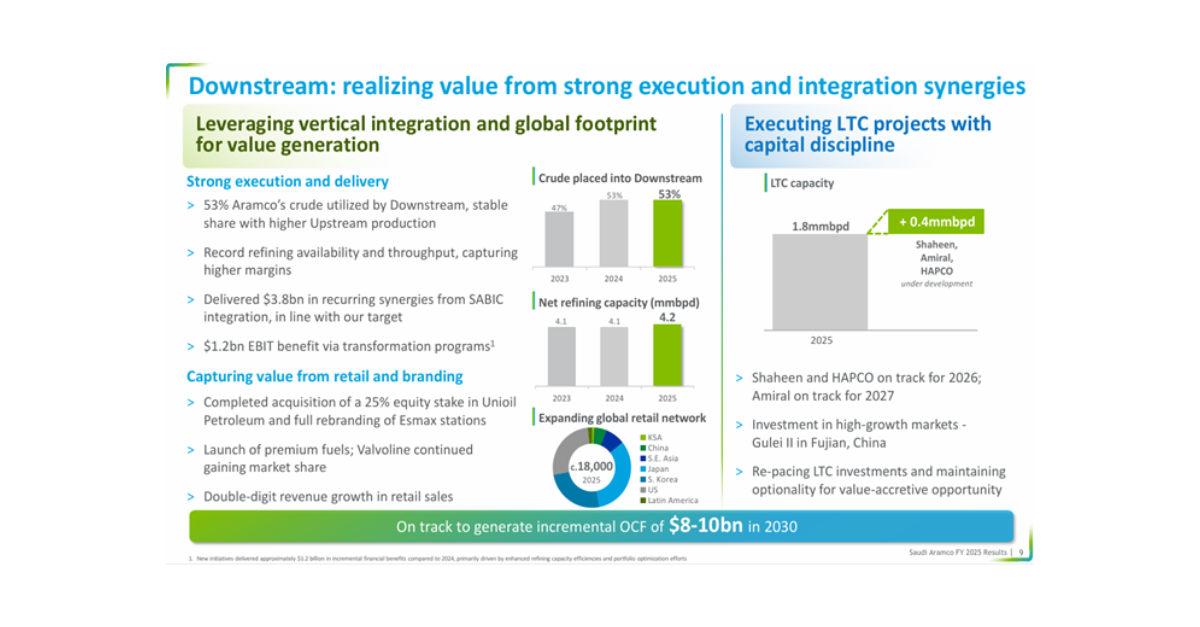

Global Market Analysis

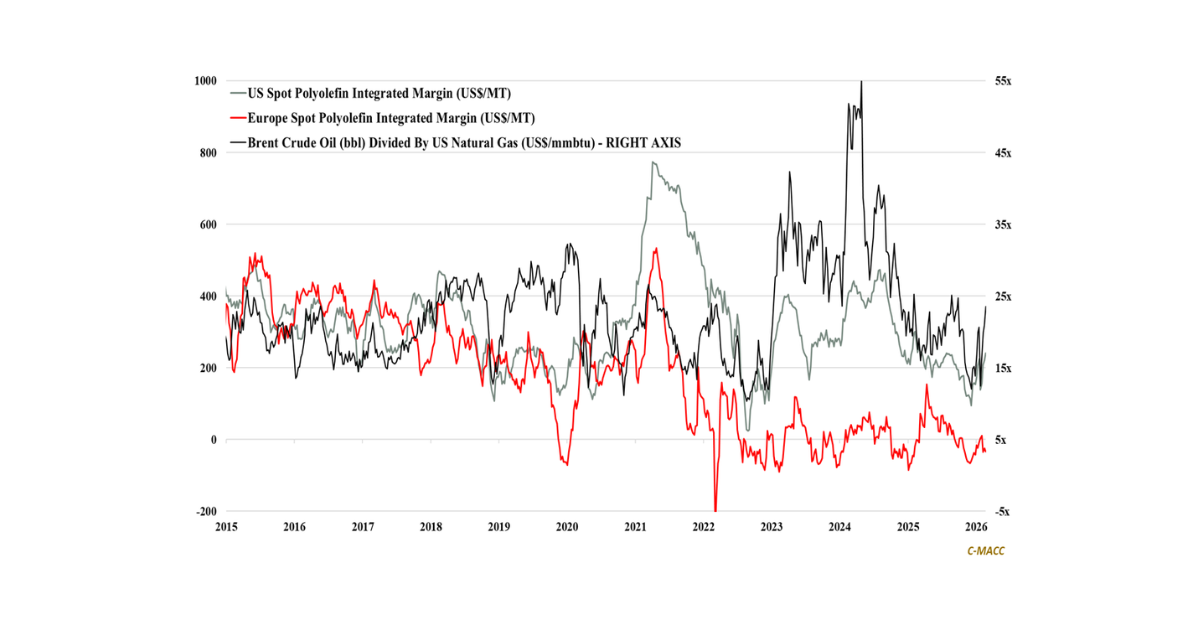

General Thoughts: Integration, logistics flexibility, and feedstock advantage are increasingly replacing scale as the chemical sector’s defining competitive edge, steering capital toward integrated production platforms.

General Thoughts: Integration, logistics flexibility, and feedstock advantage are increasingly replacing scale as the chemical sector’s defining competitive edge, steering capital toward integrated production platforms.

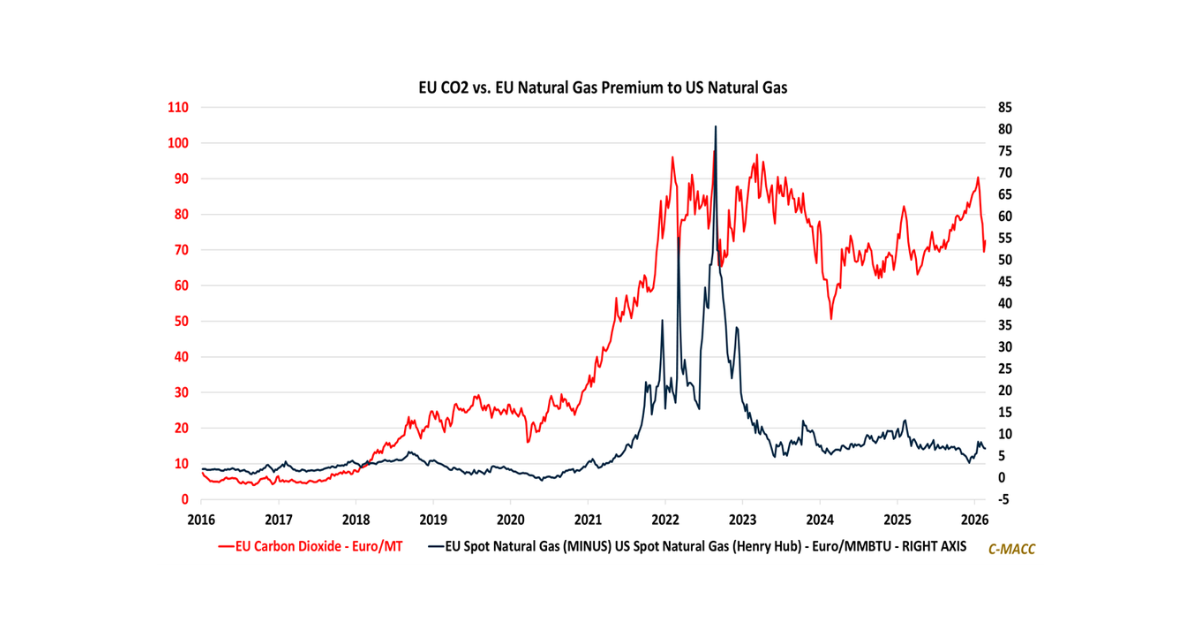

Europe’s chemical sector return outlook now hinges far less on cyclical recovery and far more on feedstock structure, carbon exposure, and policy-backed demand durability amid

General Thoughts: Simultaneous natural gas and carbon price compression eases Europe’s cost burden, yet demand fragility, structural import dependence, and risk of renewed global tightening

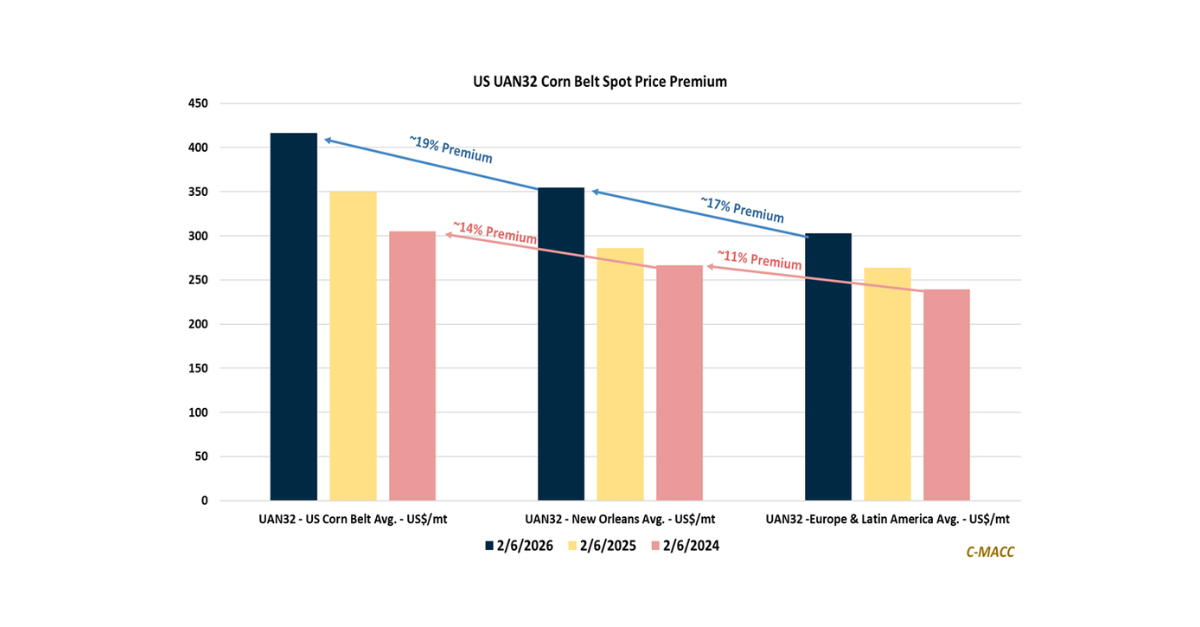

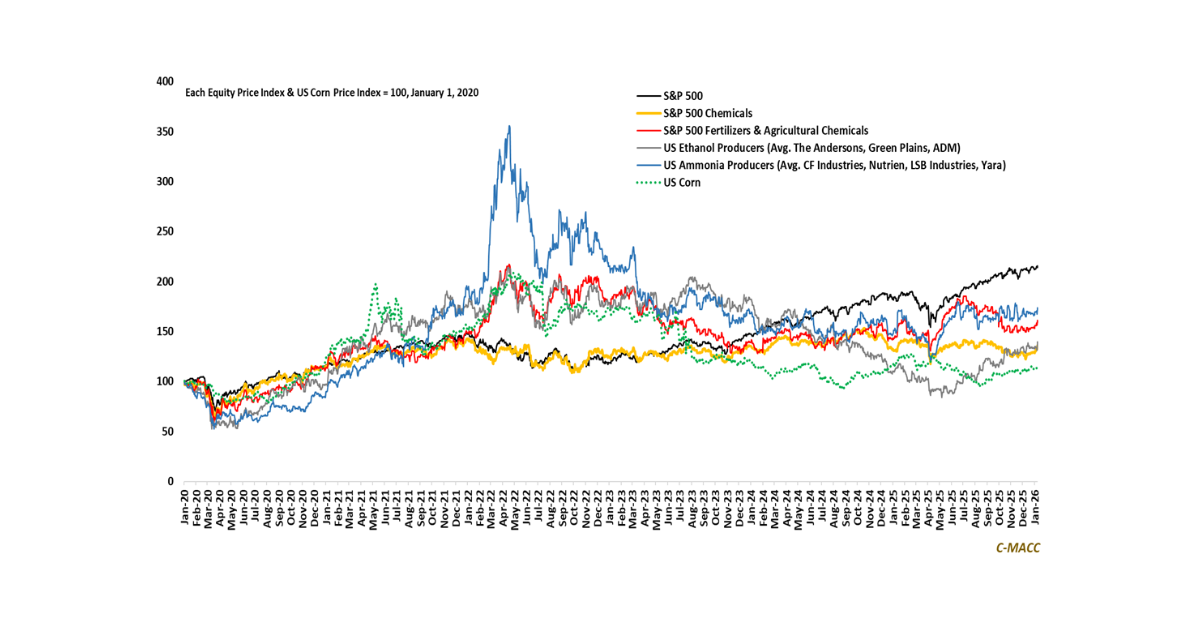

General Thoughts: Nitrogen’s outlook hinges on acreage elasticity, not ammonia rhetoric: a corn-to-soy shift could reset demand, pricing power, and capital discipline, especially if low-carbon

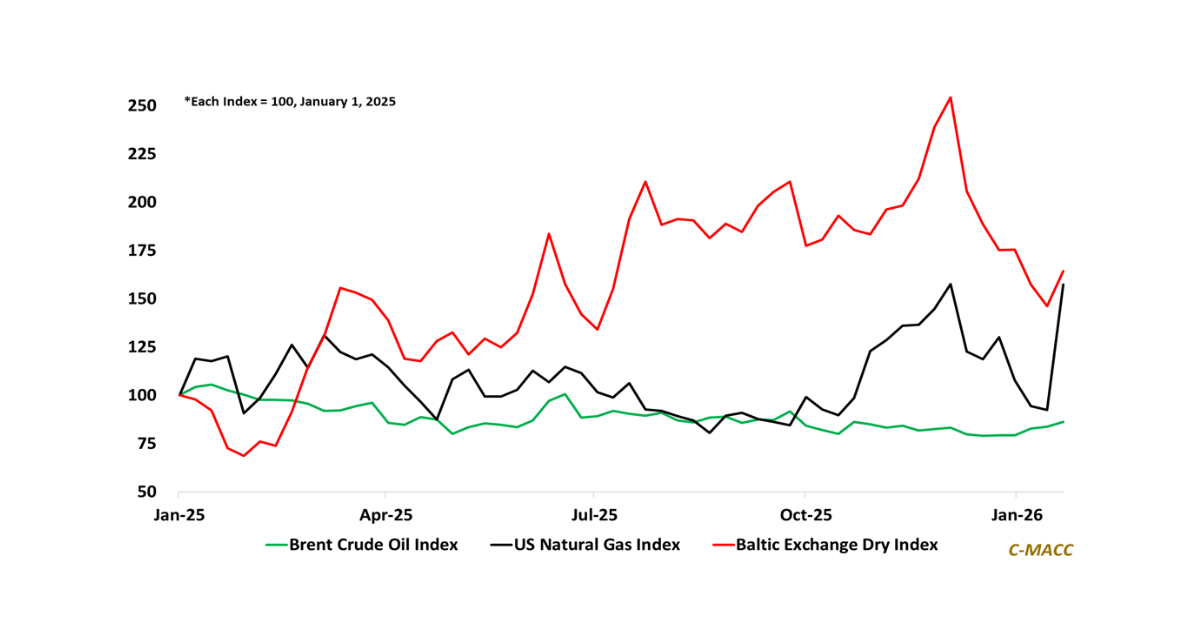

Liquidity governs commodity outcomes as volatility and freight normalization compress timing buffers, elevating focus on cash conversion discipline over utilization in 4Q25 results and 2026

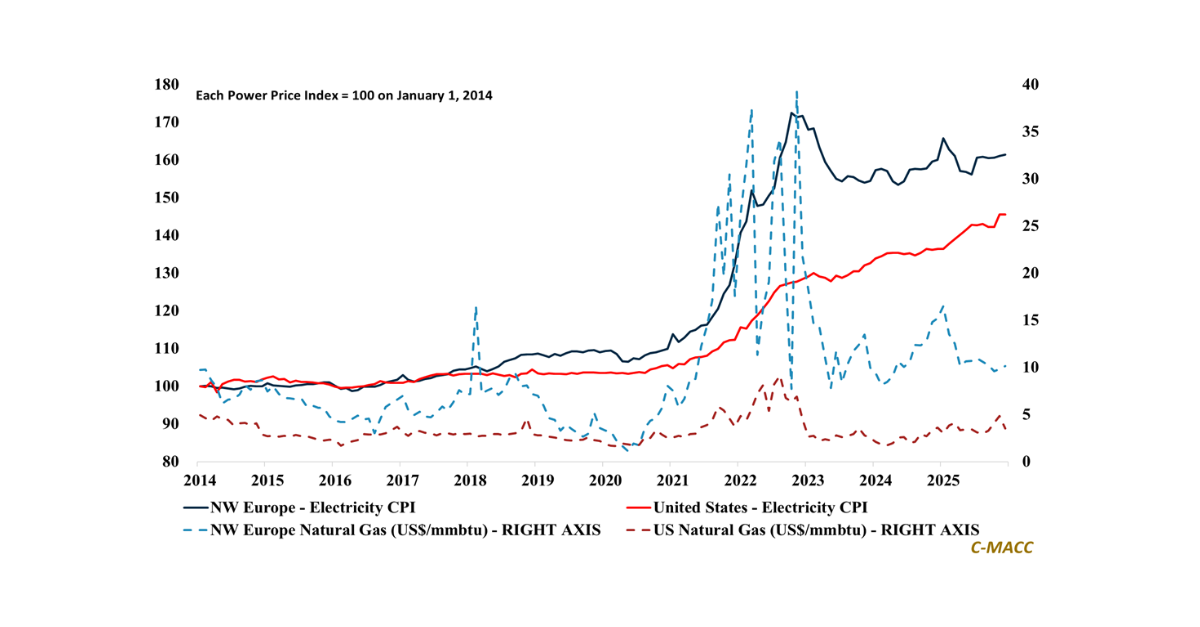

1st Topic of the Week: Europe’s power transition masks rising volatility, constrained availability, and marginal gas pricing. Can grid build-out and storage scale fast enough

General Thoughts: Weather-driven global natural gas inflation supports higher chemical prices despite relative cost positions holding, with chemical margins compressing absent structural supply cuts.

Supply

General Thoughts: Energy volatility, logistics, and policy shape margins across chemicals, agriculture, and fuels, favoring low-cost, disciplined operators as global markets transition toward execution-driven balance

The fundamental health of the global ammonia market increasingly hinges on logistics, reliability, and timing constraints, making basis risk and seasonal timing more decisive than

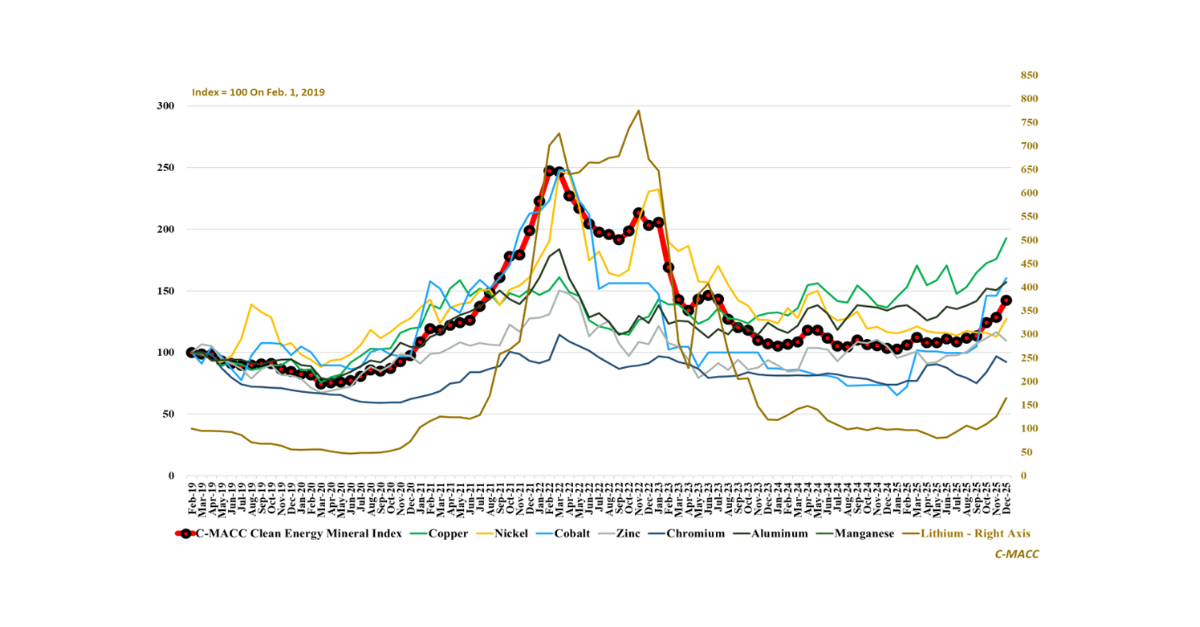

1st Topic of the Week: Are copper and lithium entering a policy-anchored price regime where security-driven supply caps upside while speculative flows amplify volatility across