Sunday Executive Summary

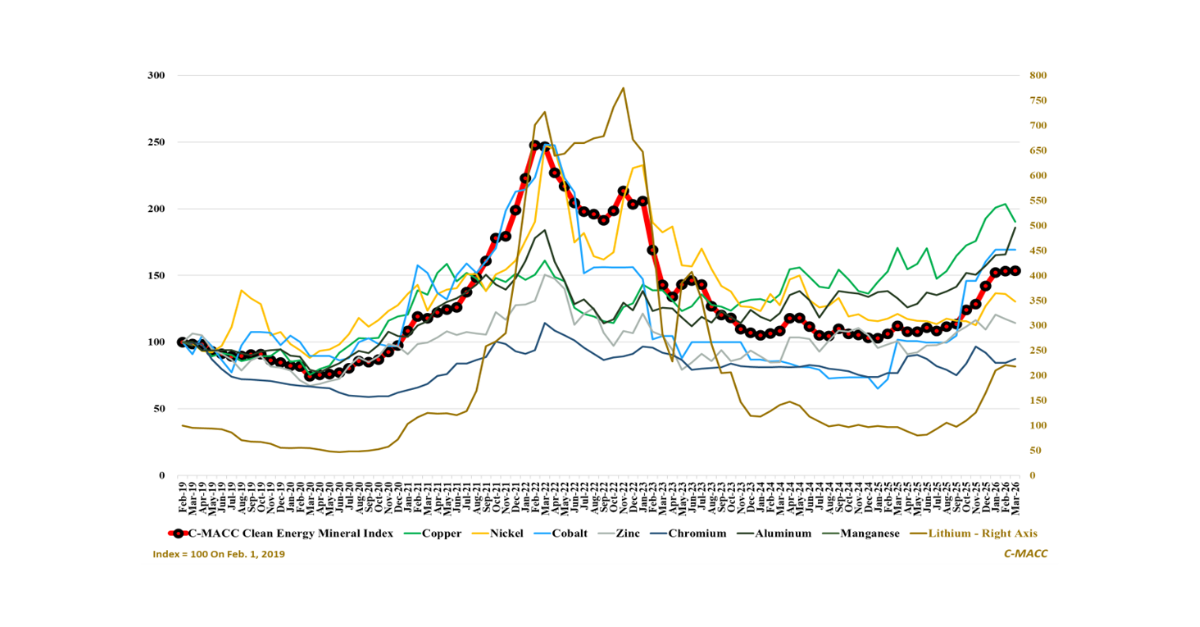

Critical minerals diverge as electrification costs fall structurally, confirming inputs are no longer the binding constraint and decisively shifting advantage toward systems that deliver reliable

Critical minerals diverge as electrification costs fall structurally, confirming inputs are no longer the binding constraint and decisively shifting advantage toward systems that deliver reliable

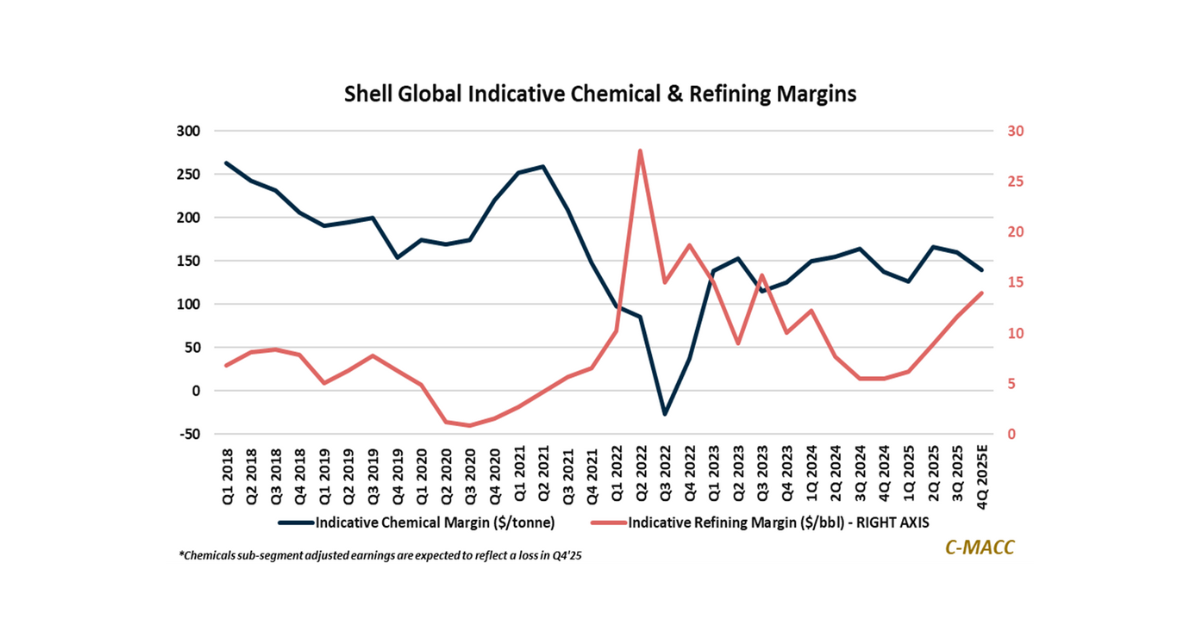

General Thoughts: Global energy shocks, narrowing sanctioned crude oil discounts, and persistent olefin oversupply converge to lift marginal costs, accelerate restructuring, and benefit gas-advantaged producers.

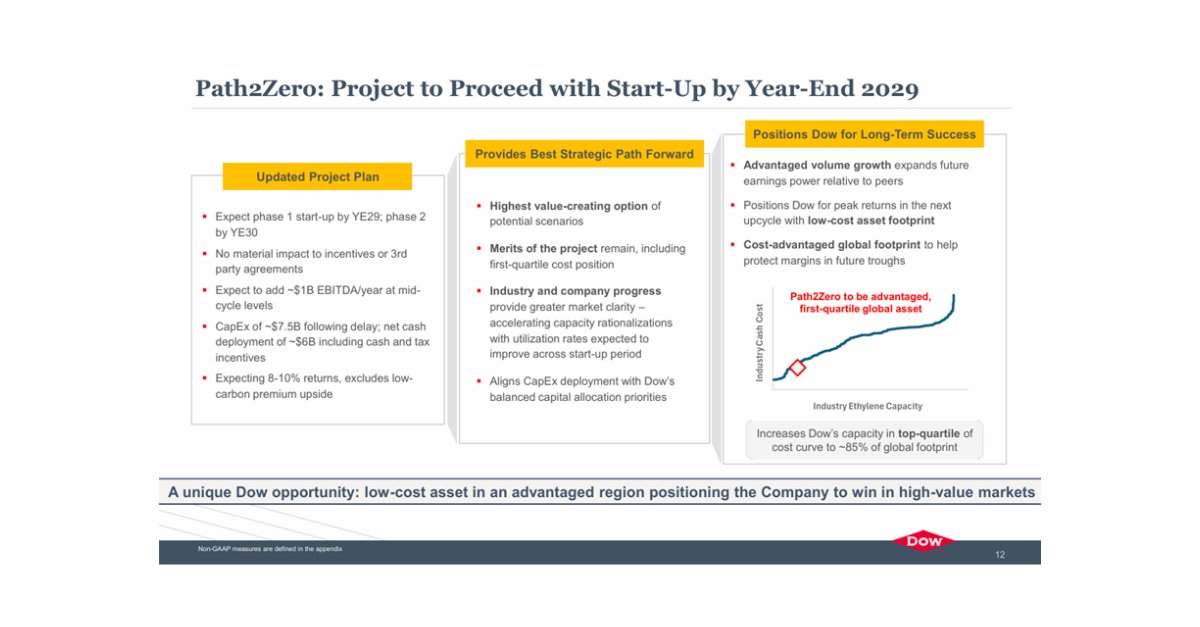

General Thoughts: Global chemical restructuring optimizes footprints, shrinks effective supply, and embeds optionality, positioning low-cost, low-carbon assets like Dow’s Path2Zero to lift returns in the

General Thoughts: Weather-driven global natural gas inflation supports higher chemical prices despite relative cost positions holding, with chemical margins compressing absent structural supply cuts.

Supply

China’s slowing consumption and persistently low relative price inflation push excess supply outward, reviving export-led clearing and intensifying global price competition as logistics increasingly normalize

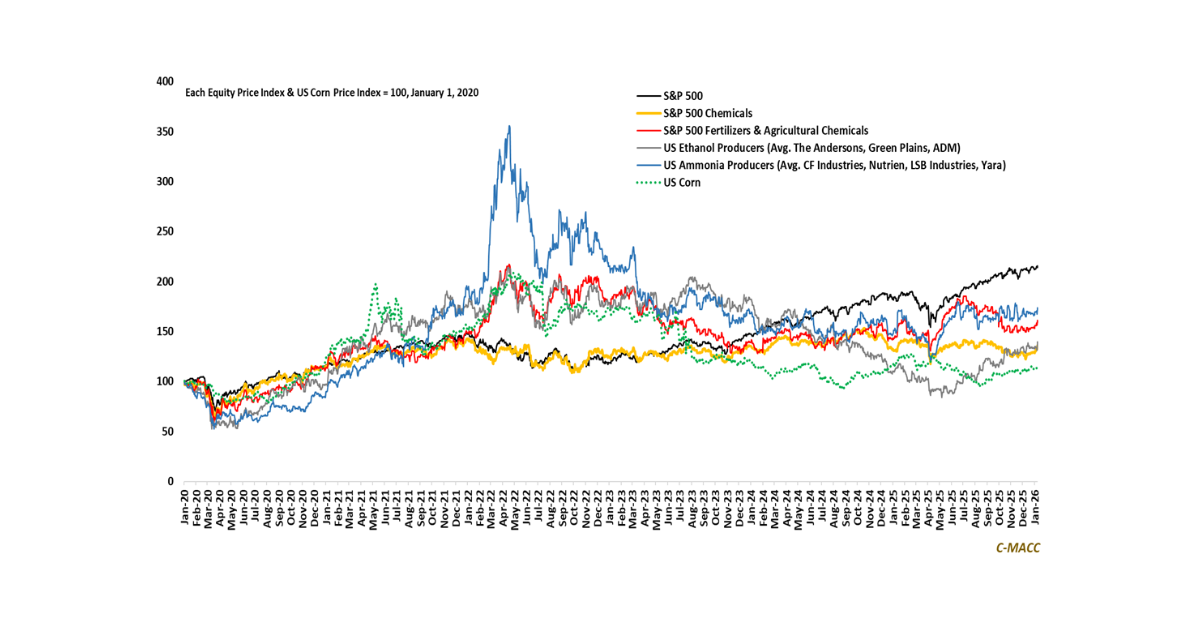

The fundamental health of the global ammonia market increasingly hinges on logistics, reliability, and timing constraints, making basis risk and seasonal timing more decisive than

General Thoughts: Global chemical downturn into 2026 will force ownership change and capital discipline, restructuring across Europe and Asia ex-China, while redefining low-cost integration as

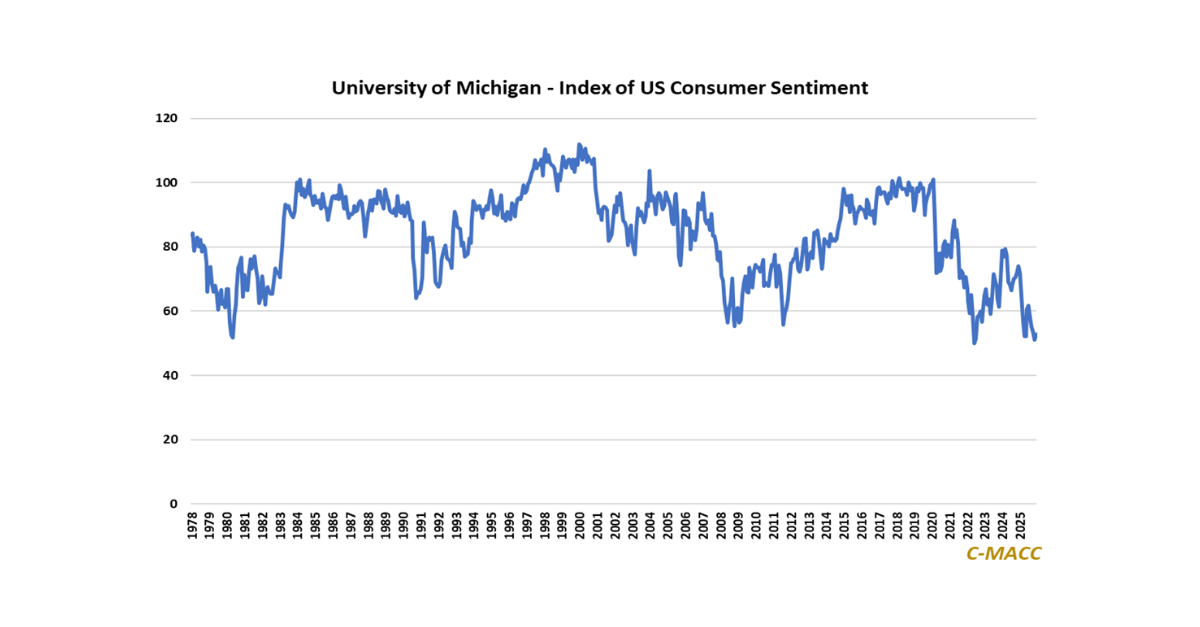

Depressed consumer sentiment and weak business expectations imply demand will not offset oversupply, with 2026 outcomes more likely to be determined by restructuring discipline rather

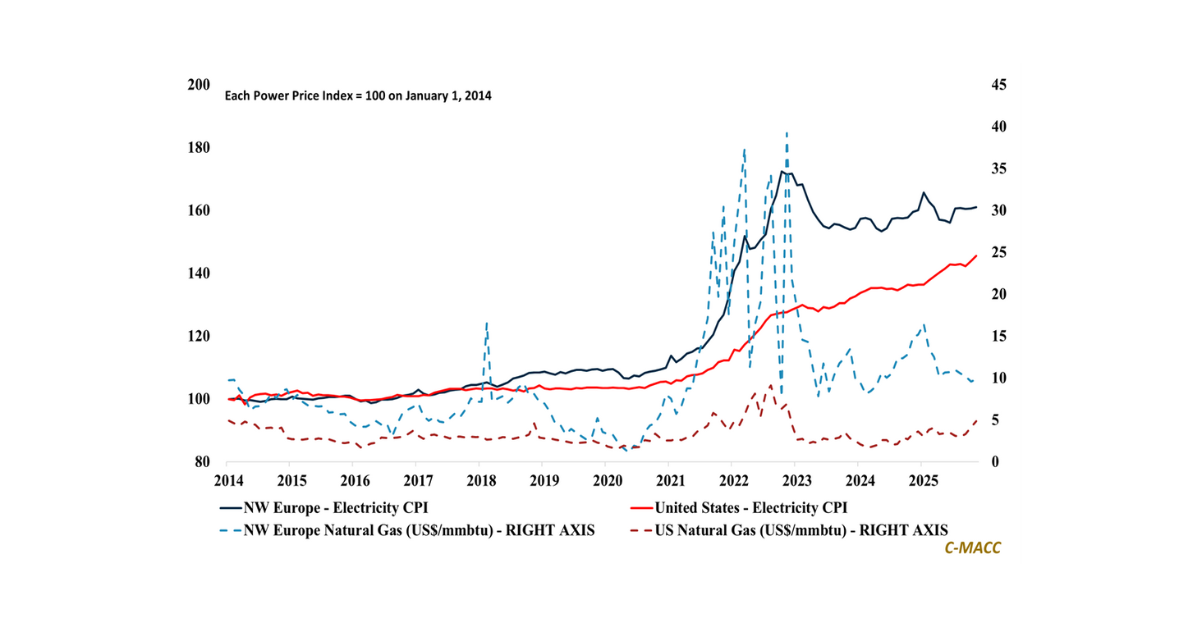

Chemical sector outcomes in 2026 will hinge more on managing volatility across power, gas, and policy, not on forecasting averages, as infrastructure constraints and capital

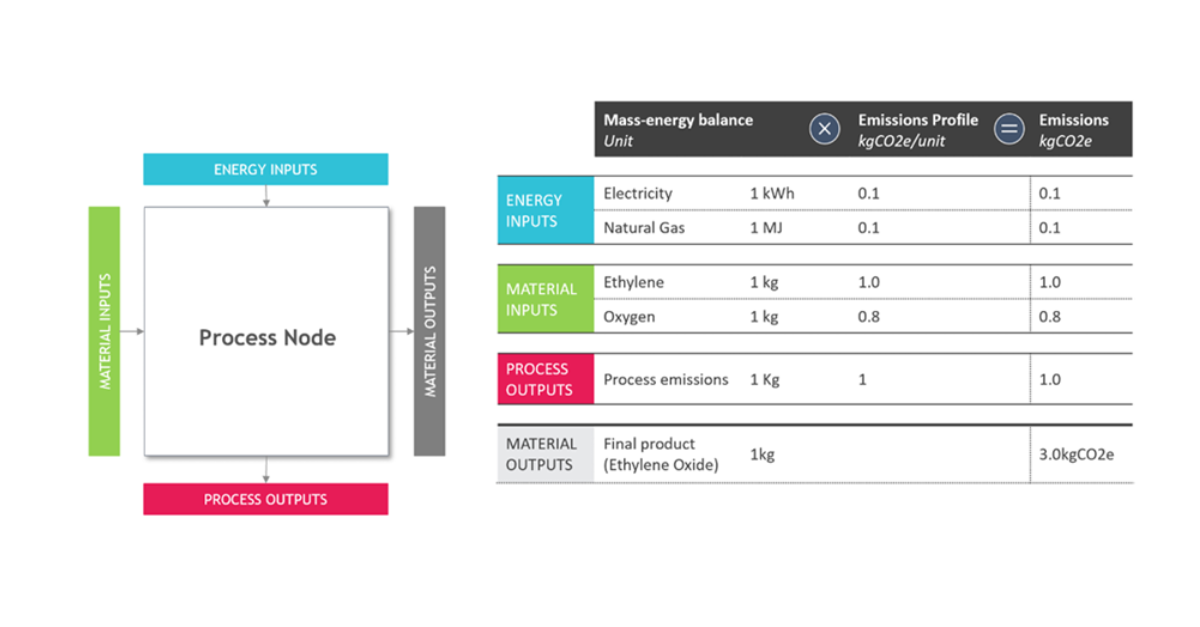

1st Topic of the Week: If verified product-level sustainability increasingly decides access and win rates, which chemical and polymer producers gain pricing power, and which