Global Market Analysis

Supply Chains Break Faster Than They Build

Key Findings

- General Thoughts: Well-capitalized firms will capitalize on policy-driven dislocations, as increasing resource nationalism fosters global supply chain diversification, rewarding scale, trust, and strategic optionality.

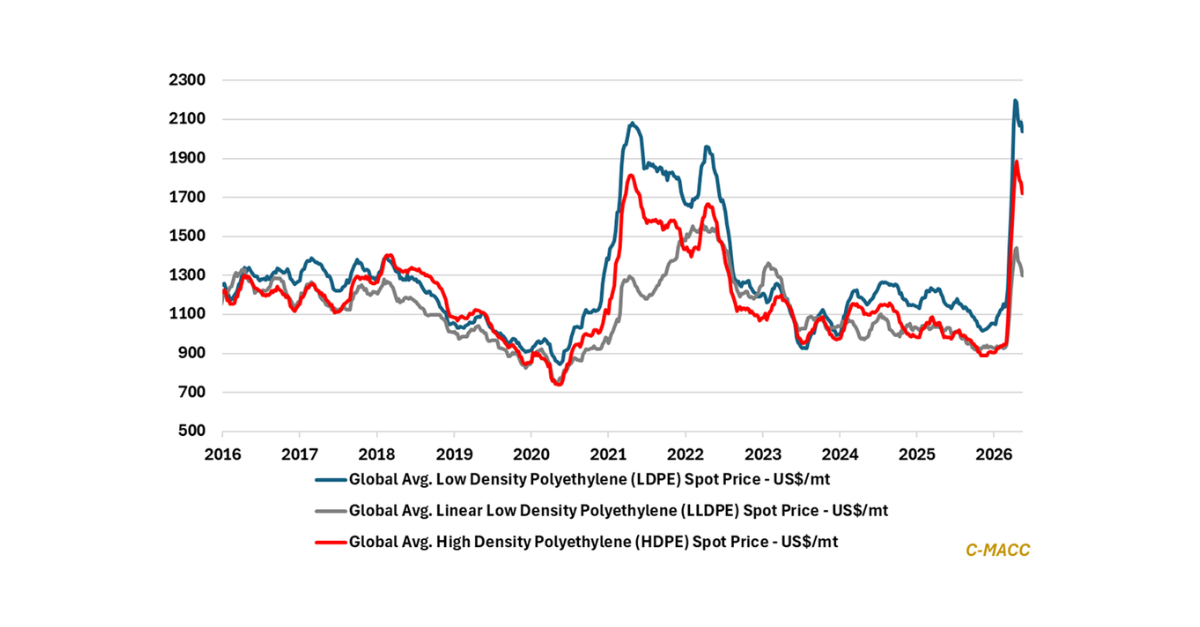

- Supply Chain/Commodities: LyondellBasell’s divestiture of legacy European assets signals a shift toward cost-advantaged growth, showing a broader industry trend toward flexible, return-optimized ownership models.

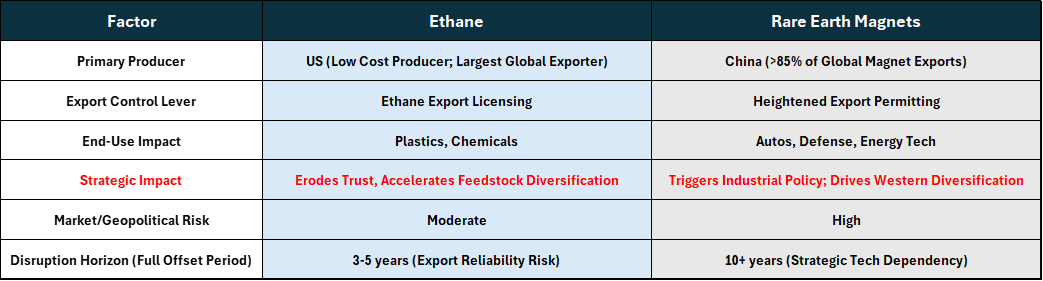

- Energy/Upstream: Export license uncertainty will likely prove transitory, but it undermines long-term confidence in US ethane exports, risking project delays, market share loss, and a structural erosion of US feedstock reliability.

- Sustainability/Energy Transition: China, the world’s largest emitter, is strategically exporting clean tech to lower-emitting countries, turning decarbonization goals into industrial leverage while reinforcing its global dominance.

- Downstream/Other Chemicals: Europe’s chemical downturn is structural, not cyclical, as weak demand and trade friction persist, while China’s rare earth curbs expose vulnerabilities and shift global competitiveness.

Exhibit 1: Short-Term Leverage, Long-Term Risk: Comparing US Ethane and China’s Rare Earth Dominance

Source: IEA, Company Reports, C-MACC Estimates, June 2025

See the PDF below for all charts, tables, and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!