Global Market Analysis

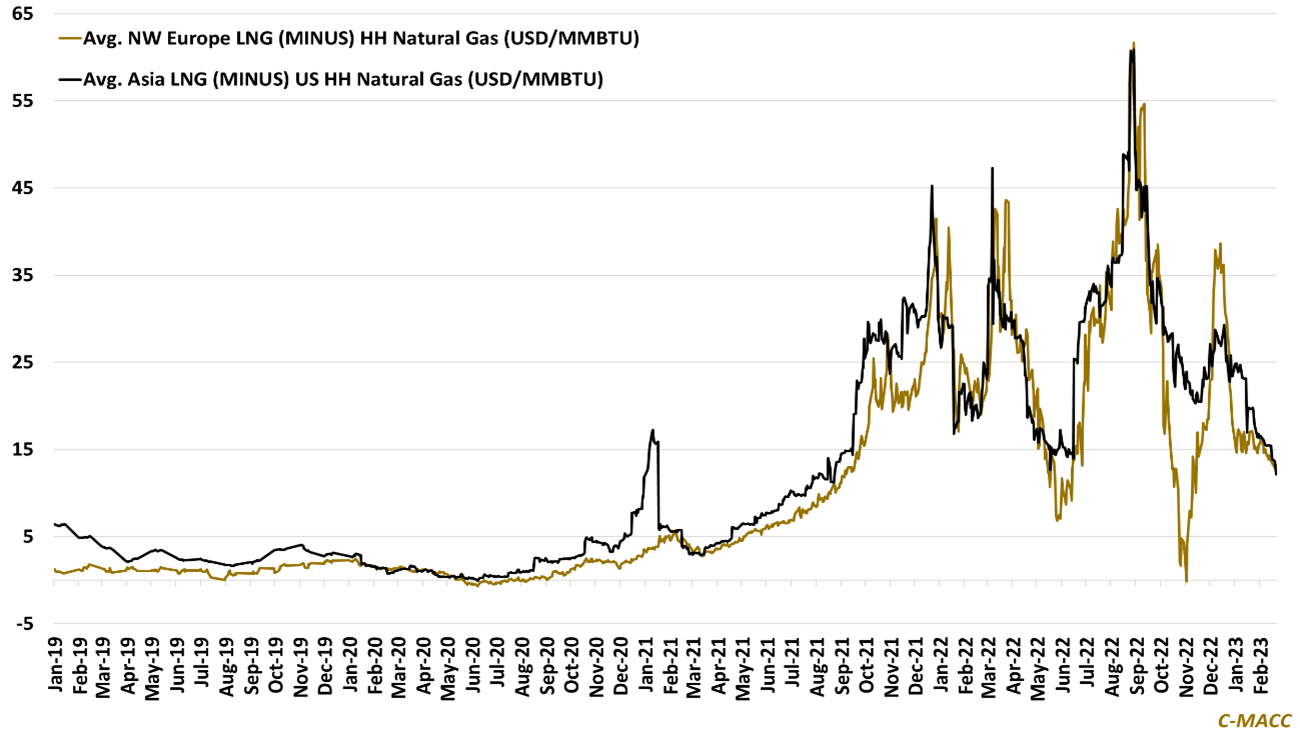

The North American chemical producer cost advantage remains significant relative to overseas peers, as is the case for domestic energy producers, suggesting sizable integration benefits.

The North American chemical producer cost advantage remains significant relative to overseas peers, as is the case for domestic energy producers, suggesting sizable integration benefits.

Ammonia leads again, following earning reports from the existing producers and more speculation around who will enter the market – our expectations are high.

Current