Global Market Analysis

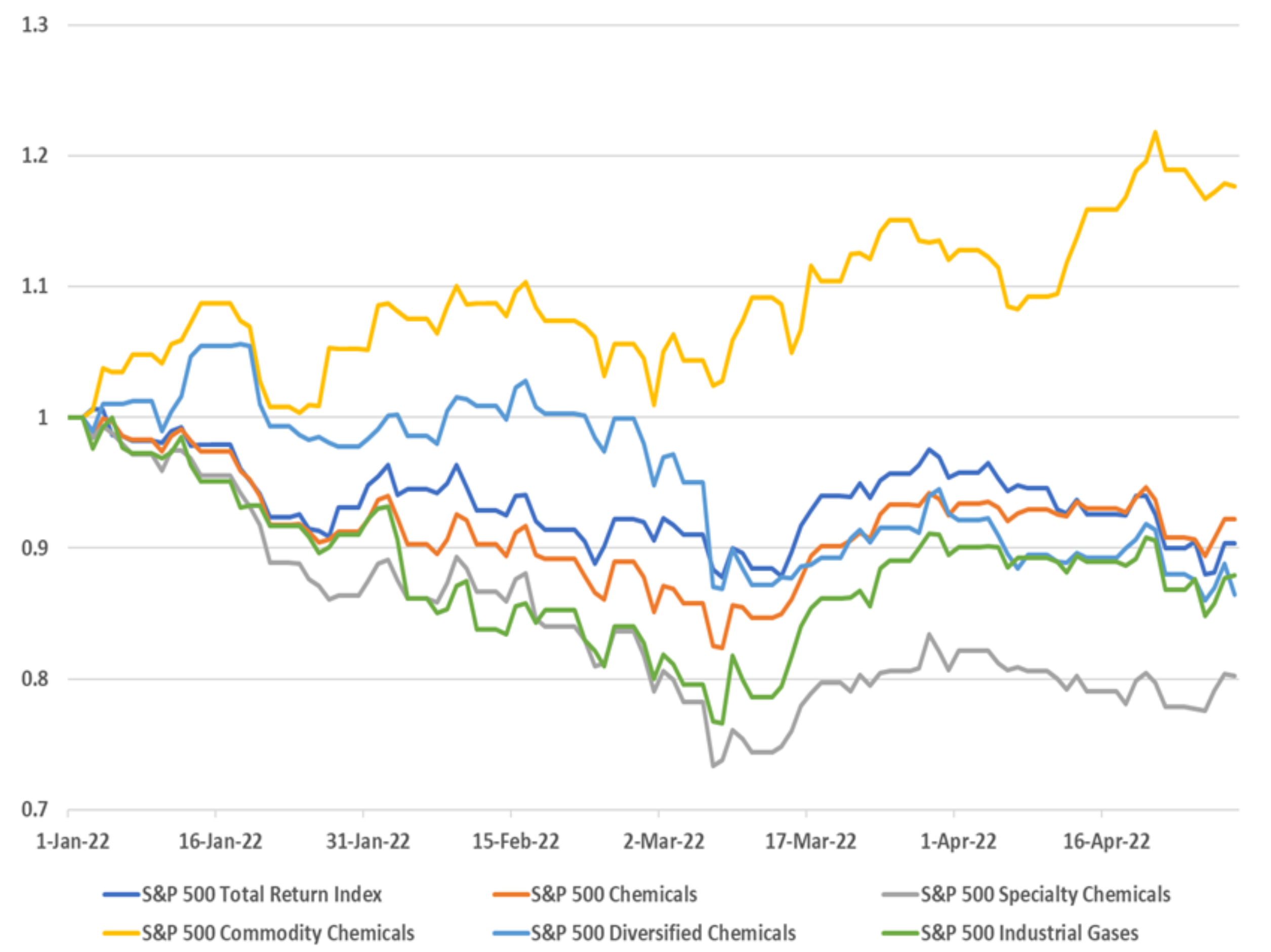

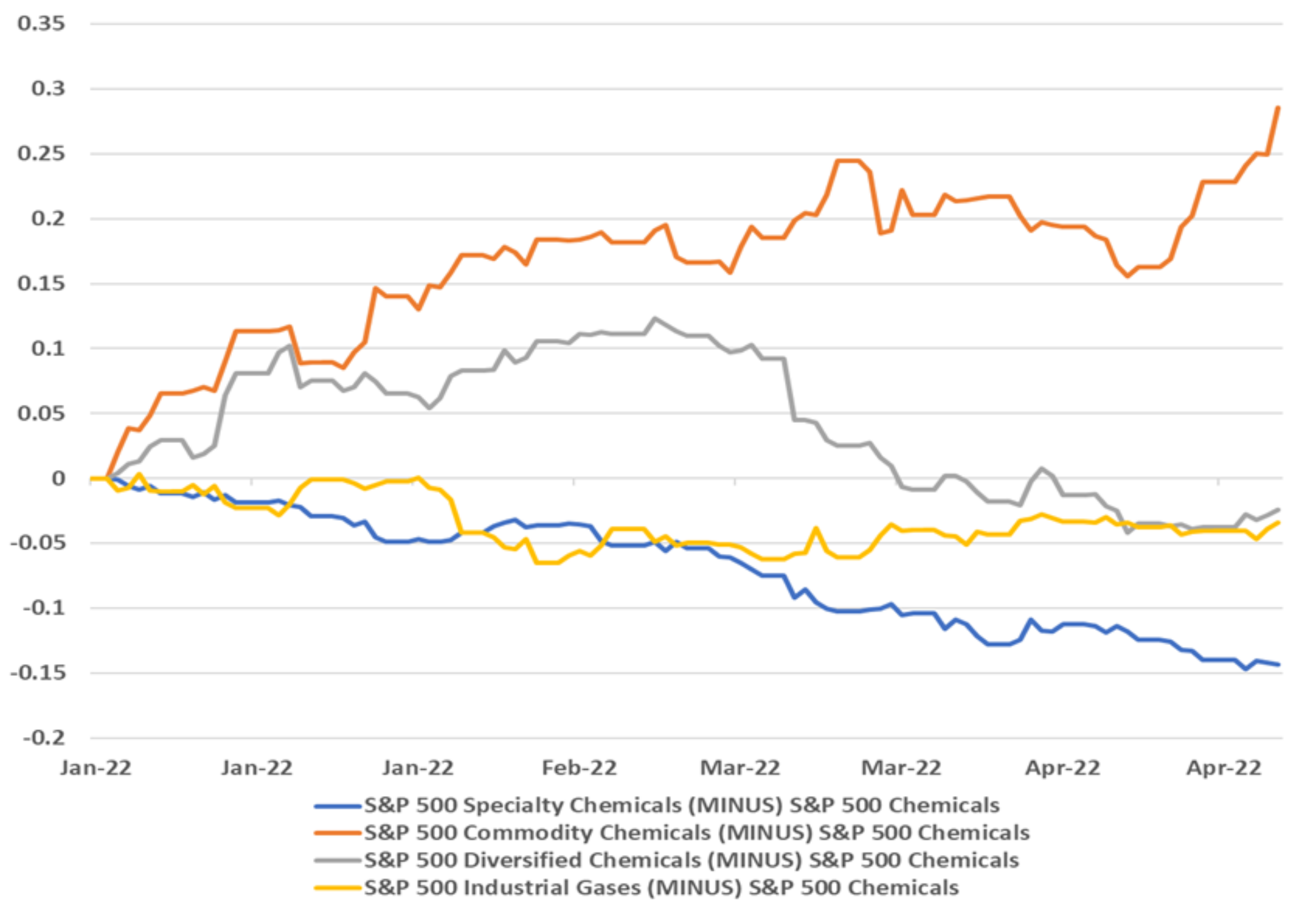

US commodity chemicals outperformed YTD, but we think a price/margin pullback among these producers is likely in 2H22. We argue that US specialty sub-sector equities

US commodity chemicals outperformed YTD, but we think a price/margin pullback among these producers is likely in 2H22. We argue that US specialty sub-sector equities

Chemical sector 1Q22 reports broadly beat expectations but reflect limited growth investment amid considerable global uncertainty. Efforts to further lift prices are mounting, and so

The wind power industry is in significant trouble and the last couple of years have been plagued with negative revisions, despite a strong demand outlook.<br

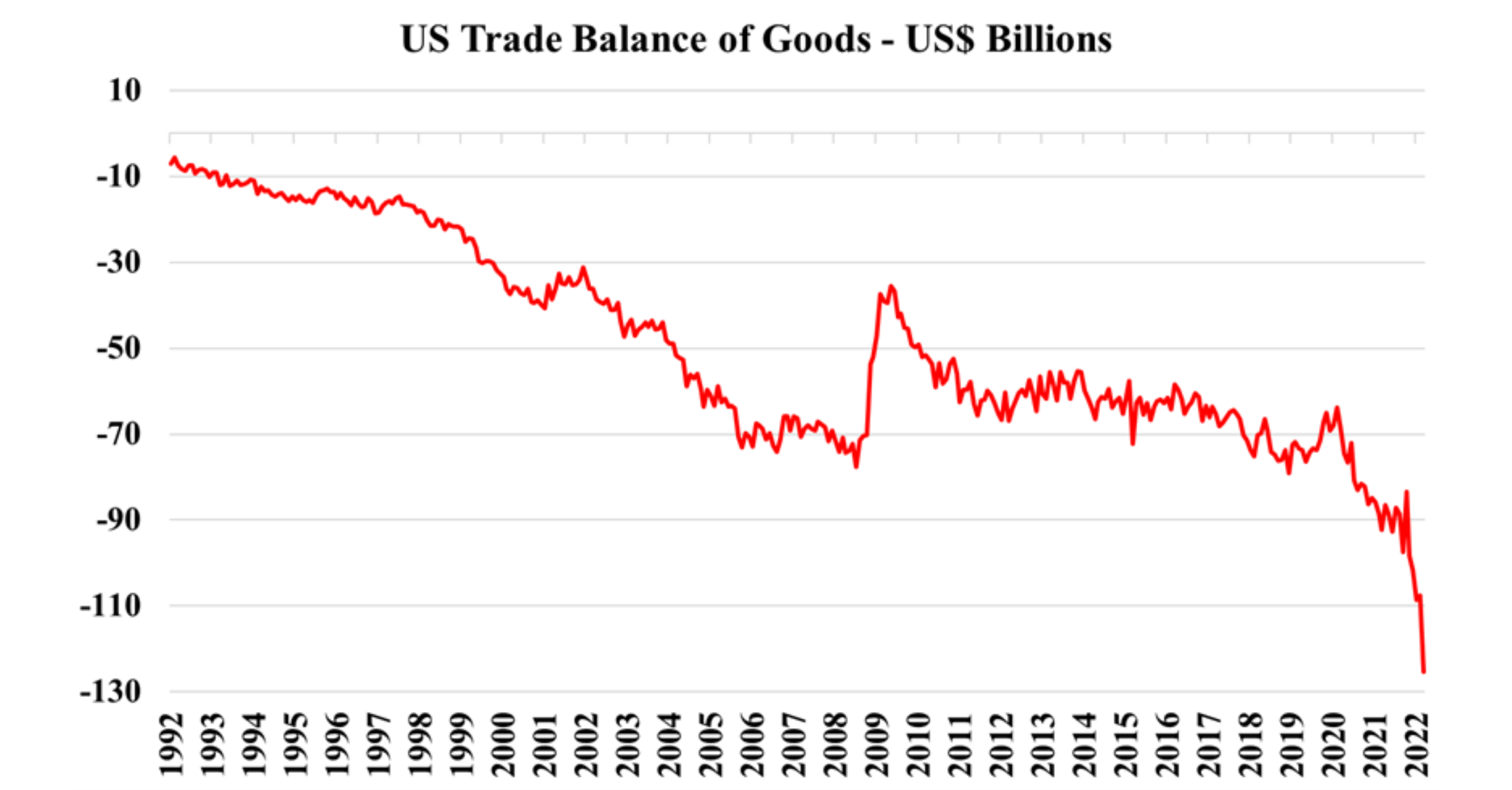

The US trade deficit for goods reached a record level in March, as high prices lured products from abroad. We discuss a few factors working

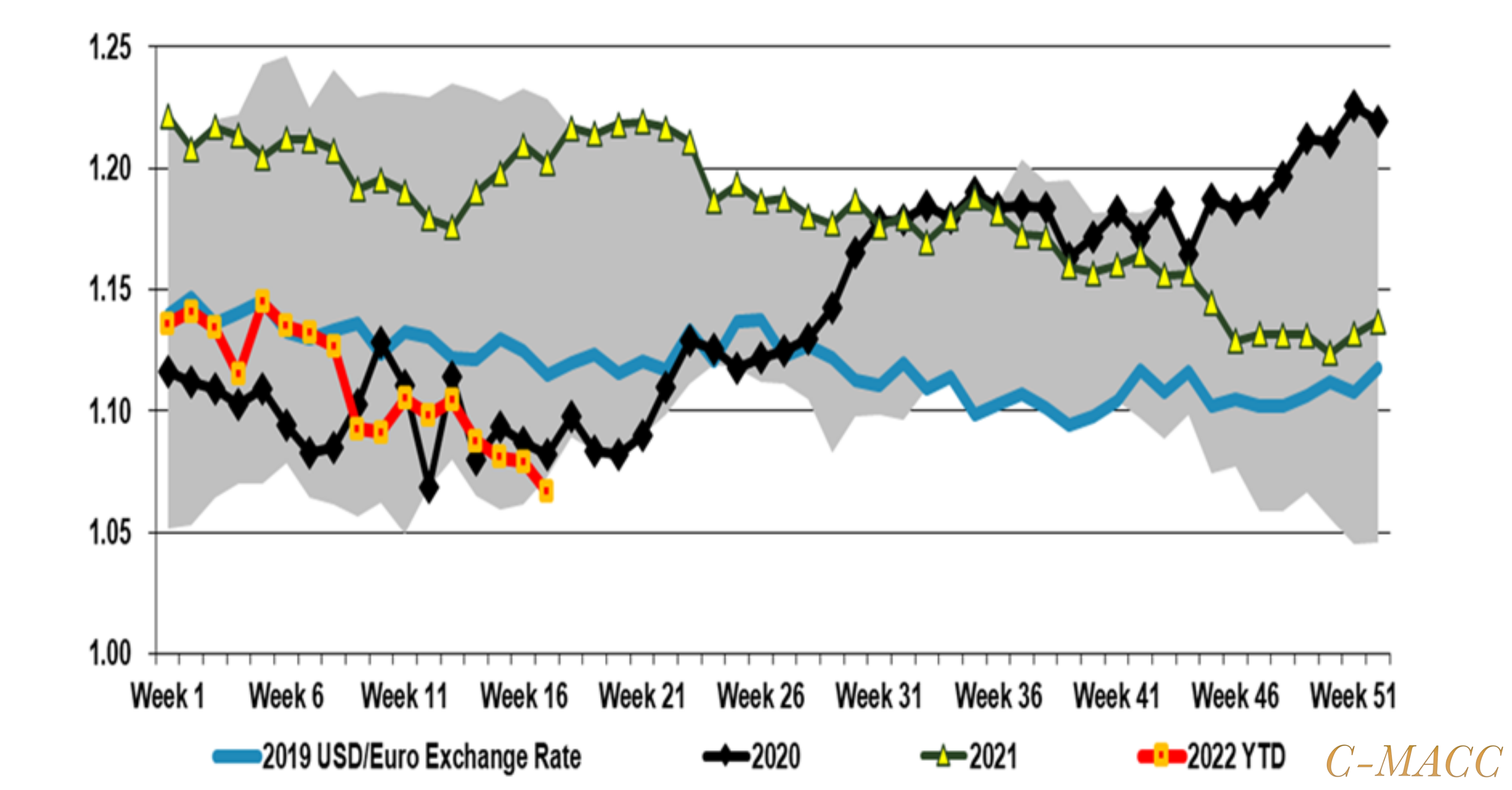

moderation. Macro indicators and our other analysis and relevant data points lift our concerns.

We highlight pertinent energy, chemical, and other corporate updates (e.g.,

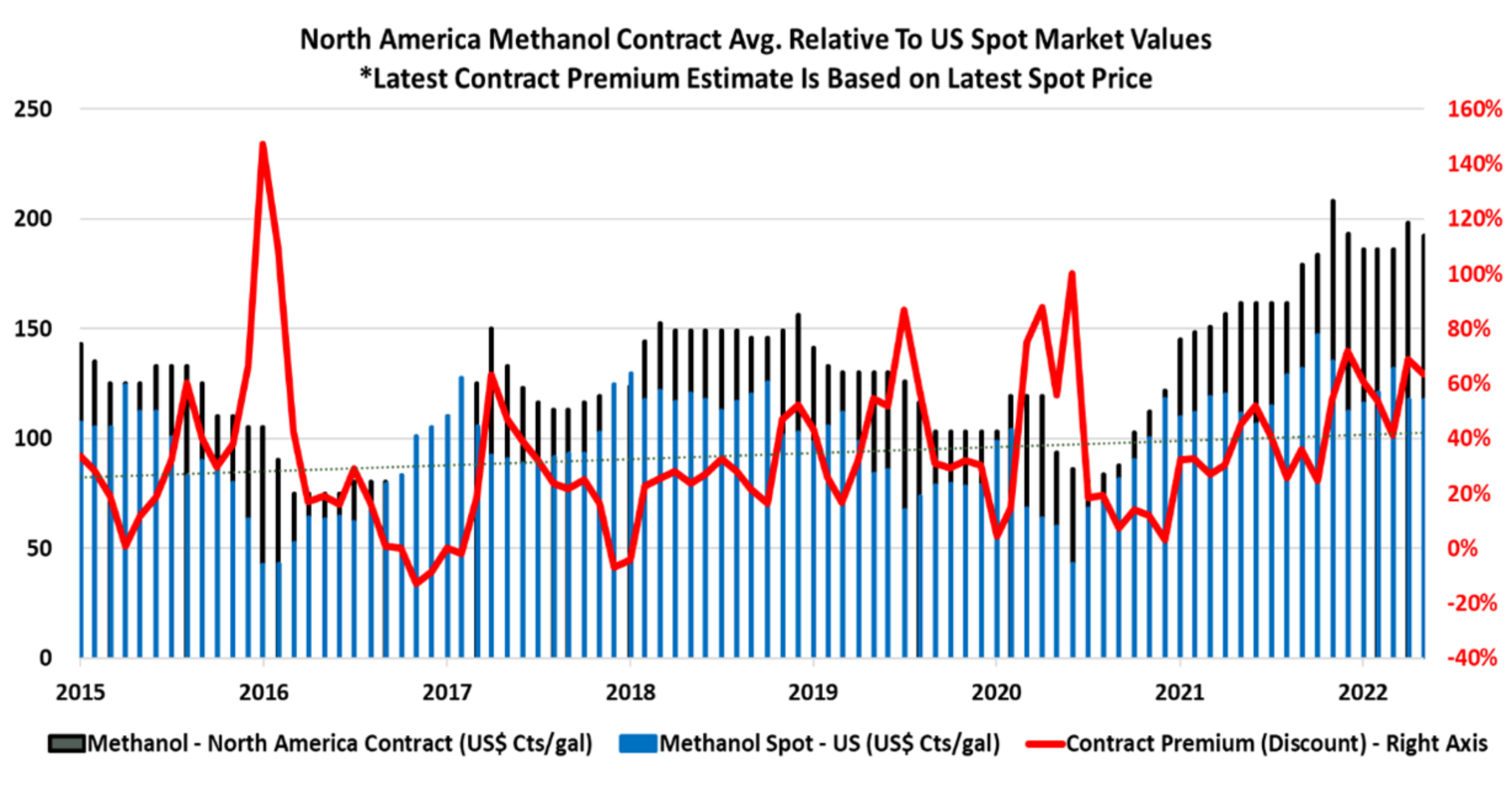

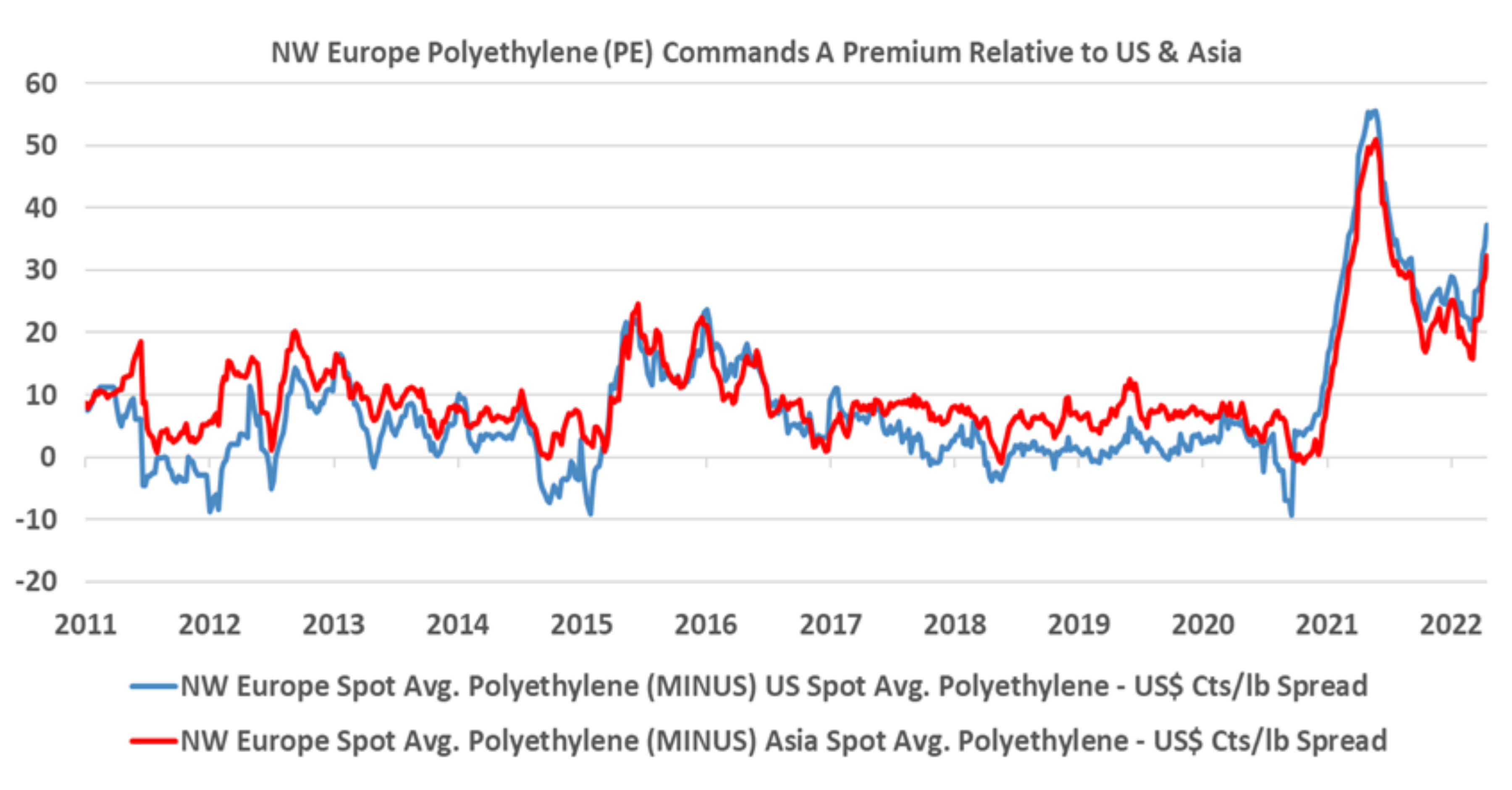

Western polymer price premiums reflect strength WoW, as global supply chain, logistic, and feedstock issues continue to favor regional disconnects. We foresee a 2H22 loosening

The global energy landscape significantly shifted in mid-1Q22, which has resulted in sector followers looking past many better than expected corporate 1Q results to 2Q

US commodity chemicals outperformed YTD, and 1H22 profit will likely beat expectations. A 2H22 commodity price/margin pullback remains a risk, but we argue that this

The route to renewable fuels and materials is not as simple as using a plant-based input, and carbon sources and sinks matter. The need for

Global market indicators remain favorable for US commodity chemical producers relative to peers abroad. We discuss 1H22 chemical price (and margin) trends and highlight factors