Sunday Executive Summary

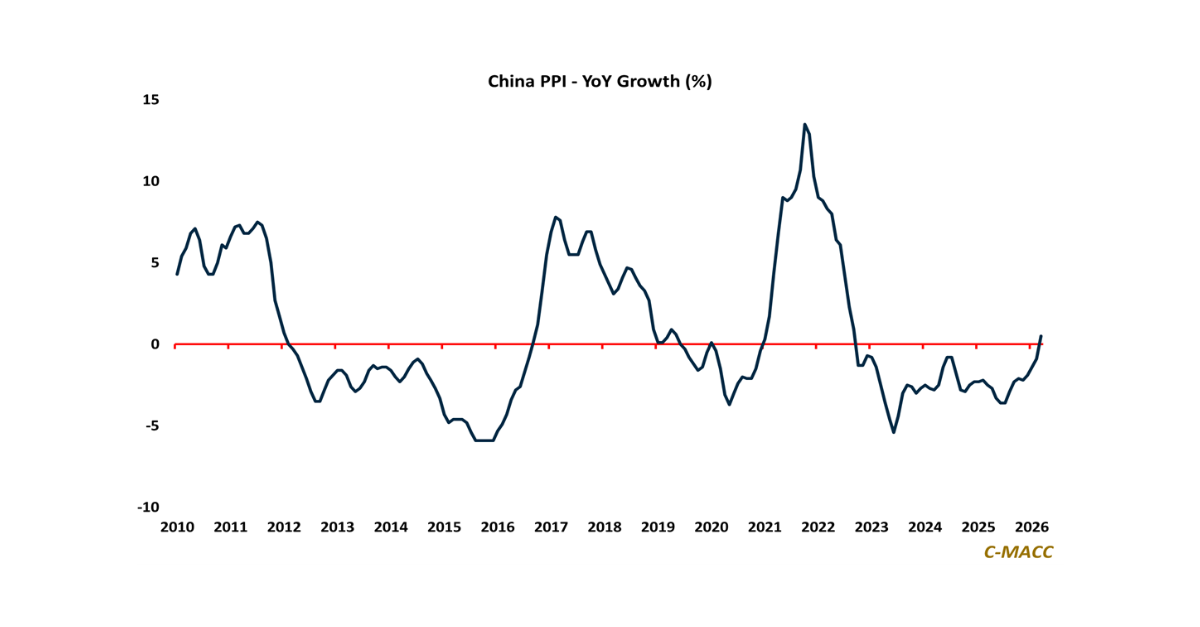

China’s 0.5% YoY factory-gate inflation in March removed a trusted global relief valve, forcing markets to underwrite firmer resin and intermediate floors, slower cost deflation,

China’s 0.5% YoY factory-gate inflation in March removed a trusted global relief valve, forcing markets to underwrite firmer resin and intermediate floors, slower cost deflation,

1st Topic of the Week: Wind input demand is shrinking as power dollars pivot to other generation sources and grid equipment; will policy ultimately redirect

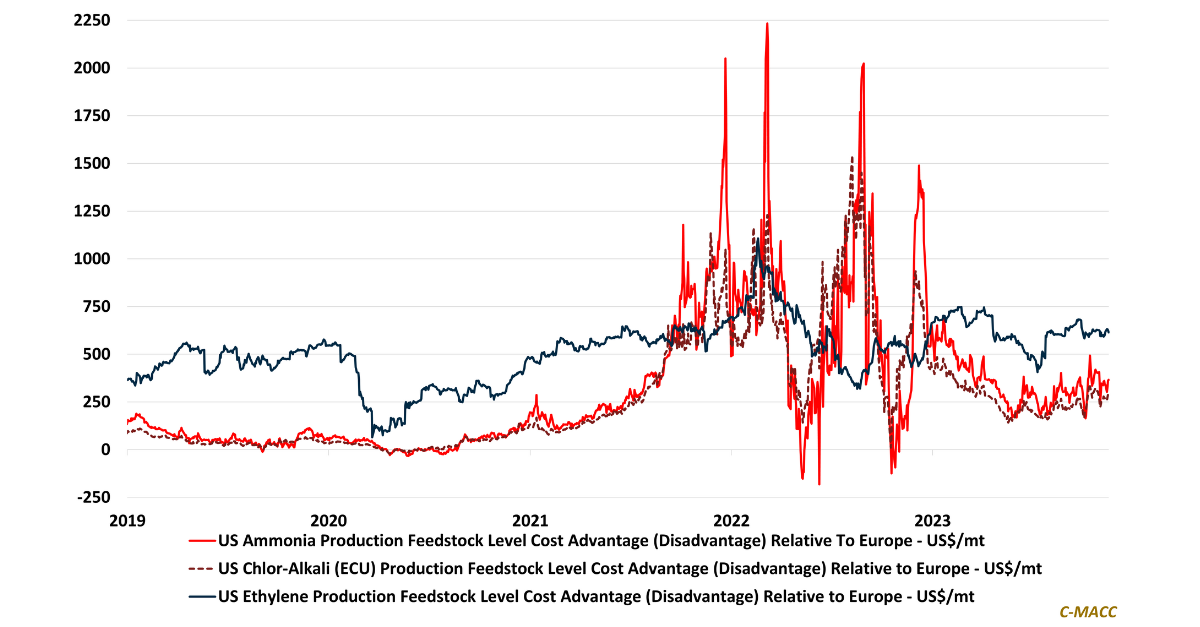

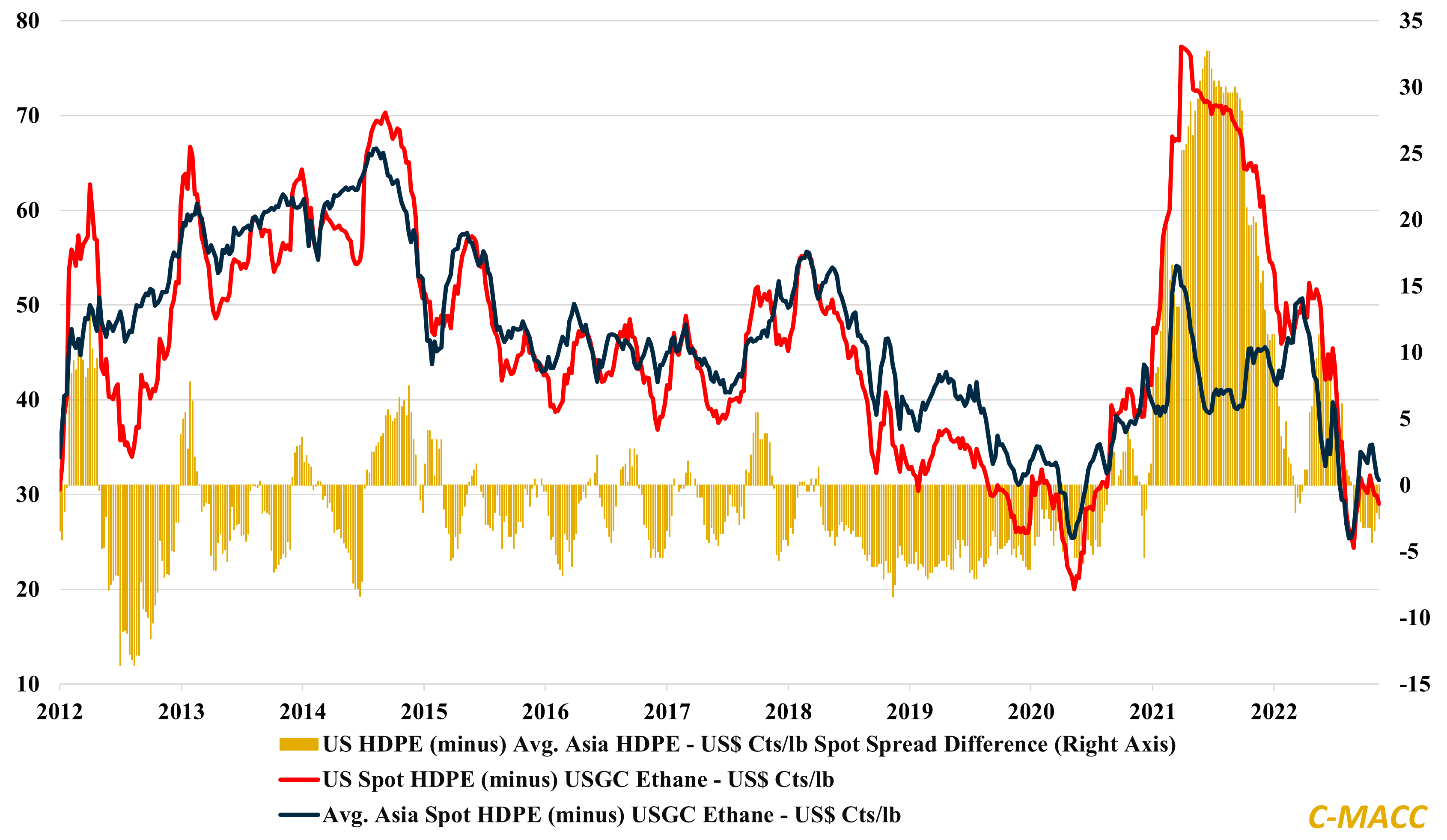

North American chemical producers have a sizable cost advantage relative to Europe and Asia – the benefits of those competing more with ex-US natural gas

The global impact of 2H23 oil market shifts on regional integrated commodity chemical profit is less difficult to gauge than for non-integrated commodity and derivative

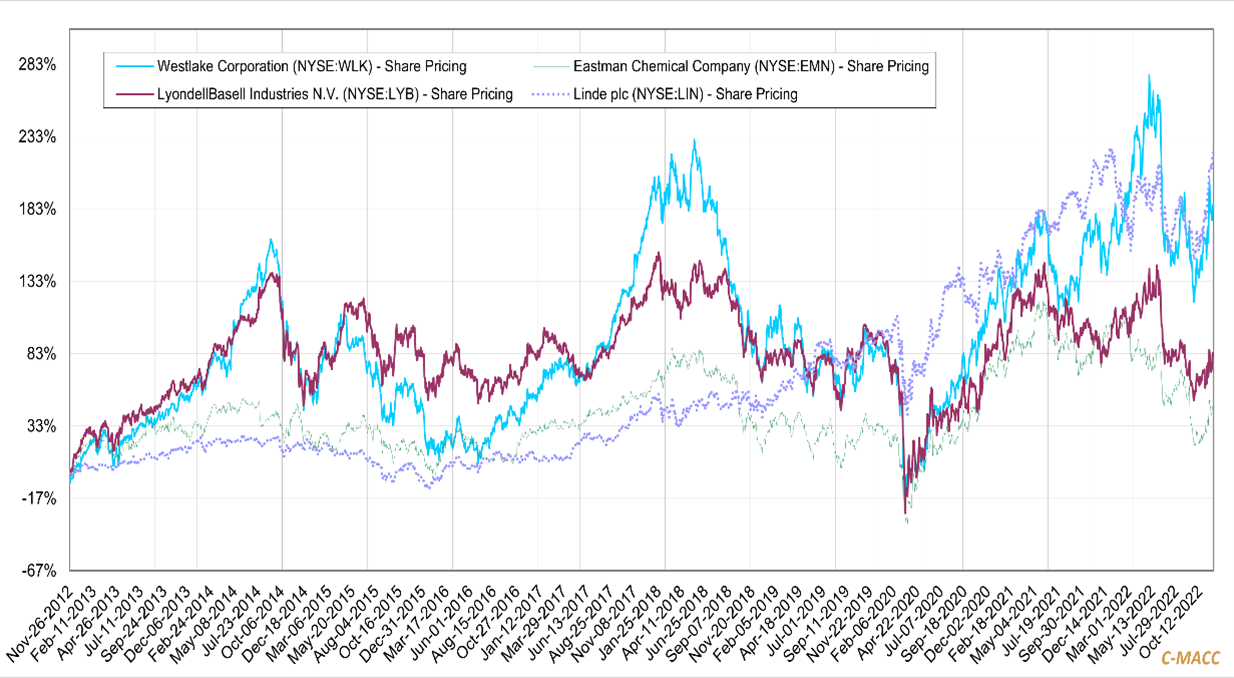

Most chemical sector investors agree that 2023 will be a tough year and 2024 will be better, but long-term risk-adjusted return views vary significantly by

As worsening business conditions into yearend lower 2023 outlooks, we think money will be made by those making consolidation moves versus those who hide.

Almost

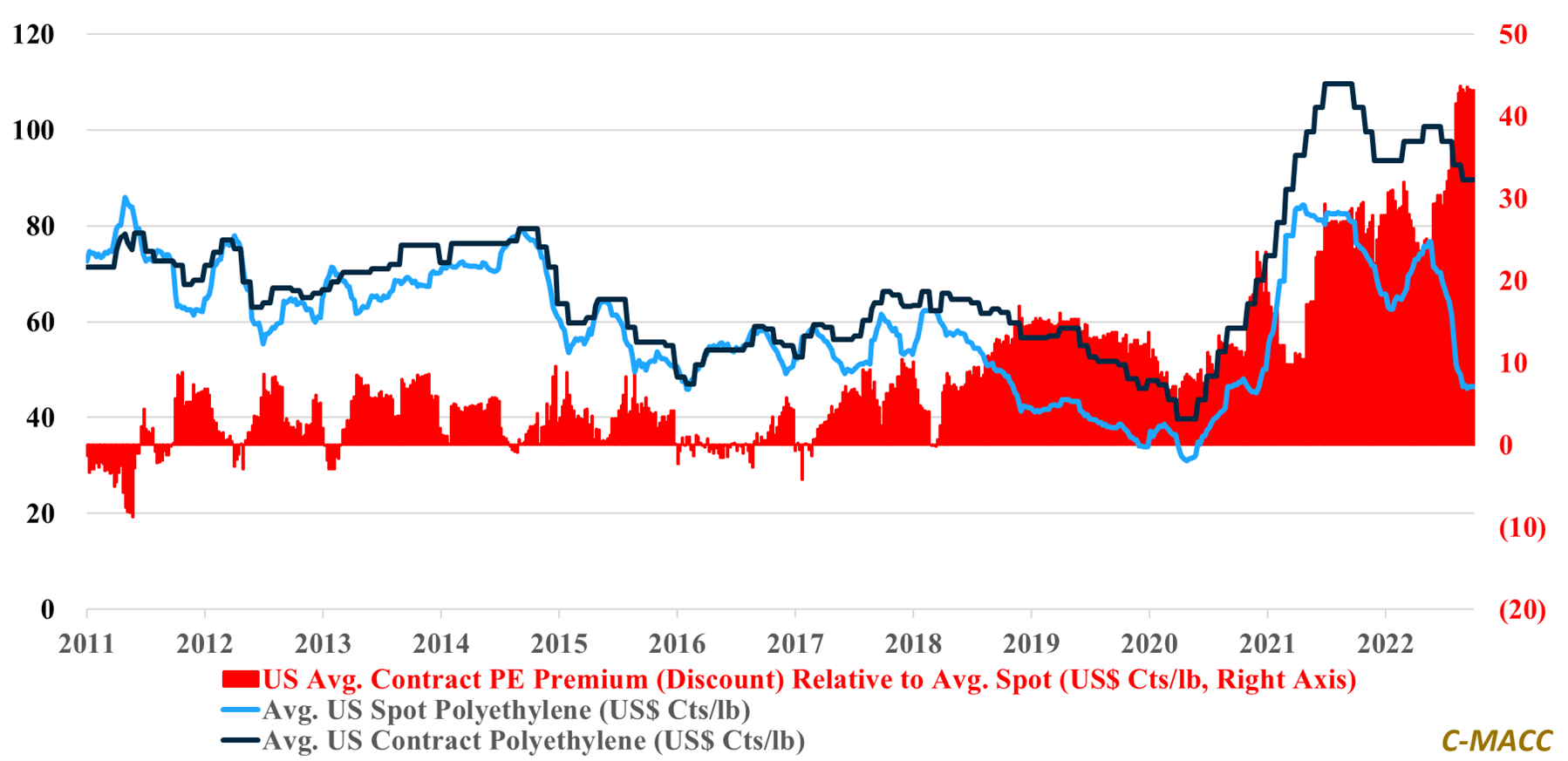

Global polymer prices, on average, step lower WoW relative to feedstocks, pushing chemical sector profit lower WoW. We discuss why a near-term sector profitability rebound

Global polymer values, on average, declined WoW, with US and Asia reflecting more declines than Europe, increasing concerns that a winter-led raw material surge could

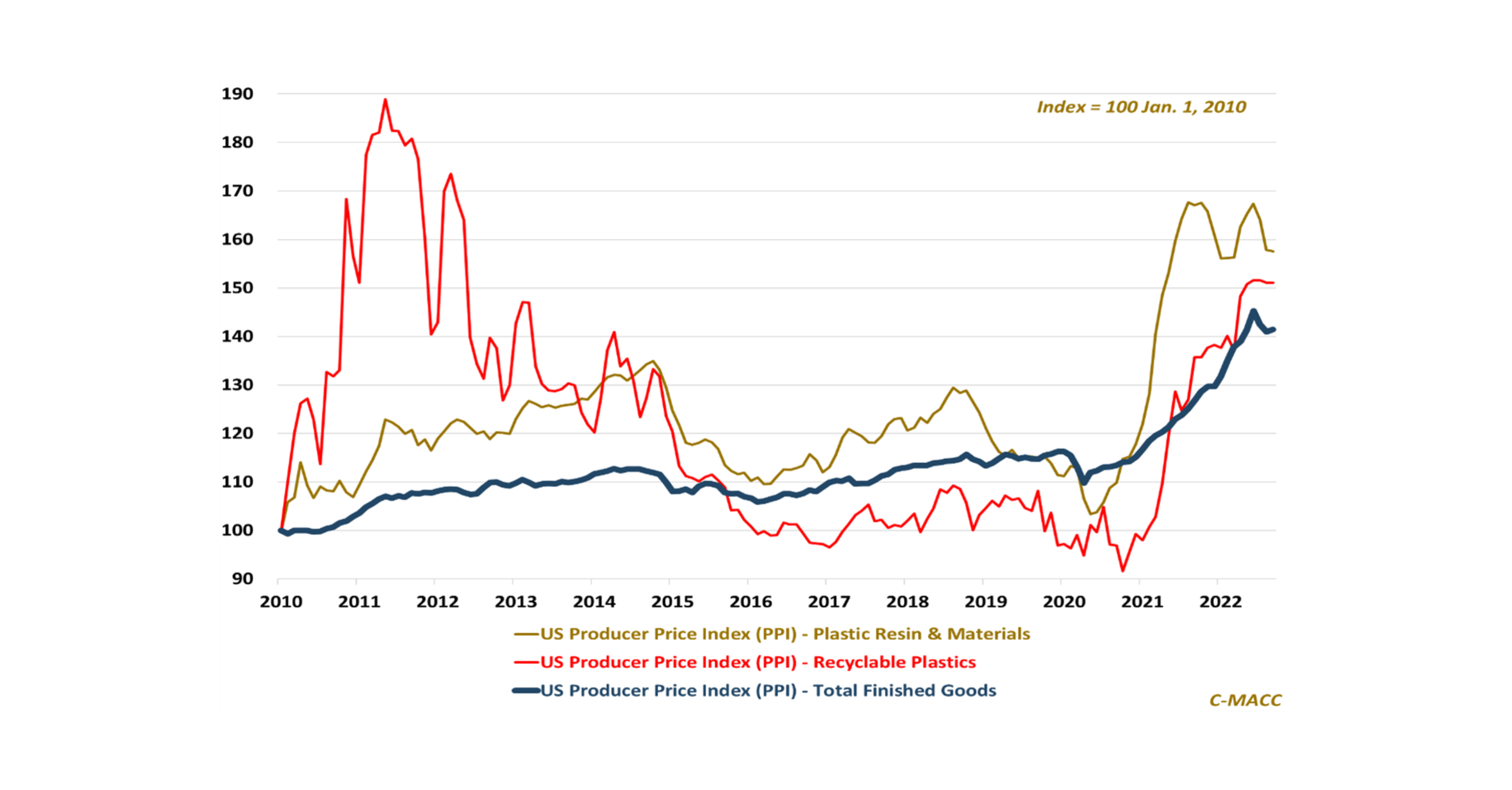

The US Sept. producer price index (PPI) posting exceeded expectations. Most views of inflation peaking in 4Q22 inadequately consider energy market and geopolitical risks.

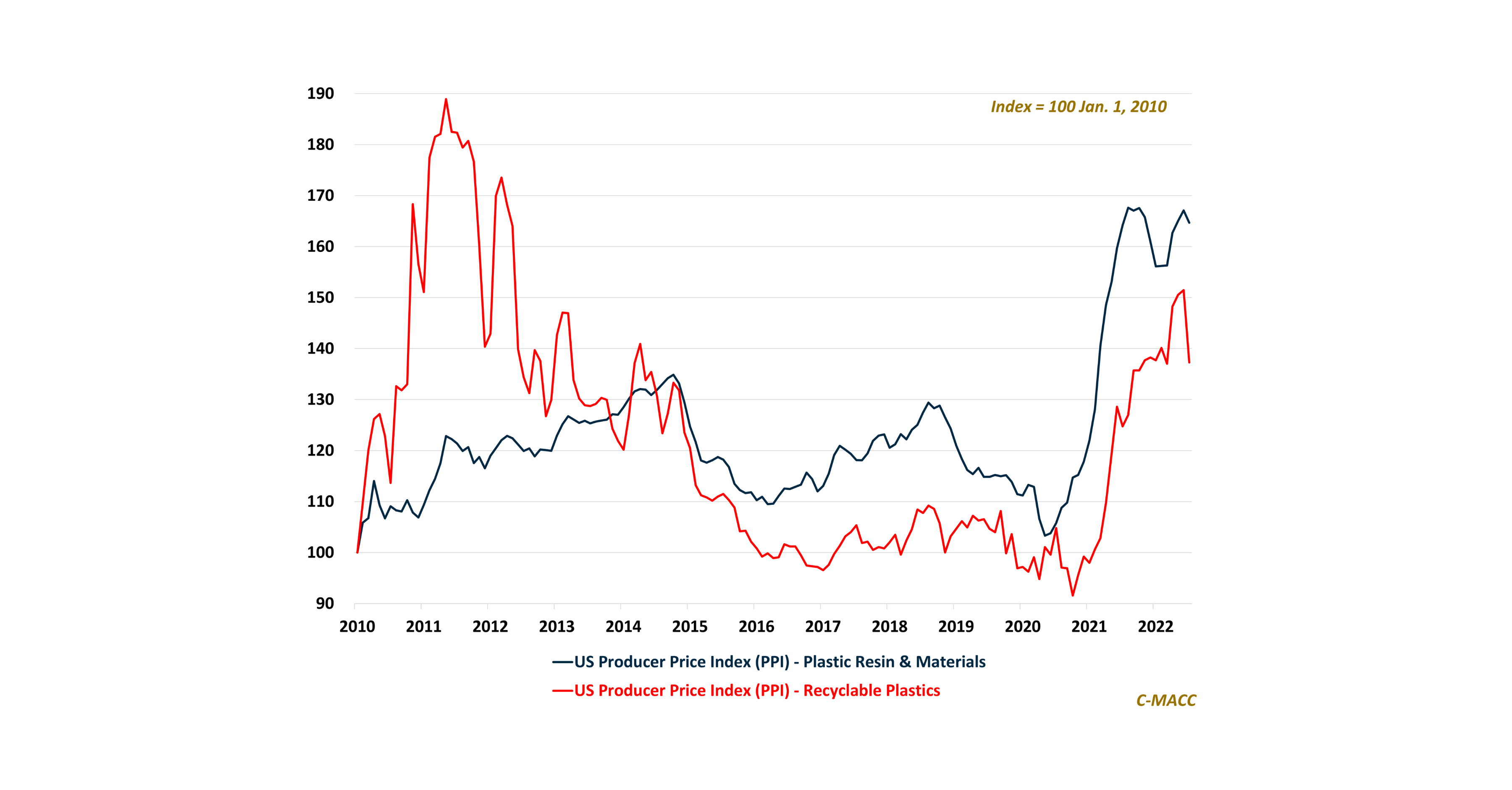

The price of plastic resin & materials and recycled plastics declined in July, and the value slide worsened in August. Recycled resin prices will likely