Global Market Analysis

General Thoughts: US relative cost advantages persist, but rising global prices are compressing downstream margins as exports rise and cost transmission accelerates across global industrial

General Thoughts: US relative cost advantages persist, but rising global prices are compressing downstream margins as exports rise and cost transmission accelerates across global industrial

General Thoughts: Supply shocks are shifting power from cost to control, concentrating value in integrated systems as export-driven convergence reshapes demand, margins, and capital allocation

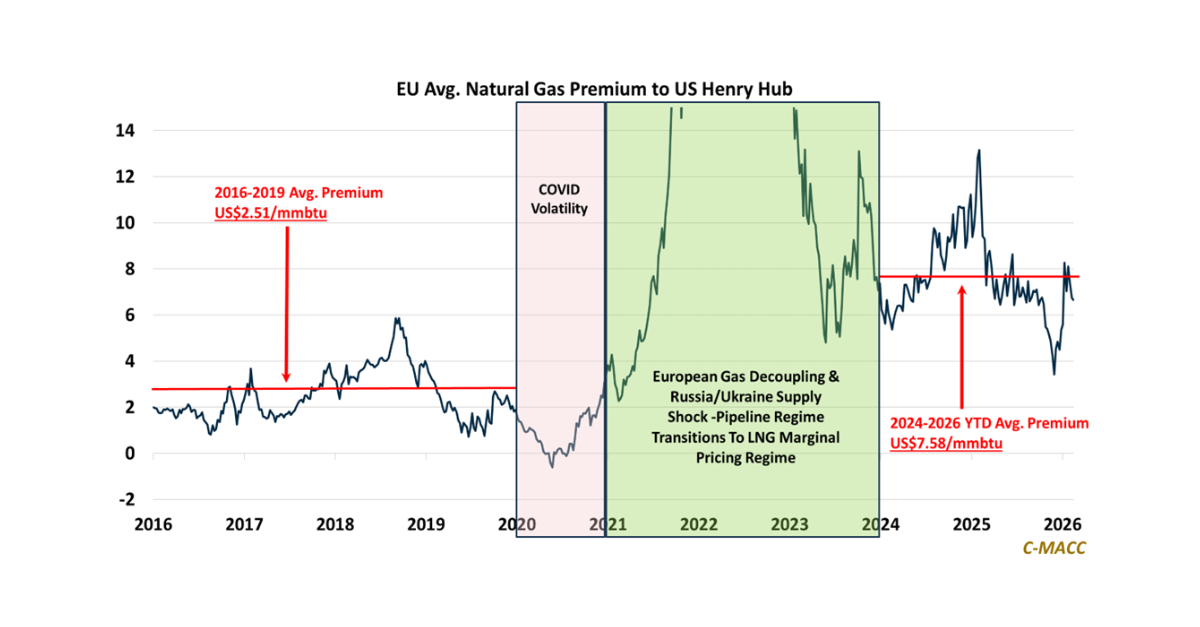

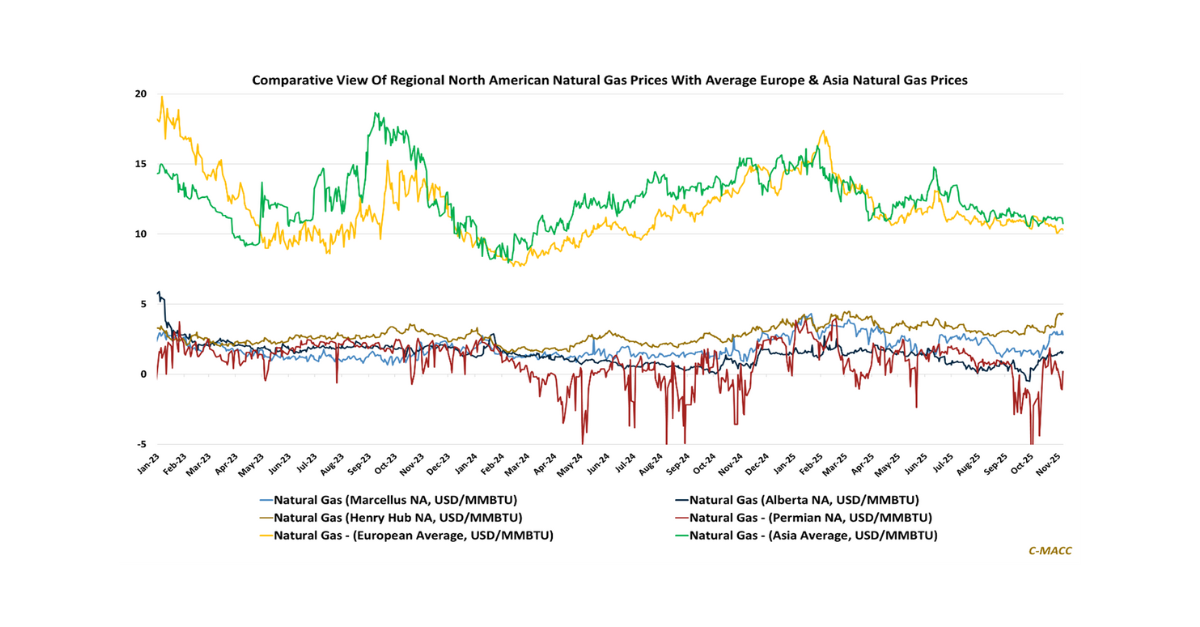

Persistent European premiums over Henry Hub confirm LNG marginal clearing as the dominant marginal price-setting mechanism, anchoring US export-linked gas economics and long-cycle infrastructure returns.

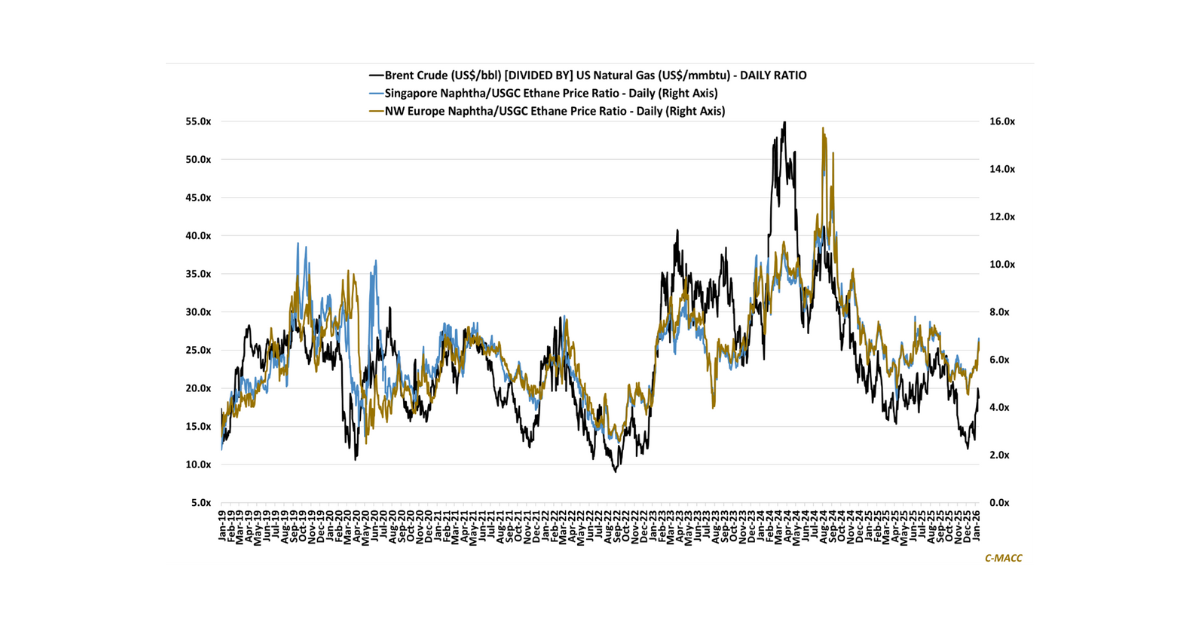

General Thoughts: Energy-linked corn economics and widening oil–gas dispersion are shifting global marginal cost leadership toward natural gas advantaged, capital-disciplined integrated production platforms globally.

Supply

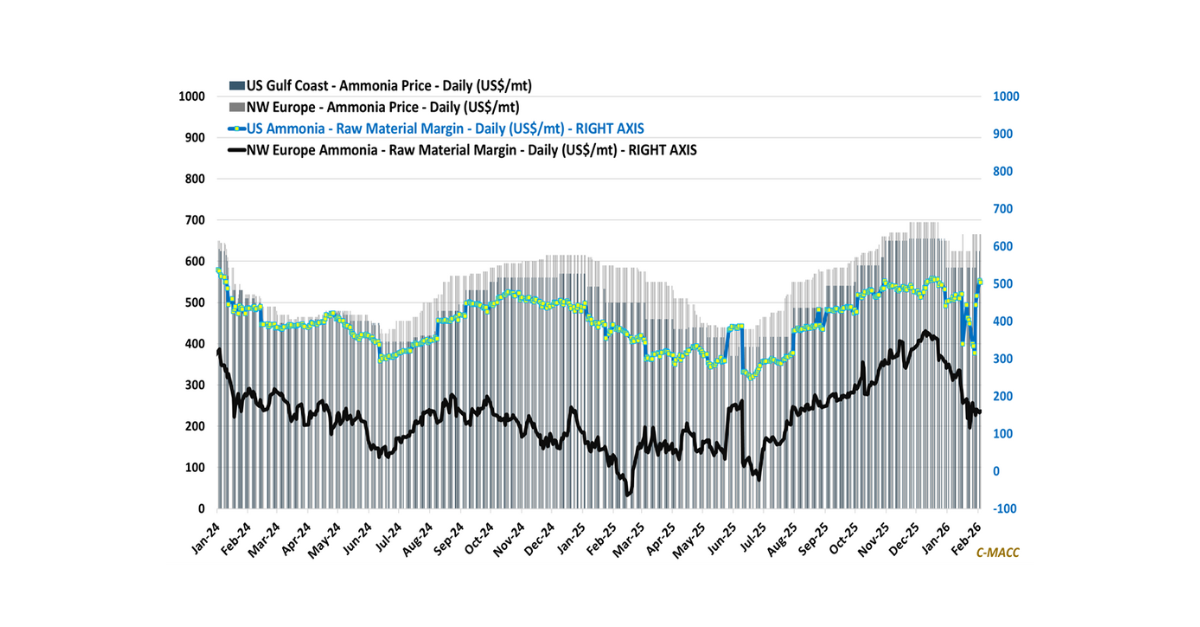

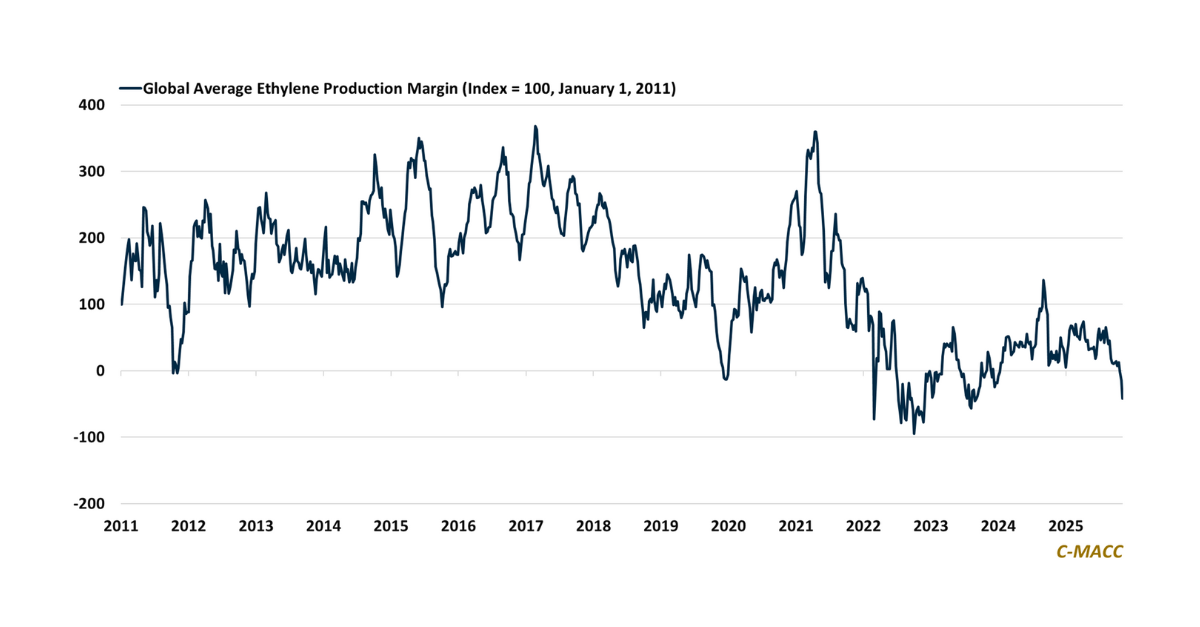

General Thoughts: Ammonia’s fertilizer-anchored cycle diverges from most chemicals, signaling tight supply and investment incentives, while petrochemicals face surplus-driven signals discouraging growth capital.

Supply Chain/Commodities:

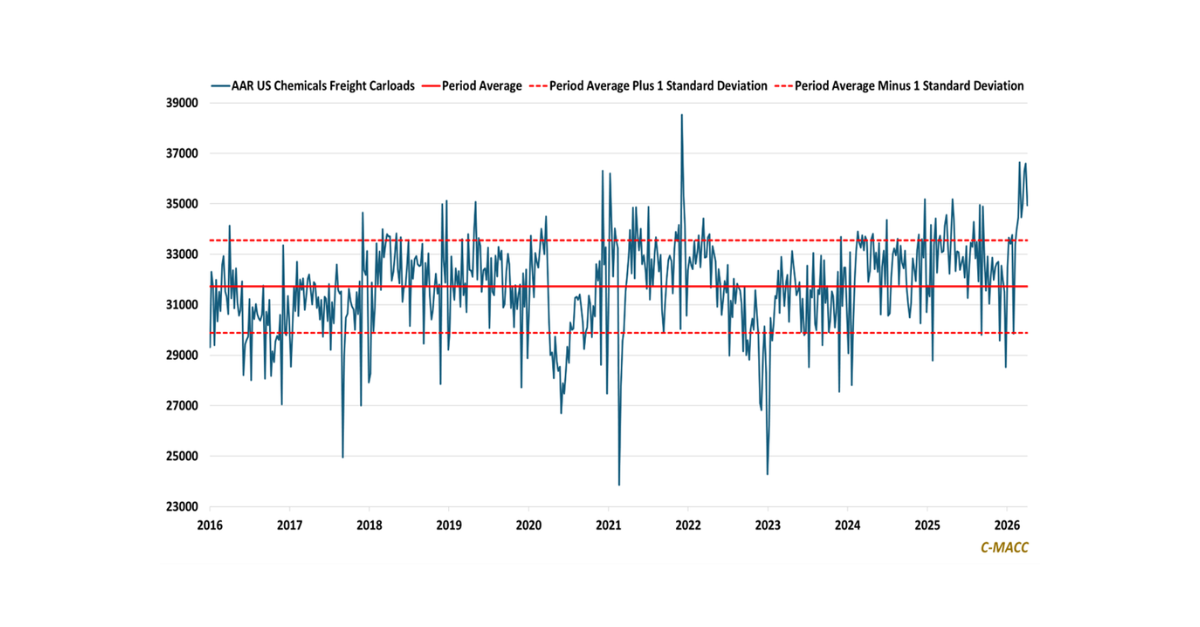

General Thoughts: Natural gas volatility now translates into risk, as export integration, consolidation, and midstream optionality reprice feedstock economics, slow marginal investment, and lift risk

China’s slowing consumption and persistently low relative price inflation push excess supply outward, reviving export-led clearing and intensifying global price competition as logistics increasingly normalize

General Thoughts: Early-2026 cost-curve shifts amid persistent chemical market oversupply are forcing restructuring, with clear evidence likely emerging in 4Q25 results and more decisive 2026

General Thoughts: Global chemical profit improvement in the near term depends less on cyclical recovery and more on rationalized capacity, cost integration, and policy agility

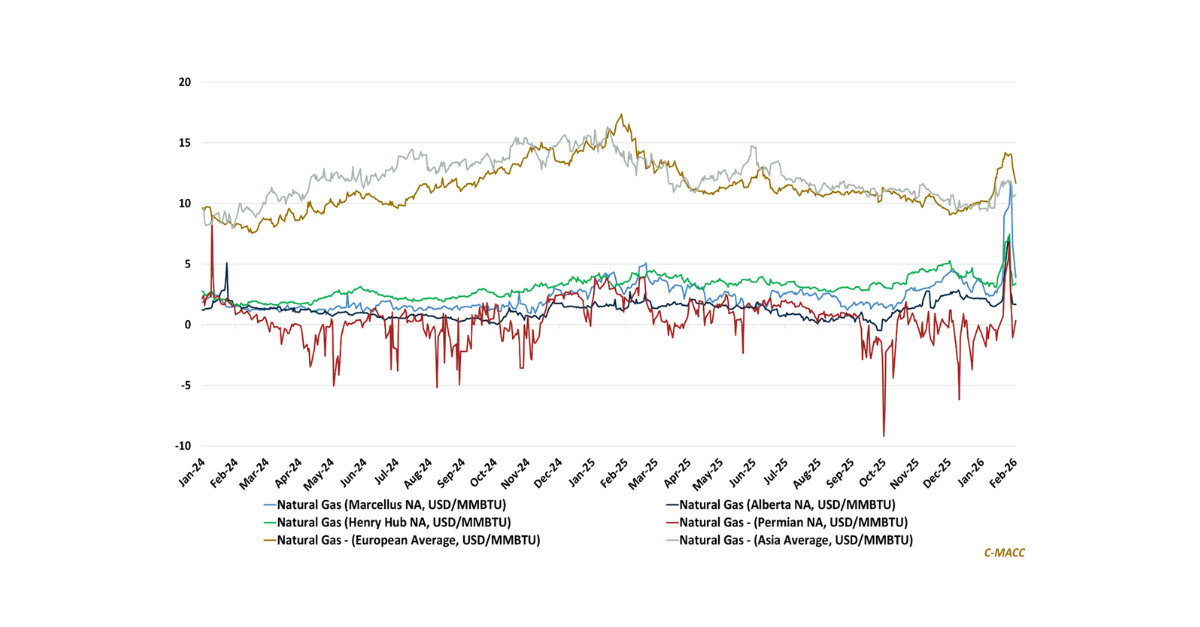

The US Gulf Coast is rapidly emerging as the world’s dominant price-setting energy hub, where infrastructure integration transforms natural gas, NGLs, and LNG into globally