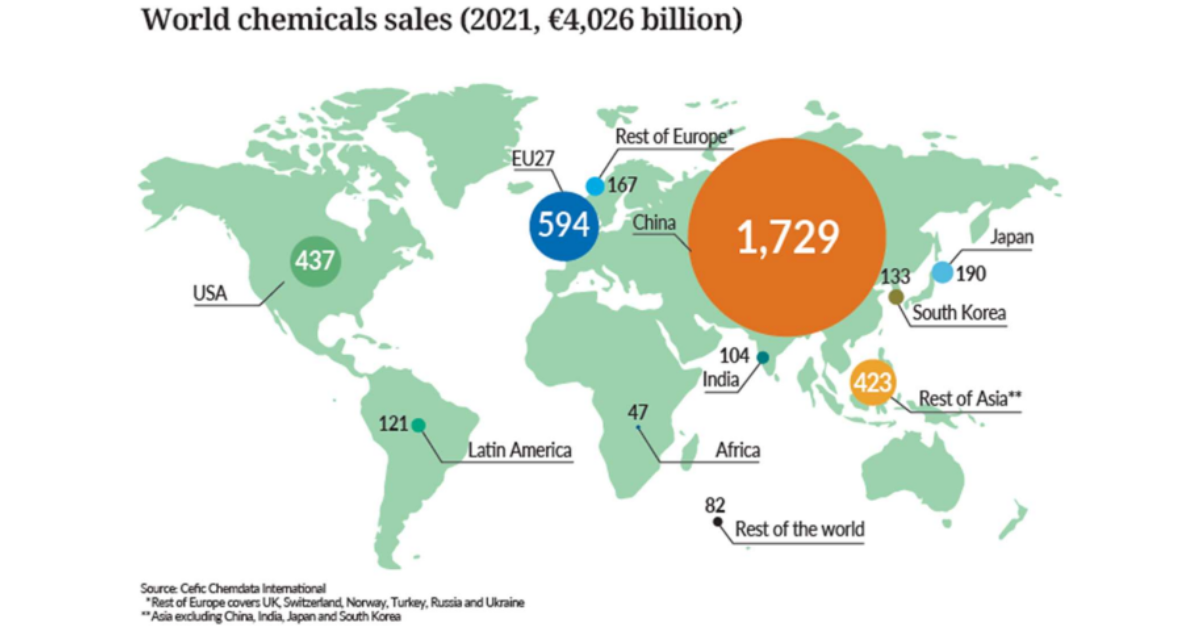

Global Market Analysis

Part of the C-MACC team will attend the PACK EXPO conference next week, and the other part will be at the CMA World Chemical Forum

Part of the C-MACC team will attend the PACK EXPO conference next week, and the other part will be at the CMA World Chemical Forum

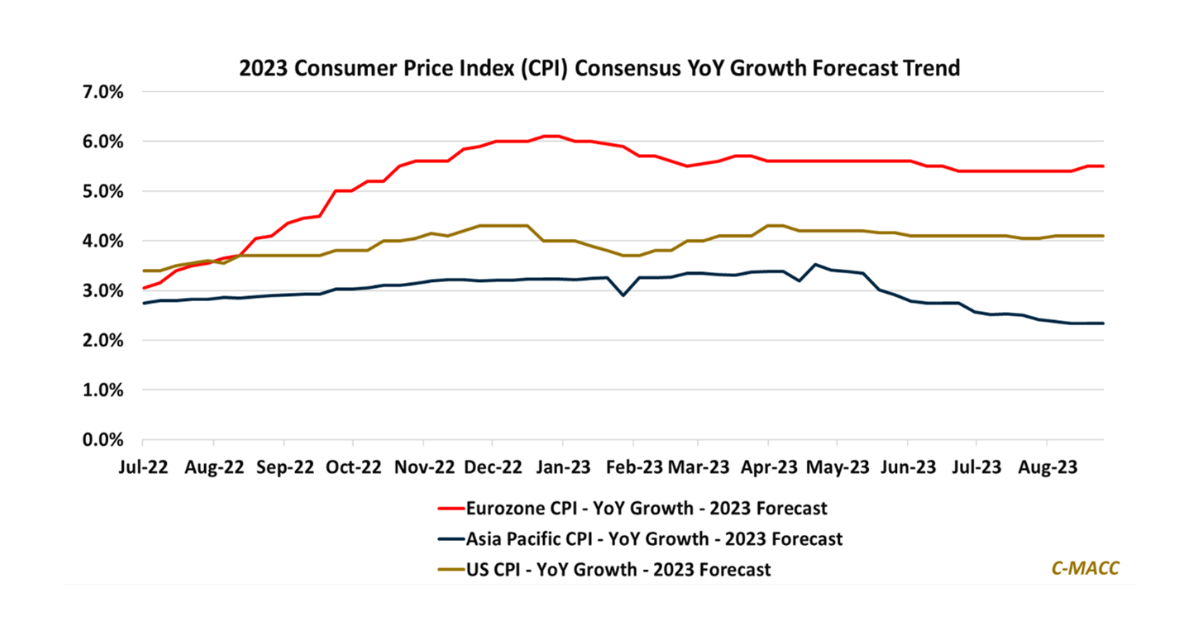

Consumer price expectations for Asia in 2023 have fallen from mid-2023 levels on an absolute basis and relative to the West – a plus for

Global chemical market business conditions have worsened since 2021. We discuss slides from Shell’s 2021 and 2023 strategic updates to show how its view of

US polyethylene (PE) producers are pushing for contract price hikes in August, which we think will further delay a much-needed non-market adjustment based on global

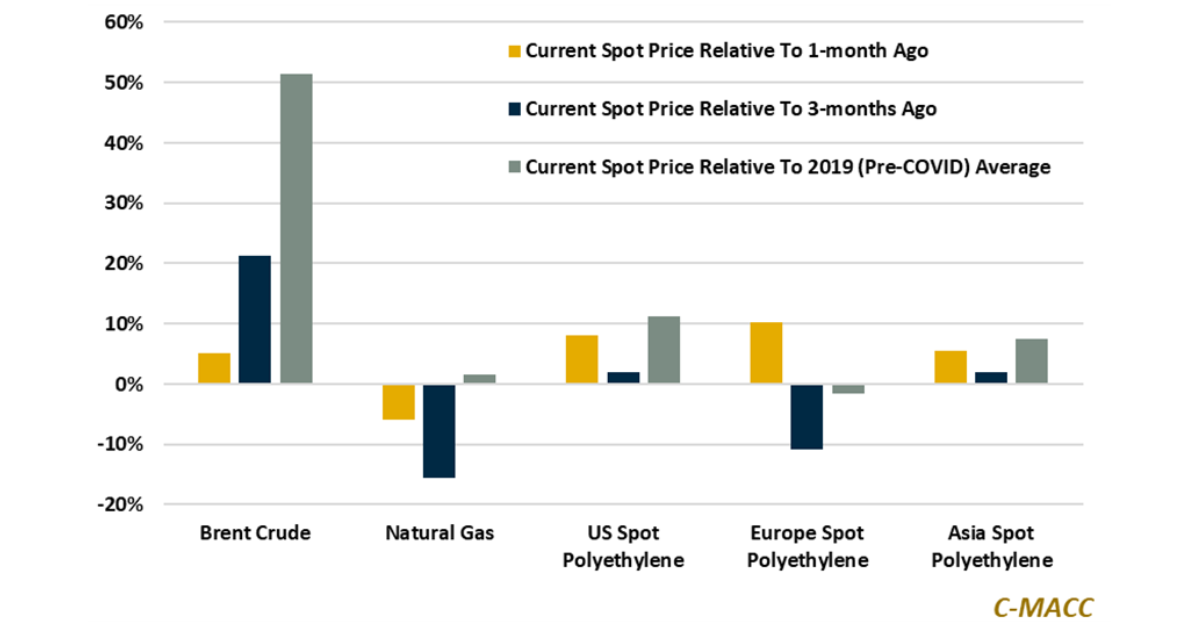

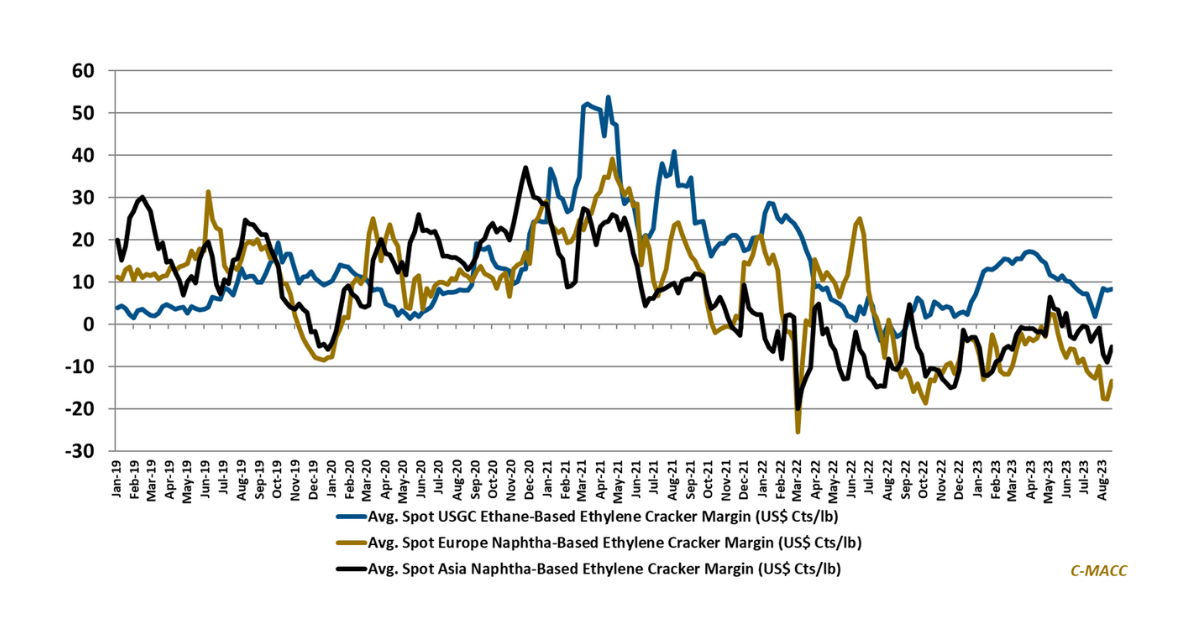

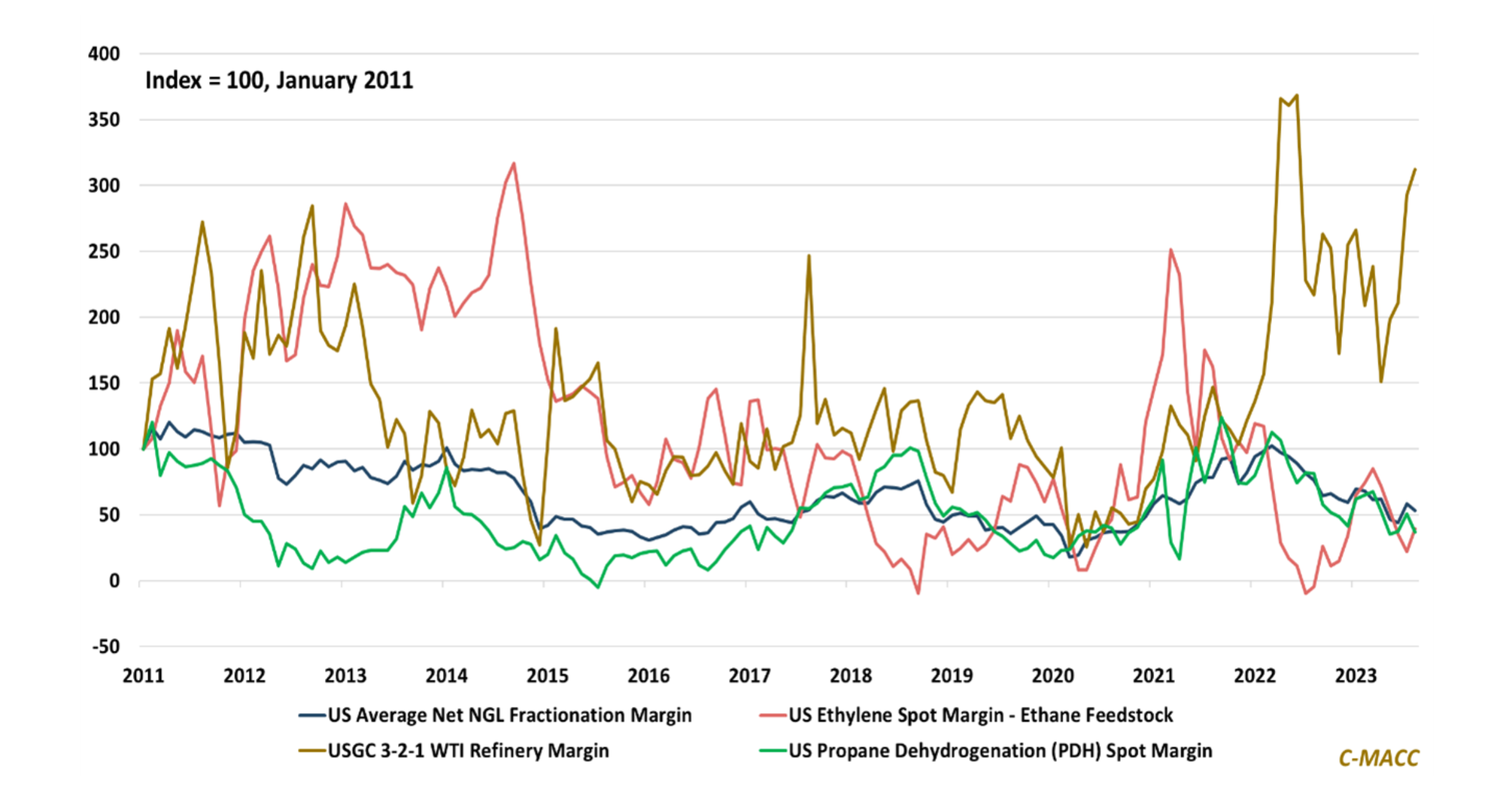

Global chemical prices have rebounded from mid-year lows, partly due to higher crude oil and related feedstocks, displaying the benefit of being a low-cost producer

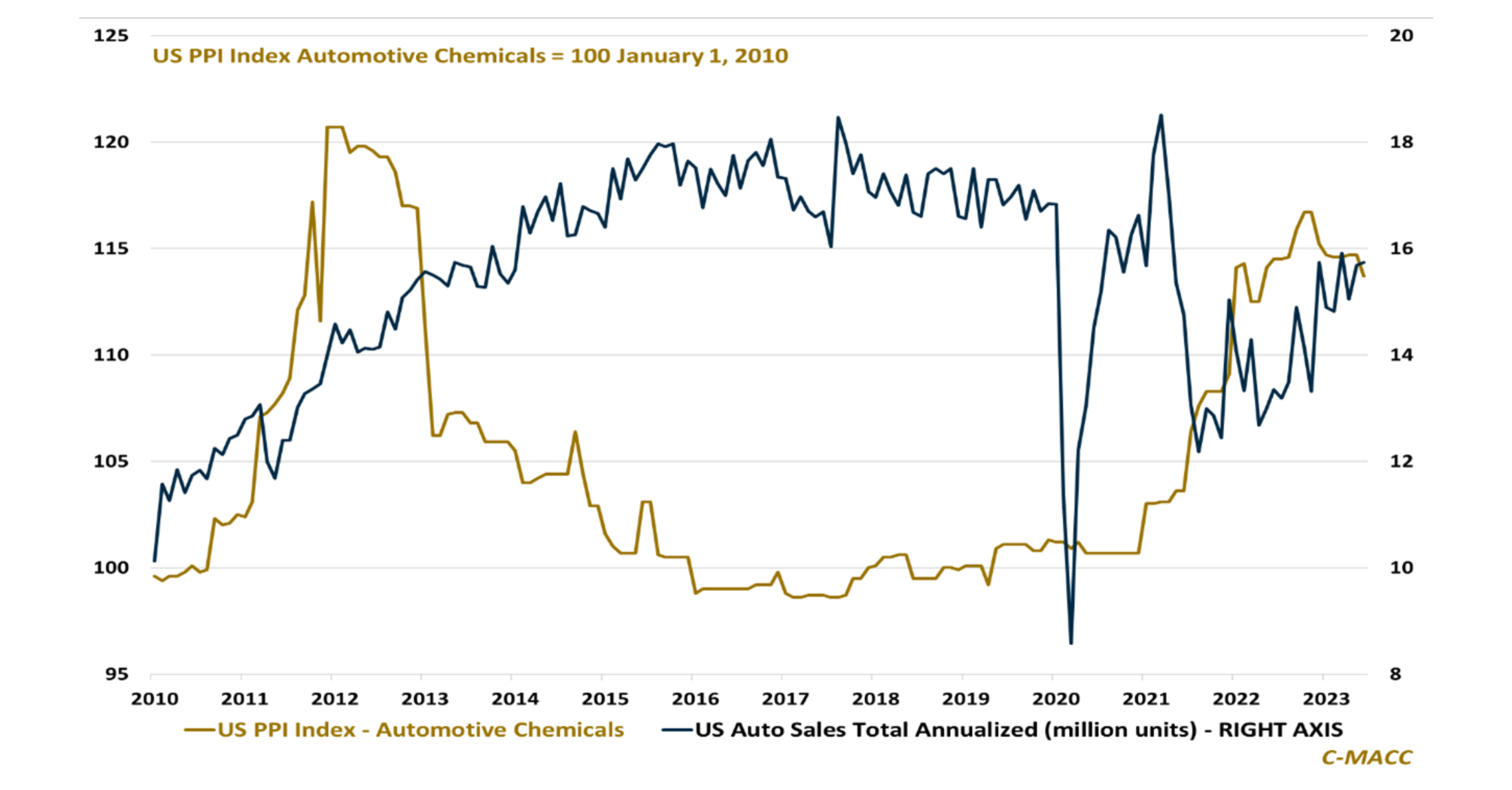

Automotive chemical suppliers have benefited from rising auto production in 2022/23, partly due to inventory rebuilding – we think significant headwinds will face auto chemical

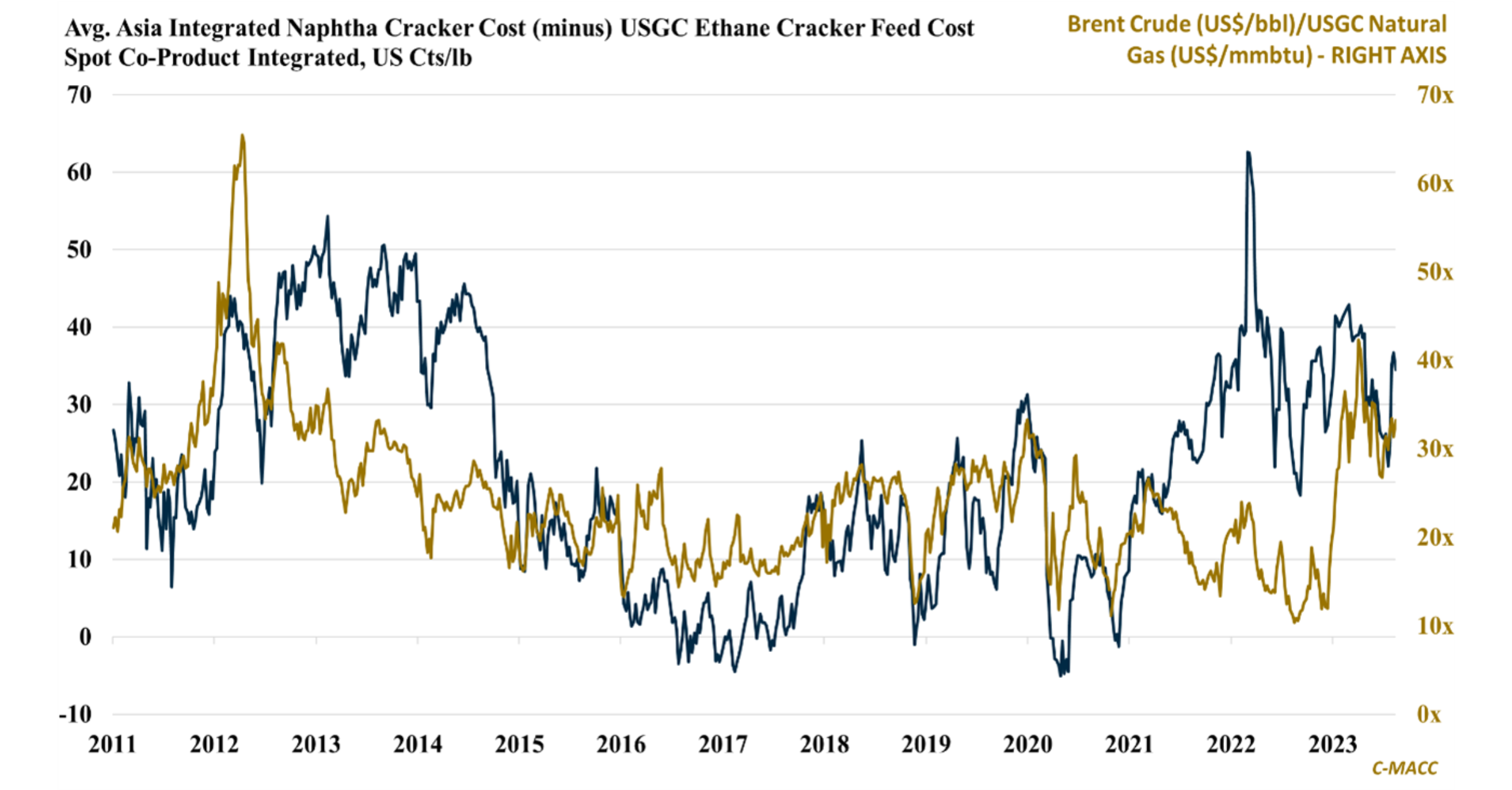

Energy and chemical sector strategic ties will strengthen as value-chain integration benefits rise – a lengthy period of low margins, even in cost-advantaged areas, will

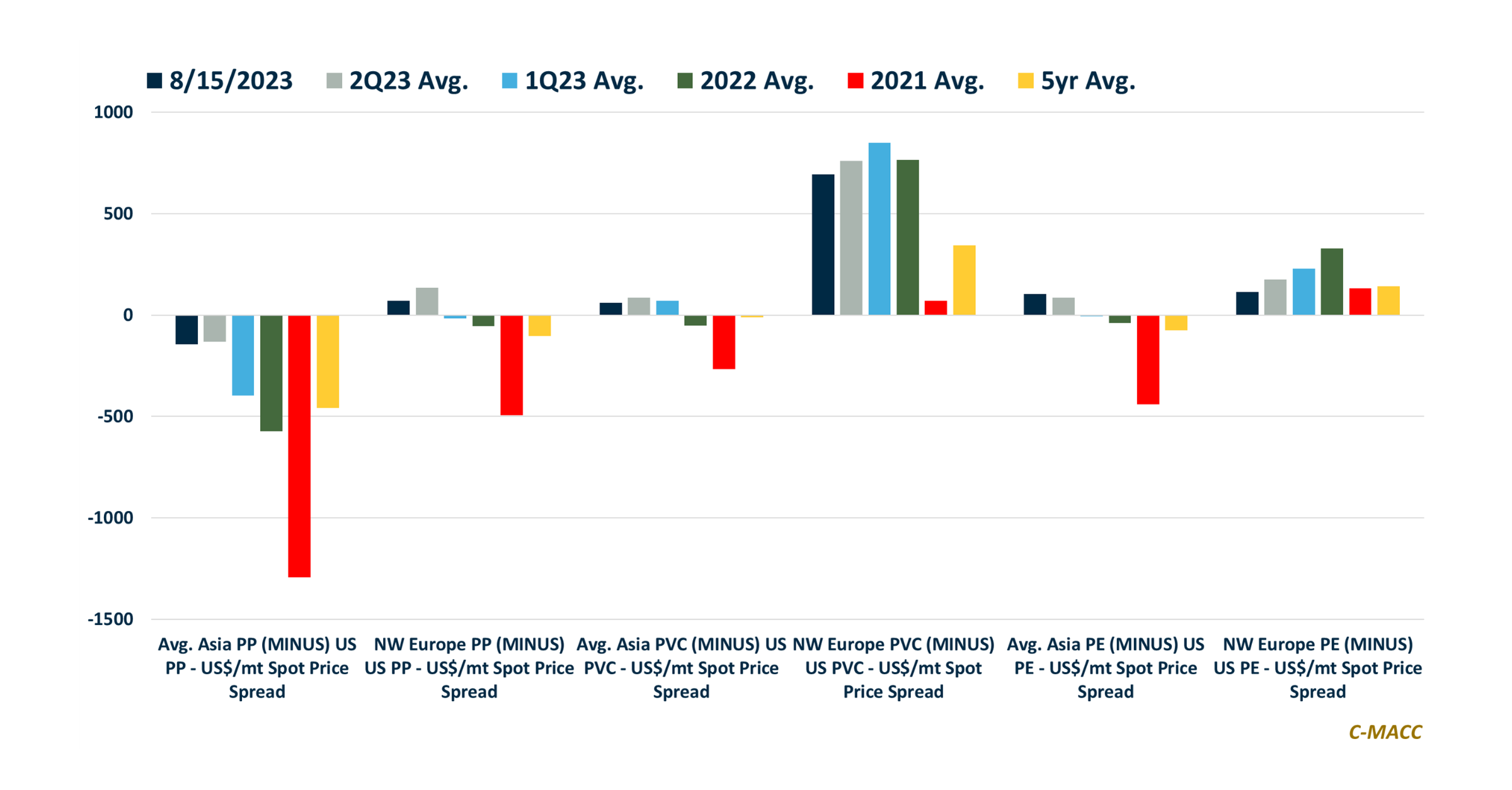

Polymer price differences (minus freight) face compression between regions as oversupplied conditions mount – global cost curve placement is the best gauge of regional integrated

The European chemical industry is cost-disadvantaged, and its end markets are mostly mature, but its sizable existing production base could offer opportunities for some amid

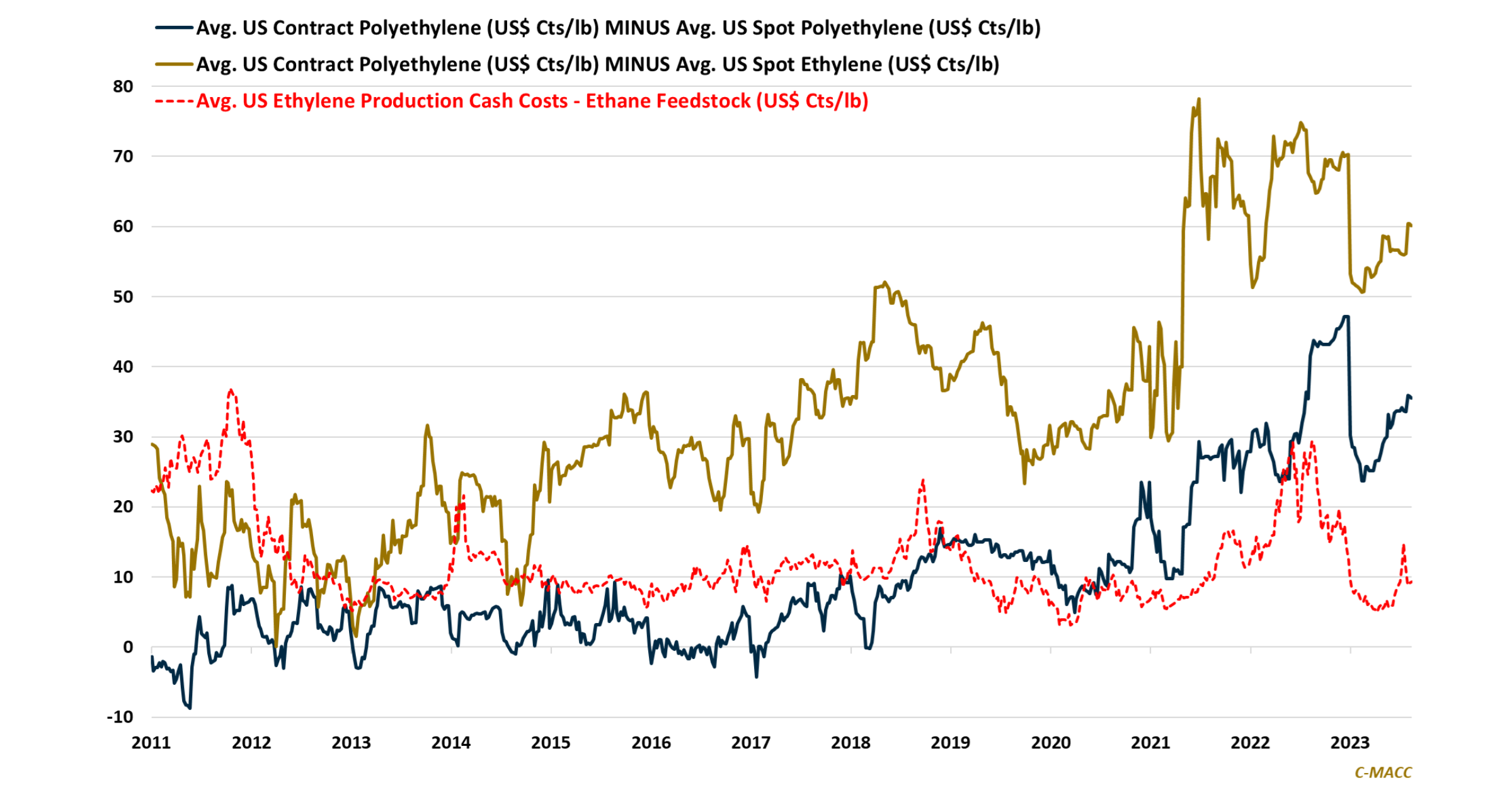

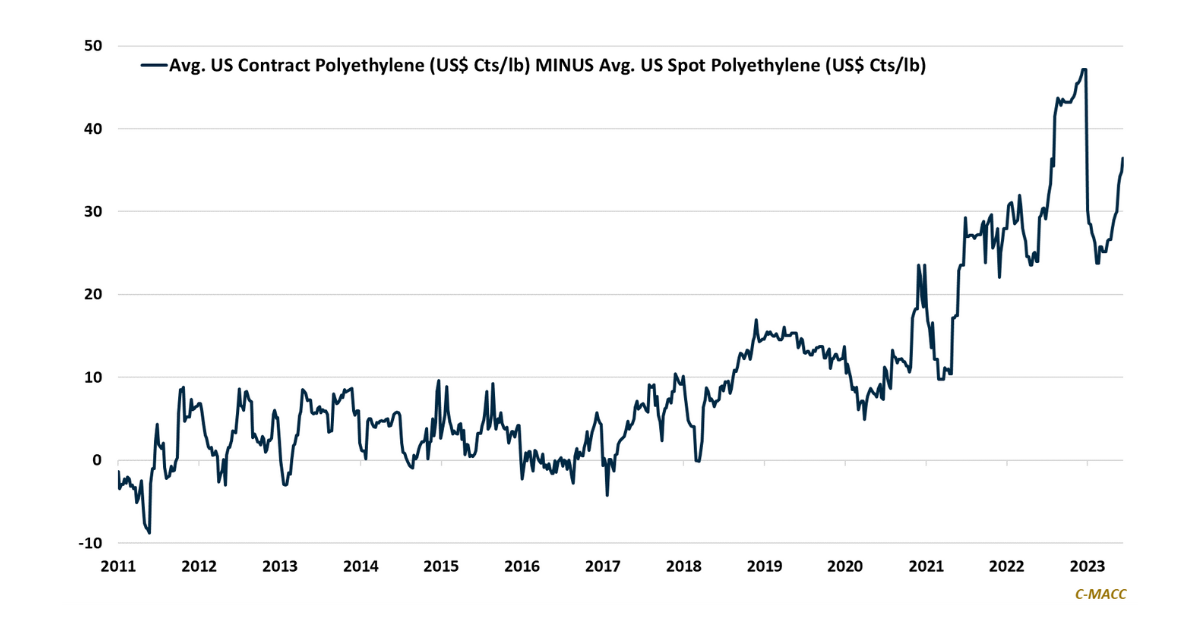

US polyethylene contract prices show an upward trend relative to spot values as exports have risen compared to domestic demand, becoming less linked to the