Sustainability & Energy Transition

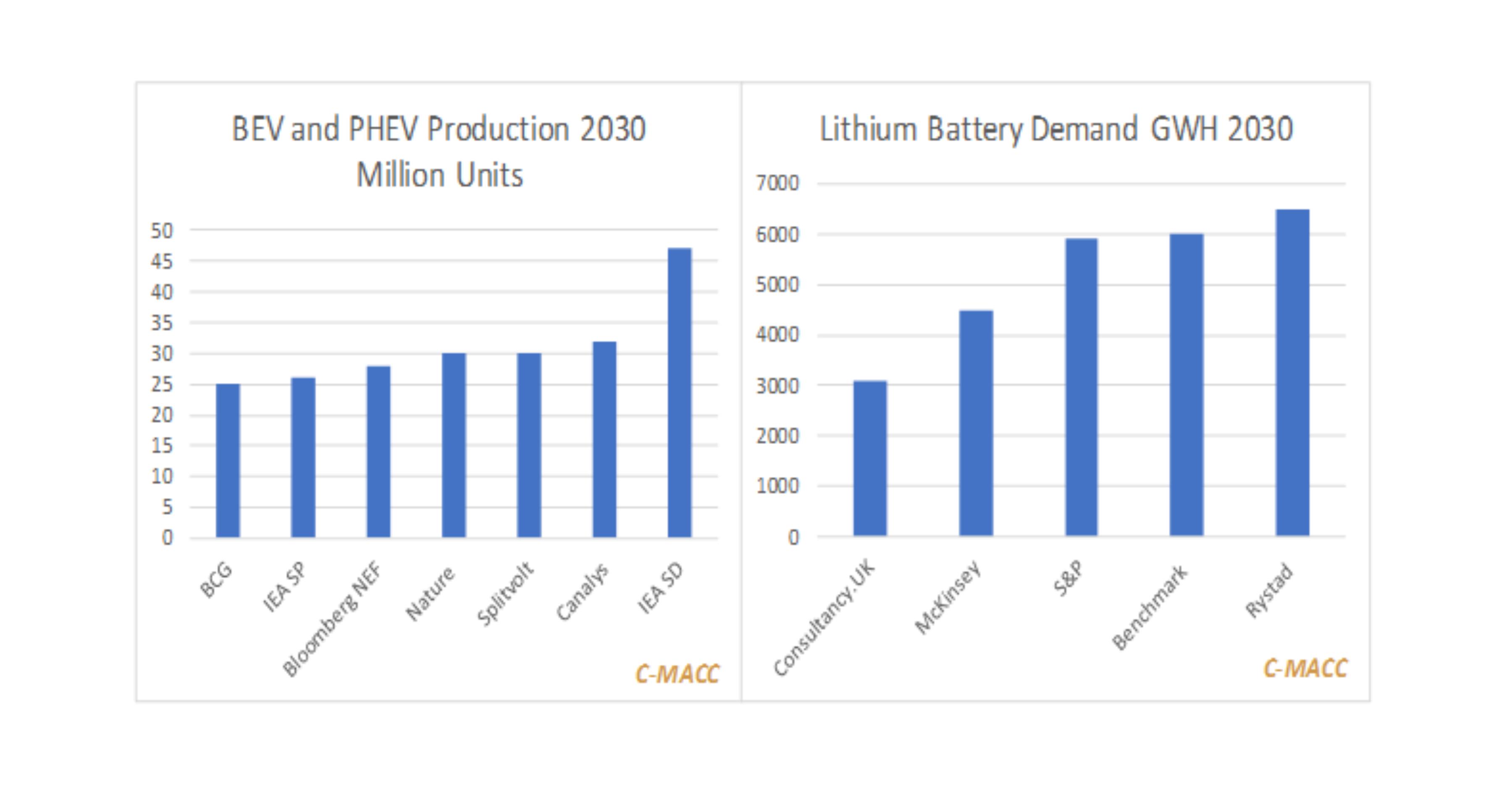

Most believe battery demand will increase quickly, but outlooks significantly vary as to how fast – the low end of the range is challenging, the

Most believe battery demand will increase quickly, but outlooks significantly vary as to how fast – the low end of the range is challenging, the

The profit headwinds that faced US petrochemical producers in 2Q were higher at the end of the quarter relative to its start. We advise corporates

Consensus energy transition and emission views appearing possible post COP26 are on shaky ground as politicians (especially in Europe) face bigger challenges.

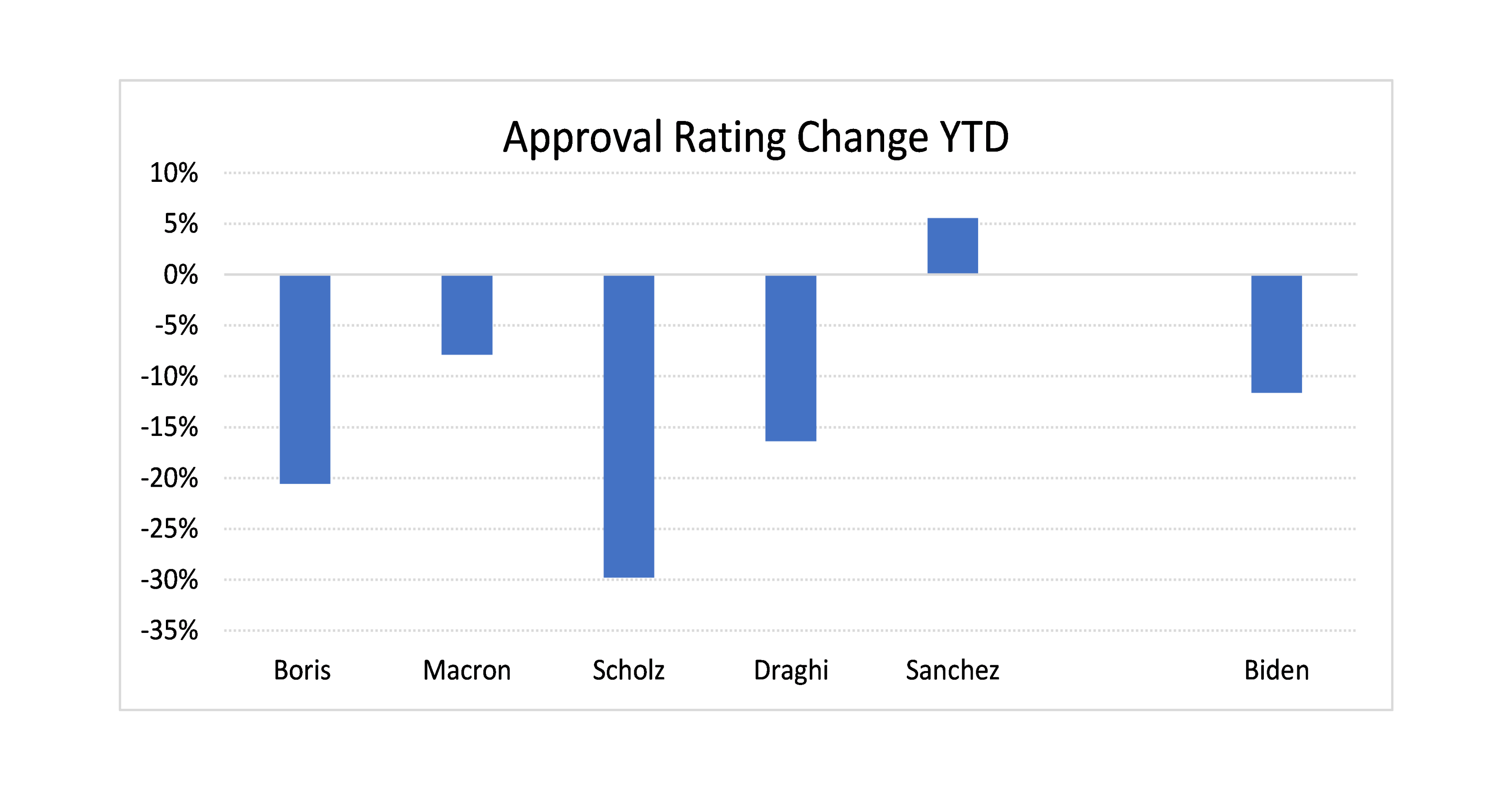

As approval

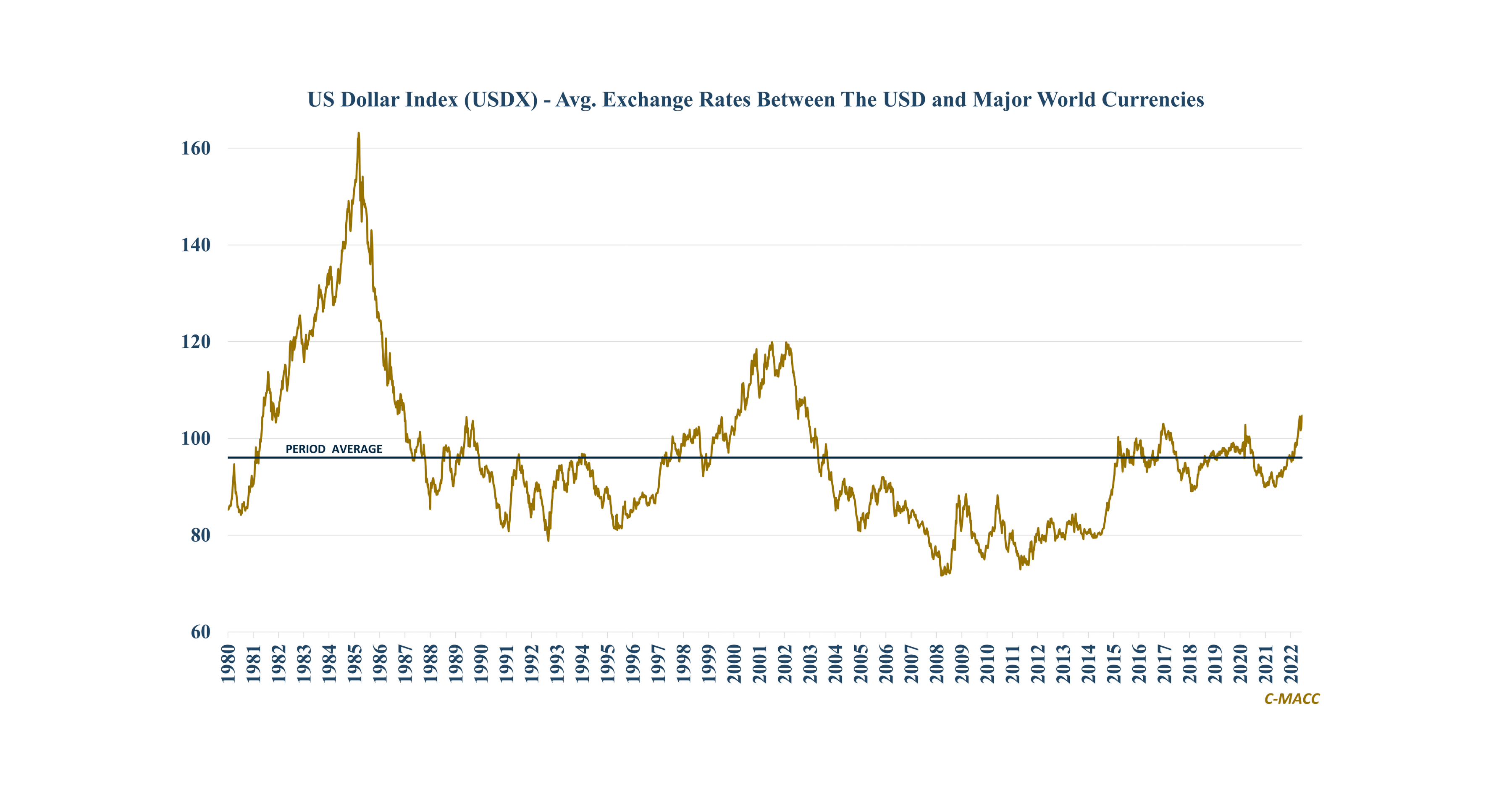

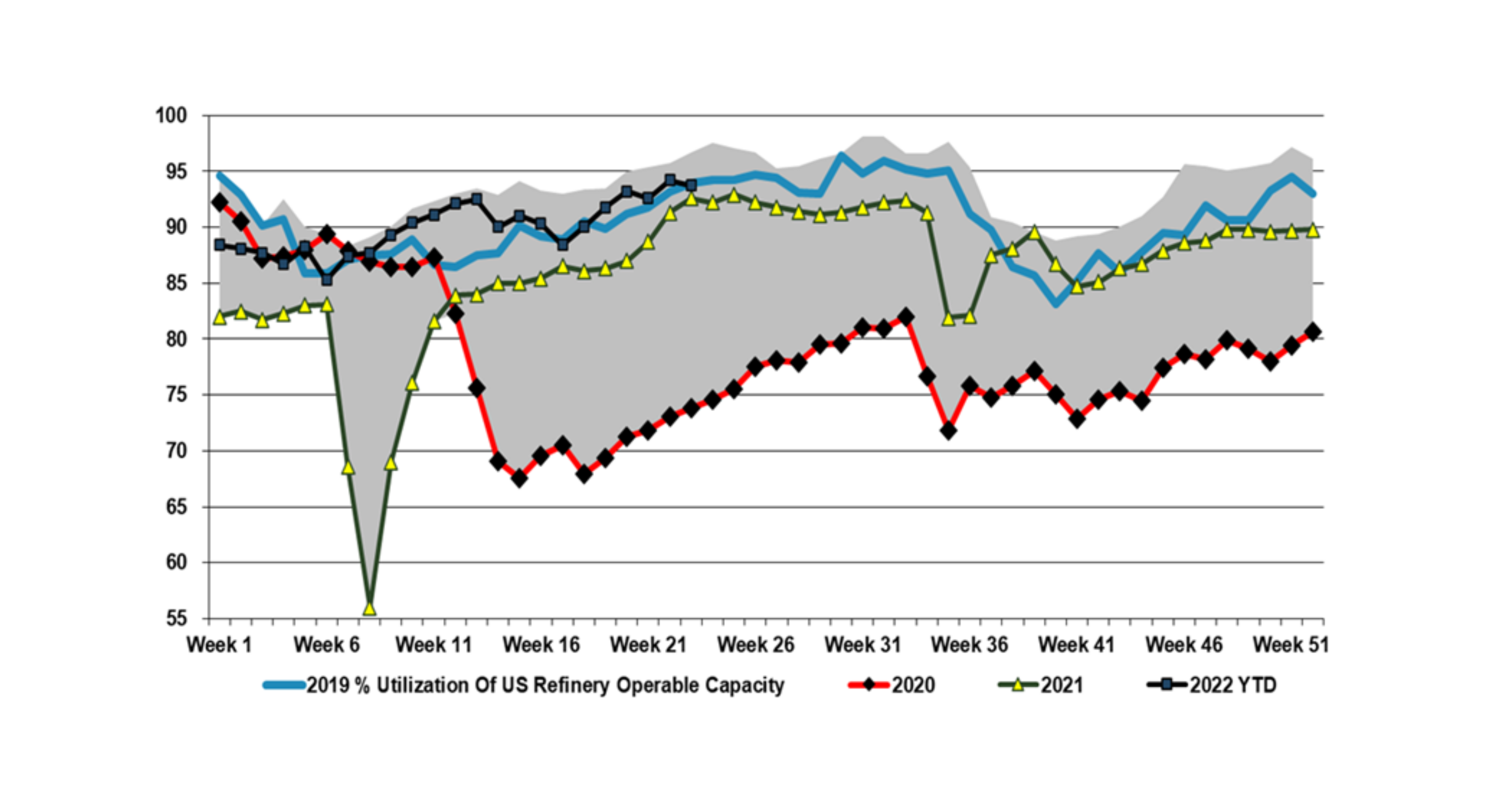

US chemical production costs surged in 2Q22 relative to Ex-US levels. US polymer price weakness, amid more supply, and an unlikely quick global cost curve

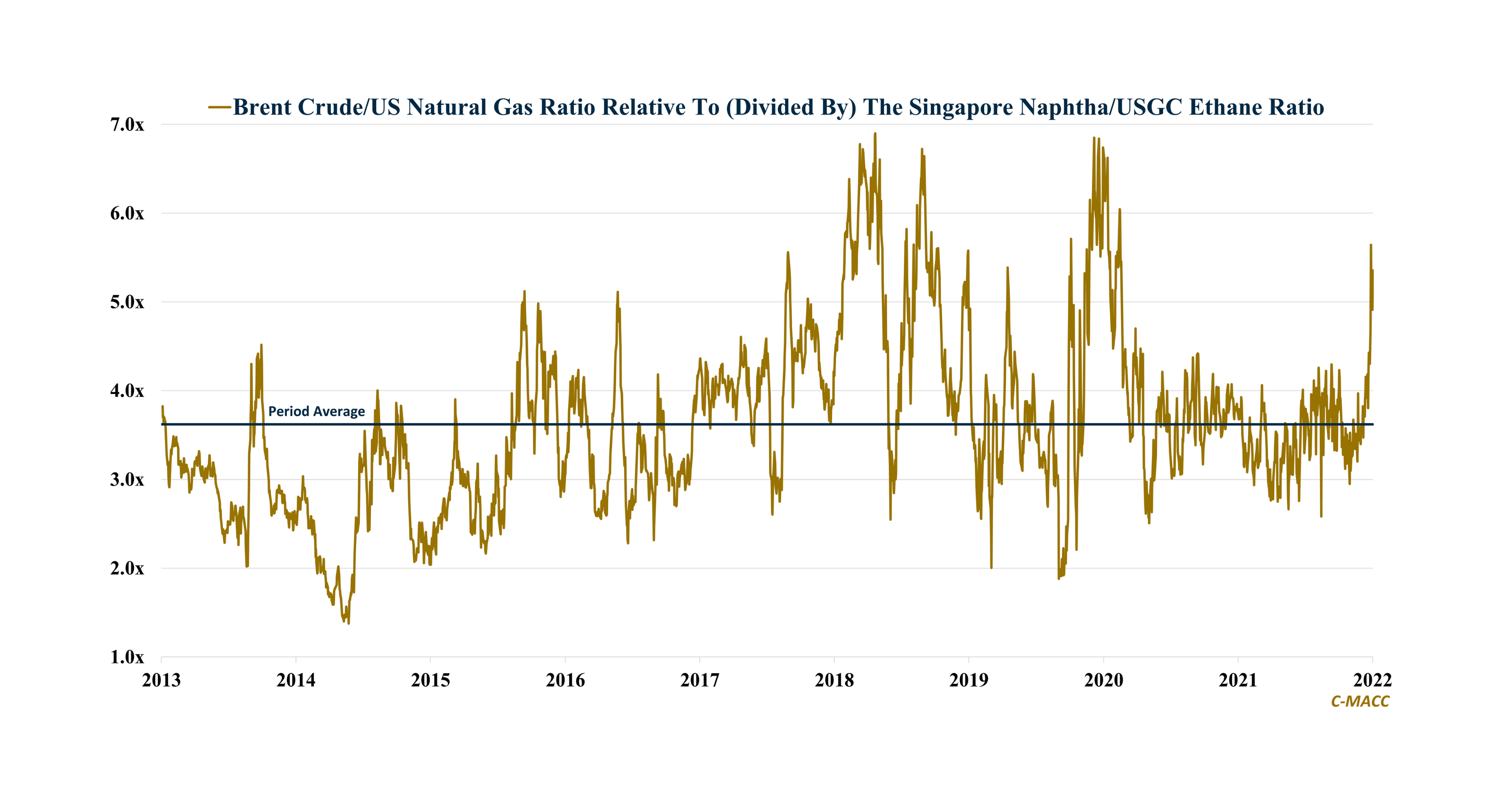

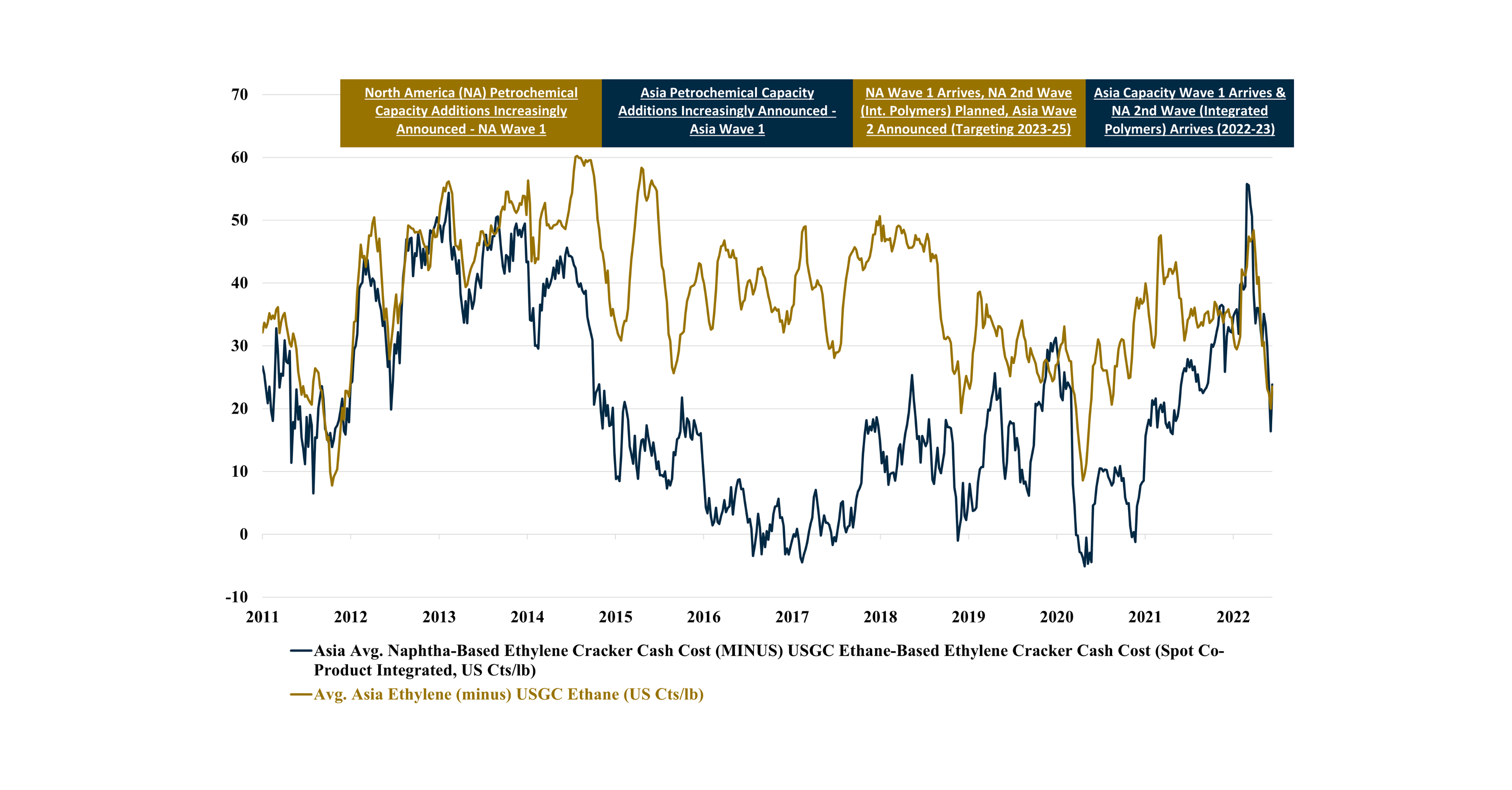

We discuss the increased rumblings of new North American commodity chemical capacity evaluations looking beyond recent sector profit headwinds and the high risk surrounding 2H22

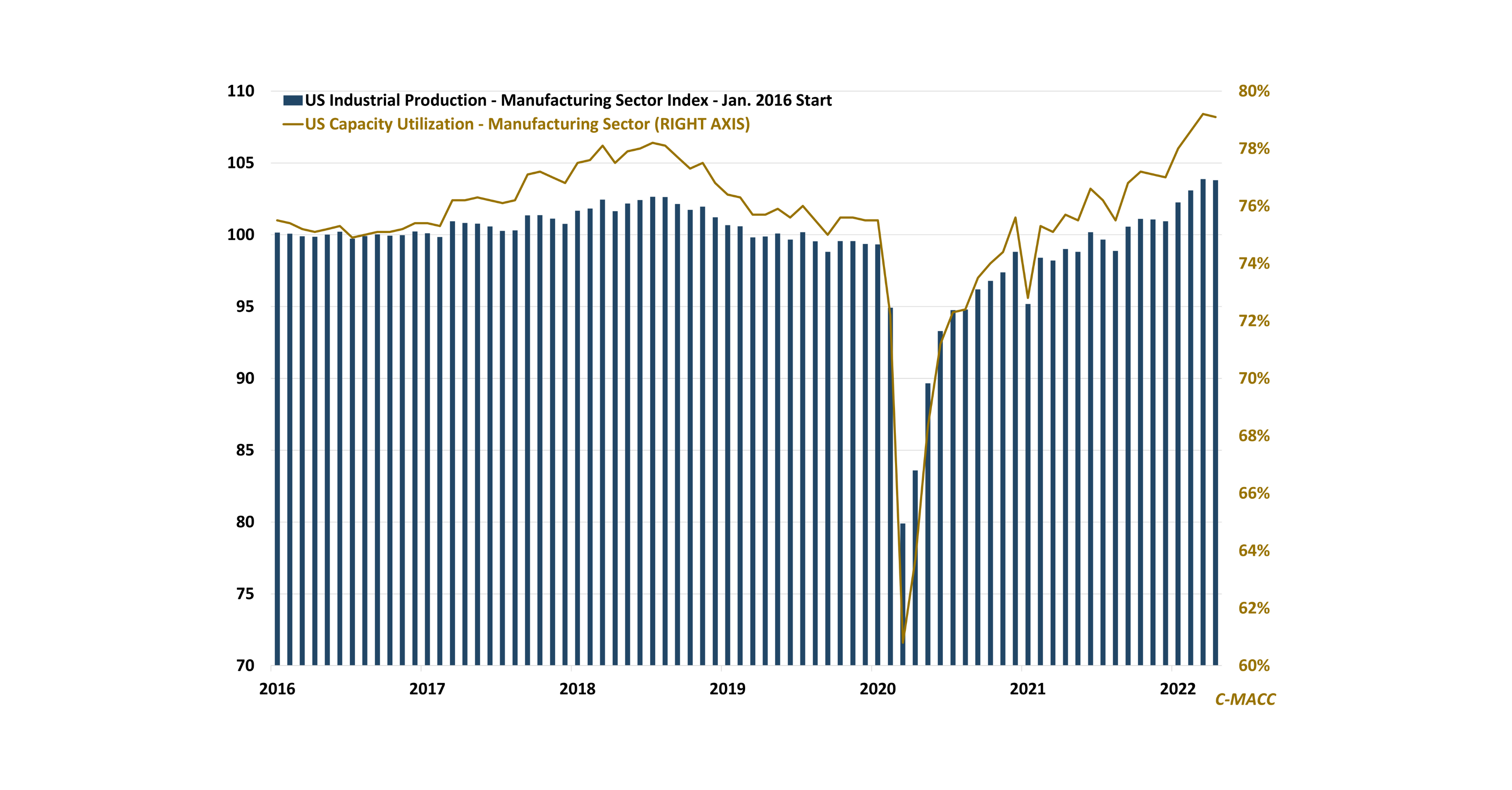

U.S. industrial production growth slowed in May due to a decline in manufacturer output, supporting our near-term chemical sector concerns amid mounting evidence that domestic

Government pressure on the traditional energy sector to boost production contradicts many of its long-term initiatives to push consumers away from these products. We flag

10 days in the UK resulted in many interesting conversations around, inflation, energy security/transition, jobs, lingering Brexit issues, Boris, Biden, and Putin.

Some of

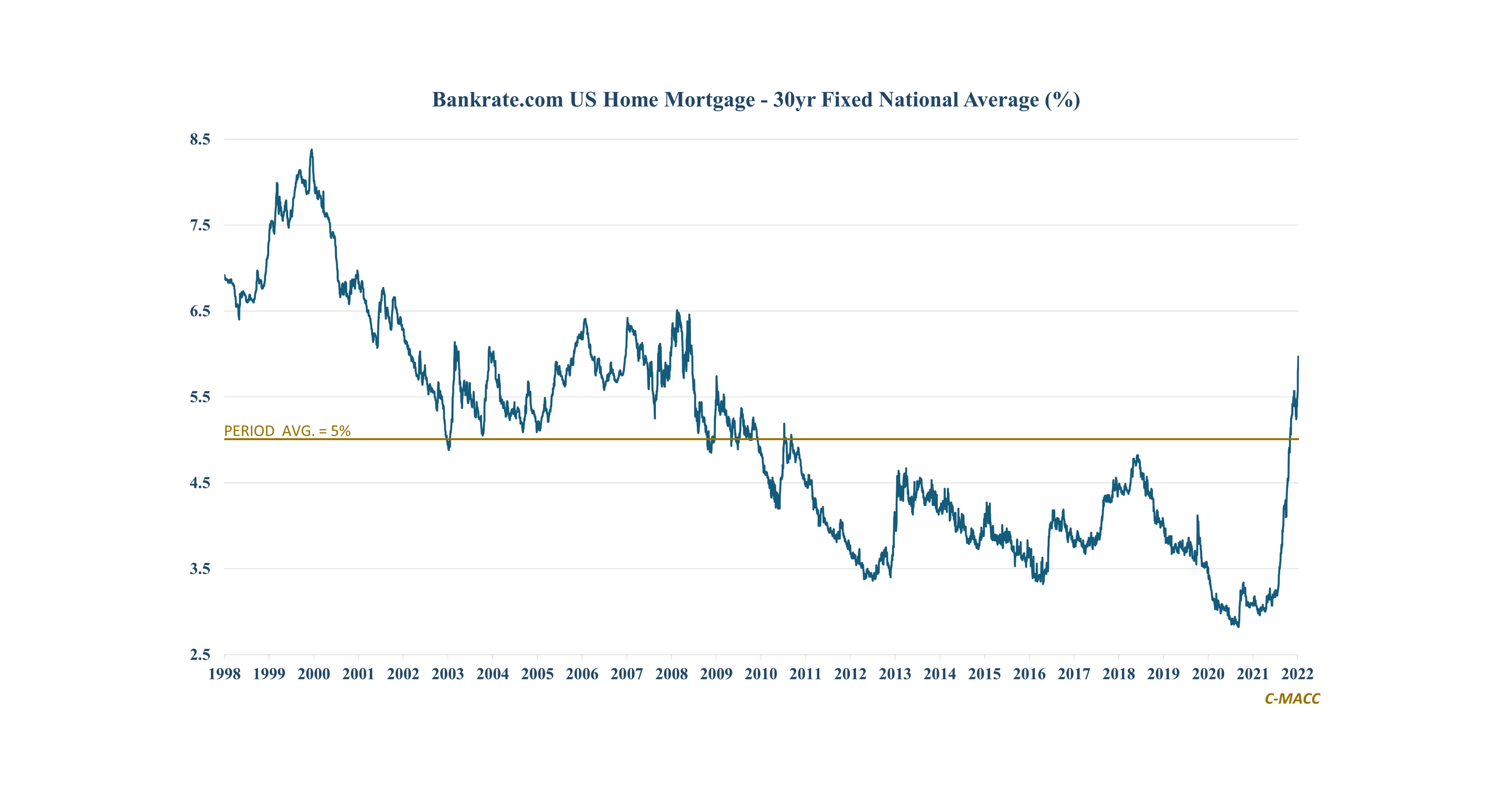

Our view of building & construction product markets is generally cautious for 2H22, as recent demand indicators have broadly turned negative. We flag the major

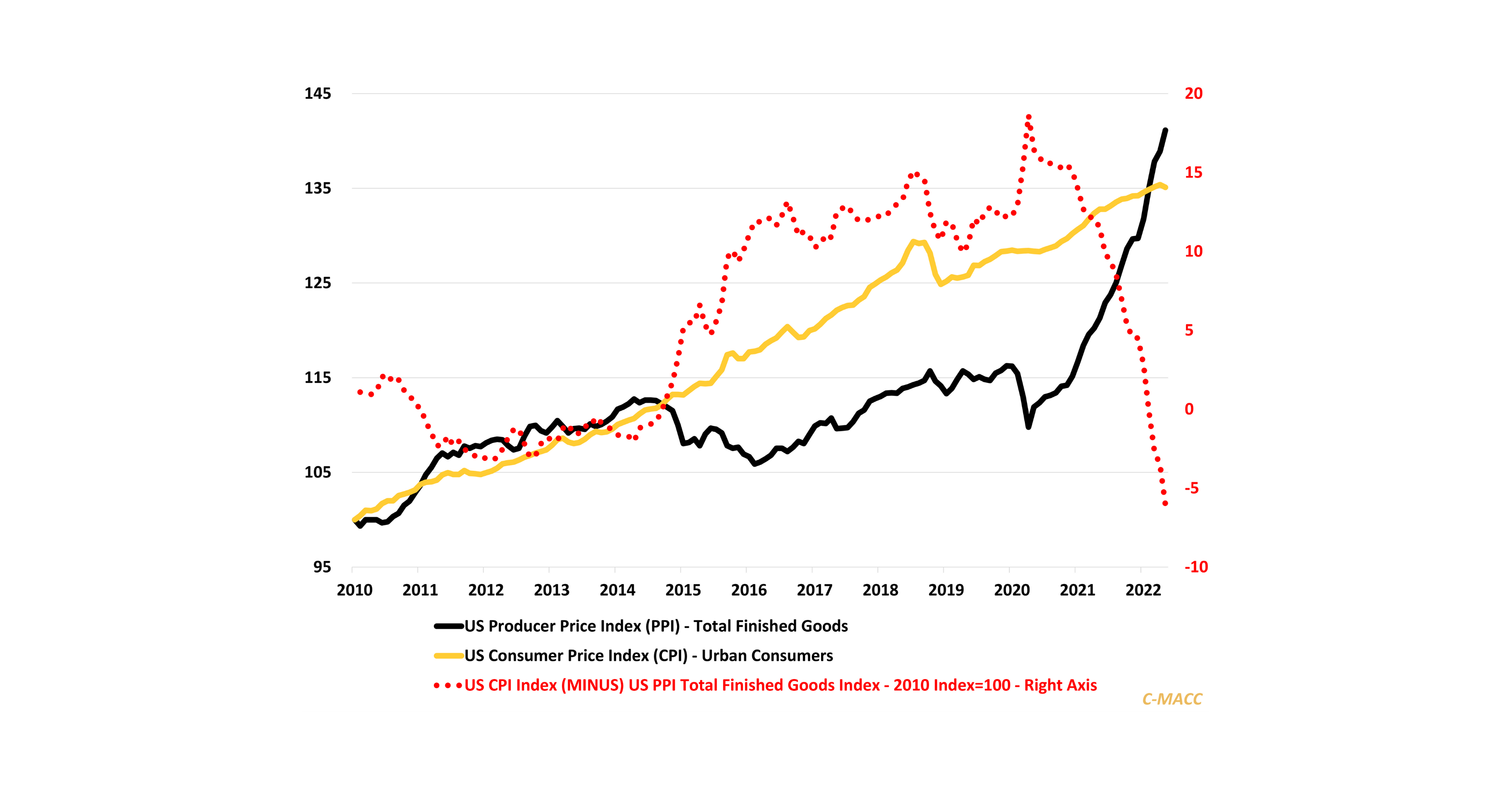

Producer prices have grown more than consumer prices YTD, suggesting end-product price hikes or margin contraction lie ahead of many product chains. We remain concerned