Sunday Executive Summary

Being low cost widens producer margins, but customer resistance can reduce utilization, realized volume, and total earnings even when the underlying cost advantage remains intact

Being low cost widens producer margins, but customer resistance can reduce utilization, realized volume, and total earnings even when the underlying cost advantage remains intact

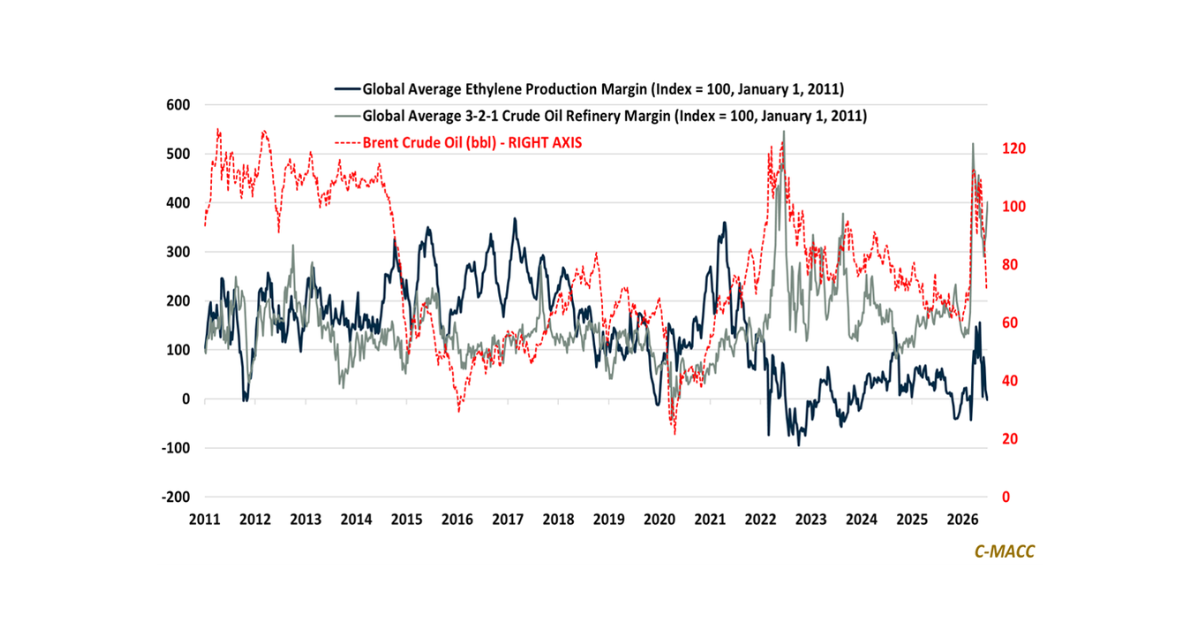

Global refining margins still outperform ethylene because tight fuel supply supports plant rates, although renewed Middle East tension has interrupted the latest decline in chemical

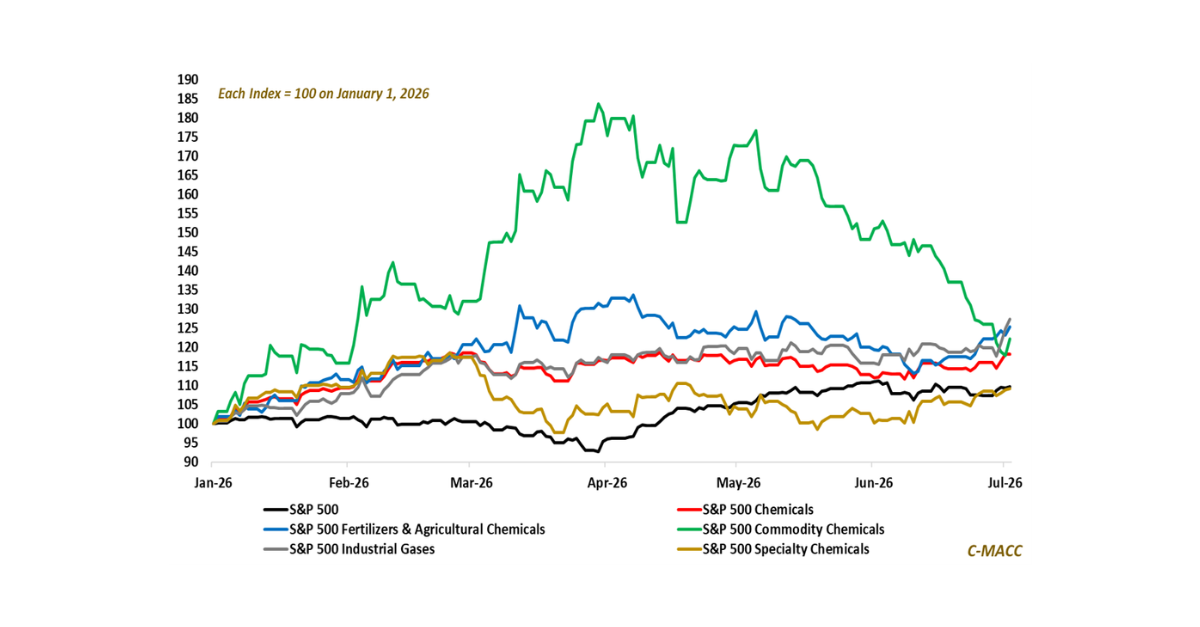

Chemical equities are turning defensive again, but the split is sharper as commodity and specialty sentiment weakens while fertilizers and industrial gases retain support.

Consensus

1H26 saw margins shift twice: conflict pricing rewarded reliable low-cost sellers in 1Q26, while falling oil-linked inputs gave buyers stronger leverage in 2Q value-chain negotiations

Route control sets the margin gate as low-cost supply realizes less value when access owners or customers govern timing, price, outlet choice, and demand commitment

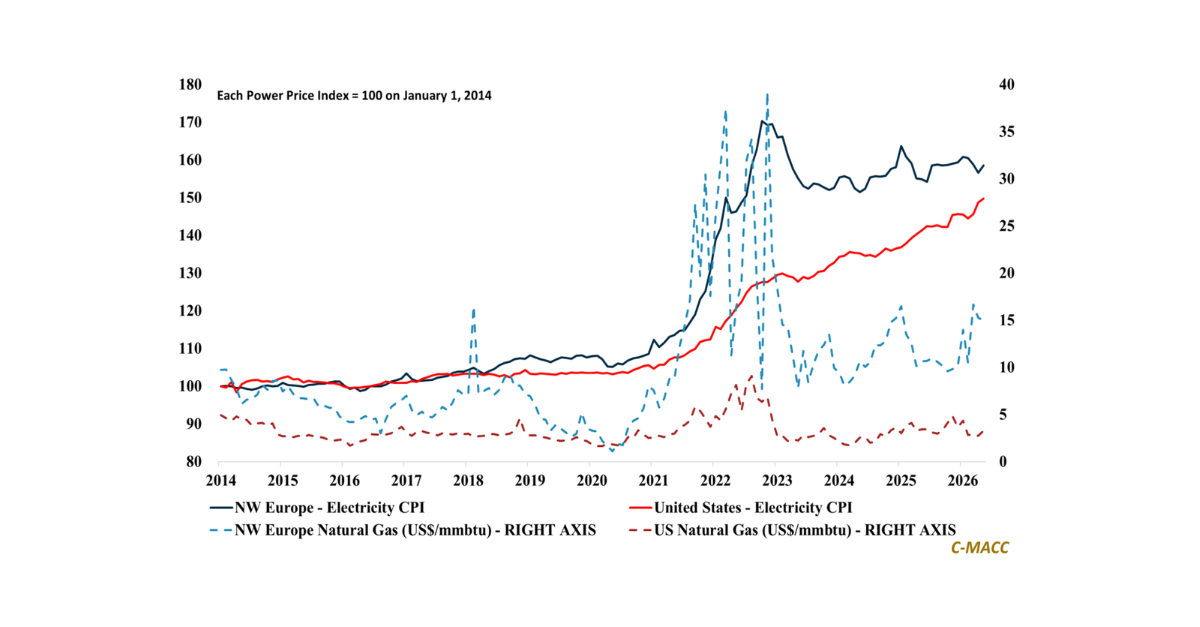

Regional and local electricity price inflation has become a signal of global competitiveness, as sticky power prices push buyers toward lower-cost supply options, while some

Chemical and polymer prices have retreated from peak 1H26 levels, but many remain above January levels, leaving buyers to judge whether relief is temporary or

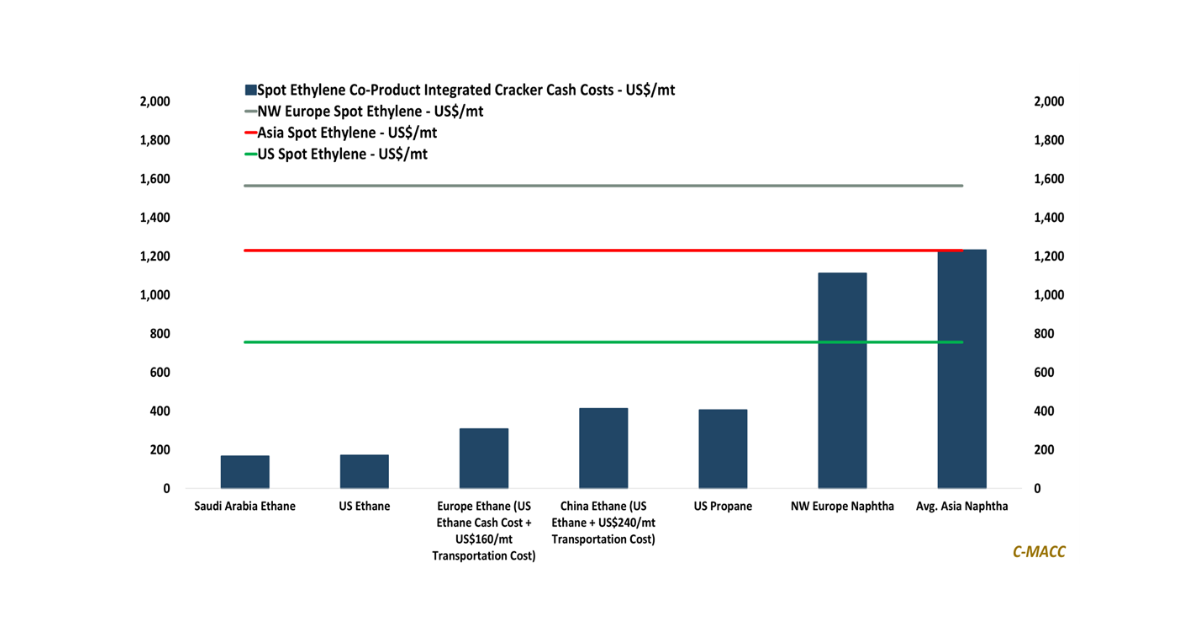

Asia’s olefins cost-recovery squeeze is forcing ex-China asset reviews, as naphtha-based production costs exceed those in Europe and Chinese exports limit derivative price recovery.

Europe’s

Apparent manufacturing stability masks shrinking usable capacity as liquidity, logistics, affordability, and operating reliability outrank installed production capability across industrial systems.

Industrial survival increasingly depends

Industrial competitiveness increasingly reflects access to qualified infrastructure, freight continuity, and grid execution rather than a nominal feedstock advantage or headline commodity pricing alone.

Europe’s