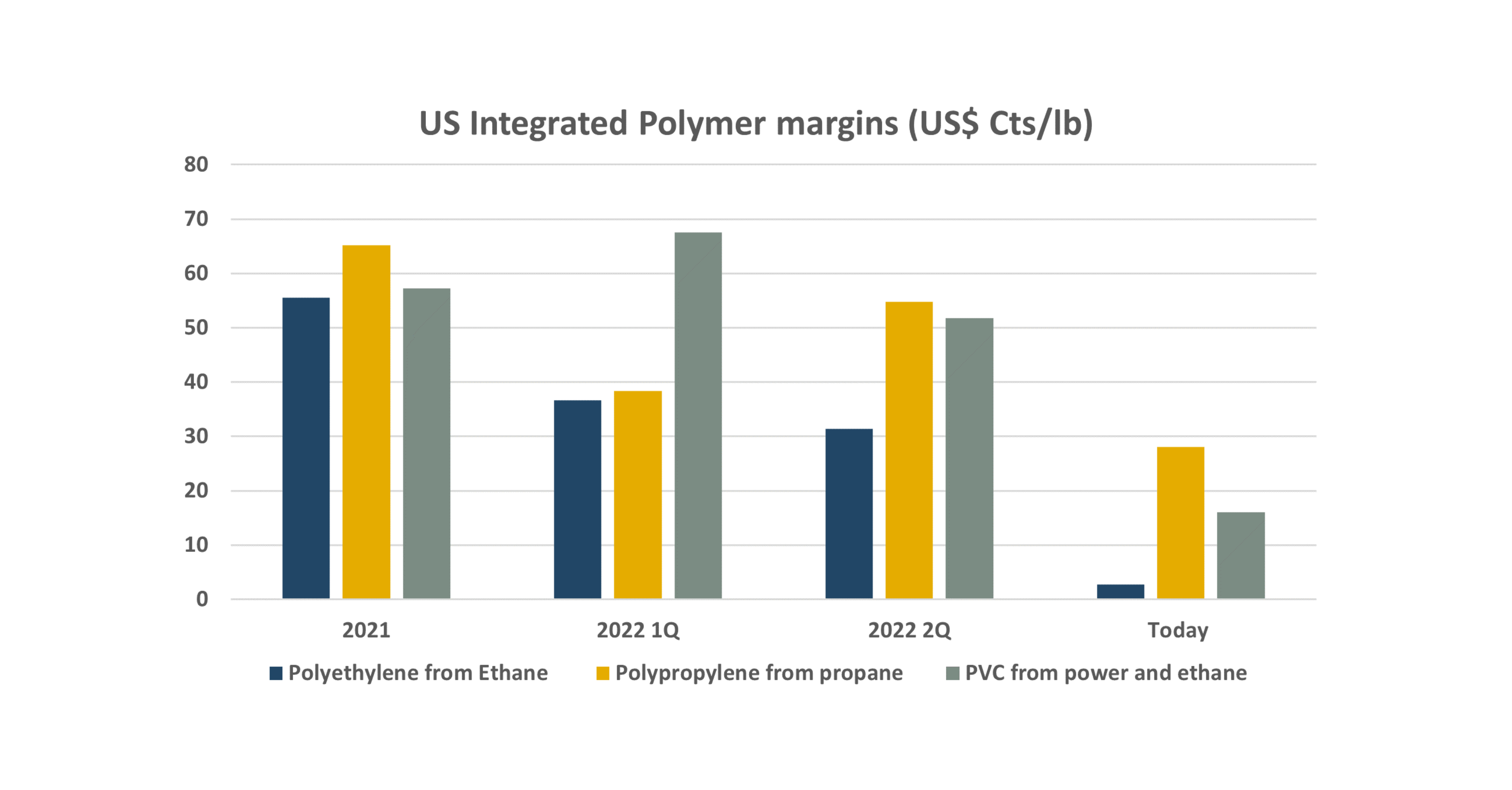

Global polymers and many other commodity chemicals have mostly fallen back to pre-covid levels. However, producer margins remain compressed amid high energy prices.

We

US refinery margins remain elevated and in favor of chemical production. We discuss its impact on propylene supply and why this market will likely be

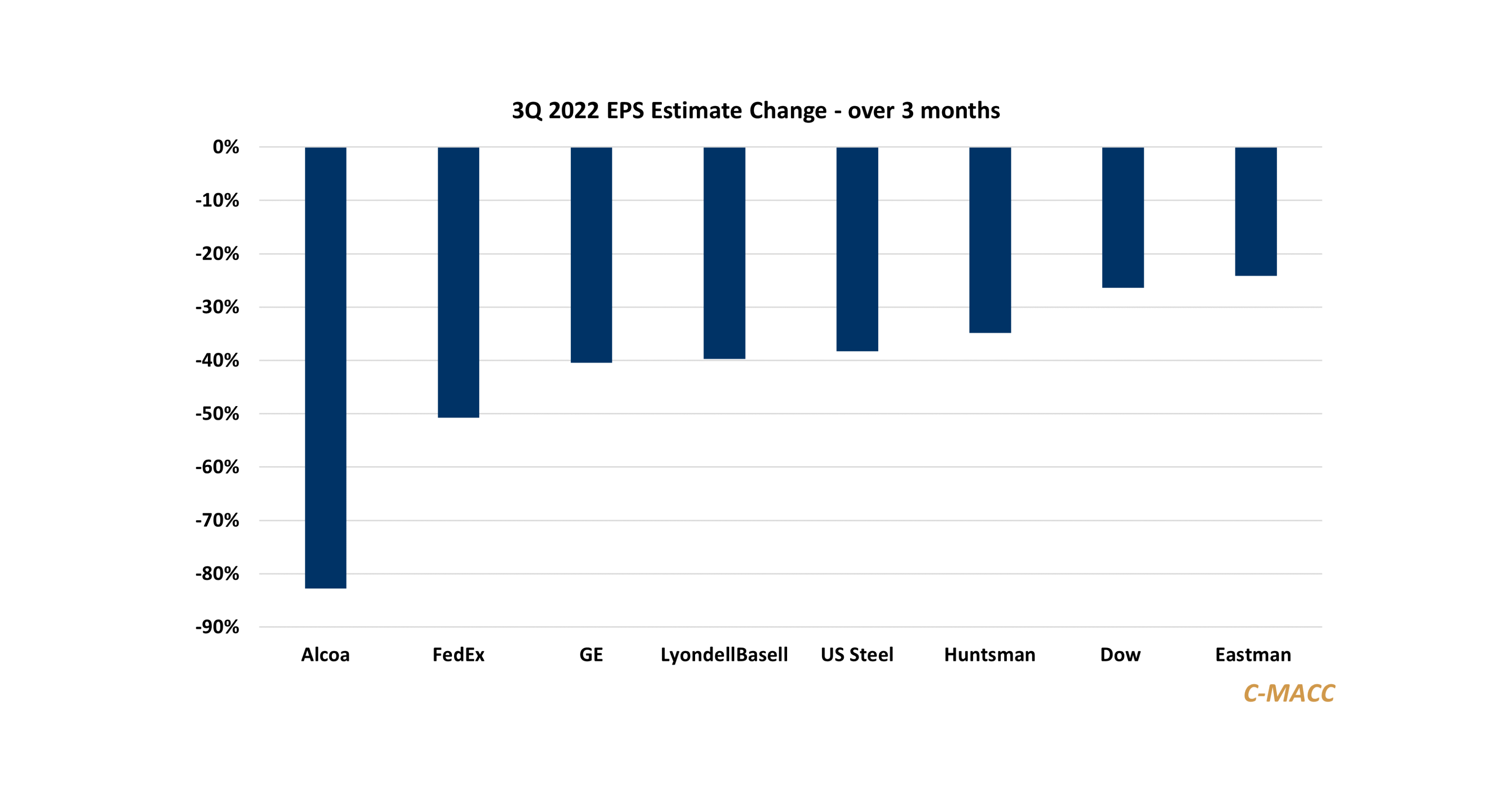

Sell-side equity research has become less about quality research than providing corporate concierge services – more estimate cuts are needed, but it could take time.<br

Chemical producers are increasingly cutting 3Q profit expectations but fail to give 4Q views despite Street estimates likely being too high – this is a

Eastman cuts its 3Q22 EPS target to a level 20% below the consensus view – we flag our research, Too Drunk To Drive – 2H22

Daily Chemical Reaction Playing The Long Game – Energy Sector Capex Drives To Chemicals, Europe Tries To Get Out Of The Bunker Key Points: We