C-MACC Sunday Executive Summary

The Shortage Is Real, But the Signal Risks Being Misread

- Contract pricing is emerging as the governing signal in constrained markets, embedding access, timing, and supply assurance, while spot pricing reflects residual, uncommitted liquidity pools.

- Inventory drawdowns are delaying demand response, shifting market clearing from marginal consumption to depletion rates, shrinking discounts, and forcing realized pricing to converge toward contract structures.

- Upstream producers with secure feedstock and contractual exposure capture pricing earlier, while downstream buyers absorb costs first, creating a persistent timing gap that transfers value upstream.

- High-cost and non-integrated producers face margin compression and restructuring pressure, reinforcing that scarcity rewards system design while exposing those reliant on spot markets and external inputs.

- Additionally, constrained supply, contract dominance, midstream control, and fragmented demand are reordering value capture upstream while downstream margins compress as pricing power is tested.

- Companies Mentioned: ExxonMobil, Chevron, Enterprise Products, LyondellBasell, Methanex, Yara, SABIC, Wacker Chemie, IMCD, Pembina, BP, ADNOC, Shell, Phillips 66, Valero, ONEOK, Mineral Resources, Albemarle, Ganfeng, Rio Tinto, Standard Lithium, Lithium Americas, KBR, Geolith, POSCO, Mangrove Lithium, BASF, Ford

- Products Mentioned: Methanol, LNG, Ethane, Naphtha, LPG, Ammonia, Nitrogen, Sulfur, Phosphate, Urea, Coal, Ngls, Natural Gas, Crude, Diesel, Jet Fuel, VGO, Copper, Aluminum, Lithium, Spodumene

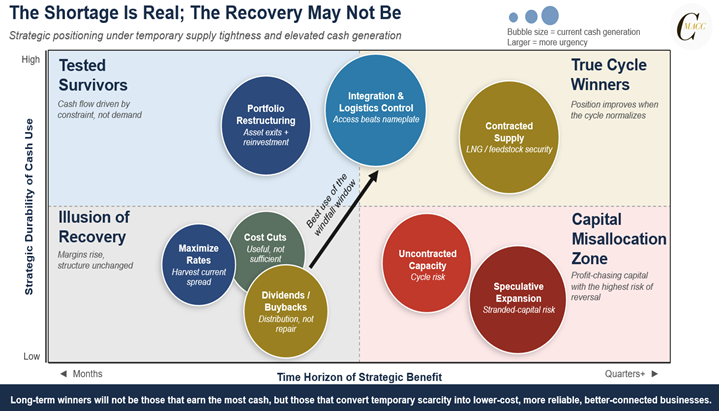

Exhibit 1: Constraint-driven profits reward availability, but structural positioning determines durable advantage.

Source: C-MACC Analysis, April 2026

See PDF below for all charts, tables and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!