Base Chemical Global Analysis

The global commodity chemical sector faces considerable margin headwinds into year-end as feedstock costs rise, while we view lower volume as the primary factor poised

The global commodity chemical sector faces considerable margin headwinds into year-end as feedstock costs rise, while we view lower volume as the primary factor poised

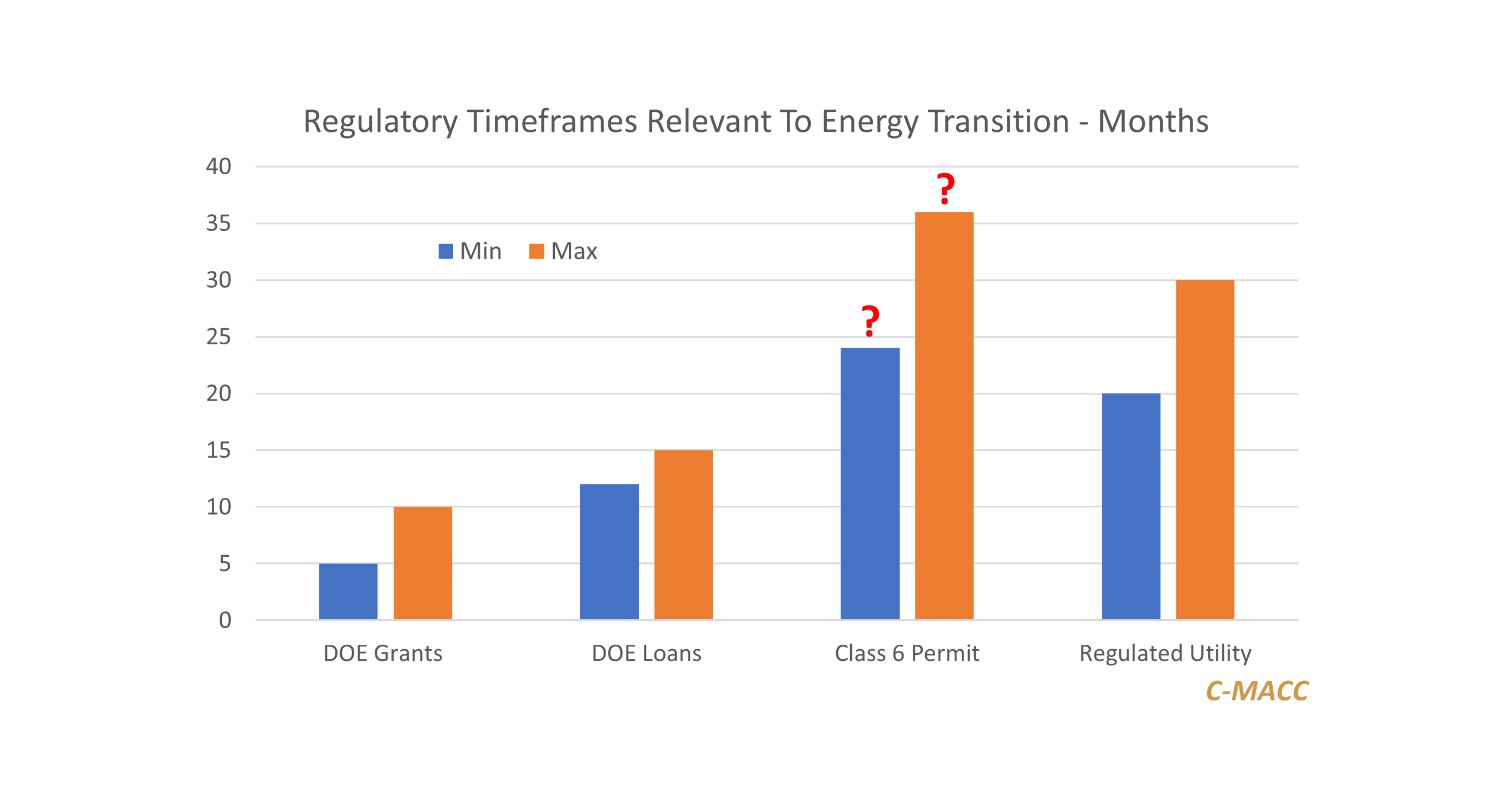

Much-needed experience curves in critical energy transition technologies will be negatively impacted by regulatory delays in the US, leading to missed targets.

Large-scale projects

We discuss the continued push among specialty chemical producers to recapture margins and more global announcements of strategic repositioning among producers.

We highlight much

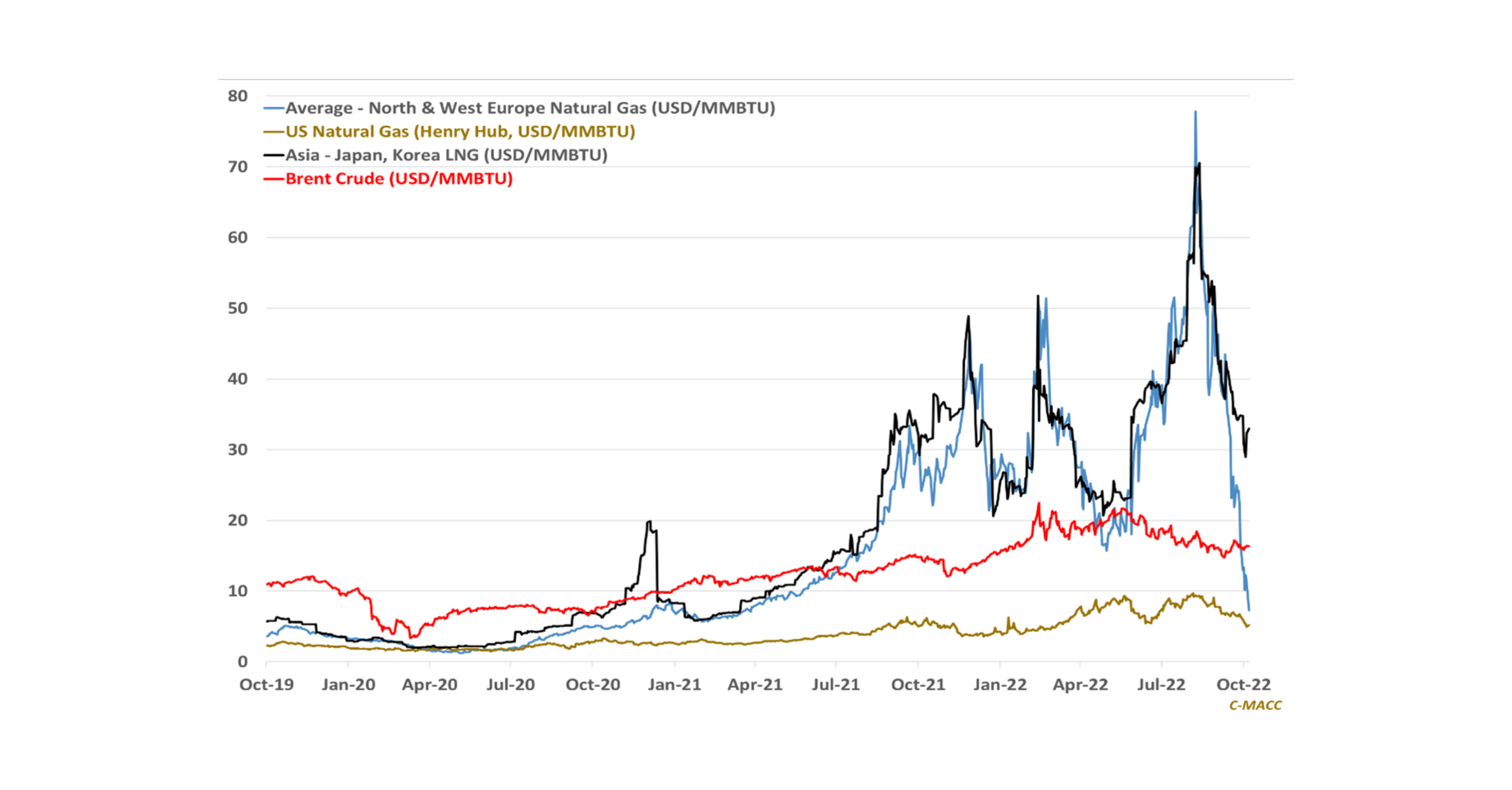

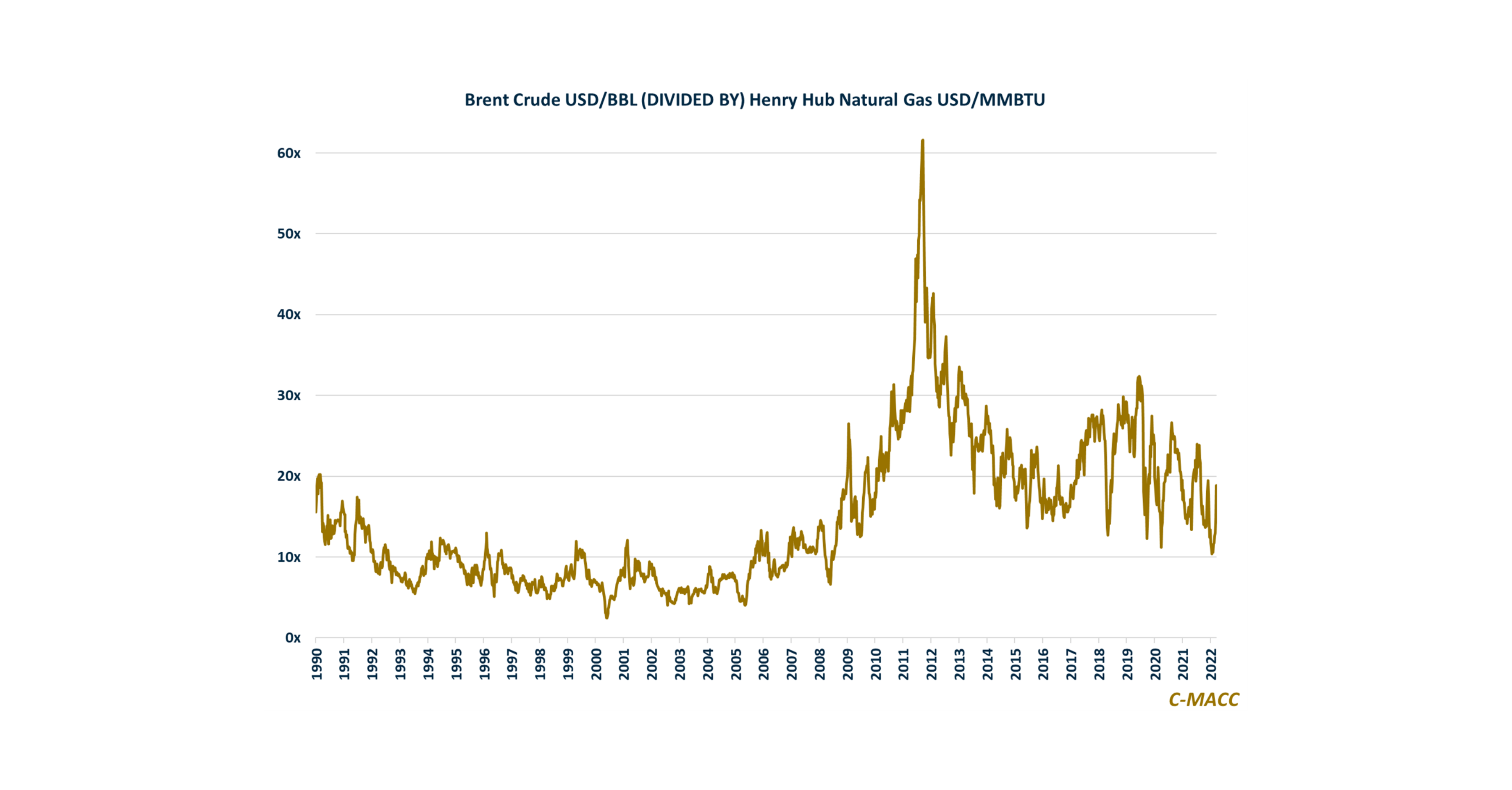

The recent pullback in global energy costs relative to YTD highs favors greater global chemical capacity to produce in markets already facing an oversupplied situation.<br

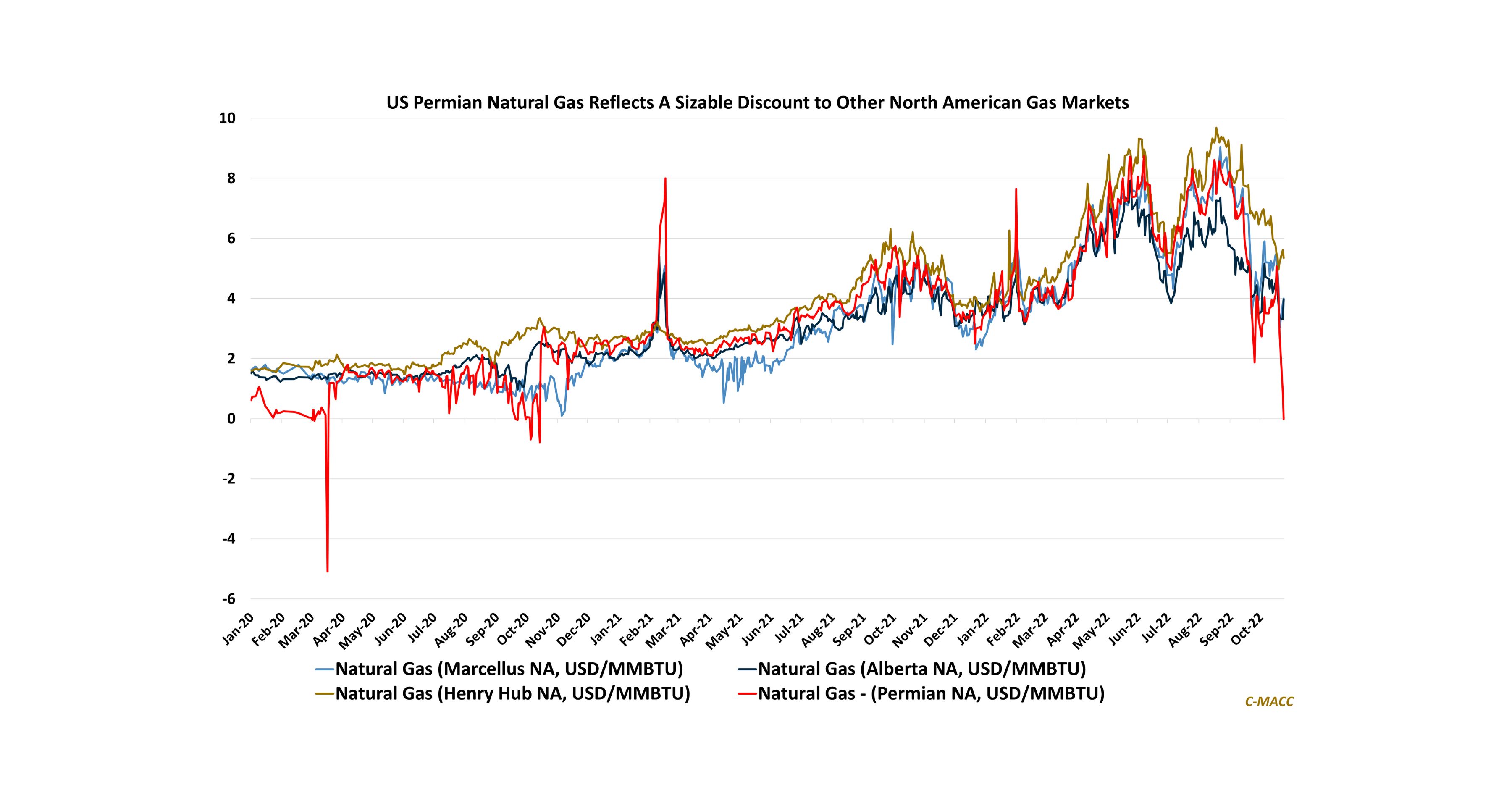

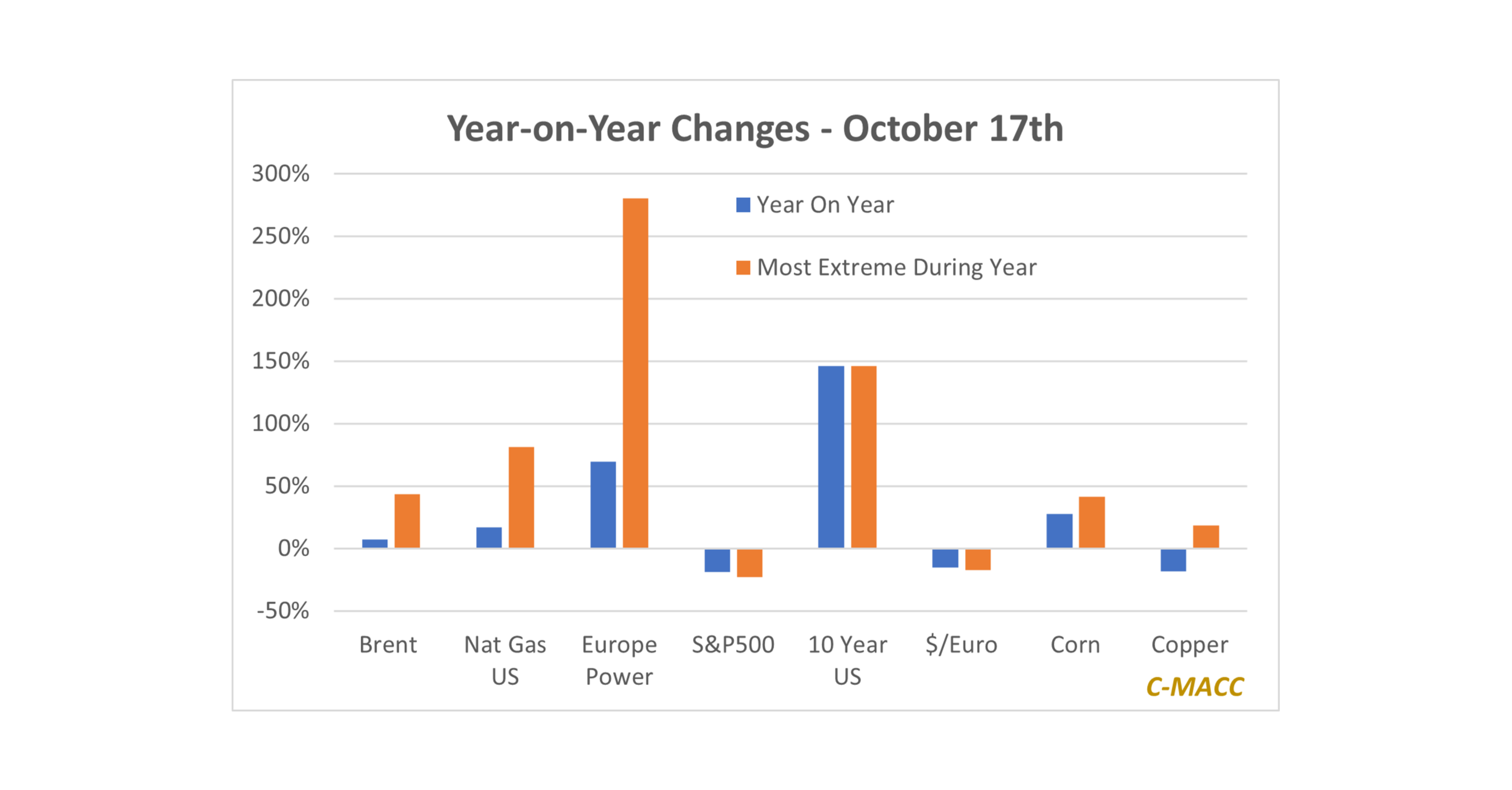

US chemical producers benefit from feedstock relief WoW, which has so far been the positive story of 4Q22. A cost rebound into year-end could push

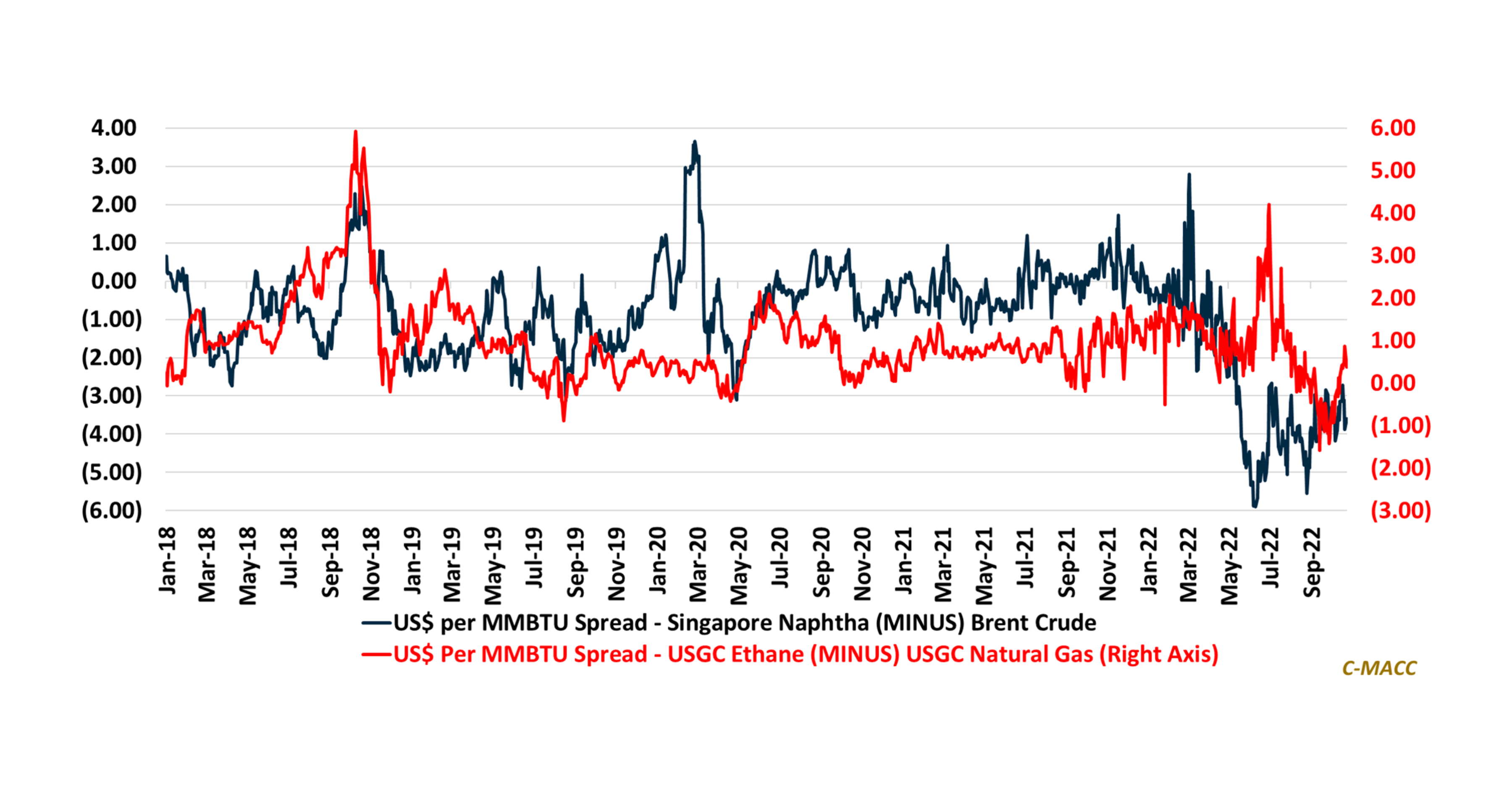

Western chemical markets, on average, have experienced cost relief relative to Asia during the first month of 4Q, but we do not think this trend

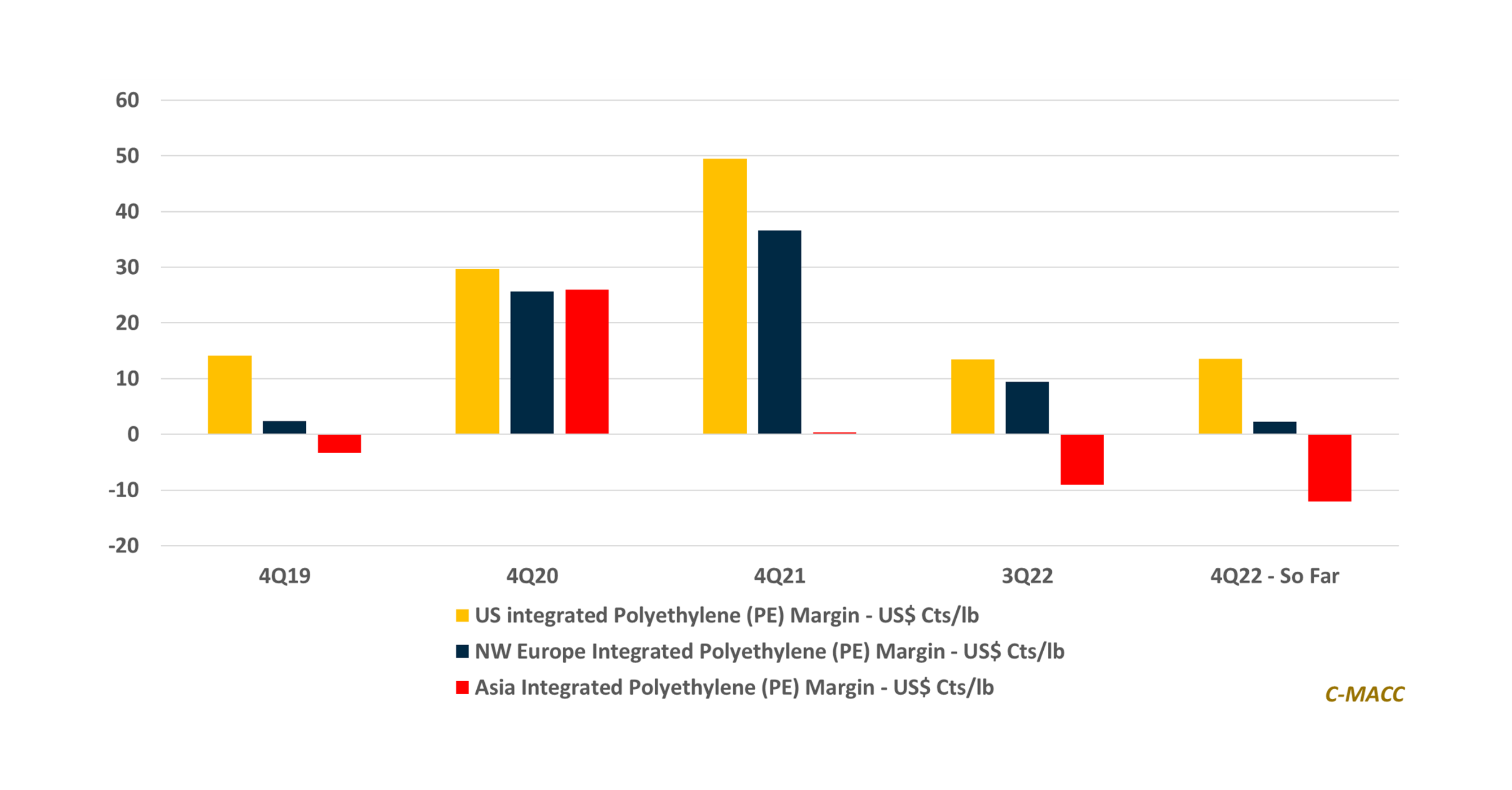

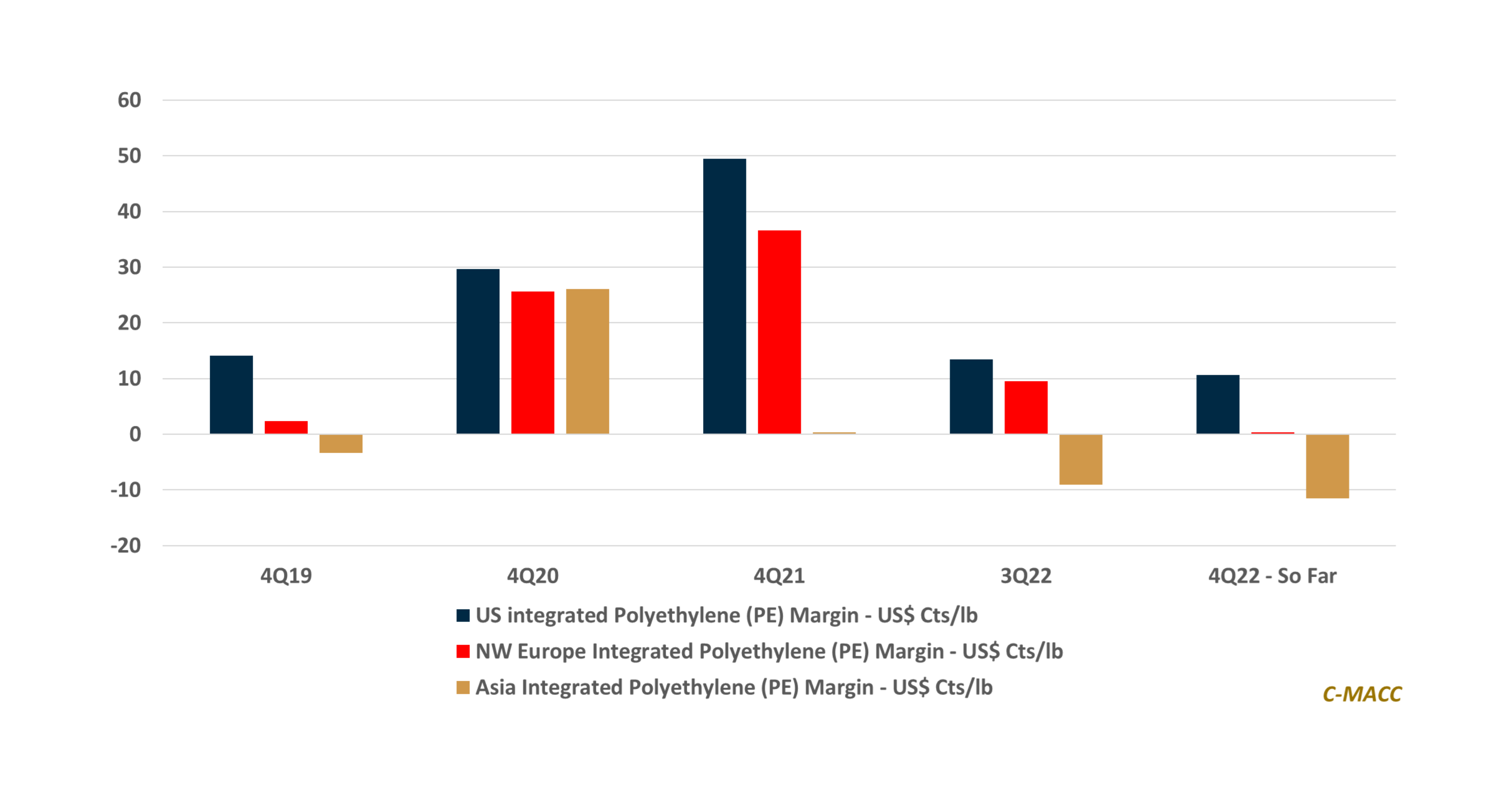

The start of 4Q22 reflects commodity chemical profit levels below the 3Q average but higher than the 3Q lows in most products – it may

COP27 could look very different from COP26, with much less broad agreement and more countries fighting their own corner much harder than last year.

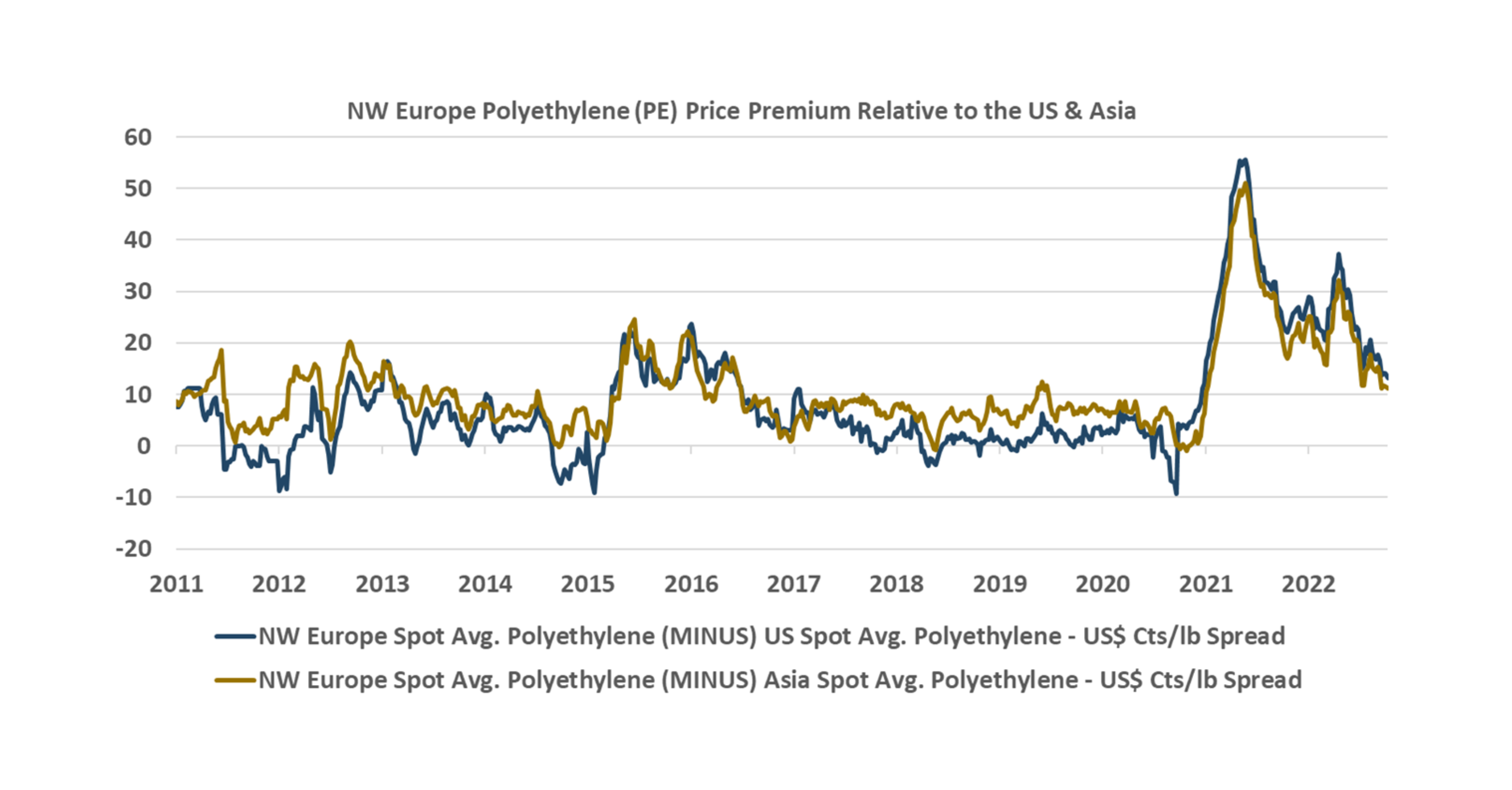

The global polymer market is showing signs of moving toward a more normal balance as regional disconnects lessen, but the upcoming winter reflects significant risk.<br

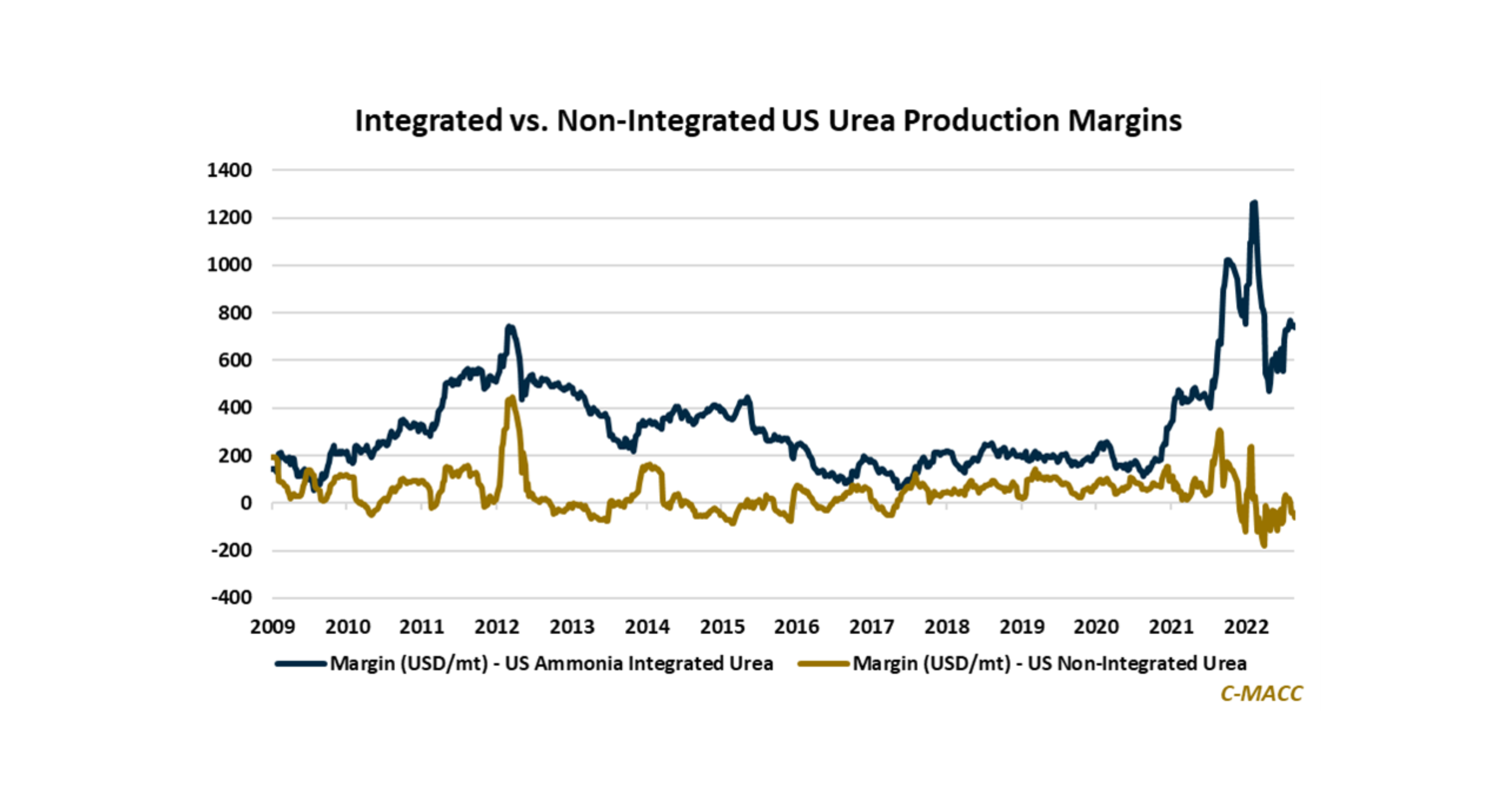

US ammonia prices held up WoW, while natural gas prices fell, spurring WoW strength in domestic margins. The global cost curve favors integrated US fertilizer