Global Market Analysis

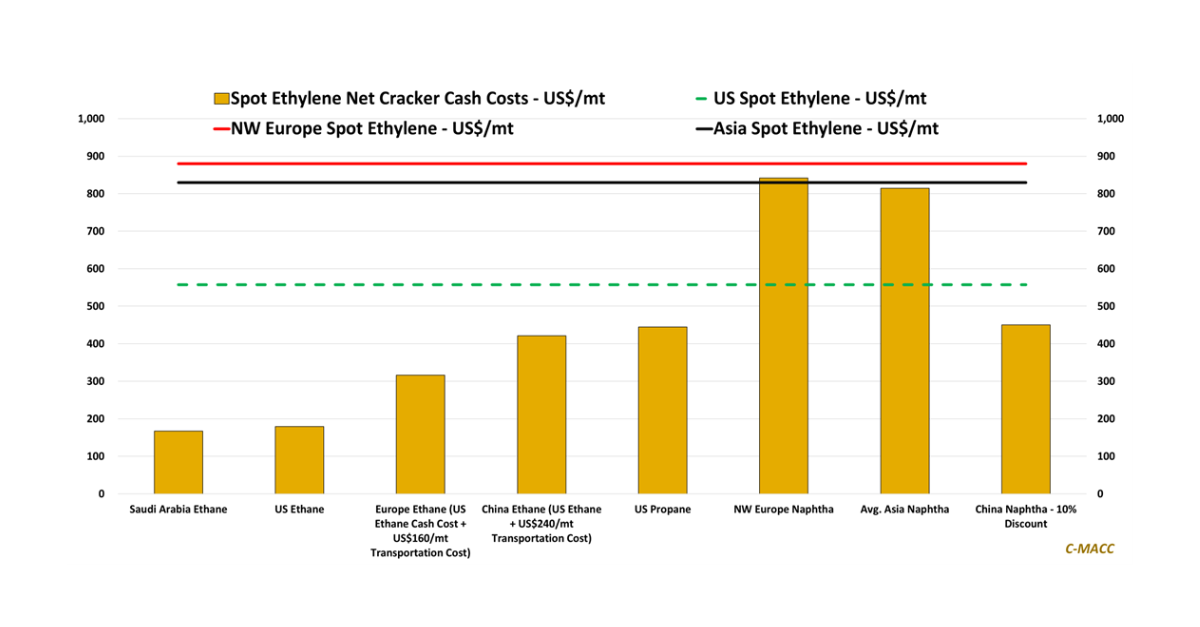

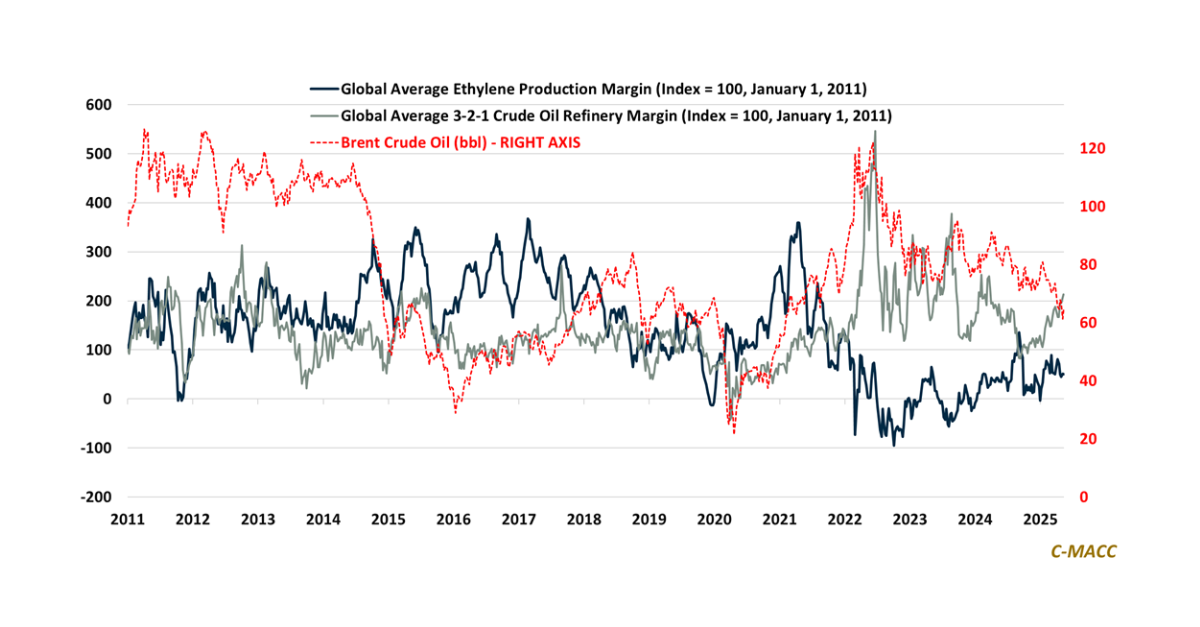

General Thoughts: US relative cost advantages persist, but rising global prices are compressing downstream margins as exports rise and cost transmission accelerates across global industrial

General Thoughts: US relative cost advantages persist, but rising global prices are compressing downstream margins as exports rise and cost transmission accelerates across global industrial

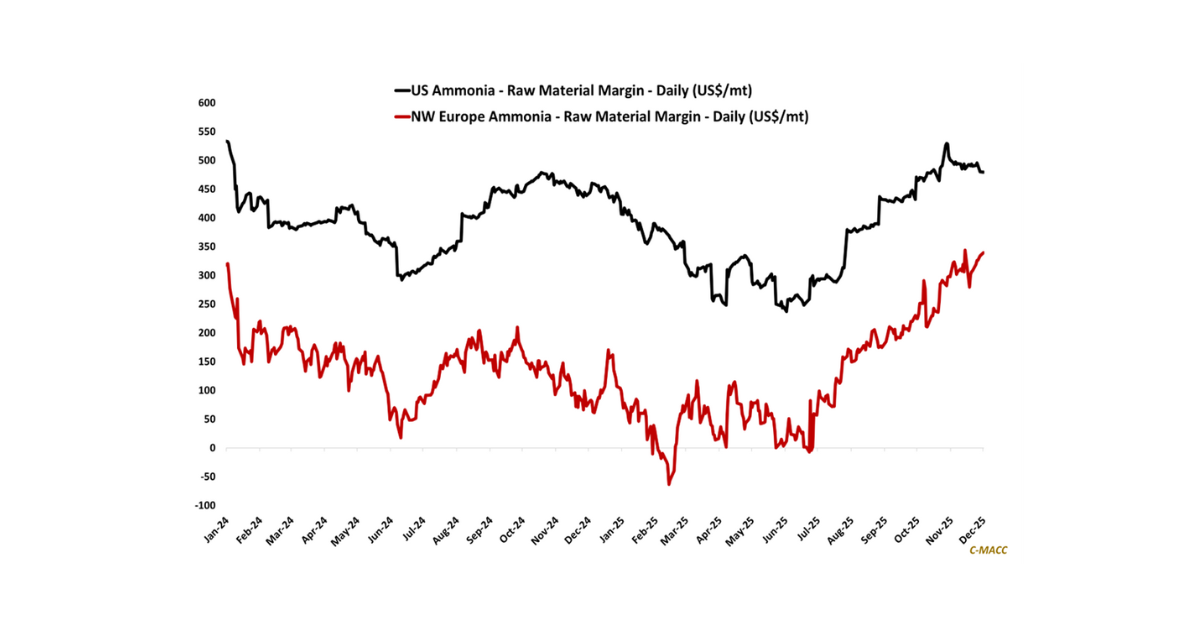

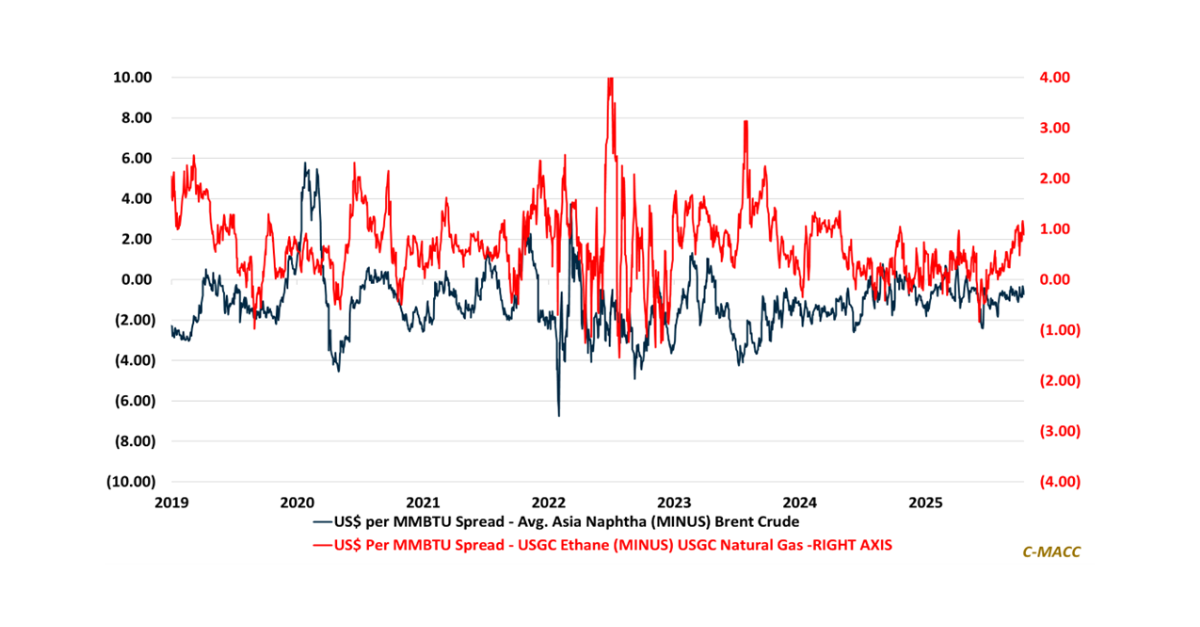

General Thoughts: Ammonia prices have surged to 2025 highs, while European and Asian natural gas prices have fallen to YTD lows relative to US levels,

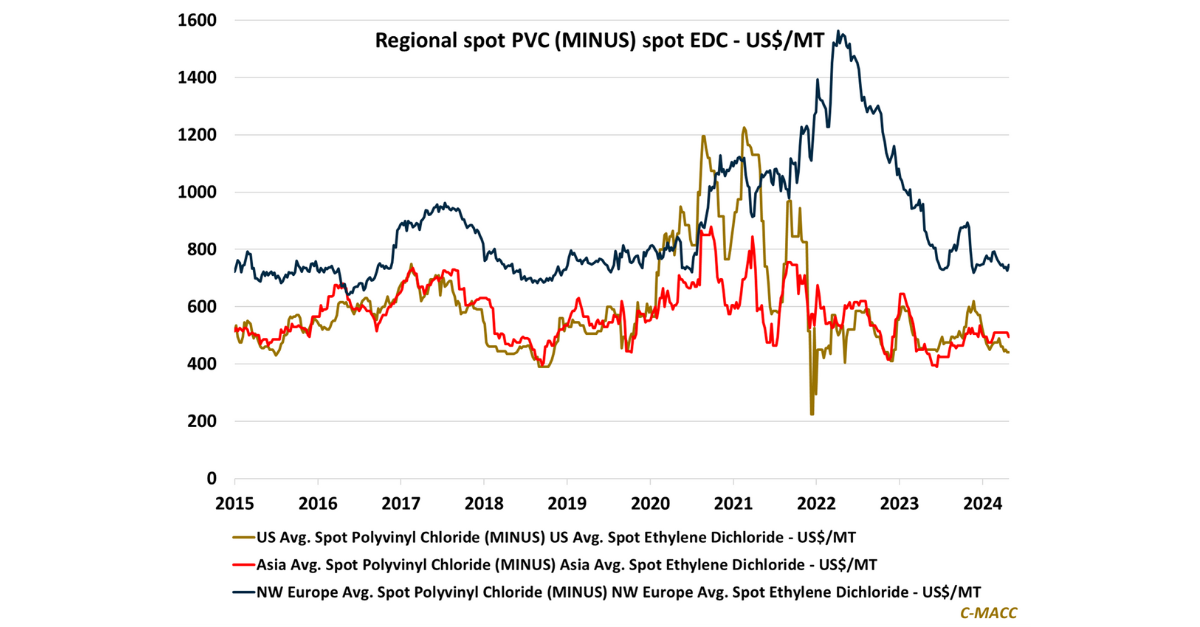

General Thoughts: Chemical feedstock dynamics increasingly signal a global inflection; margin compression forcing strategic resets, capital discipline, and system-wide realignment across industrial value chains.

Supply

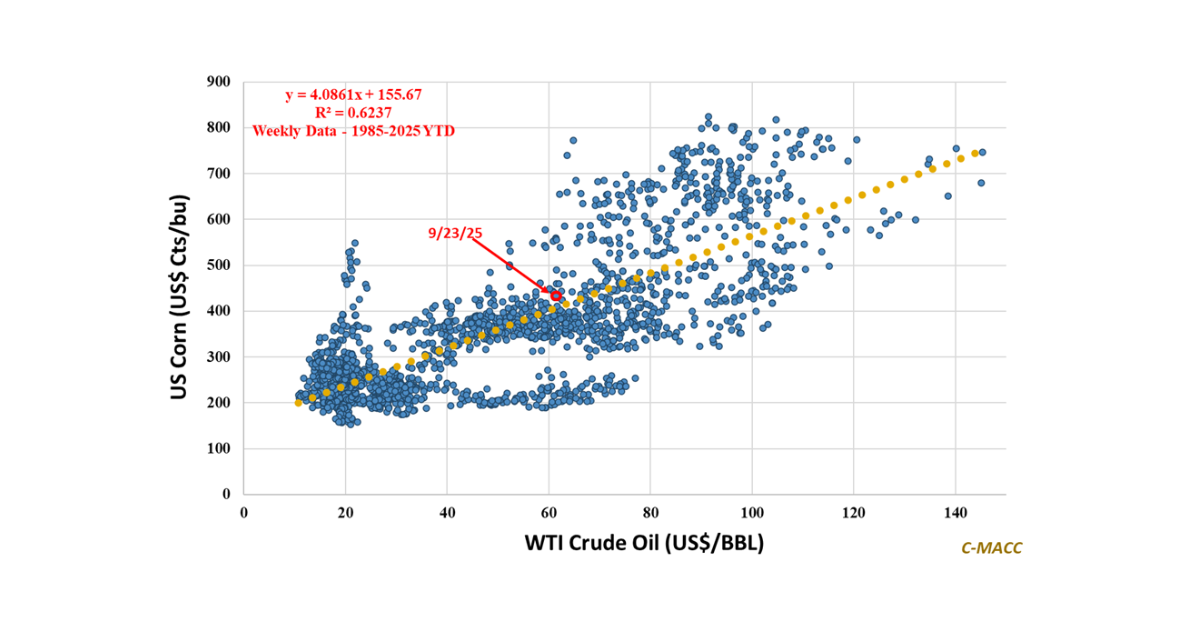

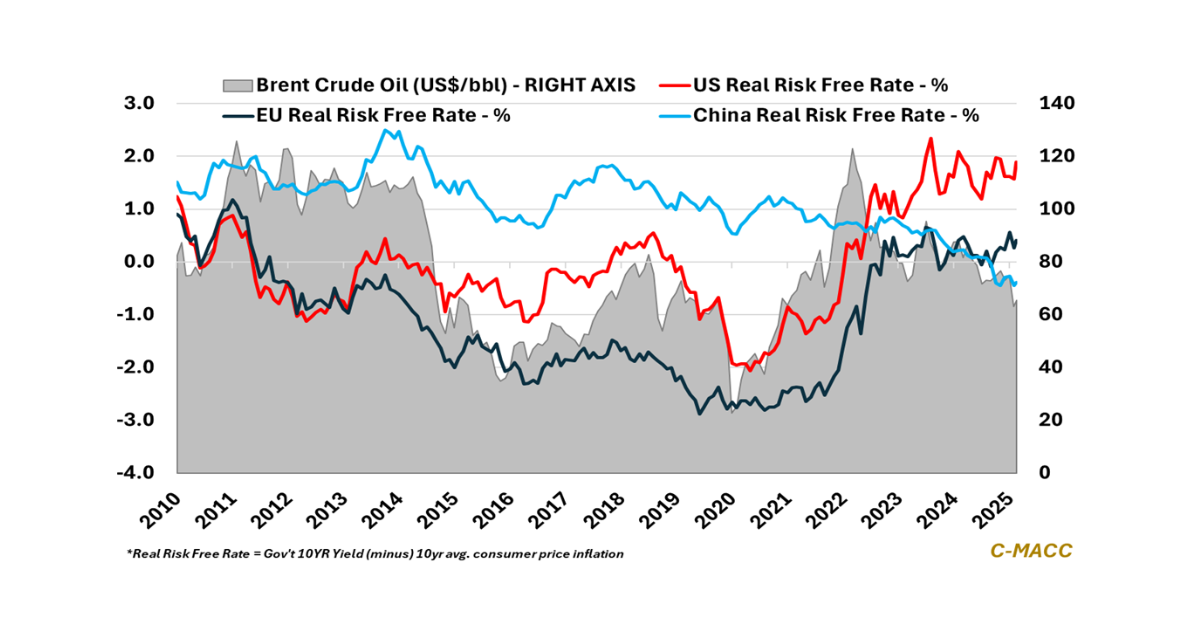

General Thoughts: Energy–agriculture linkages redefine global competitiveness and cost trajectories, reshaping inflation pathways, trade flows, investment decisions, and strategic resilience in late 2025 and 2026.

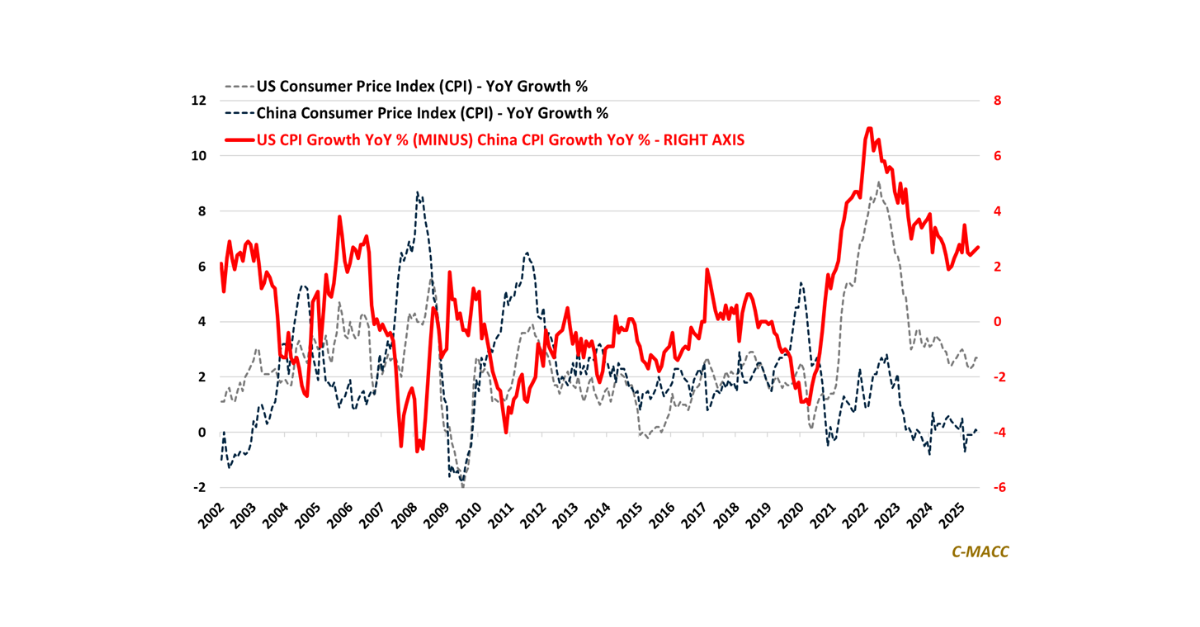

US-China inflation divergence realigns capital flows, currency dynamics, and trade competitiveness across services, manufacturing, and energy-linked exports spanning petrochemicals, agriculture, and industrial inputs.

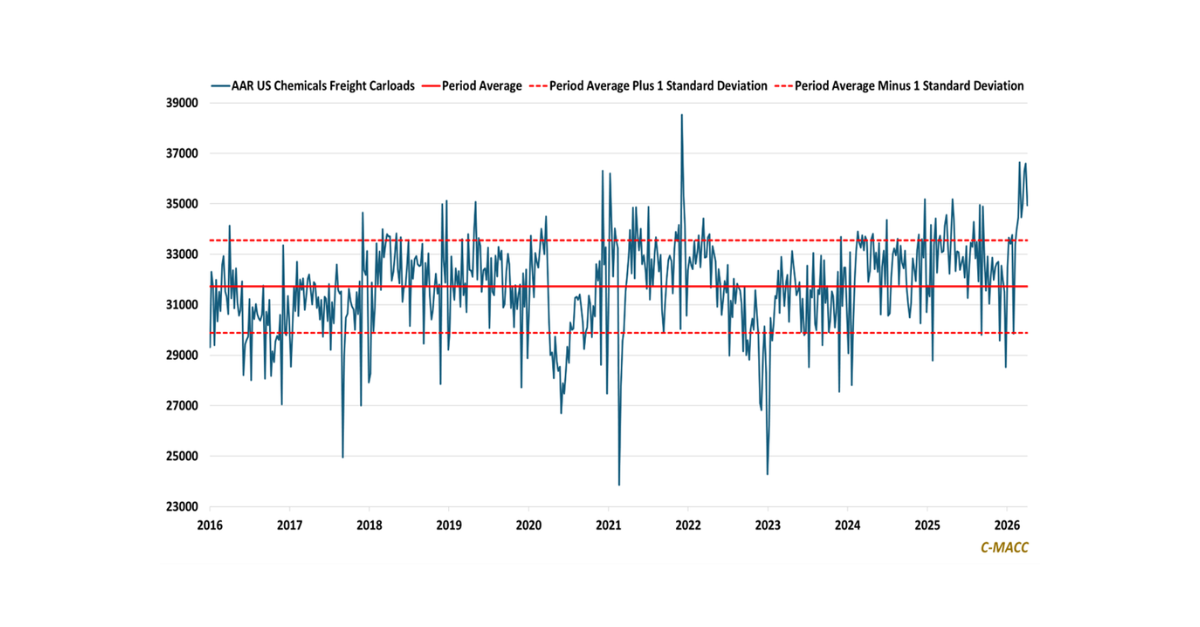

US chemical

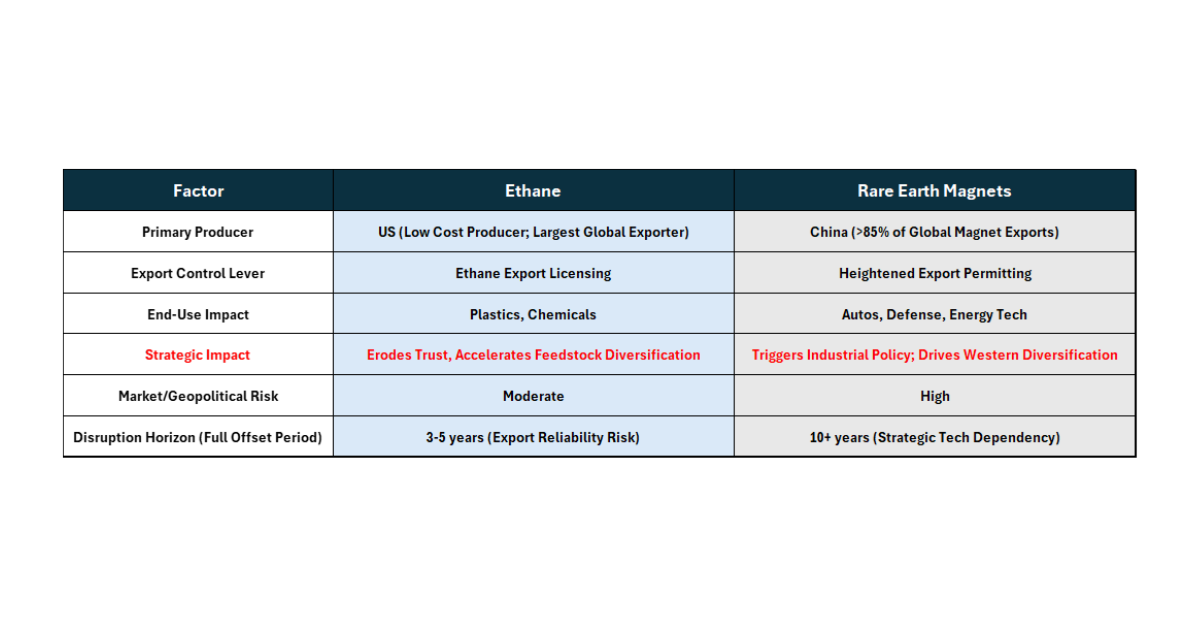

General Thoughts: In a world of tariffs, overcapacity, and policy shocks, global trade advances where structural cost leadership flows to relieve pressures on strained producers

General Thoughts: Well-capitalized firms will capitalize on policy-driven dislocations, as increasing resource nationalism fosters global supply chain diversification, rewarding scale, trust, and strategic optionality.

Supply

General Thoughts: Strategic capital, not tech or policy, is quietly redrawing global industrial maps as balance sheet-strong players invest through downturns to seize assets, shape

General Thoughts: Deep feedstock-to-chemical integration is not just a strategy—it is accelerating structural disruption and holds the potential to redraw the map of global industrial

General Thoughts: Weak global demand and oversupplied petrochemical markets have compressed profits for most, and it is putting some low-cost chemical producers in a difficult