Global Market Analysis

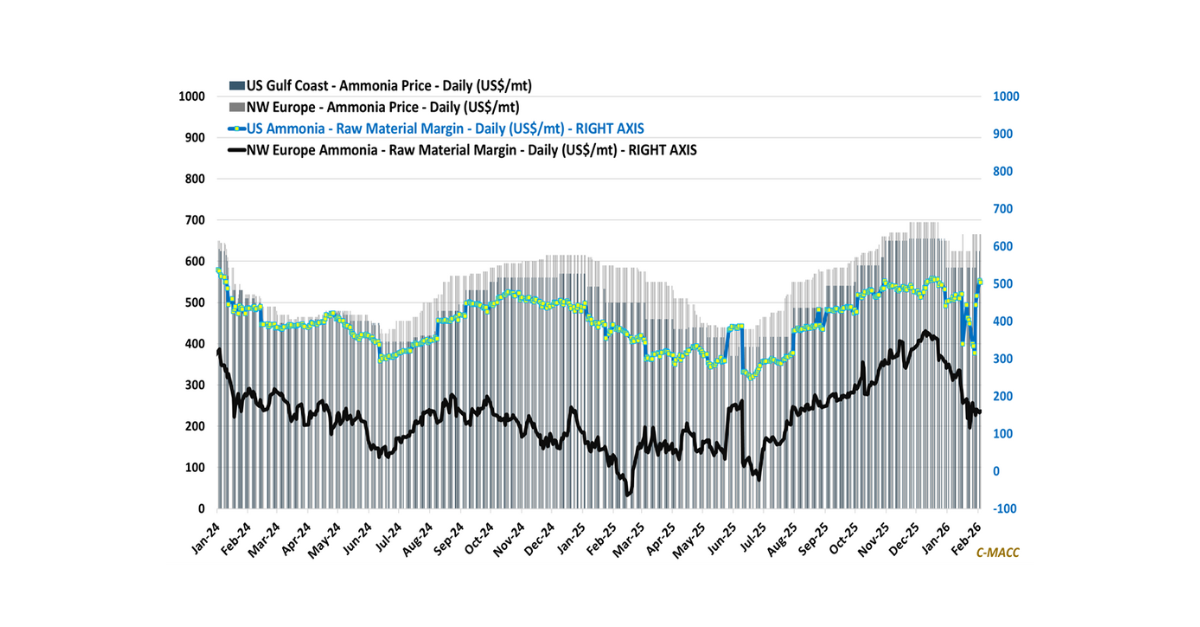

General Thoughts: Ammonia’s fertilizer-anchored cycle diverges from most chemicals, signaling tight supply and investment incentives, while petrochemicals face surplus-driven signals discouraging growth capital.

Supply Chain/Commodities: