Global Market Analysis

General Thoughts: Red Sea freight normalization could compress Western chemical market premiums, including for methanol, exposing cost curves, trade defenses, and discipline as differentiators in

General Thoughts: Red Sea freight normalization could compress Western chemical market premiums, including for methanol, exposing cost curves, trade defenses, and discipline as differentiators in

Volatility has transcended cycle theory to become global industrial gravity, where policy cadence, not demand elasticity, dictates profitability, capital sequencing, and the new tempo of

General Thoughts: The late 2025 commodity landscape rewards integrated, low-cost, logistics-agile producers, while 2026 will test who can sustain profits as new capacity, cost volatility,

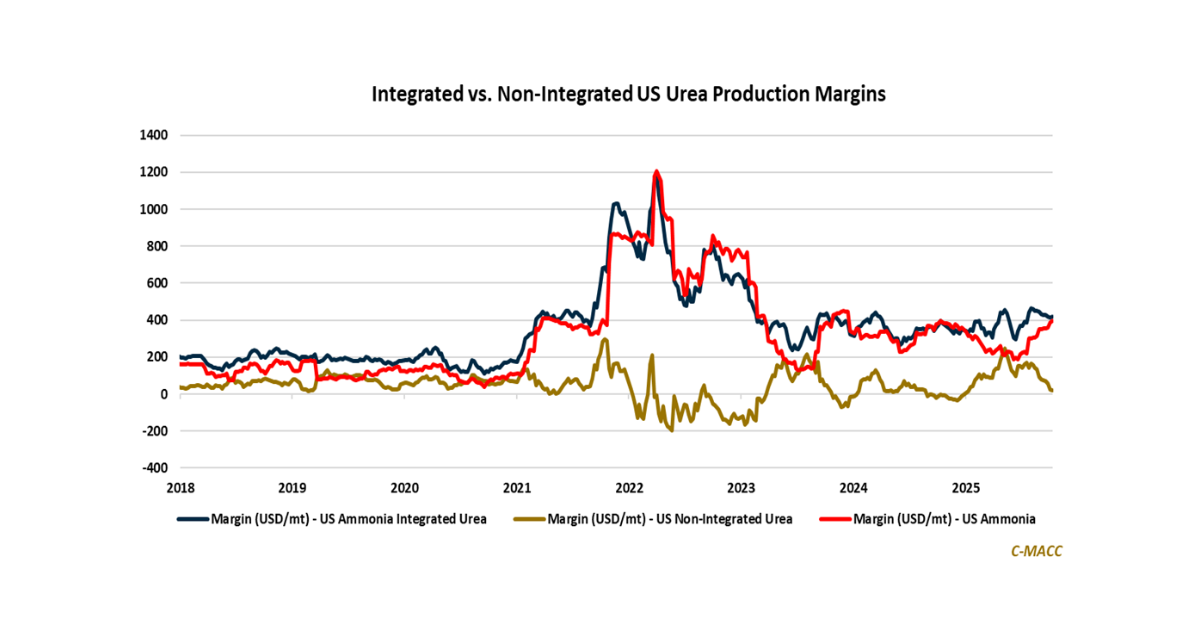

General Thoughts: Crop price strength and rising Ex-US natural gas prices relative to the US since mid-May paints an improved picture of US ammonia producer

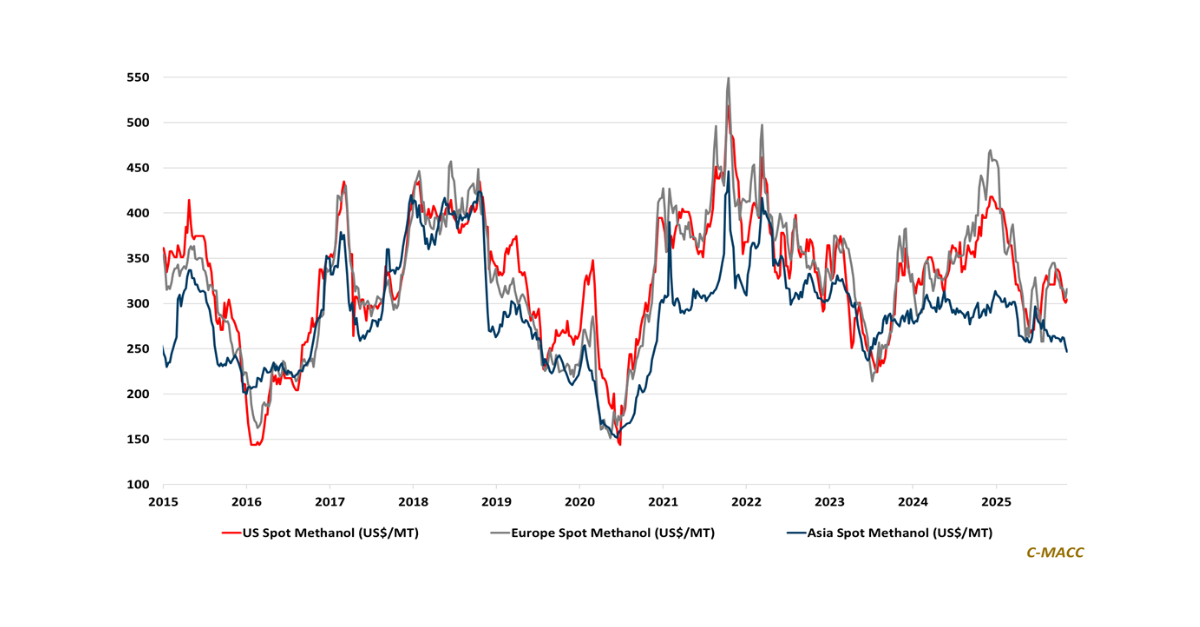

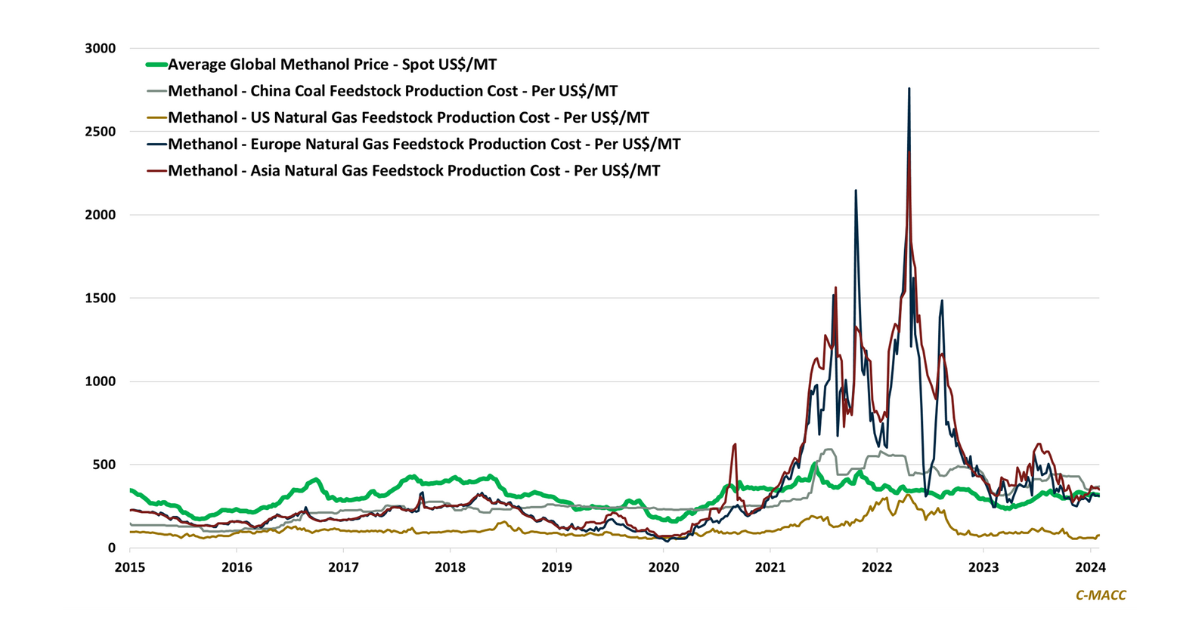

General Thoughts: North American methanol producers hold a substantial production cost advantage relative to Europe and Asia, allowing for greater profitability but also a selective

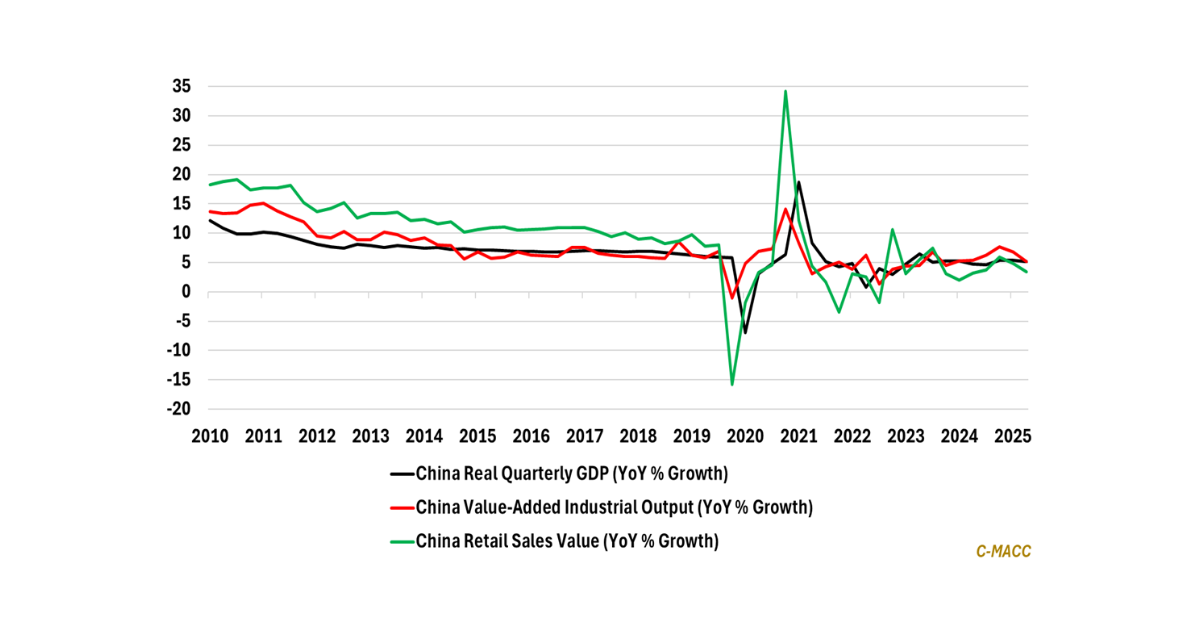

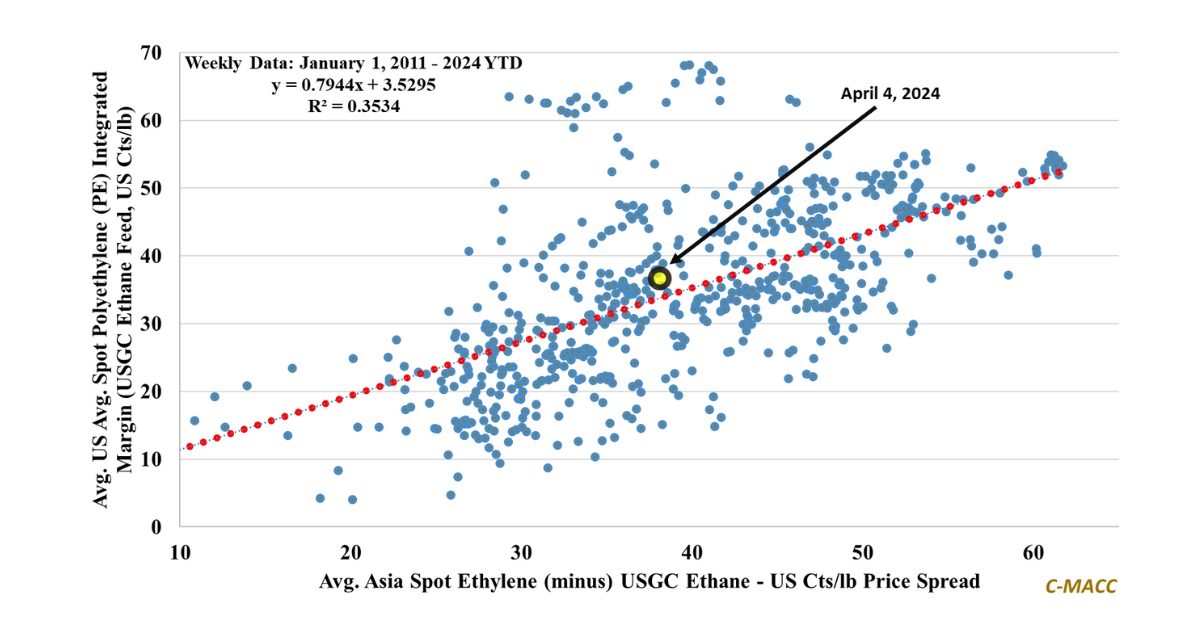

General Thoughts: The economic link between chemical feedstock suppliers and chemical producers has always been significant – recent market developments could work to quicken global

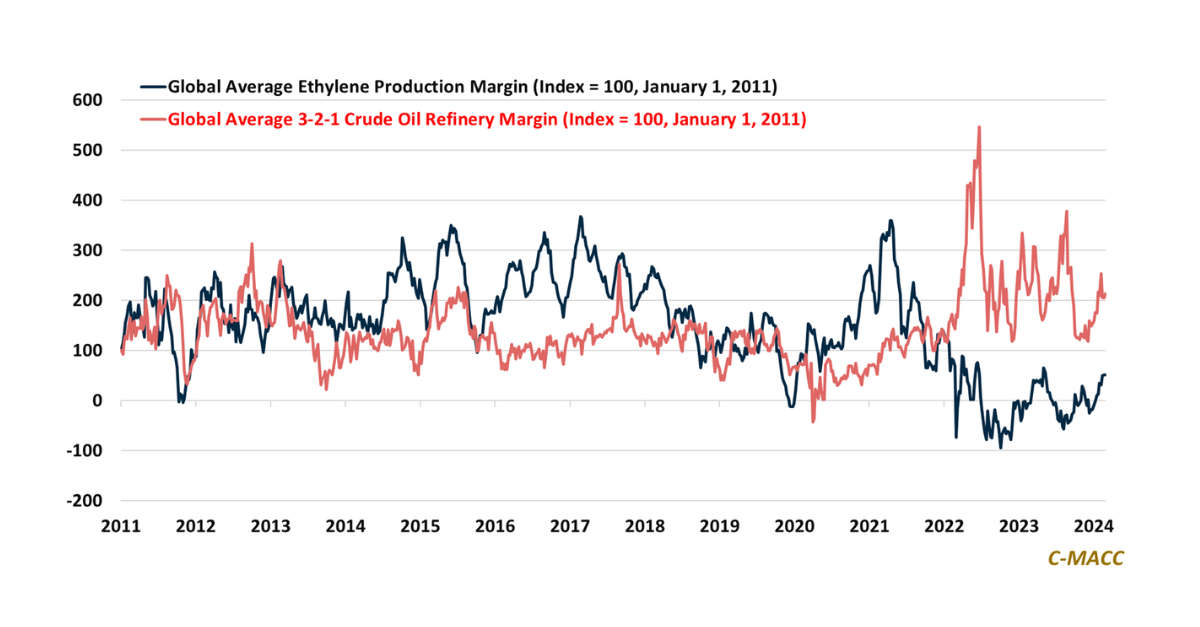

General Thoughts: Western crude oil refinery and integrated ethylene margins have surged YTD relative to Asia amid an array of outages and logistic issues –

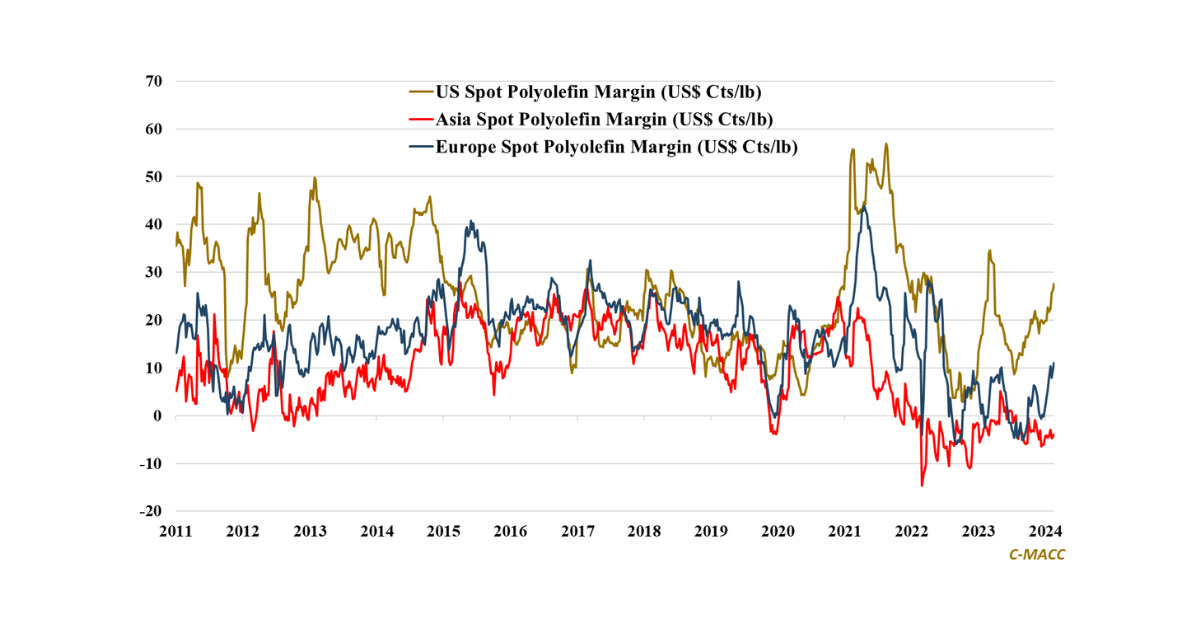

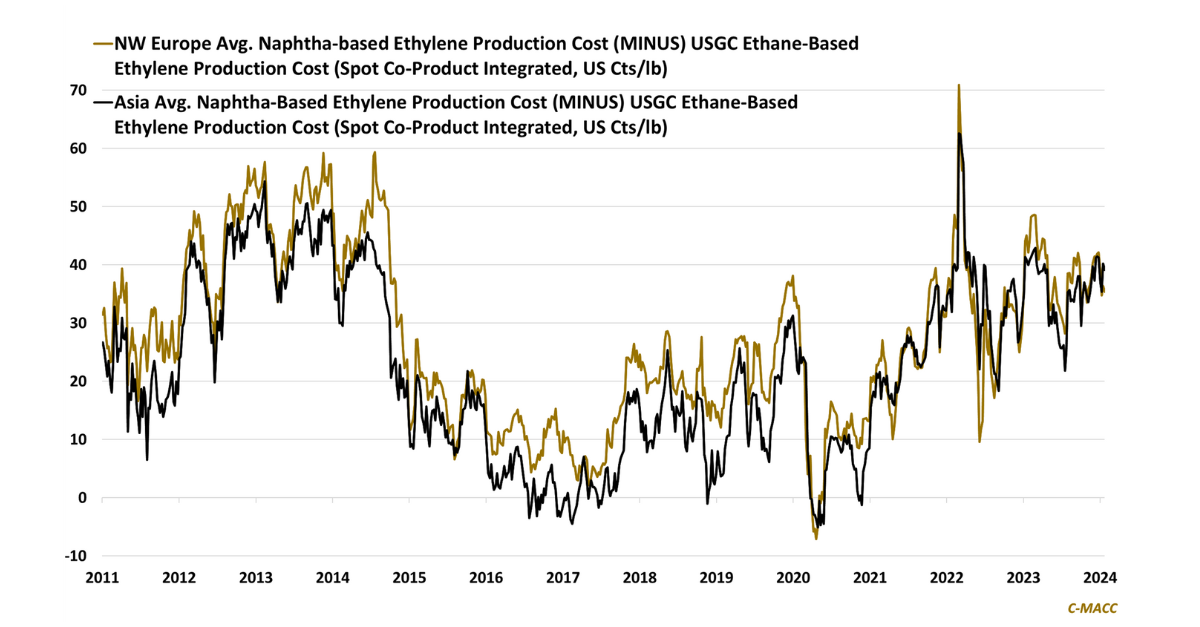

General Thoughts: Western polyolefin price strength following 4Q23 global logistical constraints, supply cuts, and recent cost curve movements are benefiting its producers and, most notably,

General Thoughts: Most chemical producers anticipate a better year in 2024, driven by improving end-demand outside the US, notably in 2H24 – the impact of

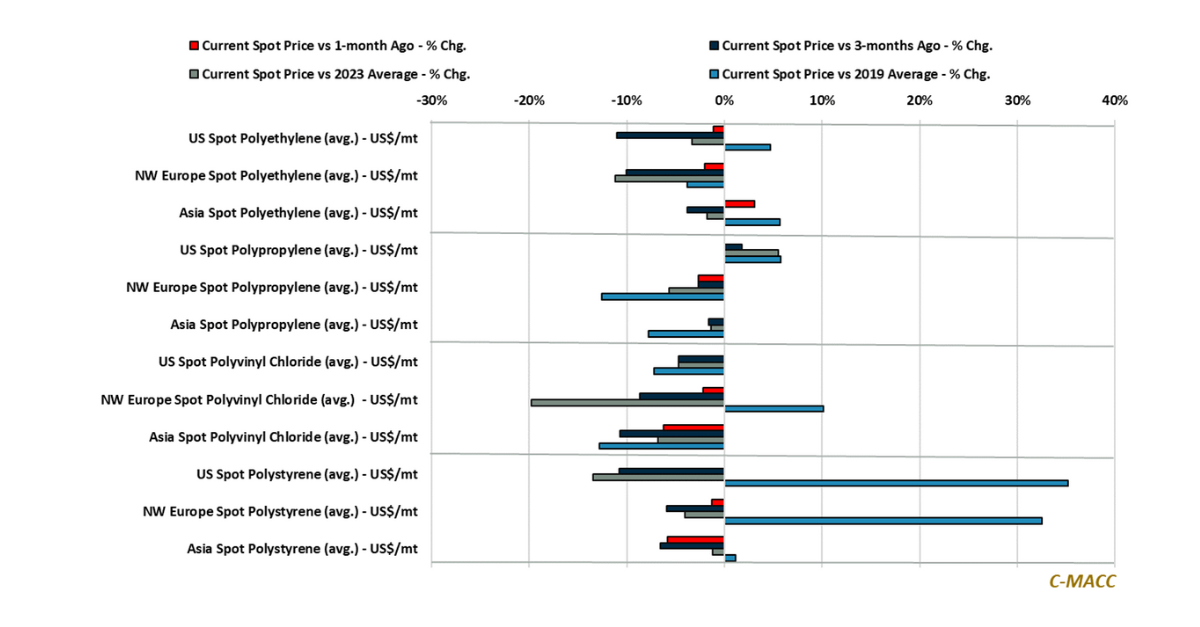

General Thoughts: US polypropylene (PP) spot price support relative to Europe and Asia is due to upstream outages and production cuts – a near-term plus