Global Market Analysis

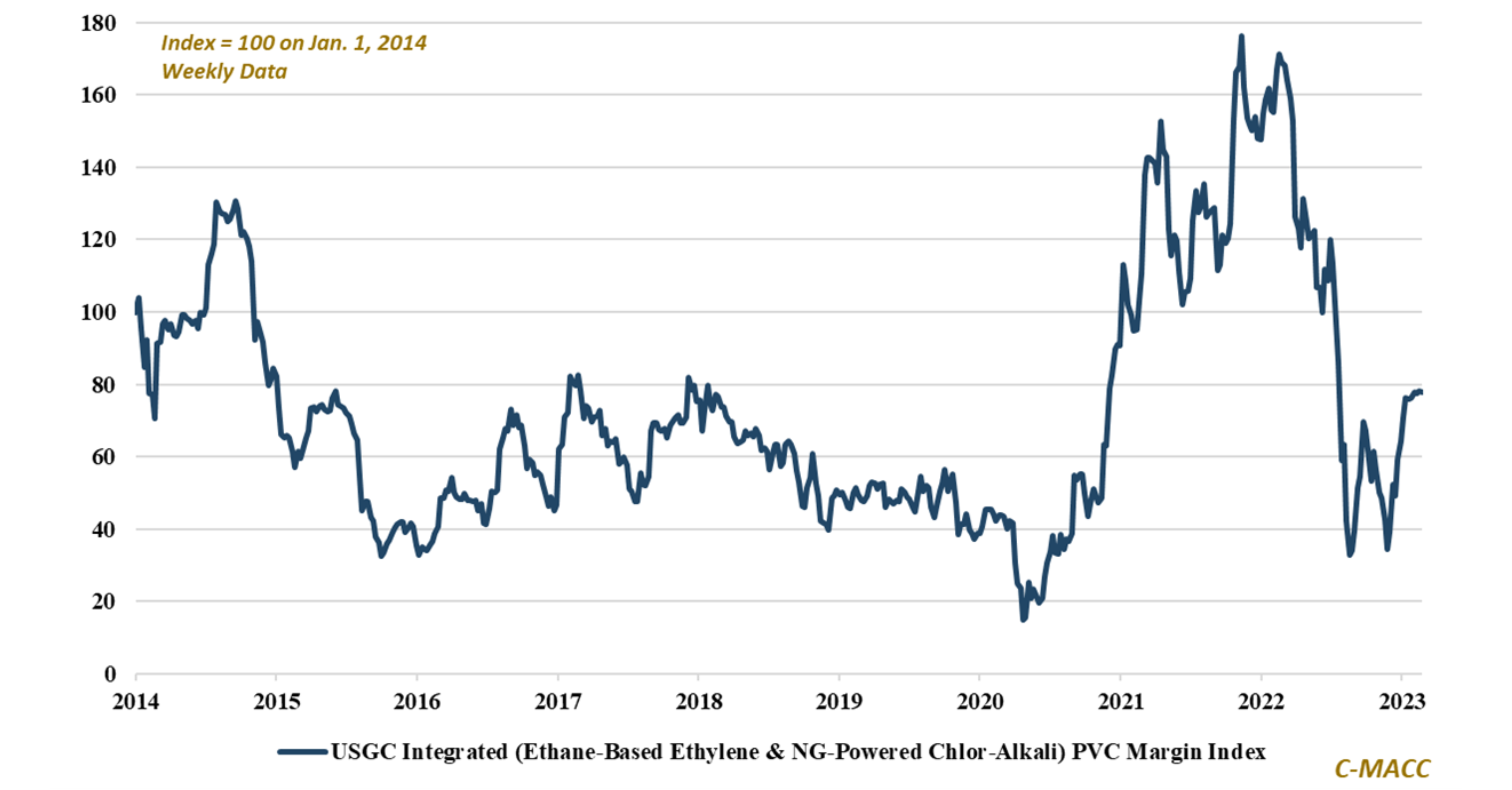

US Chlor-Vinyl margins have increased from 4Q22 lows in 1Q23, and we discuss Oxy views of this product chain in 2023 – we share a

US Chlor-Vinyl margins have increased from 4Q22 lows in 1Q23, and we discuss Oxy views of this product chain in 2023 – we share a

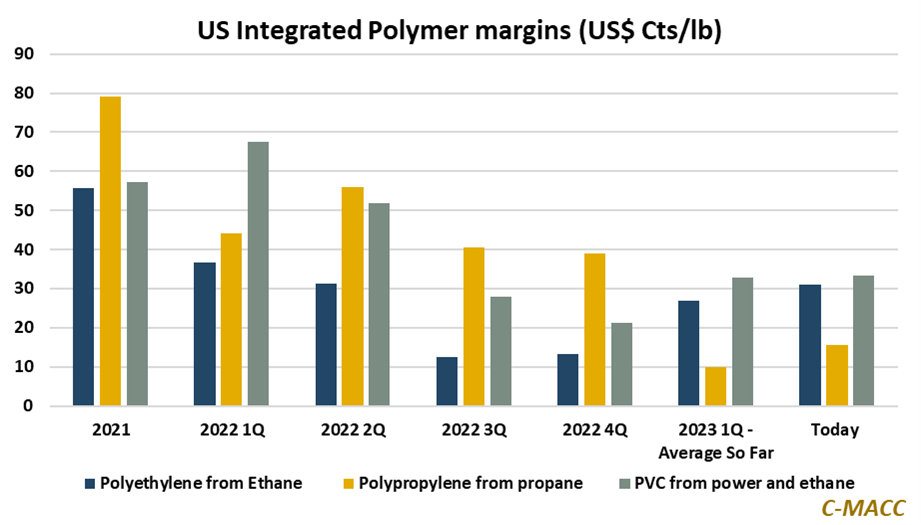

North American integrated polymer margins have broadly increased relative to 1Q23 lows – we flag US polyethylene (PE) and polyvinyl chloride (PVC) margins are higher

Our theme around the possible need for backward integration for all basic chemical producers as energy transition evolves was validated by INEOS this week.

INEOS

European chemical producers face the challenges of a global production cost disadvantage and a generally mature consumer growth profile, spurring some to make aggressive strategic

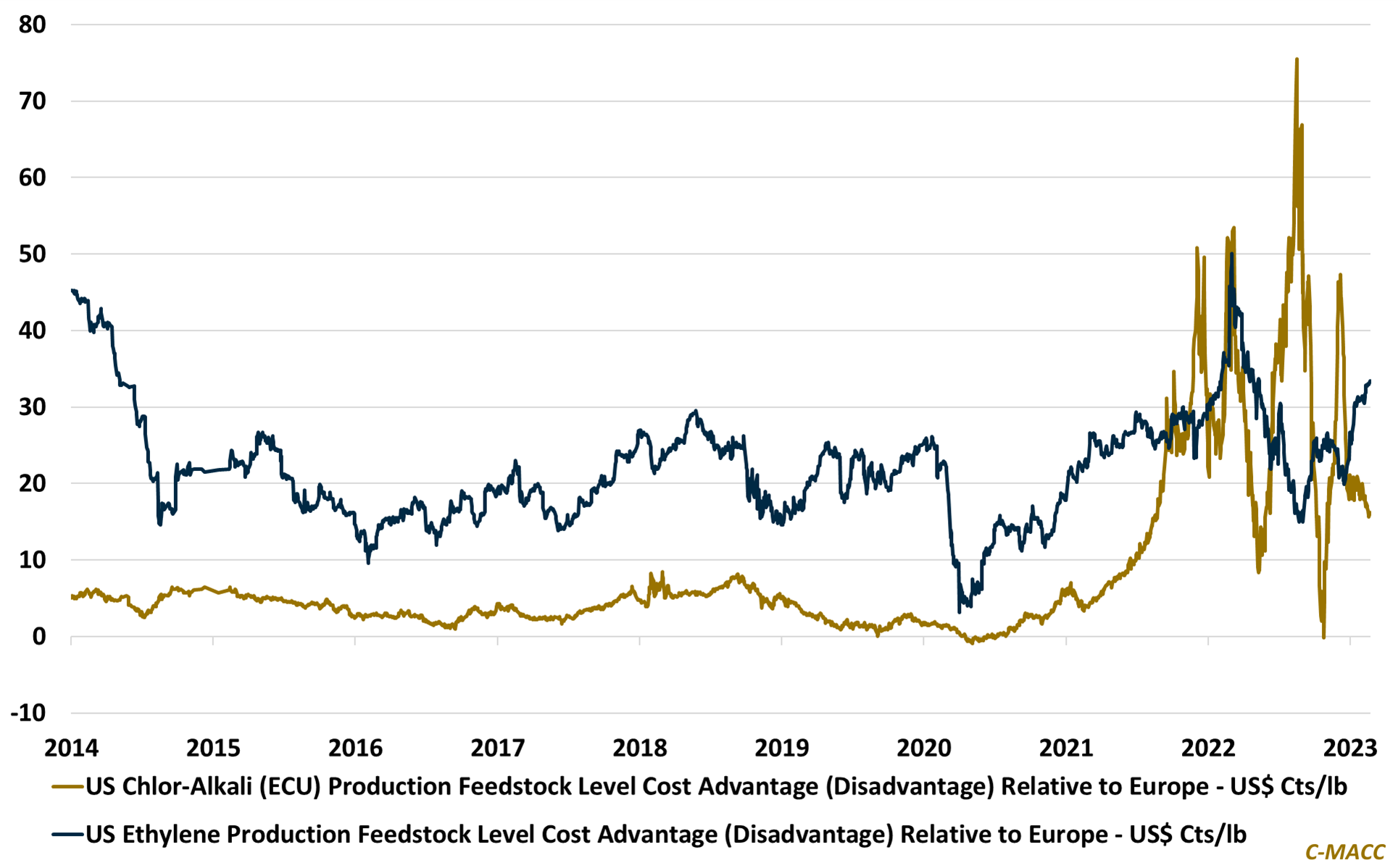

The North American chemical producer cost advantage remains significant relative to overseas peers, as is the case for domestic energy producers, suggesting sizable integration benefits.

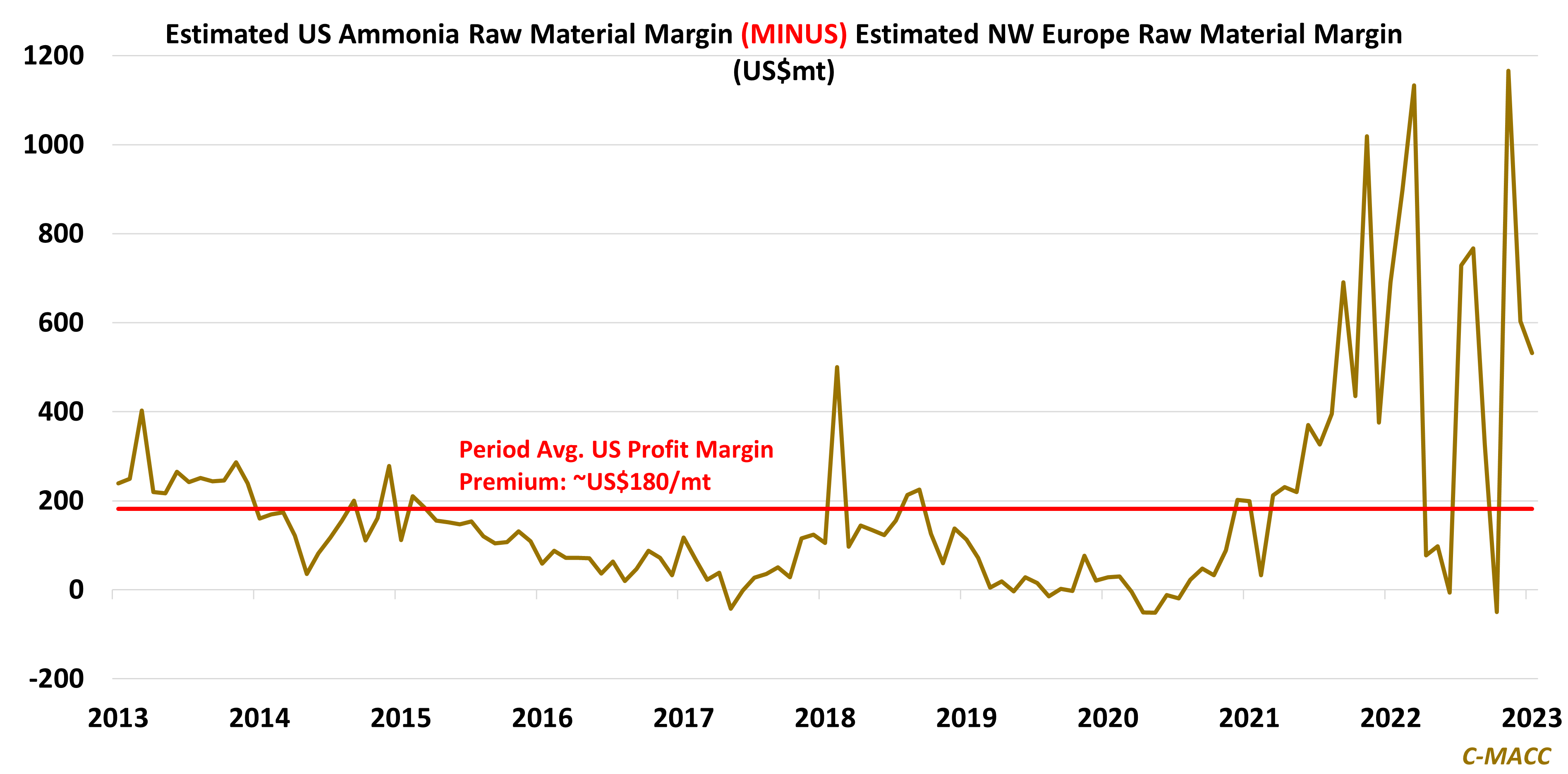

Ammonia leads again, following earning reports from the existing producers and more speculation around who will enter the market – our expectations are high.

Current

We highlight US cost advantages in Chlor-alkali and ethylene relative to Europe (and Asia), and why we take a constructive view of domestic vinyl producers,

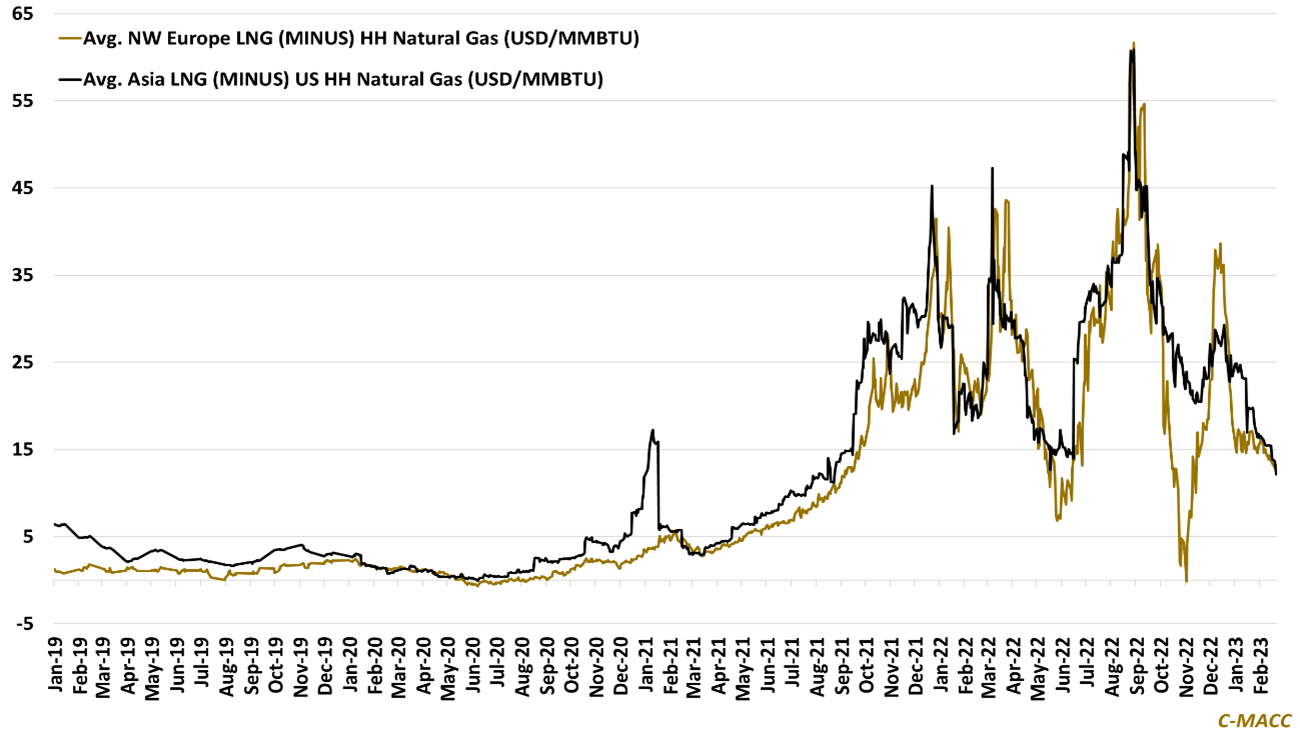

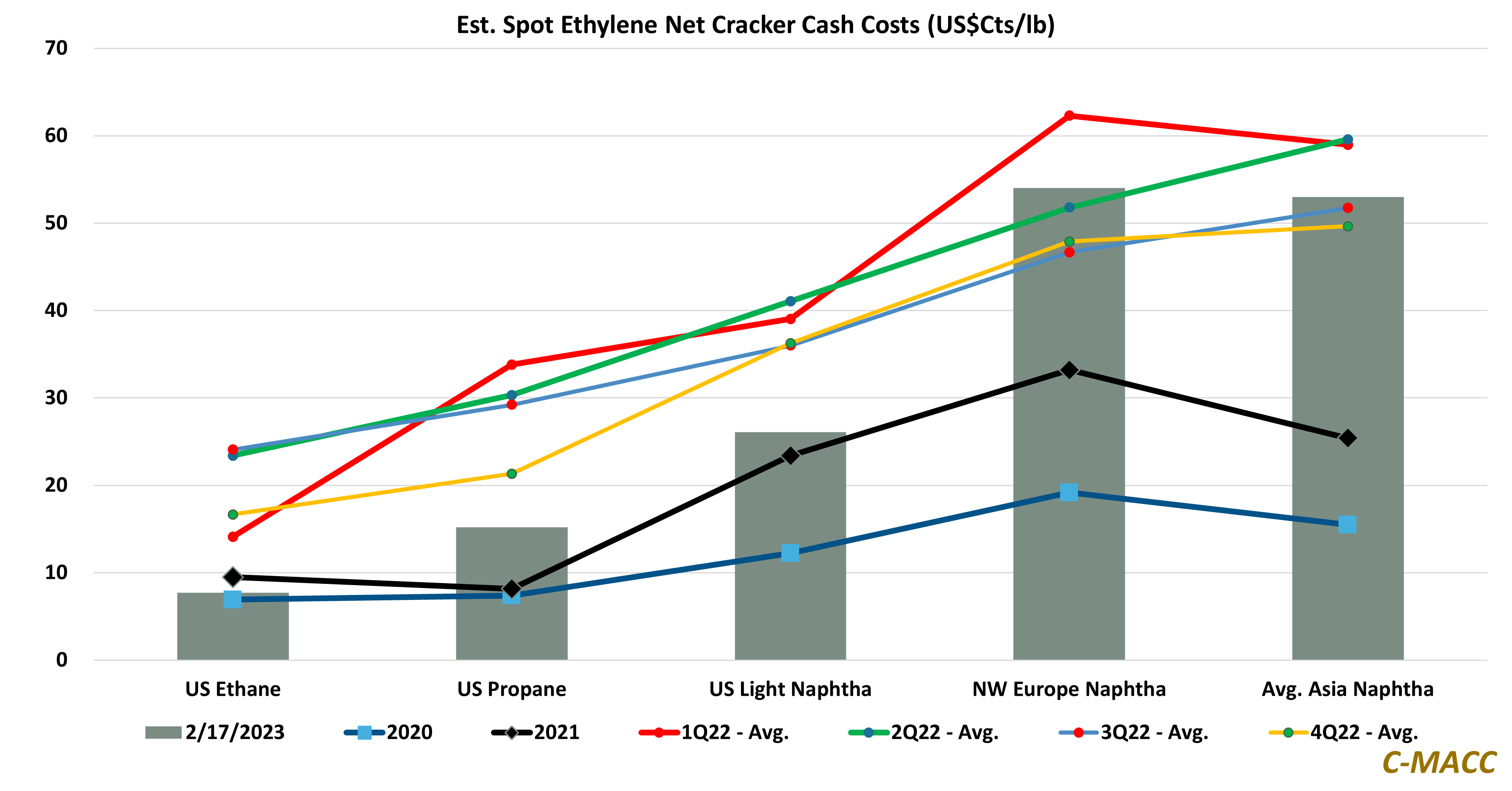

The European petrochemical industry is most at risk of further shutdown from North American competition – the production cost curve supports this move, and producers

Western consumers will likely face another year of higher prices relative to Asia, but it puts European producers most at risk with its cost disadvantage

Global ammonia market fundamentals will likely stay much tighter during the next 10 years relative to the prior period, and we foresee a considerable shift