Polymer Global Analysis

Resin To Riches: Weekly Plastic Market Insights

- General Thoughts: A key debate across polymer markets is whether current trough conditions will carry from 2025 to 2026 and potentially worsen; most expect a harsh 2026 setting. Is this why it will likely be better than most anticipate?

- Polyethylene (PE): Production rationalization and selective rationalization anchor short-term stability. September’s US inventory draw offers tactical price support as global oversupply shifts toward integration-led structural rebalancing.

- Polypropylene (PP): Global PP margins remain fragile as feedstock dislocations persist. However, integration depth and disciplined operating rates establish resilient producers amid Asia-led oversupply and Western demand stagnation.

- Polyvinyl Chloride (PVC): Global PVC prices are steady, US inventories drop in September, and construction bifurcates; differentiated, integrated producers gain an advantage while cost-intensive regions confront structural headwinds.

- Other Sector Developments: Feedstock spreads remain narrow globally, with declines seen last week across most feedstocks and monomers, suggesting downward upstream cost pressure on polymer prices in early 4Q25.

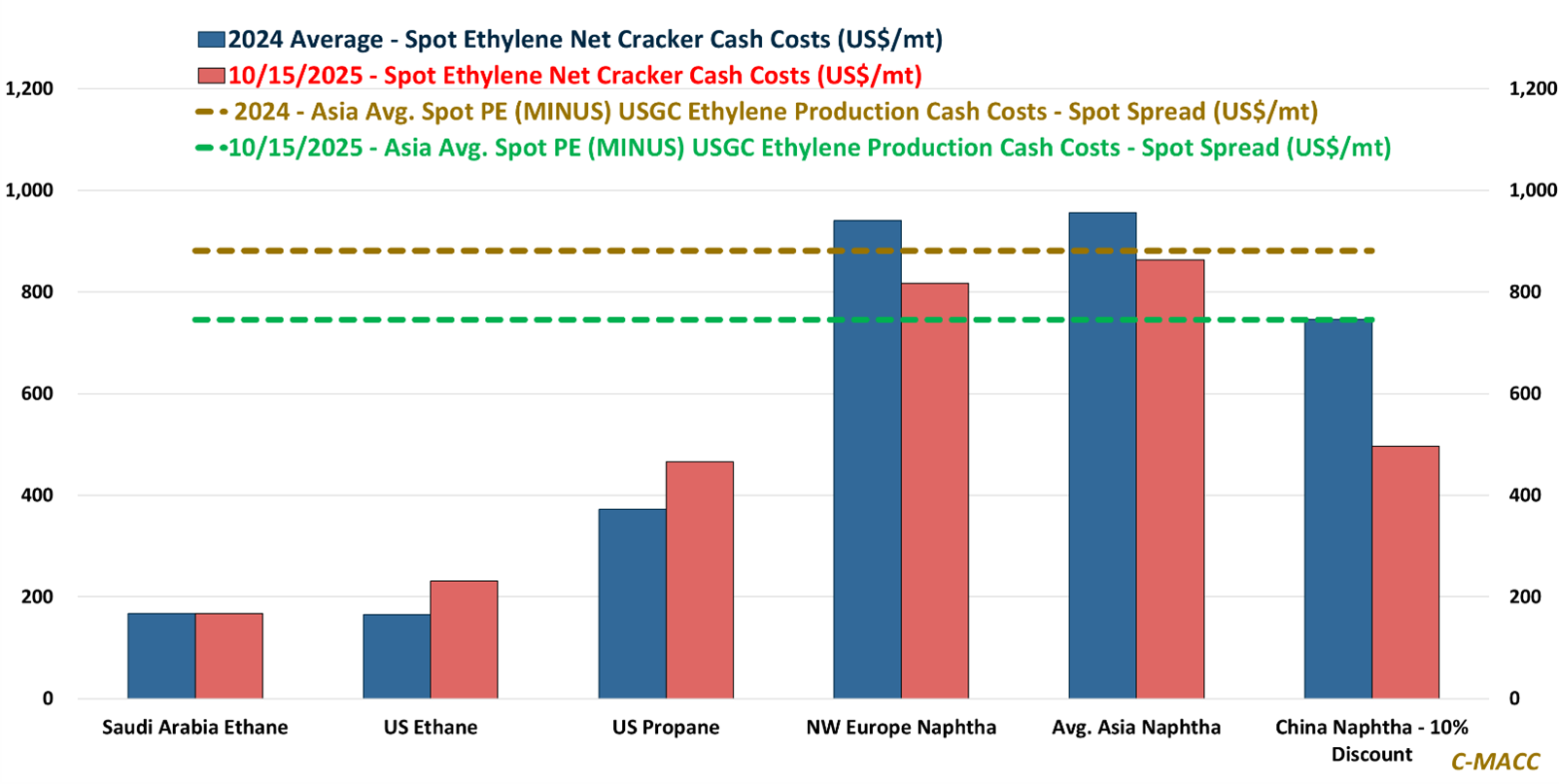

Exhibit 1 – Chart of the Day: Cost convergence signals reinvention and the early architecture of the next upturn.

Source: Bloomberg, C-MACC Estimates, October 2025

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!