Sunday Executive Summary

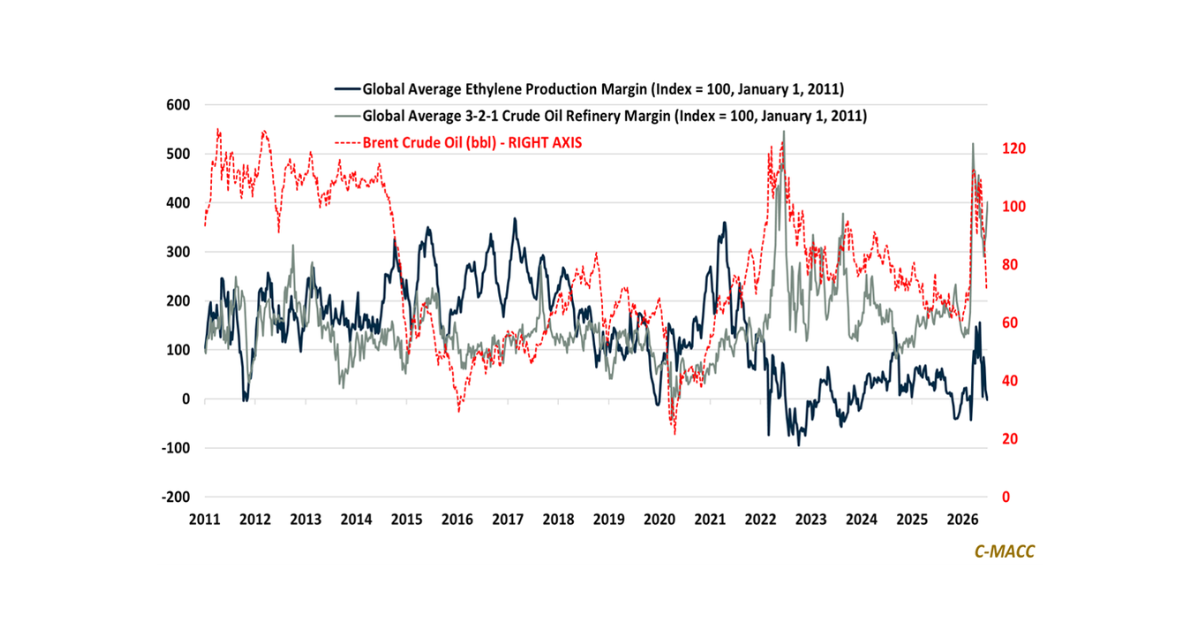

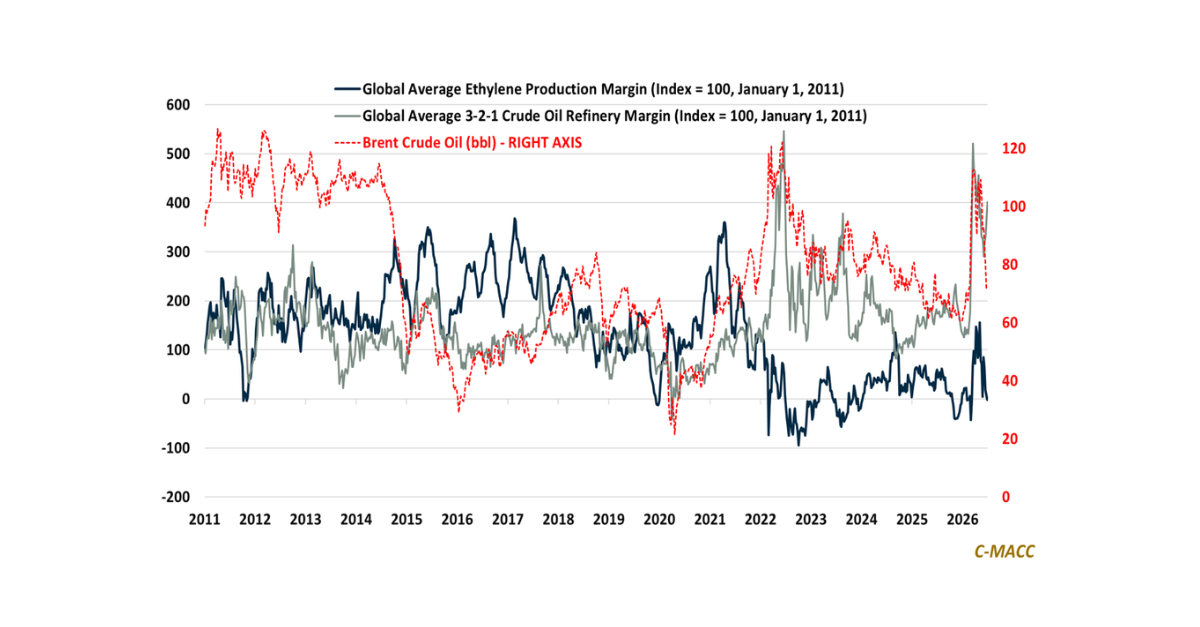

Global refining margins still outperform ethylene because tight fuel supply supports plant rates, although renewed Middle East tension has interrupted the latest decline in chemical

Global refining margins still outperform ethylene because tight fuel supply supports plant rates, although renewed Middle East tension has interrupted the latest decline in chemical

General Thoughts: Global chemical markets return to oversupply as cost curves flatten, while constrained refining supports firmer margins and steers capital toward fuels, integration, and

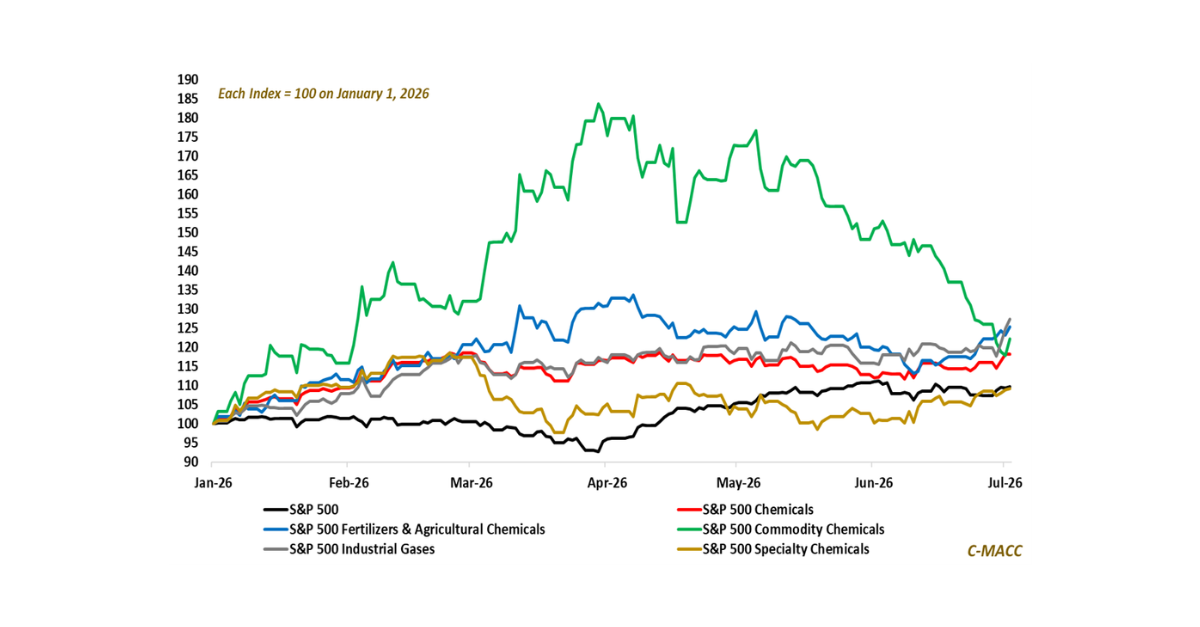

Chemical equities are turning defensive again, but the split is sharper as commodity and specialty sentiment weakens while fertilizers and industrial gases retain support.

Consensus

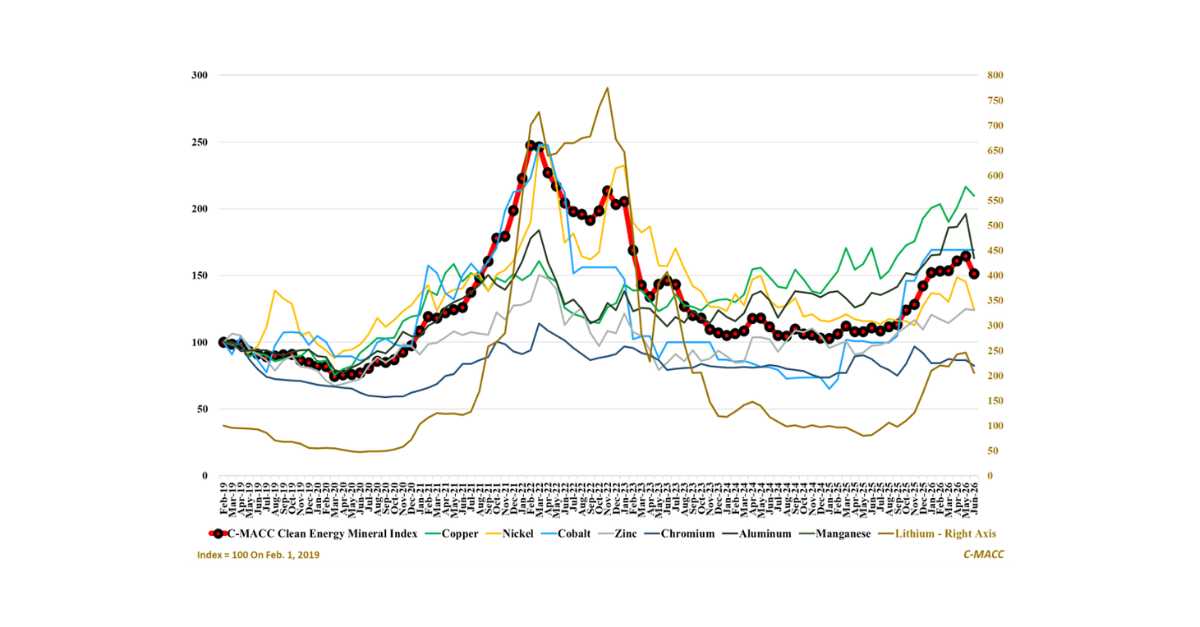

General Thoughts: June’s C-MACC Clean Energy Mineral Index pullback shows buyers paused after fossil-energy premiums faded, leaving each mineral to find support in its own

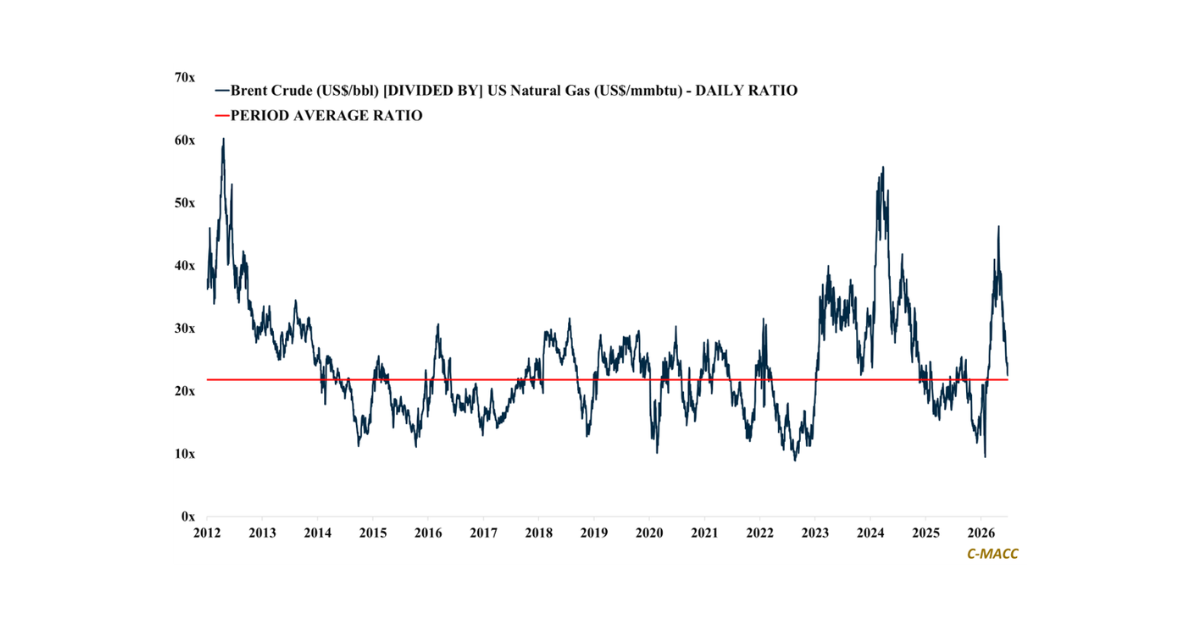

1H26 saw margins shift twice: conflict pricing rewarded reliable low-cost sellers in 1Q26, while falling oil-linked inputs gave buyers stronger leverage in 2Q value-chain negotiations

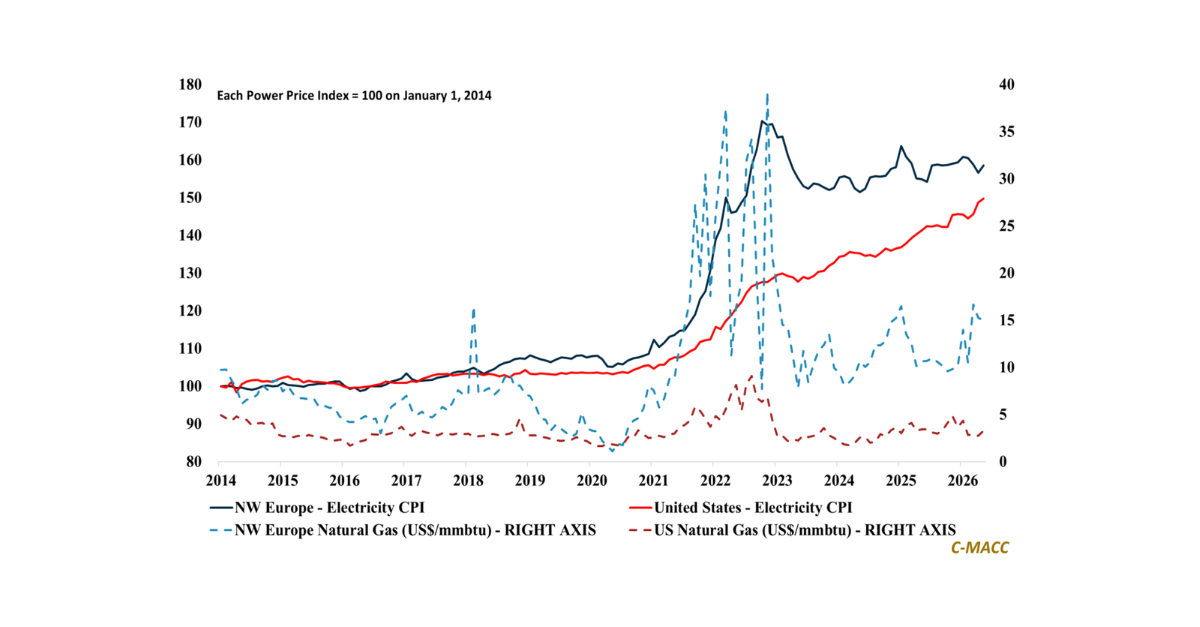

Regional and local electricity price inflation has become a signal of global competitiveness, as sticky power prices push buyers toward lower-cost supply options, while some

Chemical and polymer prices have retreated from peak 1H26 levels, but many remain above January levels, leaving buyers to judge whether relief is temporary or

General Thoughts: Supply risk is keeping many chemical chains biased upward, with MDI markets showing how outage timing and system availability can sustain hikes even

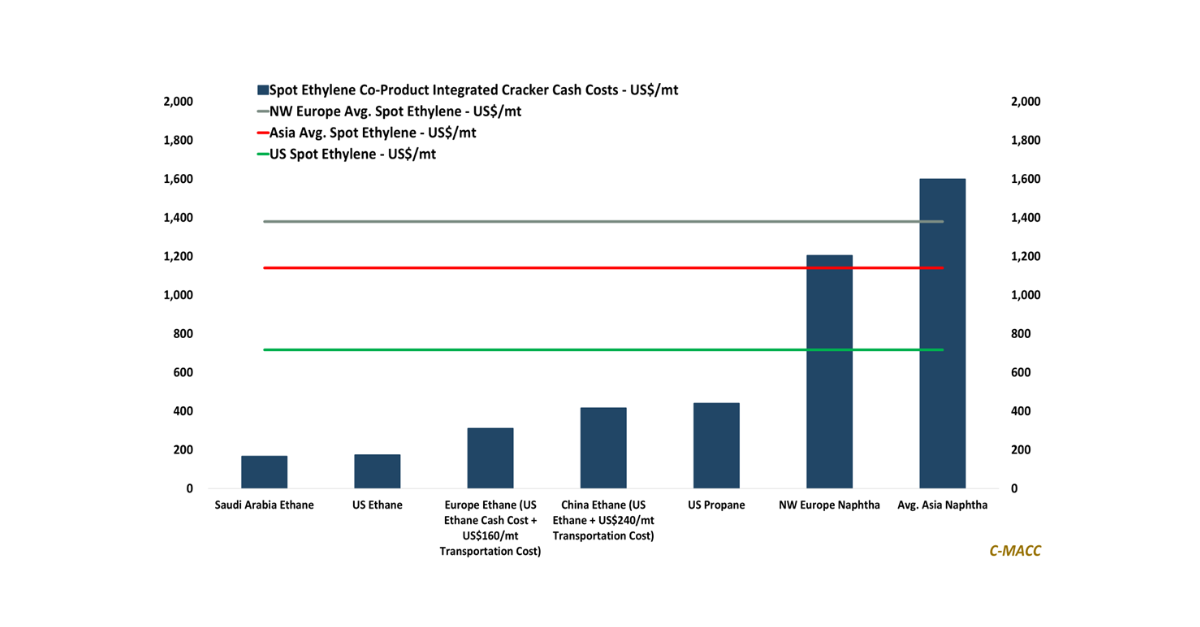

Asia’s olefins cost-recovery squeeze is forcing ex-China asset reviews, as naphtha-based production costs exceed those in Europe and Chinese exports limit derivative price recovery.

Europe’s

Affordability constraints increasingly determine pricing durability as manufacturers defend margins through promotions, inventory timing, and customer prioritization rather than demand growth.

Reliable supply commands rising