Sunday Executive Summary

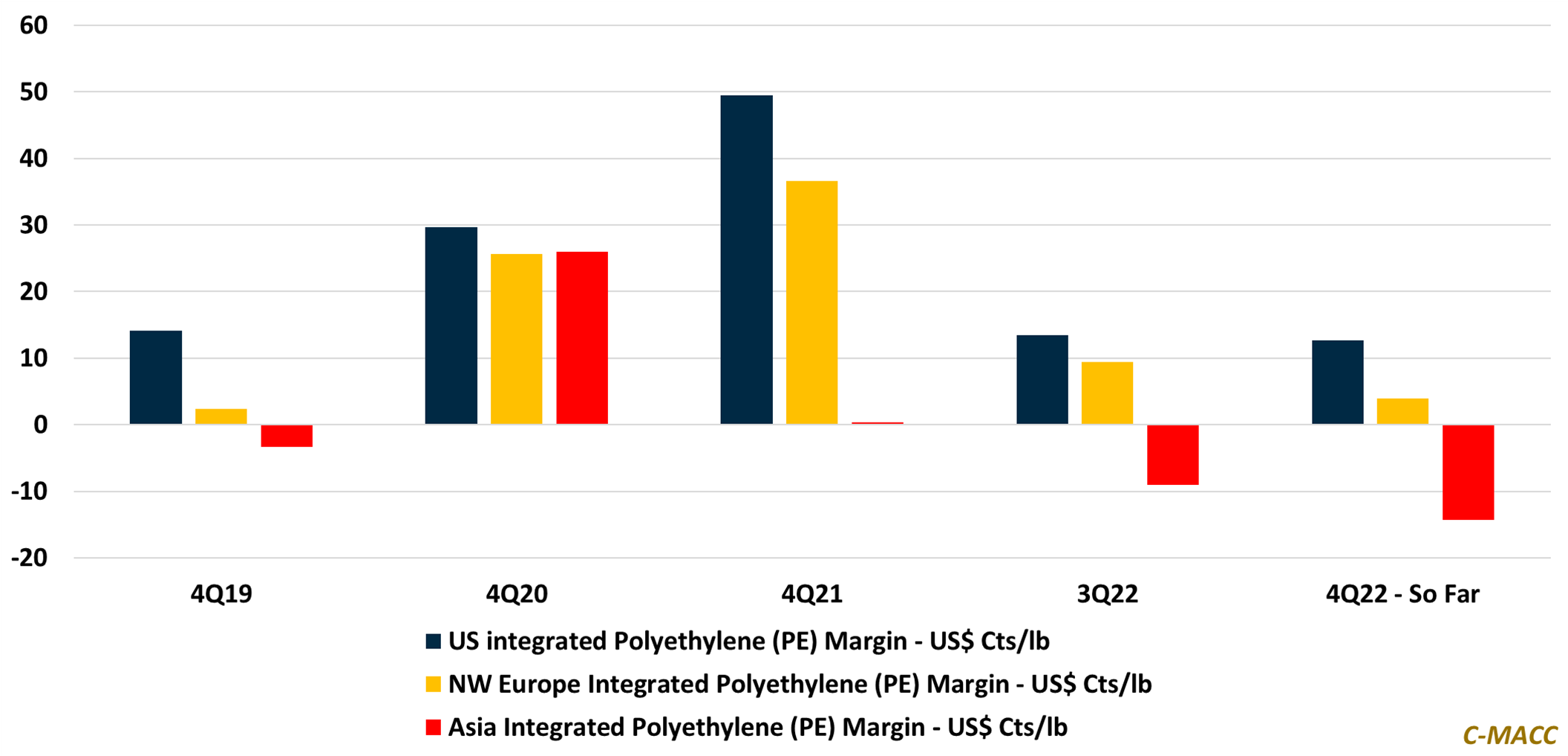

2023 is off to a bad start with low margins (but maybe not low enough) and global operating rates reflecting significant oversupply, which could worsen.

2023 is off to a bad start with low margins (but maybe not low enough) and global operating rates reflecting significant oversupply, which could worsen.

European chemical producer cutbacks will unlikely offset oversupplied Asian markets to support prices into 2023, limiting US cost benefits and forcing a battle from within.

While supply chain and cost pressure problems have eased, implying a production boost, the demand setting for most is not robust enough to support global