Global Market Analysis

The global chemical industry reflects too much capacity in most products – the steepening of the chemical cost curve is shifting production to low-cost regions,

The global chemical industry reflects too much capacity in most products – the steepening of the chemical cost curve is shifting production to low-cost regions,

US crop indicators point to higher prices and farmer incomes, while US commodity chemical indicators illustrate an oversupplied setting and rising margin pressure despite cost

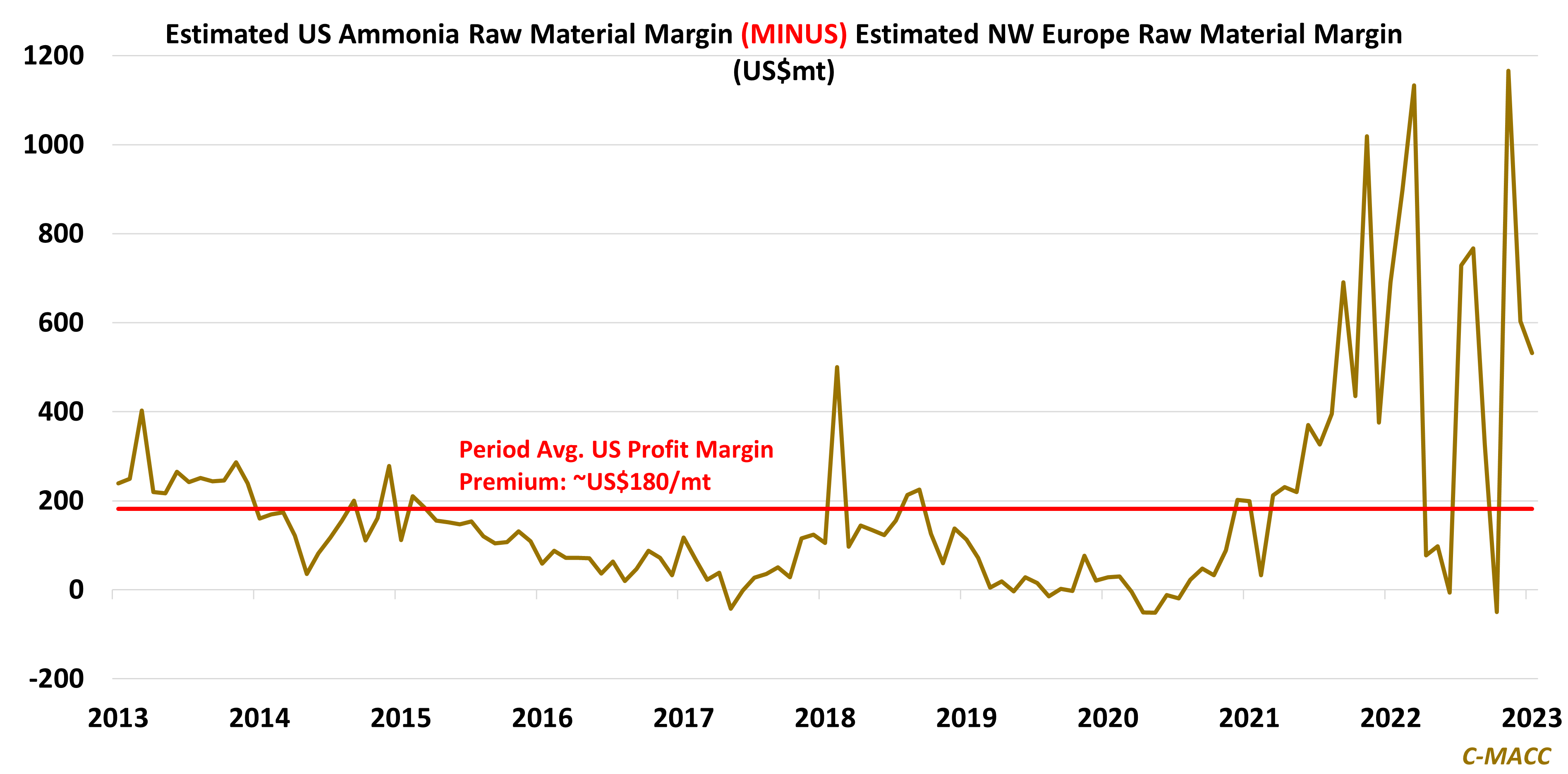

Global ammonia market fundamentals will likely stay much tighter during the next 10 years relative to the prior period, and we foresee a considerable shift

Commodity chemical producers lacking feedstock integration face difficult choices as the energy sector expands downstream, pressuring non-integrated chemical returns.

The North American petrochemical producer cost