Sunday Executive Summary

Structure, not scale, determines valuation, capital access, and resilience as oversupply, policy volatility, and higher rates punish complexity yet reward clarity, focus, optionality, disciplined execution,

Structure, not scale, determines valuation, capital access, and resilience as oversupply, policy volatility, and higher rates punish complexity yet reward clarity, focus, optionality, disciplined execution,

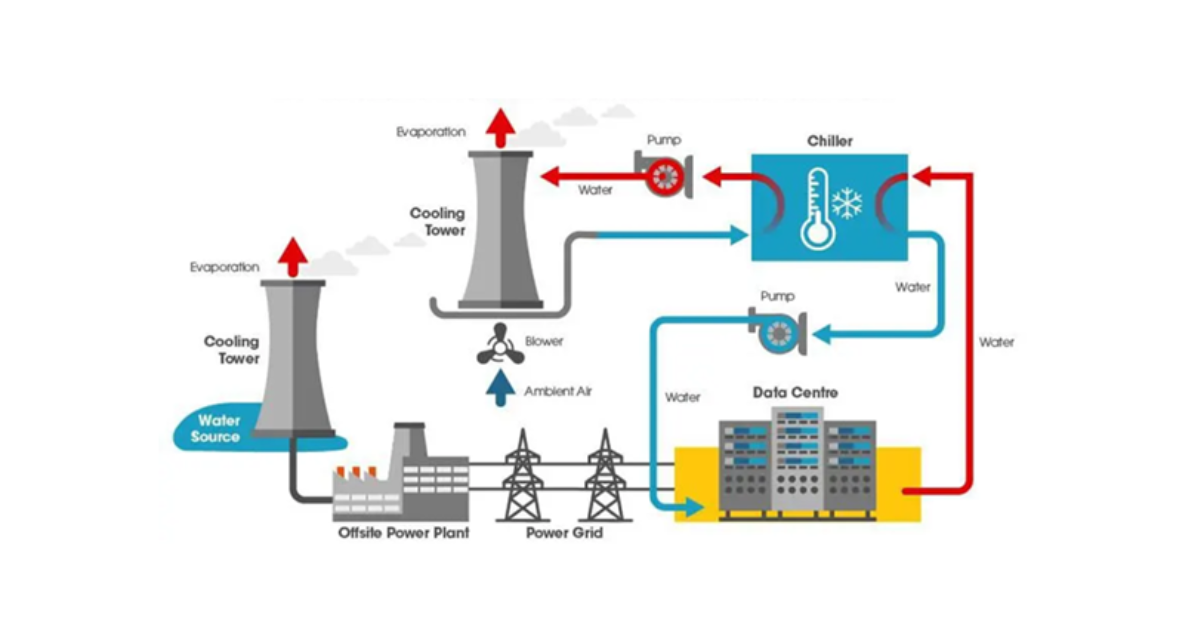

1st Topic of the Week: Water scarcity is AI’s hidden bottleneck, transforming data centers into hydrology-dependent assets. Will industry leaders secure resilient water strategies or

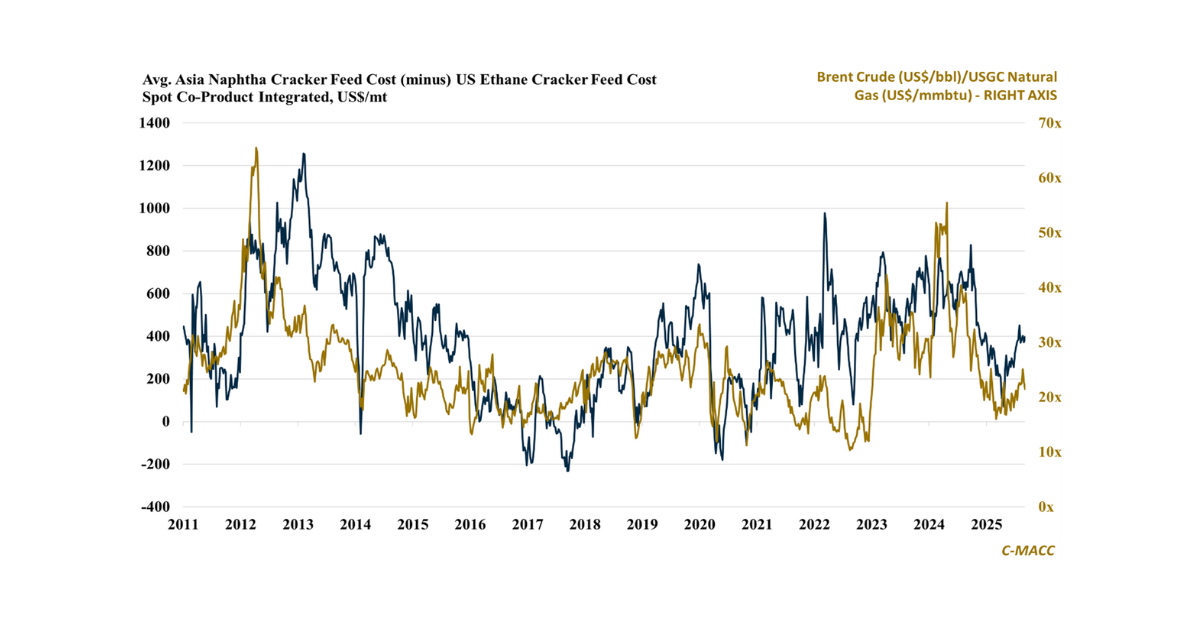

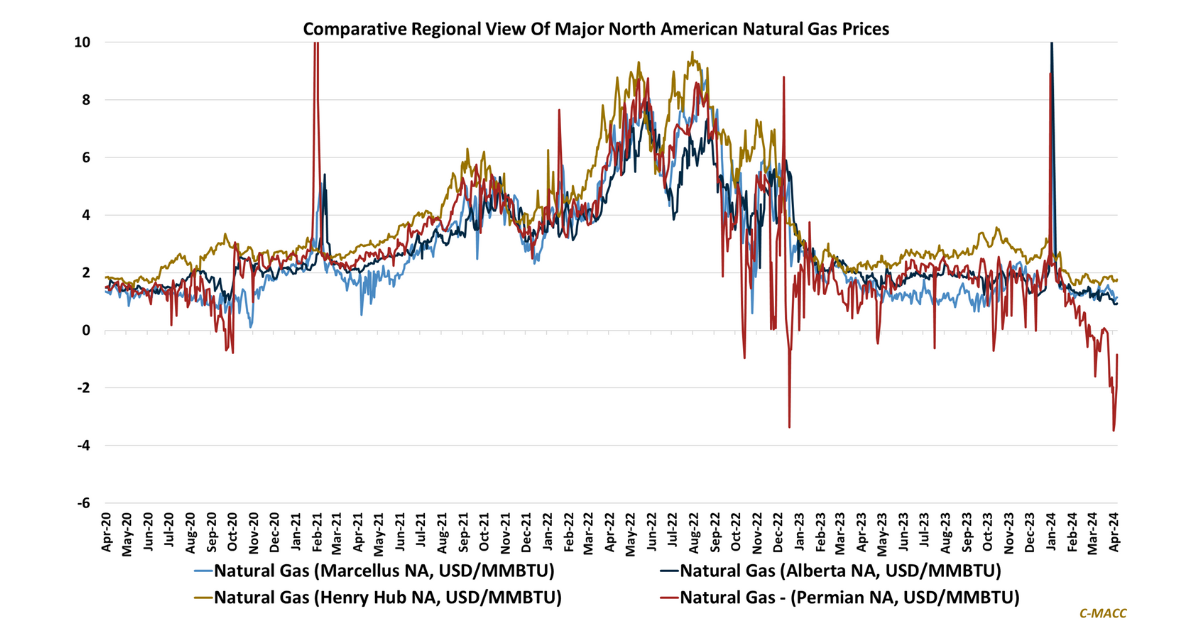

General Thoughts: Cheap North American natural gas is not a new benefit for its chemical industry, but its benefits have become pronounced amid feedstock and

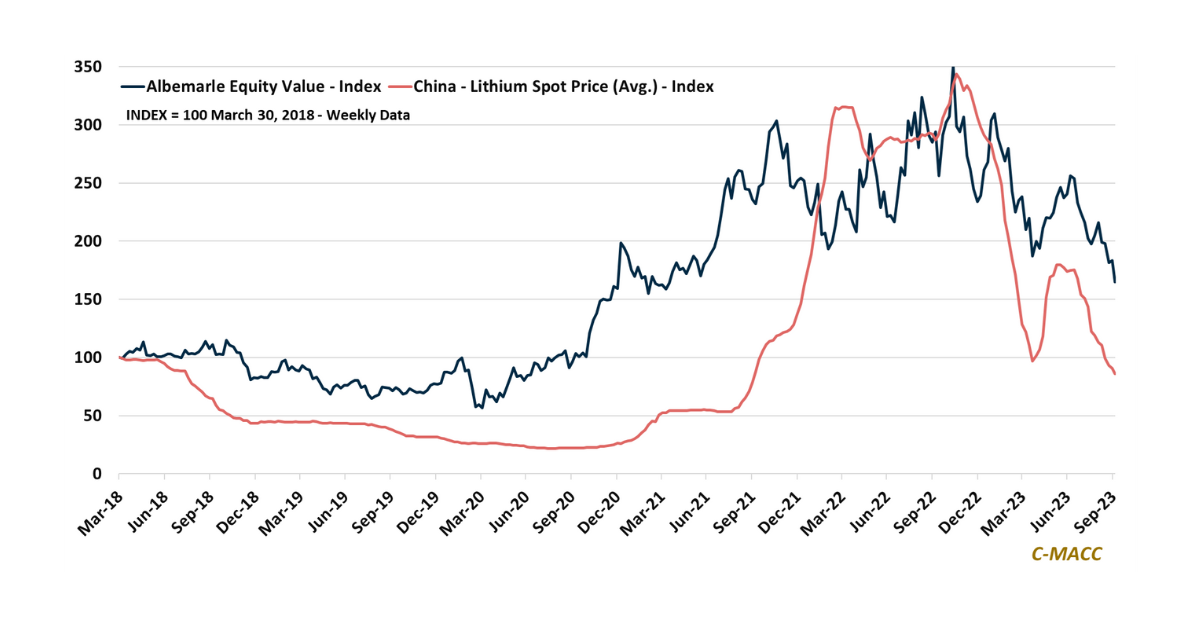

After the commodity price surge of 2021-2022, many producer equity values have followed their respective commodity prices lower in 2023 – an abrupt rebound in

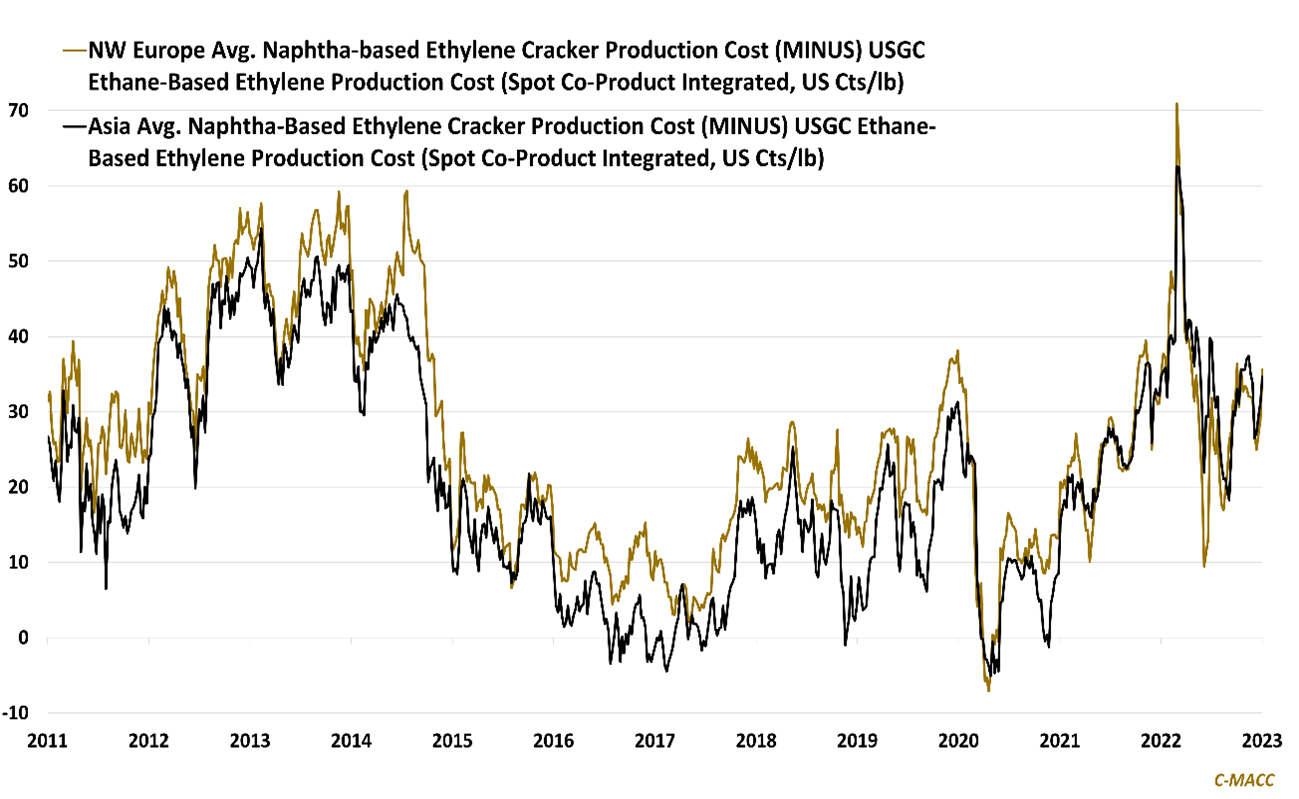

Strength in North American chemical production margins due to falling feedstock costs relative to those abroad is boosting energy sector awareness of its downstream value

Our theme around the possible need for backward integration for all basic chemical producers as energy transition evolves was validated by INEOS this week.

INEOS

European chemical producers face the challenges of a global production cost disadvantage and a generally mature consumer growth profile, spurring some to make aggressive strategic

Recent global chemical production cost movements and US price support have lifted domestic market sentiment, but our study suggests low run rates will limit the

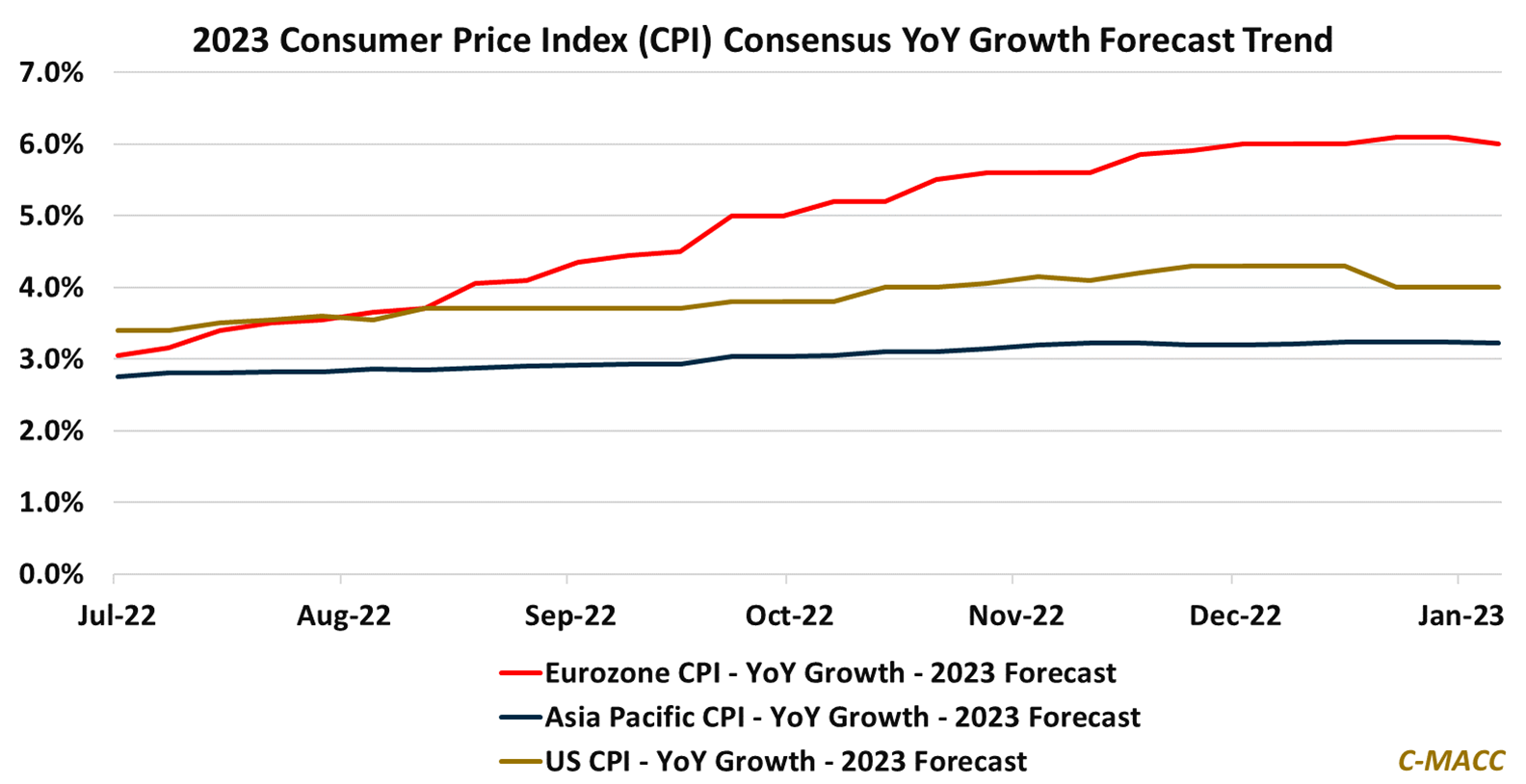

Western market consumers faced much greater price inflation than those in Asia in 2022, and most expect it to occur again in 2023. A plus

2023 is off to a bad start with low margins (but maybe not low enough) and global operating rates reflecting significant oversupply, which could worsen.