Sunday Executive Summary

2023 is off to a bad start with low margins (but maybe not low enough) and global operating rates reflecting significant oversupply, which could worsen.

2023 is off to a bad start with low margins (but maybe not low enough) and global operating rates reflecting significant oversupply, which could worsen.

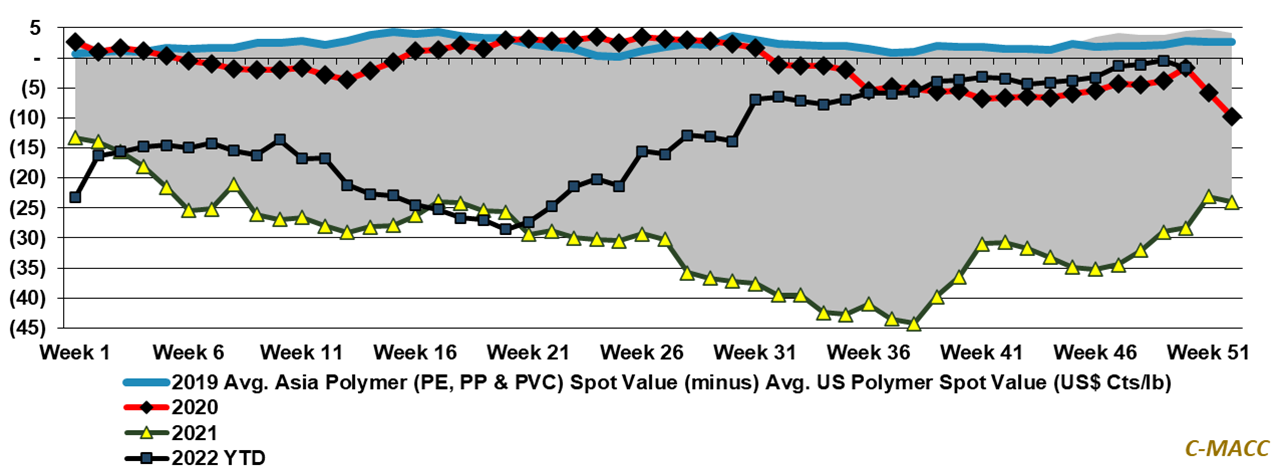

As chemical product availability increased, US spot polymer premiums relative to Asia mostly dissipated in 2H22. Domestic contract premiums are likely the next to drop.