Sunday Executive Summary

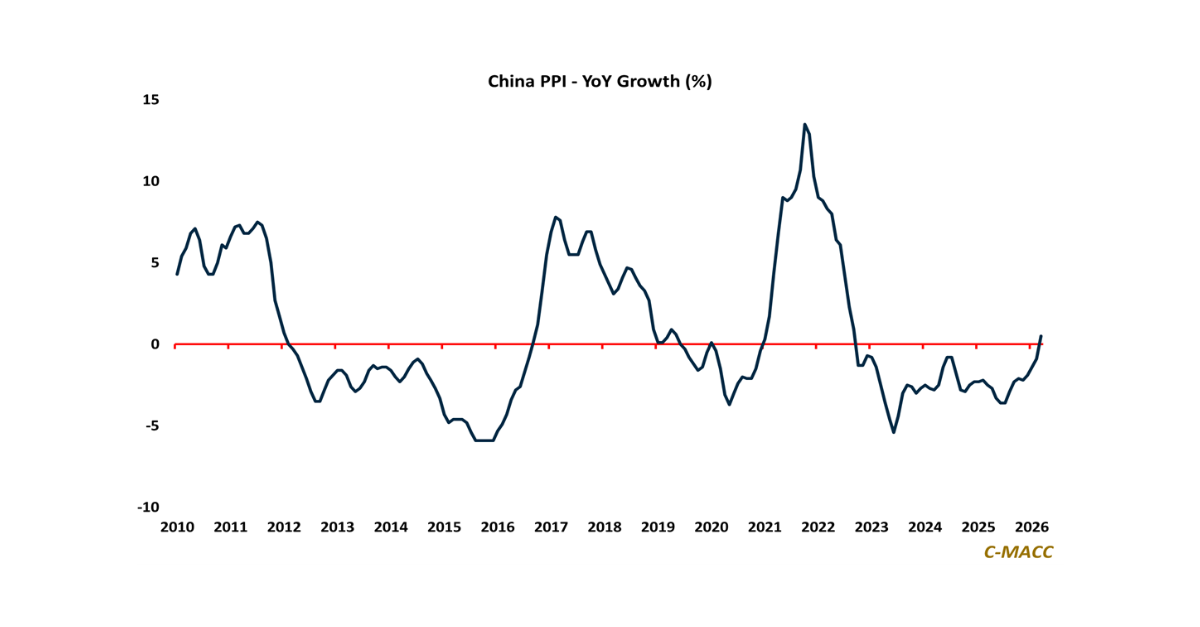

China’s 0.5% YoY factory-gate inflation in March removed a trusted global relief valve, forcing markets to underwrite firmer resin and intermediate floors, slower cost deflation,

China’s 0.5% YoY factory-gate inflation in March removed a trusted global relief valve, forcing markets to underwrite firmer resin and intermediate floors, slower cost deflation,

General Thoughts: Industrial value is shifting toward integrated systems that manage energy, logistics, and continuity to protect margins, as disruption fragments markets and limits standalone

General Thoughts: Global energy shocks, narrowing sanctioned crude oil discounts, and persistent olefin oversupply converge to lift marginal costs, accelerate restructuring, and benefit gas-advantaged producers.

China’s slowing consumption and persistently low relative price inflation push excess supply outward, reviving export-led clearing and intensifying global price competition as logistics increasingly normalize

General Thoughts: Early-2026 cost-curve shifts amid persistent chemical market oversupply are forcing restructuring, with clear evidence likely emerging in 4Q25 results and more decisive 2026

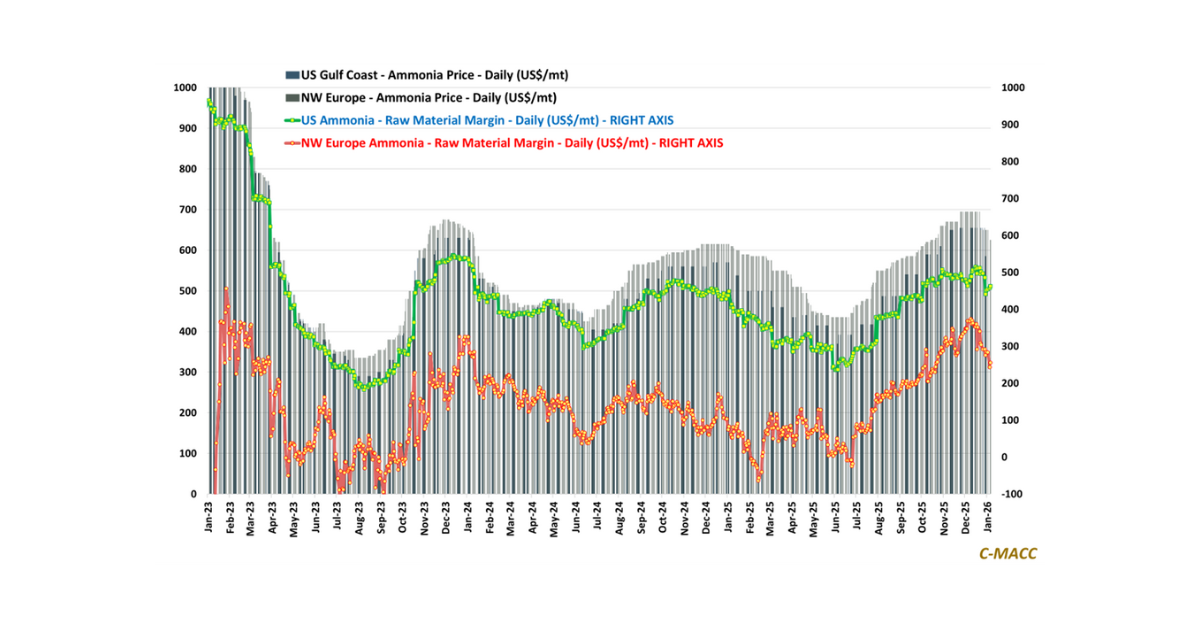

General Thoughts: Ammonia markets hinge on reliability, not recovery, keeping prices elevated as supply additions lag volatility, farmer demand flexes, and integrated low-cost producers outperform

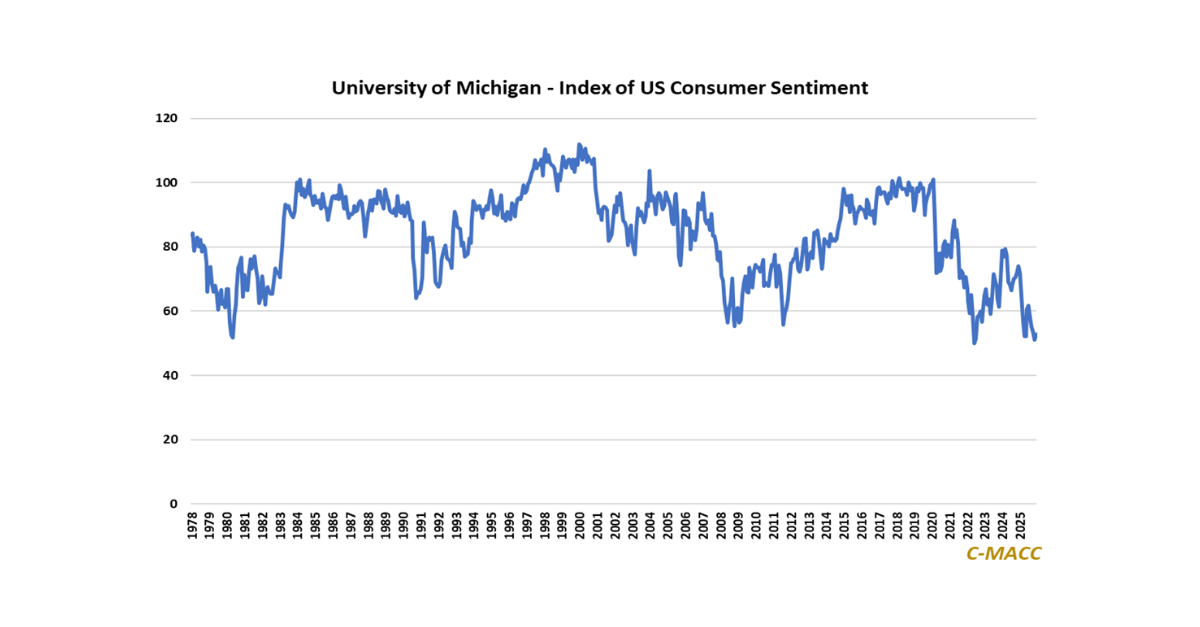

Depressed consumer sentiment and weak business expectations imply demand will not offset oversupply, with 2026 outcomes more likely to be determined by restructuring discipline rather

Chemical sector outcomes in 2026 will hinge more on managing volatility across power, gas, and policy, not on forecasting averages, as infrastructure constraints and capital

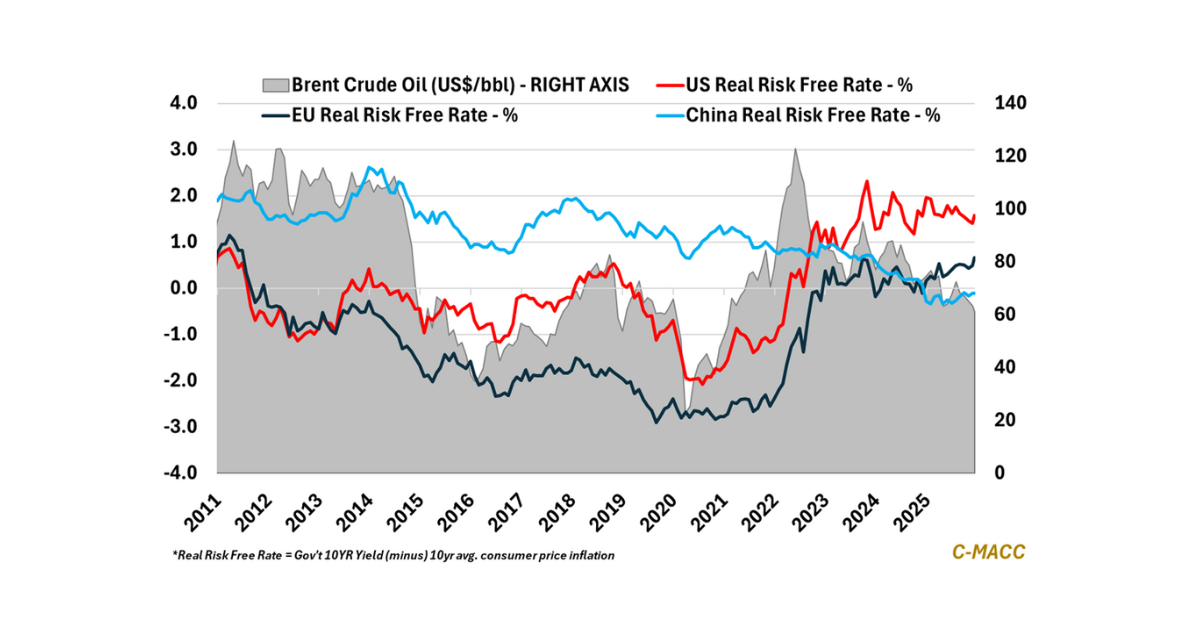

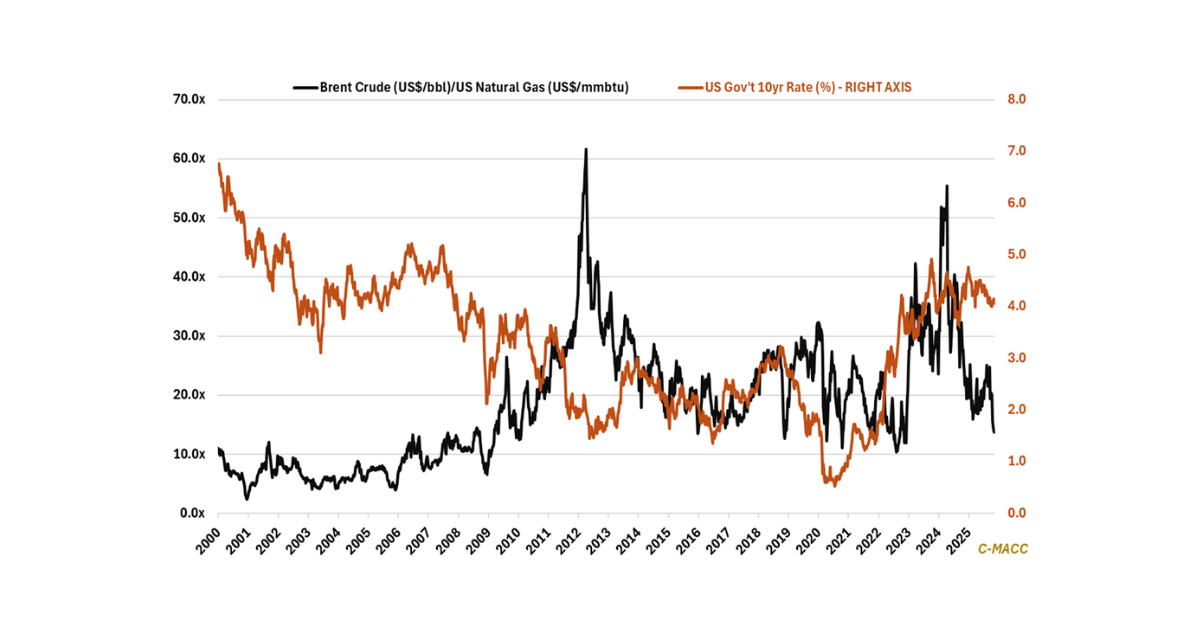

Global Market Analysis There Will Be Blood, Closures: Global Return Hurdles Further Harden Into 2026 Key Findings Exhibit 1: Real rates strengthen globally in late

Procurement-led synergy engines, not scale alone, are increasingly becoming the primary determinant of industrial competitiveness in a high-cost-capital, low-growth world increasingly defined by structural volatility.